Construction projects face countless risks that can drain budgets and halt progress. Weather damage, theft, and accidents happen daily across Dallas-area job sites.

We at Brooks Cannon Insurance Group see builders lose thousands when they skip course of construction insurance. This specialized coverage protects your investment from foundation to final inspection.

What Does Course of Construction Insurance Actually Cover

Course of construction insurance protects three major areas that can destroy your project budget. Property damage coverage activates when storms, fires, or vandalism strike your building site. This protection covers the structure itself, stored materials, and temporary installations like scaffolding. Weather-related incidents pose significant risks for Dallas builders who face notorious hailstorms and tornadoes.

Property Damage Protection

Your policy covers direct damage to the building under construction from covered perils. Fire damage, lightning strikes, and wind damage fall under standard coverage. The policy also protects materials you store on-site, whether they sit in temporary storage areas or await installation. Temporary structures like construction trailers and equipment sheds receive protection too (assuming they support the main construction project).

Third-Party Liability Coverage

The policy covers bodily injury claims when visitors, delivery drivers, or passersby suffer injuries on your construction site. A single slip-and-fall accident can result in substantial medical bills and legal fees. This coverage handles lawsuits from non-employees who suffer injuries due to construction activities. Property damage to neighboring buildings from construction operations also falls under this protection.

Equipment and Materials Theft Protection

Theft protection covers tools, equipment, and building materials stored on-site or in transit. Construction sites face significant theft risks that can impact project budgets substantially. Your policy reimburses stolen copper wiring, power tools, and building supplies at replacement cost. Some policies extend coverage to materials stored off-site at approved locations (giving you flexibility while maintaining protection).

These coverage areas work together to protect your investment, but understanding what your policy excludes proves equally important for complete protection. Residential ground-up construction or renovations require specific coverage considerations that vary by project type and scope.

