Builders risk insurance cost varies dramatically depending on your project scope, location, and construction timeline. If you’re planning a build in the Dallas area, understanding what you’ll actually pay is essential before breaking ground.

We at Brooks Cannon Insurance Group help contractors and property owners navigate these costs every day. This guide breaks down the real numbers and shows you concrete ways to reduce your premiums.

What Drives Your Builders Risk Insurance Quote

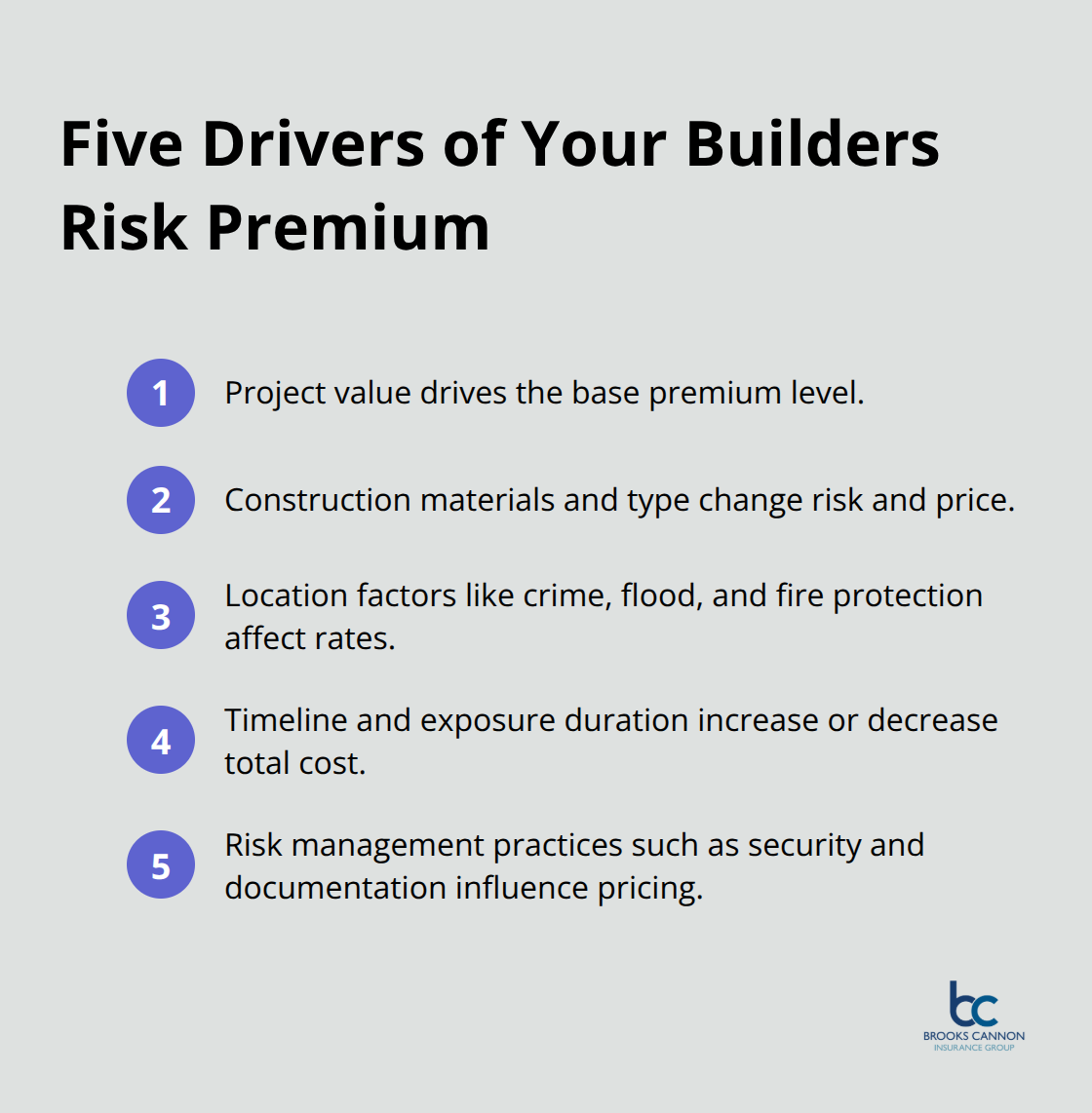

Your builders risk premium hinges on five concrete factors that underwriters assess before quoting you a price. Project value is the biggest lever-premiums typically run 1% to 4% of your total construction budget annually, according to industry data. A $500,000 residential project in Dallas might cost $2,500 to $20,000 per year depending on other variables, while a $1 million commercial build could run $3,000 to $5,000 annually.

