Texas businesses face specific legal obligations when it comes to general liability insurance. While the state doesn’t mandate coverage for all companies, certain industries and situations require protection.

We at Brooks Cannon Insurance Group see many Dallas-area business owners confused about these requirements. Understanding your obligations protects both your company and your financial future.

Which Texas Businesses Must Carry General Liability Insurance?

Government Contract Requirements

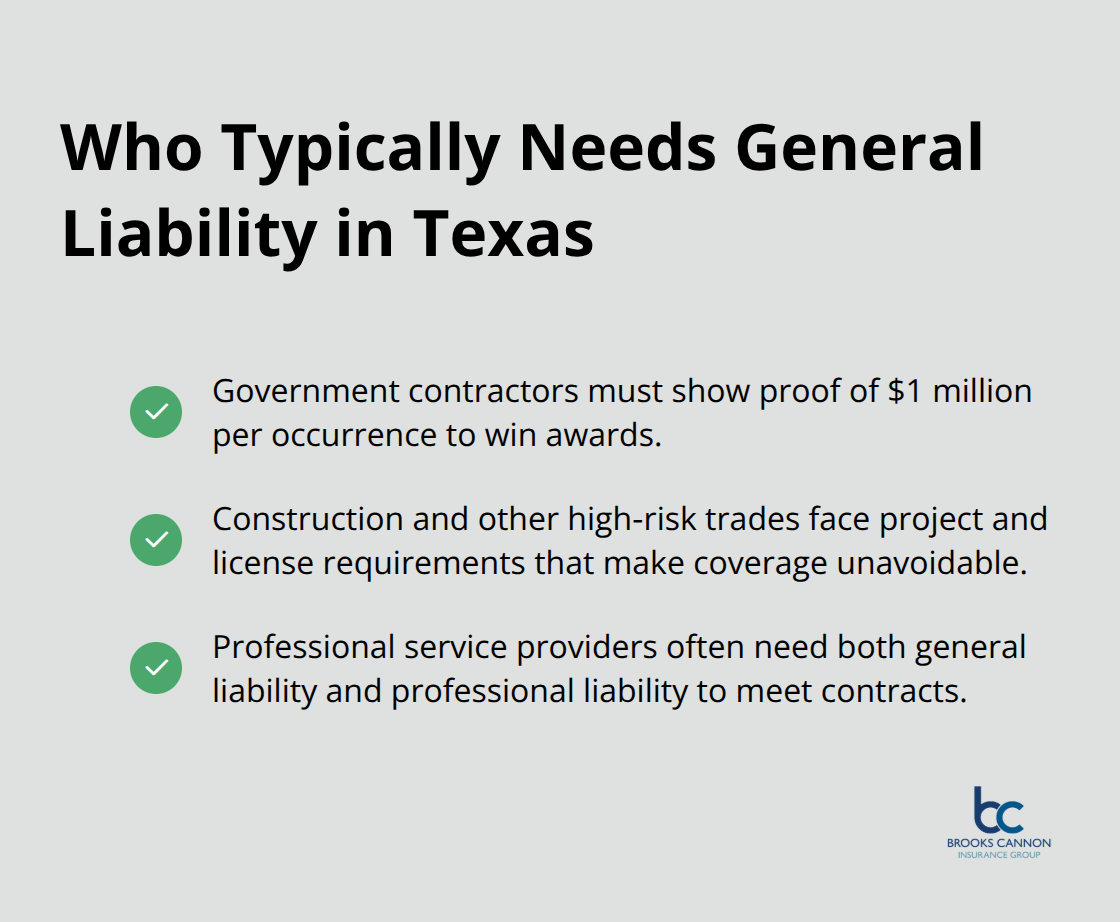

Texas businesses that contract with government entities face mandatory liability insurance requirements when state agencies include provisions in their contracts for goods or services. State agencies and municipalities require proof of general liability insurance with minimum limits of $1 million per occurrence before they award contracts. Government contracts consistently include specific insurance requirements beyond basic mandates.

Construction and High-Risk Industry Standards

Construction companies in Texas encounter the strictest coverage expectations. While state law doesn’t mandate general liability insurance, licensing boards and project requirements make coverage practically unavoidable. The Texas Department of Licensing and Regulation requires proof of insurance for most contractor licenses. Commercial property owners demand certificates of insurance before they allow contractors on-site.

