Small business liability insurance stands as the financial shield between your company and potential lawsuits that could bankrupt your operation overnight.

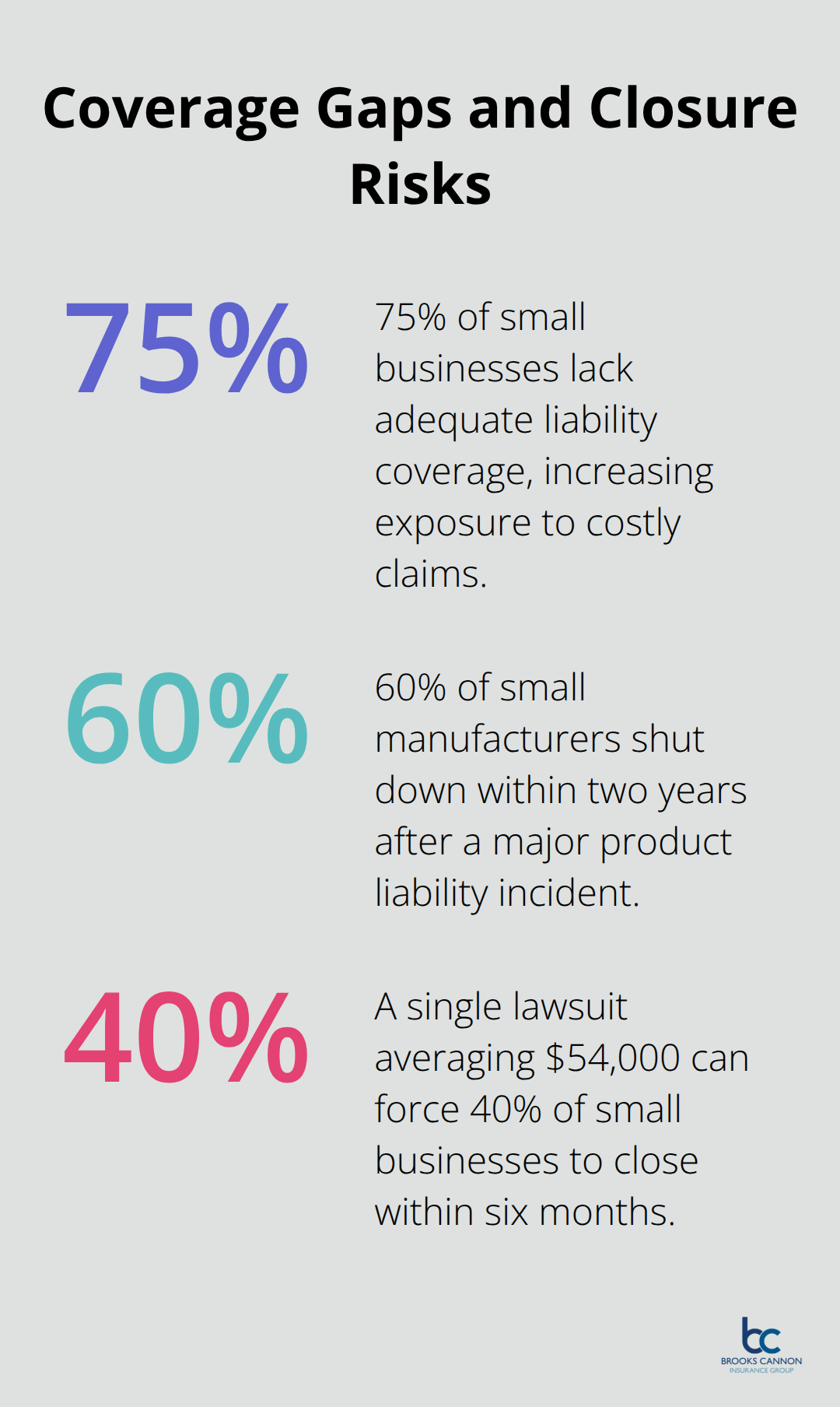

We at Brooks Cannon Insurance Group see Dallas entrepreneurs face liability claims daily – from slip-and-fall accidents to product defects. Without proper coverage, a single lawsuit averaging $54,000 can force 40% of small businesses to close permanently within six months.