The hard costs-materials, labor, and equipment-drive this calculation directly, so if your material budget climbs mid-project, your coverage limit and premium shift upward.

[Construction Type] Swings Your Premium by 50% or More

The materials and methods you use can dramatically shift your quote. Fire-resistive construction costs significantly less to insure than wood-frame builds because the risk profile is fundamentally different. Steel structures fall in the middle. If you’re planning a Dallas-area renovation using standard wood framing, you’ll pay higher premiums than a new metal-frame commercial structure of the same value. Masonry noncombustible construction generally sits between wood frame and steel in terms of pricing. Specify your materials early to prevent surprises when you receive quotes-switching from wood to fire-resistive components mid-planning can save thousands annually.

Location Amplifies Costs in Predictable Ways

Dallas contractors benefit from being away from coastal hurricane zones and wildfire-prone regions, but proximity to flood zones or areas with high theft rates still raises premiums. A fire station nearby can lower costs by a meaningful percentage, while projects in high-crime neighborhoods pay more. The underwriter evaluates your specific address and surrounding risk factors before calculating your rate.

Project Duration Directly Impacts Your Annual Cost

Longer timelines mean more exposure to weather, theft, and vandalism. A six-month project costs less to insure than an 18-month one at the same value because the risk window is shorter. Short-term projects sometimes qualify for rates as low as 0.3% to 0.5% of project value, while extended builds creep toward the higher end of standard ranges. This timeline factor makes it worth accelerating your schedule if feasible-every month you cut from construction reduces your total insurance expense.

Understanding these five drivers positions you to anticipate your costs before you request quotes. Next, we’ll look at what Dallas-area contractors actually pay and how your project stacks up against regional benchmarks.

What Dallas Builders Actually Pay for Coverage

Texas builders face a straightforward pricing reality: your premium scales directly with project value, but Dallas contractors typically pay less than their counterparts in coastal or wildfire-prone states. For a $500,000 residential project in the Dallas area, expect annual premiums between $2,500 and $10,000 depending on construction type and timeline. Commercial projects of $1 million value run roughly $3,000 to $5,000 annually based on standard 1% to 4% of project value calculations. These numbers assume wood-frame or standard construction; fire-resistive materials lower your cost meaningfully, while renovation work pushes premiums higher due to existing structure complications. A $100,000 small residential project might cost $300 to $500 monthly, while a $3 million commercial build could run $250 to $500 monthly depending on risk factors. Short-term projects benefit from reduced rates as low as 0.3% to 0.5% of project value since your exposure window shrinks considerably. The key takeaway is this: Dallas market rates sit below national averages because you avoid the hurricane, flood, and wildfire premiums that plague Florida, California, and coastal Texas regions. Your location advantage means a $1 million project here costs less than the same scope in Houston’s flood zone or San Francisco’s earthquake territory.

Residential Versus Commercial Pricing Tells You Where to Focus

Residential wood-frame construction typically carries premiums toward the 0.5% to 0.8% range of project value, making a $400,000 home build run roughly $2,000 to $3,200 annually. Commercial projects, especially fire-resistive steel or masonry structures, often qualify for lower rates in the 0.25% to 0.4% range, so a $1 million commercial build might cost only $2,500 to $4,000 annually. This reversal happens because commercial construction generally uses safer materials and attracts experienced contractors with strong safety records. Renovations break the pattern entirely, commanding premiums at 0.4% to 0.7% because existing structures introduce unknown hazards and complicate coverage. If you compare bids on similar-value projects, the construction type matters far more than whether the project is residential or commercial. Dallas agents see too many contractors underestimate renovation costs because they anchor to residential pricing without accounting for the complexity premium. Request separate quotes for each scenario rather than assuming a baseline applies across all project types.