Construction businesses typically need $2 million aggregate coverage to meet industry standards. Manufacturing and trade businesses face similar pressures, with most commercial leases requiring general liability protection.

Professional Service Provider Obligations

Professional service providers (consultants, architects, and engineers) must carry general liability insurance to secure client contracts. Most professional agreements include insurance requirements that exceed basic coverage. These businesses often need both general liability and professional liability insurance to meet contractual obligations. The combination protects against both physical incidents and professional errors.

Financial Consequences of Uninsured Operations

Texas businesses that operate without adequate insurance face severe financial exposure. The state records thousands of business-related lawsuits annually, with significant legal costs for small businesses. Companies without general liability insurance must pay these costs directly, often leading to financial hardship. Workers’ compensation becomes mandatory if businesses choose not to carry coverage and face workplace injury claims. Uninsured businesses leave owners personally liable for judgments and settlements.

Understanding these requirements helps business owners make informed decisions about their coverage needs and the specific protection levels that different industries demand.

What Protection Does General Liability Coverage Actually Provide?

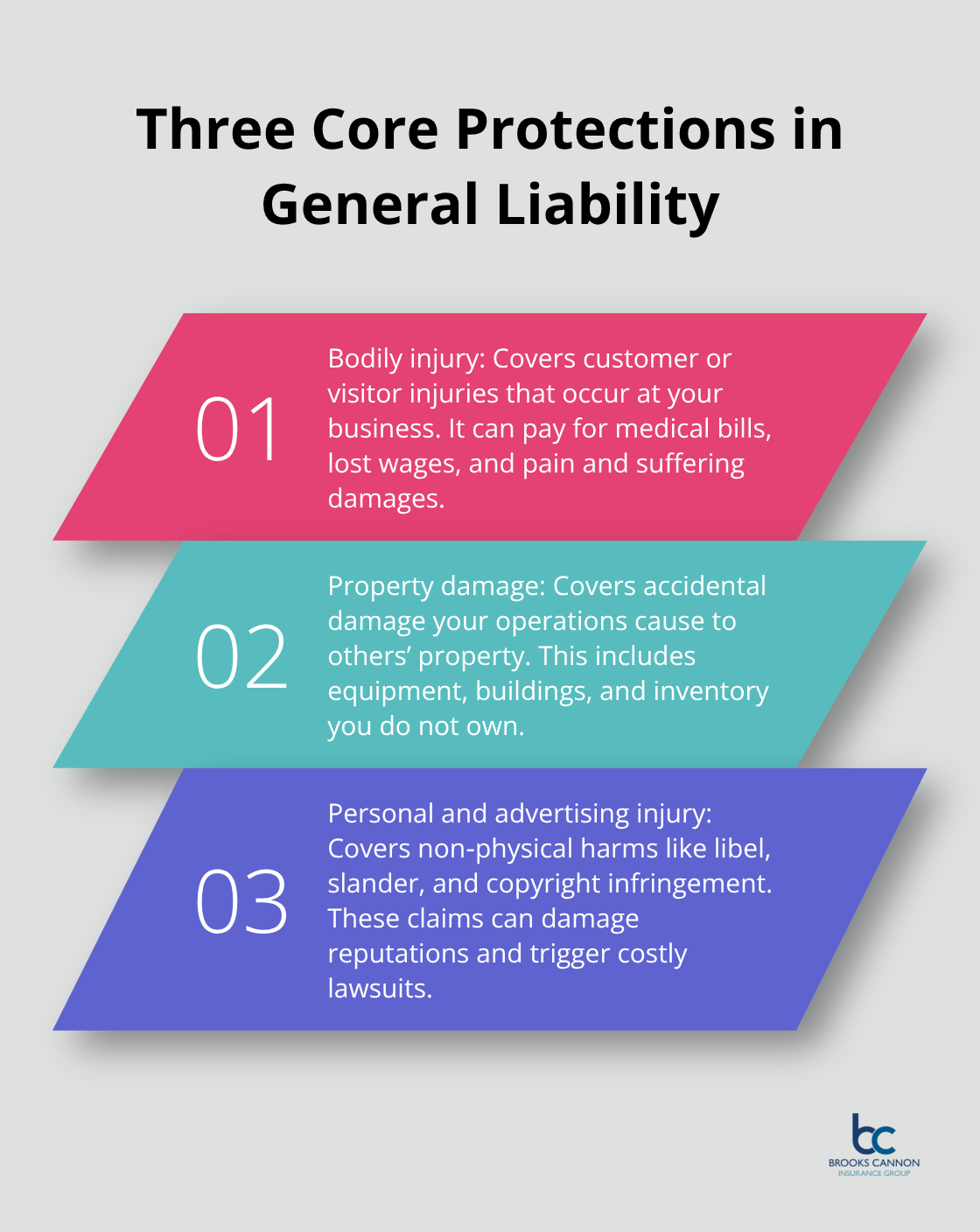

General liability insurance delivers three fundamental protection layers that Texas businesses cannot afford to ignore. The primary coverage protects against bodily injury claims when customers or visitors suffer physical harm on your business premises. Standard policies cover medical expenses, lost wages, and pain and suffering damages. Property damage coverage handles situations where your business operations accidentally damage someone else’s property, including equipment destruction, building damage, or inventory loss. Personal and advertising injury protection addresses non-physical harm claims, including libel, slander, and copyright infringement accusations that can devastate business reputations and trigger expensive lawsuits.

Medical Payments Coverage Limits

Most Texas general liability policies include immediate medical payments coverage between $1,000 and $10,000 per incident, regardless of fault determination. This coverage pays for minor injuries without lengthy legal proceedings, often preventing small incidents from escalating into major lawsuits. Smart business owners use this feature to maintain positive customer relationships while protecting their liability exposure.