Understanding Small Business Liability Insurance

What General Liability Insurance Covers

General liability insurance protects your business against third-party claims for bodily injury, property damage, and personal injury lawsuits. This coverage handles medical expenses when customers slip on wet floors, legal fees when your employee accidentally damages client property, and settlements for advertising injury claims. The Insurance Information Institute reports that 75% of small businesses lack adequate liability coverage, which leaves them vulnerable to claims that average $15,000 to $50,000 per incident.

Professional Services Need Different Protection

Professional liability insurance covers errors and omissions in your services, while general liability handles physical accidents and property damage. Service-based businesses face different risks than retail operations. A marketing consultant who faces a lawsuit for campaign failures needs professional liability, not general coverage. However, that same consultant needs general liability when clients visit their office and could slip on stairs. Workers compensation claims cost businesses an average of $41,000 per incident (according to the National Safety Council), which makes this coverage mandatory in most states once you hire employees.

The Claims That Close Businesses Fast

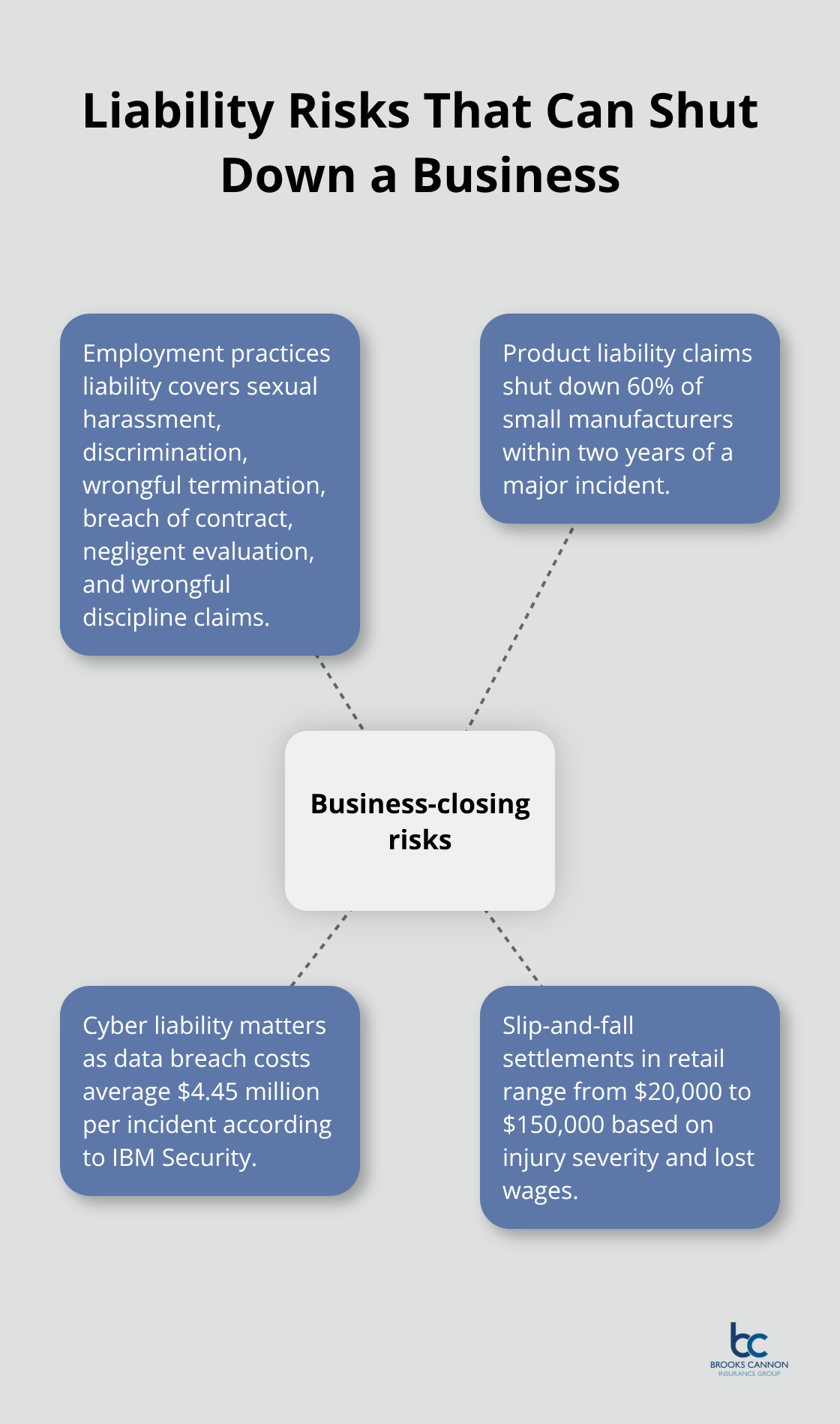

Employment practices liability covers sexual harassment, discrimination, wrongful termination, breach of contract, negligent evaluation, and wrongful discipline claims. Product liability claims shut down 60% of small manufacturers within two years of a major incident. Cyber liability becomes essential as data breach costs average $4.45 million per incident according to IBM Security. Most devastating are slip-and-fall claims in retail environments, where settlements range from $20,000 to $150,000 based on injury severity and lost wages.

These liability exposures multiply when you consider how different coverage types work together to protect your specific business operations.

Essential Coverage Types for Small Businesses

Bodily Injury and Property Damage Protection

Bodily injury protection covers medical expenses, lost wages, and legal costs when customers or visitors get hurt on your property. The National Safety Council reports that workplace injuries cost small businesses an average of $42,000 per claim, but customer injuries on business premises average $33,000 per incident. Retail businesses face the highest risk, with slip-and-fall claims being a significant portion of premises liability lawsuits.

Manufacturing operations see different patterns – equipment-related injuries average $67,000 per claim according to OSHA data. Property damage coverage handles situations where your business operations damage someone else’s property, with average claims that range from $8,000 to $25,000 per incident.

Product Liability and Completed Operations Coverage