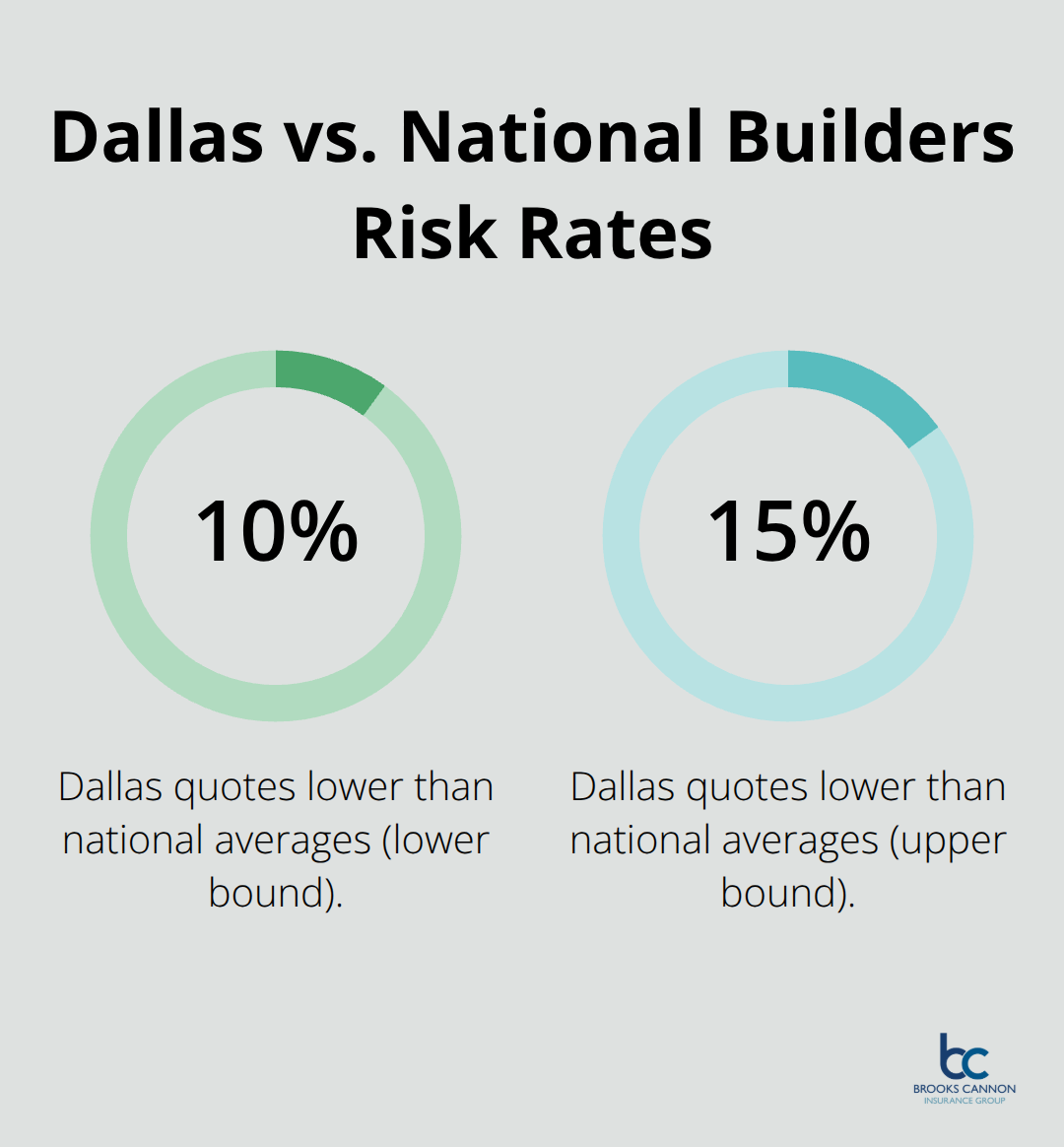

Dallas Rates Lag National Benchmarks by 10 to 15 Percent

Independent agents working across multiple carriers confirm that Dallas-area projects consistently quote 10% to 15% lower than national averages when all other variables match. A $2 million mixed-use project in Dallas might cost $6,000 to $8,000 annually, while the identical scope in Miami or Los Angeles could easily exceed $10,000 due to regional disaster exposure and higher theft rates.

This geographic advantage disappears if your project sits in flood-prone areas near the Trinity River or in neighborhoods with elevated crime rates, so your specific address still matters tremendously. Contractors bidding against firms in California or Florida can legitimately factor lower insurance costs into their proposals, giving Dallas builders a competitive edge on total project expense. Material costs have climbed steadily, and replacement cost coverage means you pay current prices when claims occur, not your original purchase prices.