However, medical payments coverage has strict limitations and excludes employee injuries, which require separate workers compensation protection.

Legal Defense Cost Protection

Legal defense coverage represents the most valuable aspect of general liability insurance, often exceeding actual damage awards in complex litigation. Defense costs operate outside policy limits in most Texas policies (meaning insurers pay legal expenses without reducing available coverage for settlements or judgments). The Insurance Information Institute reports that average legal defense costs reach $15,000 per claim for small businesses, making this protection financially essential. Insurers provide experienced legal teams familiar with Texas business law, significantly improving defense outcomes compared to self-representation or independently hired attorneys.

Understanding these coverage components helps business owners evaluate their protection needs as they consider the various factors that influence their insurance costs and premium structure.

What Drives Your General Liability Insurance Costs?

Insurance premiums depend on measurable risk factors that insurers evaluate during underwriting. Business size significantly impacts costs through annual revenue and employee count, with retail businesses typically paying $600 to $800 annually while construction companies face $1,000 to $1,300 due to higher injury risks. Texas work-related injuries involving days away from work, job transfer, or restrictions occurred at significant rates in 2021-2022, which drives premium calculations for high-risk industries. Very small, low-risk businesses pay $480 to $720 annually, while restaurants average $1,500 to $1,800 because of frequent slip-and-fall incidents.

Location and Claims History Shape Premium Calculations

Dallas businesses face higher premiums than smaller Texas towns due to increased foot traffic and litigation frequency. Texas saw 12,000 business-related lawsuits in 2024, with urban areas that experience disproportionate claim activity. Past claims signal future risk to insurers, which causes premium increases that persist for three to five years. Clean claims histories qualify businesses for preferred rates, while multiple incidents can double standard premiums. Smart business owners implement safety measures like non-slip mats and clear walkways to prevent incidents and maintain favorable rates.