Why Construction Projects Fail Without Proper Insurance

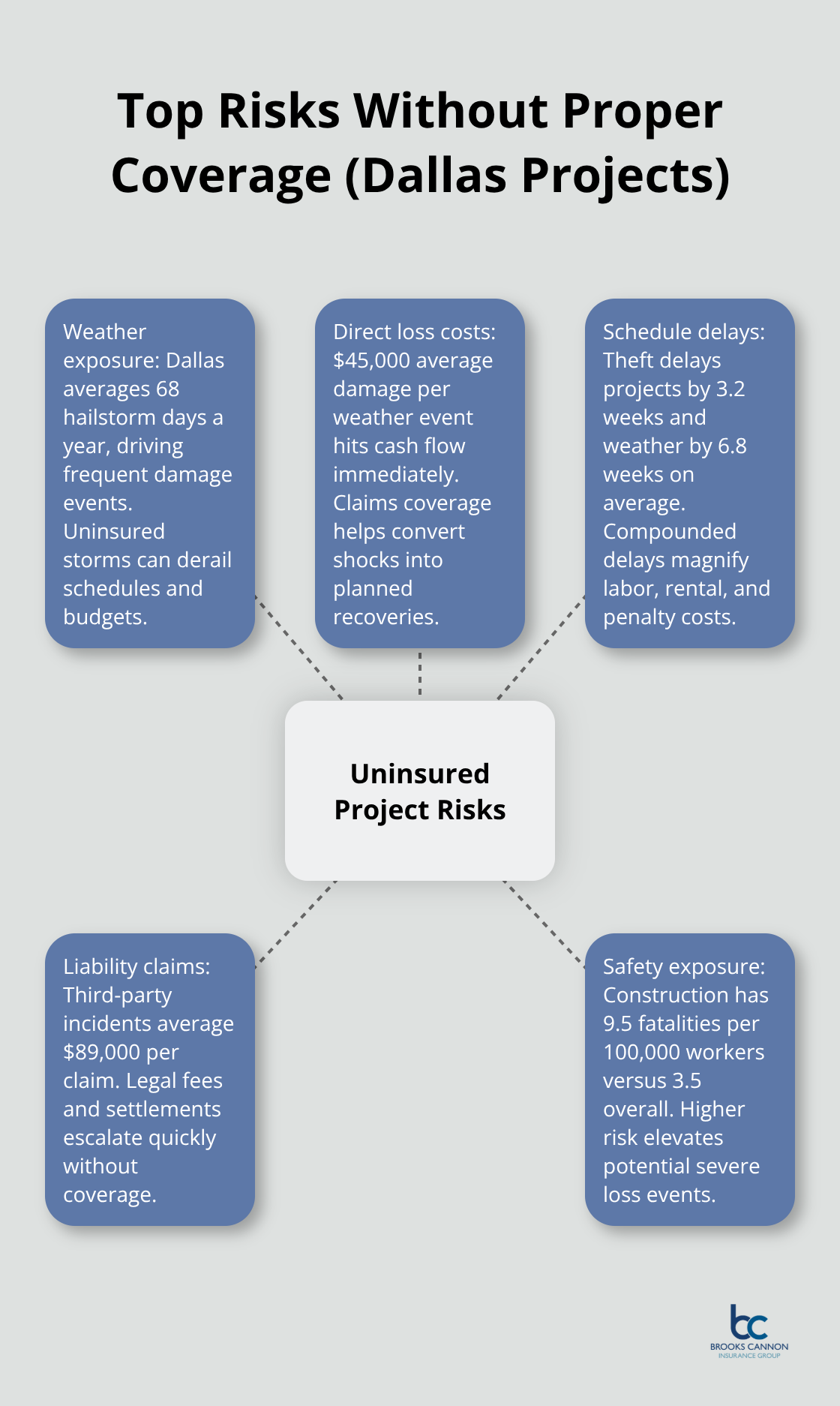

Dallas construction sites face an average of 68 hailstorm days annually according to National Weather Service data, which makes weather protection non-negotiable for local builders. Each uninsured weather event costs contractors an average of $45,000 in direct damages plus project delays that compound costs exponentially. Course of construction insurance transforms these potentially devastating losses into manageable insurance claims that keep projects on schedule.

Weather Damage Costs Add Up Fast

Texas ranks second nationally for construction weather damage with annual losses that exceed $2.8 billion across the state. Hailstorms damage roofing materials, siding, and equipment within minutes while tornadoes can destroy entire construction phases. Builders face complete project restarts after severe weather hits uninsured sites, which turns profitable jobs into financial disasters that threaten business survival.

Worker Accidents Create Massive Liability Exposure

Construction sites experience 9.5 worker fatalities per 100,000 workers compared to 3.5 across all industries according to Bureau of Labor Statistics data. Third-party injuries from falling debris or construction equipment create liability claims that average $89,000 per incident. Subcontractor accidents on your site become your responsibility without proper coverage, which exposes builders to lawsuits that can bankrupt successful companies overnight.

Project Delays Multiply Original Costs

Material theft alone causes 3.2 weeks of average project delays while weather damage extends timelines by 6.8 weeks on average. Each week of delay adds 2.3% to total project costs through extended equipment rentals, labor overtime, and penalty clauses (making quick recovery essential for profitability). Smart builders calculate these multiplier effects before they break ground rather than discover them during crisis situations when coverage gaps become expensive lessons.

These financial risks highlight why builders need comprehensive protection, but not all policies offer the same level of coverage or exclusions that could leave you exposed.

Key Policy Features and Exclusions

Course of construction insurance policies contain specific financial terms that directly impact your project budget and claim recovery. Coverage limits typically range from $500,000 to $50 million based on total project value, with most Dallas commercial projects that require $2-5 million in coverage. Deductibles start at $2,500 for residential projects but jump to $25,000-$100,000 for commercial builds, which means you absorb initial losses before insurance coverage activates. Higher deductibles reduce premium costs by 15-30% but create substantial out-of-pocket expenses when claims occur.

Coverage Limits and Deductible Structures

Insurance carriers calculate coverage limits based on total completed project value rather than current construction phase value. A $3 million office building requires $3 million in coverage even during early foundation work when actual value sits at $200,000. This approach protects against total loss scenarios but increases premium costs throughout the entire construction timeline.

Deductible structures vary significantly between residential and commercial projects (with commercial builds facing substantially higher out-of-pocket costs). Wind and hail deductibles often carry separate terms that range from 1-5% of total coverage limits in Texas markets.

Standard Exclusions That Create Coverage Gaps

Insurance companies exclude design defects, faulty workmanship, and normal wear from coverage regardless of premium payments. Mechanical breakdown of equipment, earth movement that includes landslides, and flood damage require separate endorsements that cost 8-12% of base premiums. Employee theft by your own workers falls outside standard coverage while third-party theft receives full protection.

Ordinance and law changes that force code upgrades create expensive gaps unless you purchase specific endorsements. War, nuclear hazards, and intentional damage by the insured remain universally excluded across all carriers.