What Moves Your Quote Up or Down

Your specific address, materials, and timeline create the real variation in what you’ll pay. A fire station nearby can lower costs by a meaningful percentage, while projects in high-crime neighborhoods pay more. The underwriter evaluates your location and surrounding risk factors before calculating your rate. If you accelerate your schedule, every month you cut from construction reduces your total insurance expense. Short-term projects sometimes qualify for rates as low as 0.3% to 0.5% of project value, while extended builds creep toward the higher end of standard ranges. Fire-resistive construction costs significantly less to insure than wood-frame builds because the risk profile is fundamentally different. Specify your materials early to prevent surprises when you receive quotes-switching from wood to fire-resistive components mid-planning can save thousands annually.

Understanding these pricing patterns positions you to anticipate your costs before you request quotes and to identify where you can trim expenses without sacrificing protection. The next section shows you concrete strategies that actually lower your premiums.

Reduce Your Premium Without Cutting Coverage

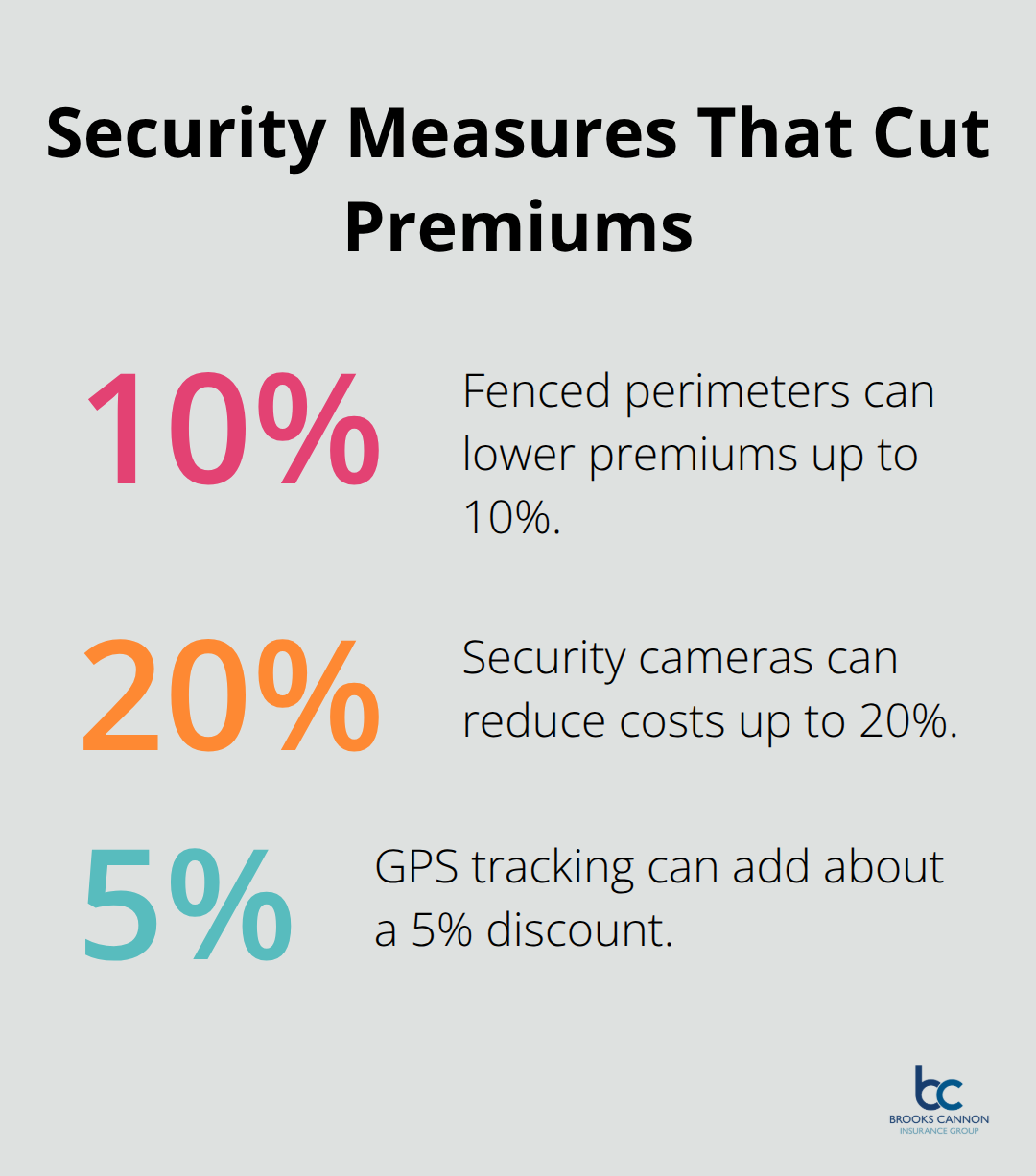

Security measures on your job site deliver measurable premium reductions that underwriters reward immediately. Fenced perimeters with controlled access lower premiums by 5% to 10%, while security cameras reduce costs by 5% to 20% depending on coverage quality and monitoring.

GPS tracking on high-value equipment and materials cuts theft risk enough that some carriers quote an additional 5% discount. These aren’t theoretical savings-underwriters price risk based on loss history, and sites with documented security consistently file fewer theft and vandalism claims. Start security implementation before your policy quotes arrive so you can mention these measures to agents and lock in lower rates from day one.

Material cost documentation matters equally. Photograph incoming shipments, maintain invoices organized by delivery date, and track waste percentages. When a claim occurs, replacement cost coverage pays current market prices rather than your original purchase cost, so detailed records prove what you actually lost and at what price point.

Independent Agents Negotiate Rates Below Online Quotes

Online calculators and instant quote tools rarely reflect what you’ll actually pay because they can’t factor in your specific risk profile and negotiating leverage. Independent agents typically reduce policy prices by 10% to 15% compared with instant quotes, according to industry data, and they secure same-day coverage in many cases. An agent working with multiple top-rated carriers can shop your project across 15 or more insurers simultaneously rather than accepting the first quote you find online.