Coverage Limits and Deductible Strategy

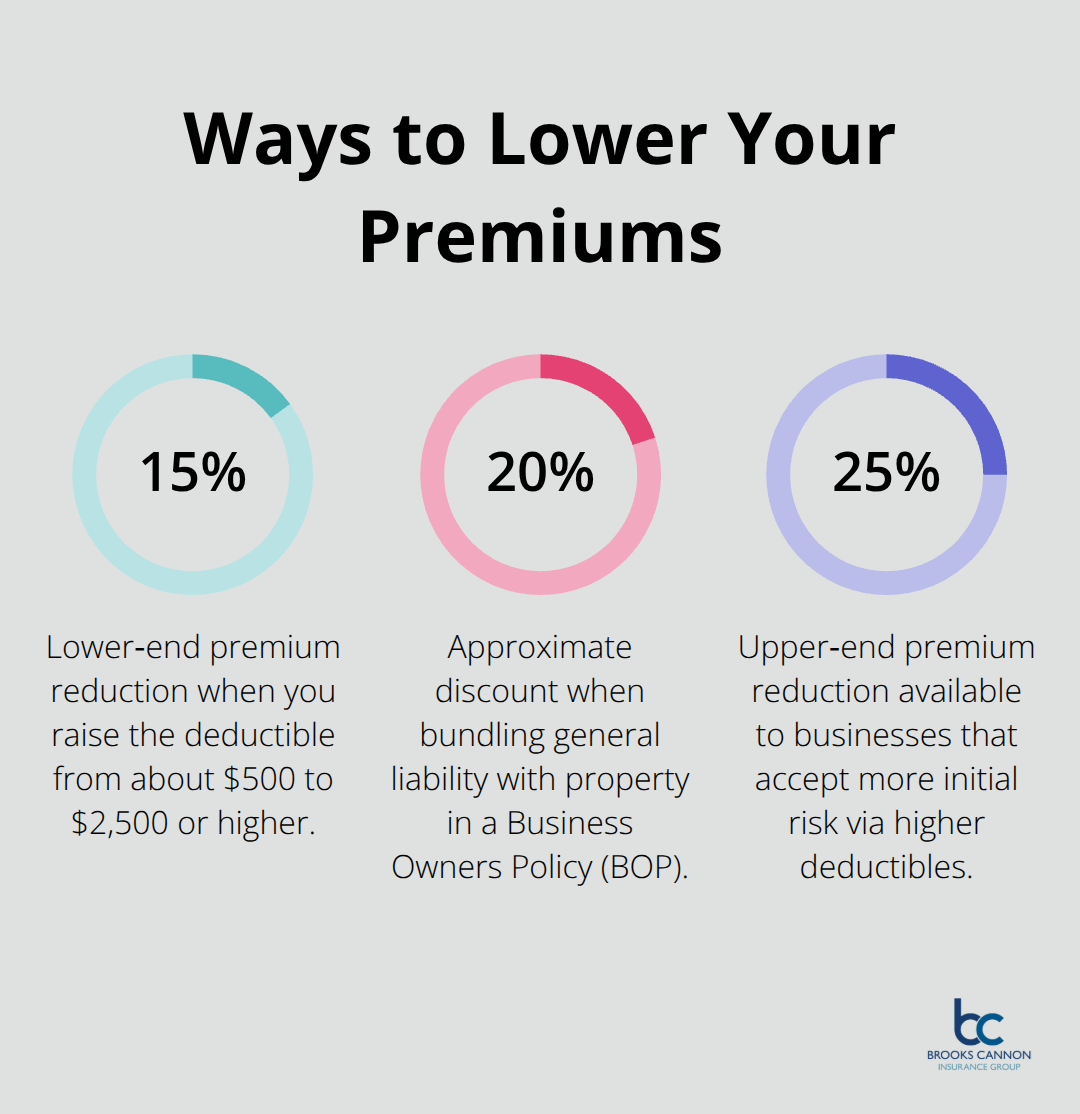

Standard coverage limits of $1 million per occurrence and $2 million aggregate meet most contract requirements, but businesses can reduce premiums when they raise deductibles from $500 to $2,500 or higher. Higher deductibles can lower annual premiums by 15-25% for businesses that accept more initial risk.

Business Owners Policies that combine general liability and property coverage cost approximately 20% less than separate policies, which makes them ideal for small businesses with commercial property. The Texas Property and Casualty Insurance Guaranty Association protects policyholders up to $300,000 if insurers become insolvent (providing additional security for coverage investments).

Final Thoughts

Texas businesses must understand that general liability insurance requirements vary significantly by industry and contract obligations. Government contractors need minimum $1 million coverage, while construction companies typically require $2 million aggregate limits. Professional service providers face dual obligations for both general liability and professional coverage.

Appropriate general liability insurance Texas protection starts with accurate risk assessment. Document your business operations, employee count, and annual revenue. Obtain quotes from multiple carriers, as underwriters apply different criteria between insurers (making comparison shopping essential for optimal rates).

Experienced local professionals make the difference between adequate protection and costly coverage gaps. We at Brooks Cannon Insurance Group work with multiple top-rated carriers to find optimal coverage and rates for each client’s unique situation. Our licensed experts understand Texas-specific requirements and help businesses navigate complex coverage decisions while maintaining competitive premiums.