Enhanced Coverage Options Worth the Investment

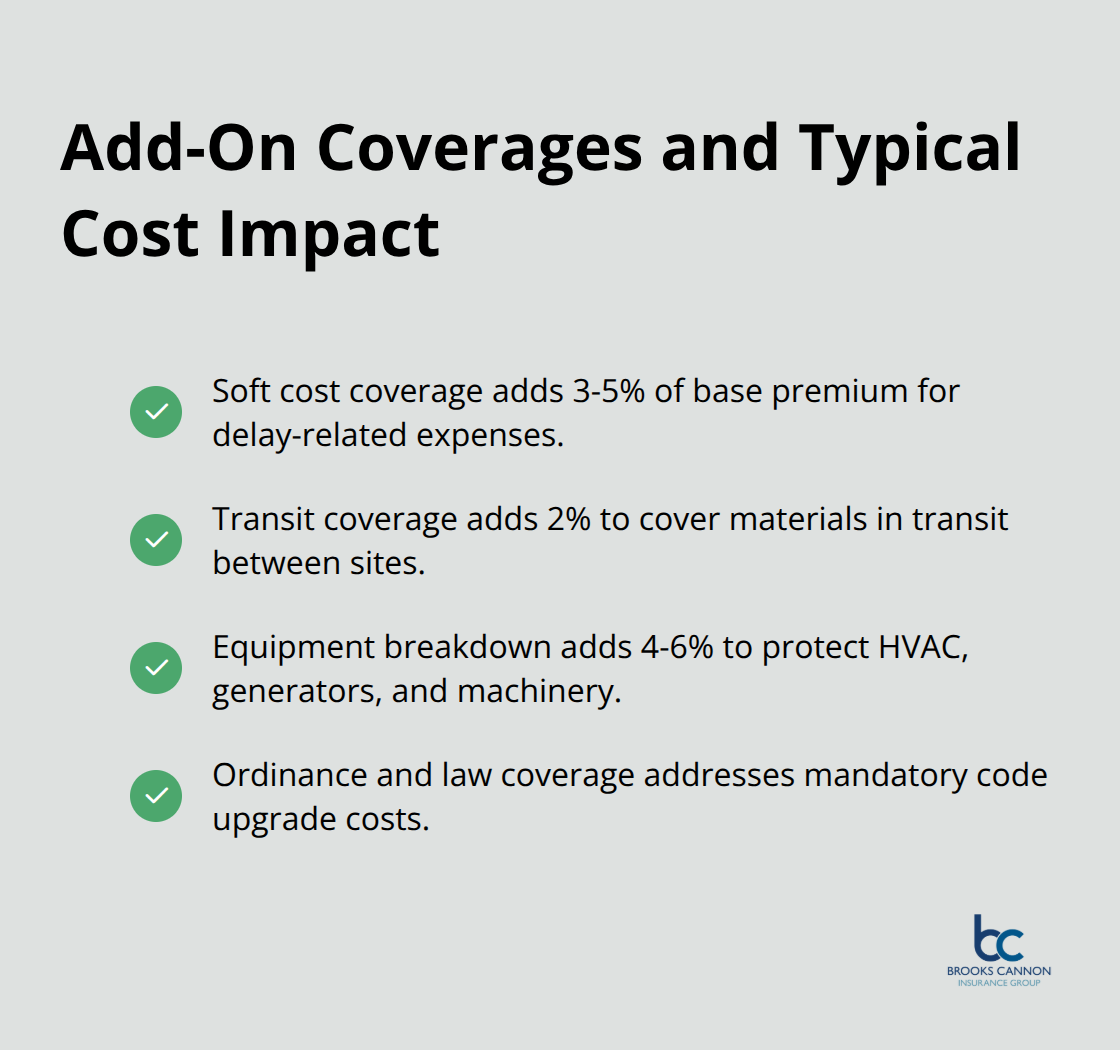

Soft cost coverage protects against additional interest, permit fees, and architect expenses when project delays occur at 3-5% of base premium costs. Transit coverage extends protection to materials while they move between suppliers and job sites for an additional 2% premium charge. Equipment breakdown endorsements cover HVAC systems, generators, and construction machinery for 4-6% extra cost but prevent total replacement expenses.

Ordinance and law coverage handles mandatory code upgrades that create significant expenses for commercial projects. These endorsements transform basic policies into comprehensive protection that covers real-world construction scenarios rather than theoretical minimum coverage.

Final Thoughts

Course of construction insurance protects Dallas builders from financial disasters that destroy profitable projects. Weather damage costs $45,000 per incident while liability claims reach $89,000 and project delays multiply costs by 2.3% weekly. These documented realities impact construction sites across Dallas daily, not theoretical scenarios that might happen.

Experienced insurance professionals transform complex policy terms into practical protection strategies. We at Brooks Cannon Insurance Group analyze your specific project requirements and connect you with competitive coverage from top-rated carriers. Our team understands Dallas construction risks and creates policies that address real-world scenarios rather than minimum requirements.

Smart builders secure quotes before they break ground rather than shop for coverage after problems develop. Brooks Cannon Insurance Group provides comprehensive analysis of your construction insurance needs with competitive rates from leading carriers (preventing expensive lessons that bankrupt unprepared contractors). Proper coverage early in the process protects your investment and keeps projects on track.