Request quotes from at least three agents and have them compete directly for your business-this competitive pressure drives real savings without sacrificing coverage quality. Bundling your builders risk policy with commercial general liability, commercial property, or commercial auto insurance through one agent amplifies discounts because carriers reward consolidated relationships. A contractor bundling five policies typically saves 15% to 25% across the entire package compared with purchasing policies separately. Ask your agent specifically about bundle discounts and whether switching your existing business policies to the same carrier would unlock additional savings on your builders risk premium.

Material Costs and Timeline Control Your Bottom Line

Project value climbs when material costs spike mid-construction, which means your coverage limits must rise to prevent underinsurance. Conduct quarterly coverage reviews on projects lasting longer than six months and raise limits promptly if material costs climb 10% or more. Long projects running 18 months or longer accumulate material price inflation that your original premium calculation didn’t anticipate, leaving you exposed if a loss occurs.

Acceleration of your schedule cuts exposure time and directly reduces your total insurance cost because shorter-duration projects qualify for lower rate multipliers. Every month you trim from your timeline saves money on premiums while simultaneously reducing your exposure to weather, theft, and vandalism. Subcontractors supplying their own materials should carry their own builders risk coverage rather than relying on your policy, which clarifies responsibility and prevents coverage gaps. Require subcontractors to provide proof of builders risk coverage before they deliver materials to your site, and obtain waivers of subrogation to prevent disputes over who pays when losses occur.

Final Thoughts

Builders risk insurance cost ultimately depends on five concrete factors: project value, construction materials, location, timeline, and your risk management practices. Dallas contractors benefit from geographic pricing advantages that run 10% to 15% below national averages, though your specific address and construction type still determine what you’ll actually pay. A $500,000 residential project here costs $2,500 to $10,000 annually, while a $1 million commercial build runs roughly $3,000 to $5,000 depending on materials and scope.

The single most effective way to reduce your premium is requesting quotes from multiple carriers simultaneously through an independent agent who shops your project across numerous insurers rather than accepting the first price you find online. Bundling your builders risk policy with commercial general liability, commercial property, or commercial auto insurance amplifies savings by 15% to 25% across your entire package. Security measures like fenced perimeters and monitored cameras deliver documented premium reductions of 5% to 20%, and these discounts apply immediately when you mention them during the quoting process.

We at Brooks Cannon Insurance Group work with multiple top-rated carriers to find the best coverage and pricing for your specific project. Our licensed experts understand Dallas market rates, regional risk factors, and the material cost documentation that prevents underinsurance claims. Contact Brooks Cannon Insurance Group today to request quotes from agents who understand construction risk and can deliver the competitive pricing your project deserves.