Product liability coverage becomes mandatory once you manufacture, distribute, or sell physical products. The Consumer Product Safety Commission tracks over 15,000 product-related injuries annually that result in lawsuits. Completed operations coverage protects service businesses after work finishes – a plumber whose repair fails months later needs this protection.

These policies protect against defects that cause harm after products leave your control or services conclude. Manufacturing defects, design flaws, and inadequate warnings all trigger product liability claims that average $45,000 per incident but can reach millions in severe cases.

Personal and Advertising Injury Protection

Personal injury coverage handles non-physical harm like false imprisonment, wrongful eviction, or invasion of privacy claims. Advertising injury protection covers trademark infringement, copyright violations, and defamation in your marketing materials. These claims average $28,000 per incident but can reach six figures when intellectual property violations occur.

Dallas service businesses particularly need this coverage as social media marketing increases exposure to advertising injury claims through competitor disputes and customer review conflicts (especially in competitive markets like real estate and professional services).

The cost of these coverage types varies significantly based on your industry risk level and business size, which directly impacts your business insurance premium calculations.

Cost Factors and Money-Saving Strategies

Industry Risk Level Impact on Premiums

Construction companies pay 300% more for liability insurance than office-based consultants because construction workers face significant workplace injury risks. Restaurants pay double what accounting firms spend due to slip-and-fall risks and food-related illness claims. Manufacturing operations see premiums spike when they handle hazardous materials – chemical manufacturers pay rates that start at $3,200 annually while software companies average $680 for the same coverage limits.

Healthcare practices face malpractice exposure that pushes professional liability costs to $8,000-$15,000 annually. Marketing consultants pay $600-$1,200 for similar protection. Insurance carriers assess your specific industry risks and price policies accordingly.

Business Size and Revenue Considerations

Insurance carriers calculate premiums based on your annual revenue because larger businesses face greater exposure. Companies that earn under $100,000 annually pay base rates, but businesses that generate $500,000 see premiums increase by 40-60%. Million-dollar revenue companies face rate jumps of 100-150% over smaller operations.

The National Association of Insurance Commissioners data shows businesses with 10+ employees pay 85% more than solo operations due to increased liability exposure. Your payroll size directly correlates with premium costs because more employees create more potential liability scenarios.

Bundling Policies and Deductible Options

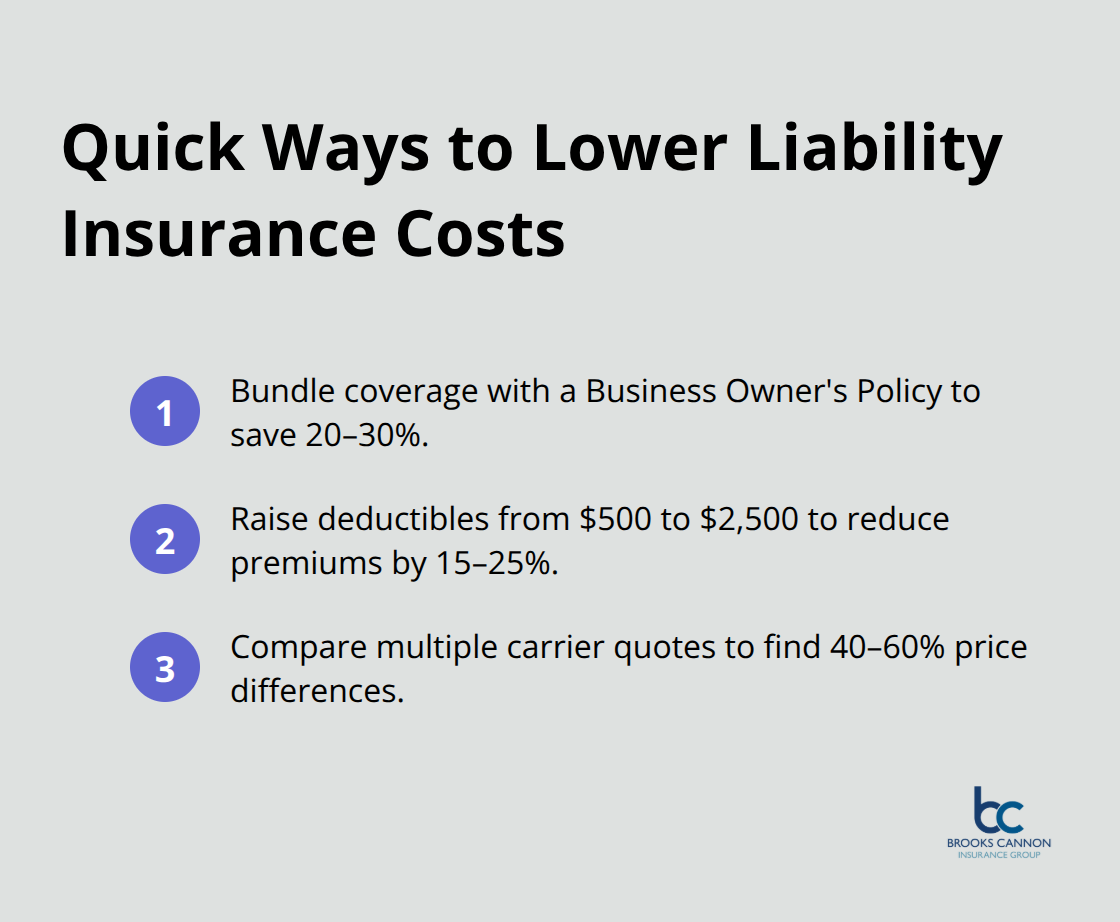

Smart business owners purchase Business Owner’s Policies that bundle general liability, commercial property, and business income coverage for 20-30% savings compared to separate policies. These packages offer comprehensive protection while reducing administrative complexity and total costs.

Deductible selection significantly impacts your annual premiums. Companies that raise deductibles from $500 to $2,500 reduce annual premiums by 15-25% (but must maintain adequate cash reserves for potential claims). Higher deductibles work best for businesses with strong cash flow and lower claim frequency.

Multiple carrier quotes reveal price variations of 40-60% for identical coverage, which makes comparison shopping essential for cost control.

Final Thoughts

Small business liability insurance represents the difference between surviving a lawsuit and closing your doors permanently. The statistics paint a clear picture: 40% of businesses without adequate coverage shut down within six months of a major claim. This protection becomes non-negotiable when you consider that employment practices claims are six times more likely than cyber incidents, and the average liability settlement reaches $54,000.

The right coverage starts with honest risk assessment. Manufacturing operations face different exposures than consulting firms, and your industry directly impacts premium costs. Construction companies pay 300% more than office-based businesses because their risk profiles differ dramatically, while million-dollar companies see premiums jump 100-150% over smaller operations.

The smart approach involves comparing multiple carriers since identical coverage can vary by 40-60% between insurers (Business Owner’s Policies deliver 20-30% savings by bundling general liability with property coverage). Independent agents provide access to multiple carriers and expert guidance through complex coverage decisions. We at Brooks Cannon Insurance Group help Dallas businesses find optimal protection through our network of top-rated carriers and local market expertise.