Your luxury home isn’t like other properties, and your insurance shouldn’t be either. Standard homeowners policies leave expensive homes and collections dangerously underprotected, which is why we at Brooks Cannon Insurance Group specialize in luxury home insurance for Dallas-area homeowners.

High-net-worth properties need coverage that matches their real value. This guide walks you through what sets luxury policies apart and how to protect what matters most.

What Coverage Do You Actually Need for Your Luxury Home

Replacement Cost vs. Market Value

Luxury homes in the Dallas area typically exceed $1 million in replacement cost, and standard homeowners policies cap out around $2 million in dwelling coverage. That sounds adequate until you factor in construction inflation, specialized materials, and the actual cost to rebuild. A $3 million home with imported marble flooring, custom millwork, and high-end smart home integration costs significantly more to restore than its market value suggests. Insurance companies measure this through replacement cost value, not market value, which means they calculate what it would take to rebuild from scratch with equivalent materials and craftsmanship. This distinction matters enormously because luxury homes with unique architectural features often face underinsurance gaps when policies rely on standard calculations.

Protecting Your Collections and Personal Property

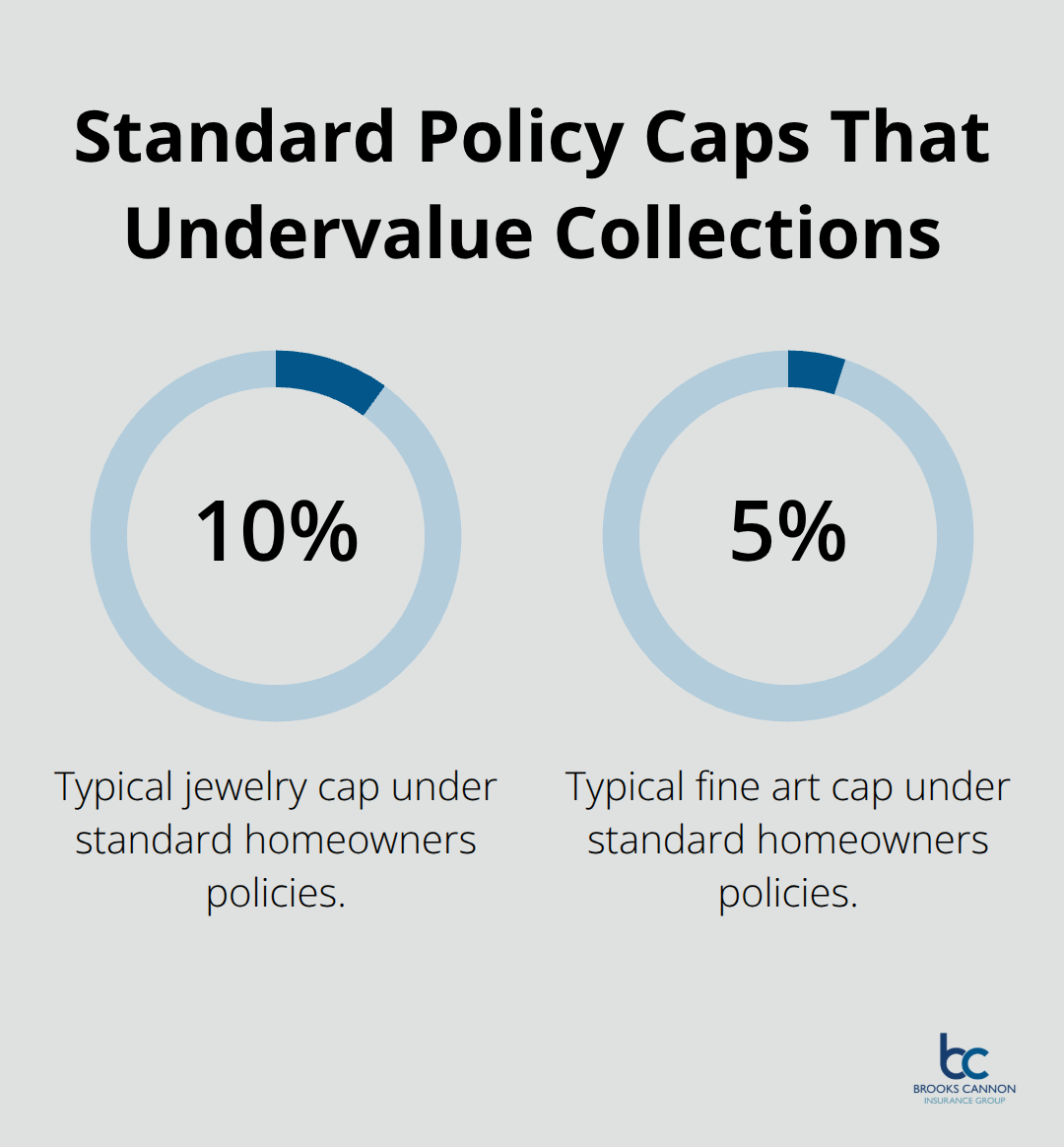

Your collections and personal property demand equally specialized attention. Fine art, jewelry, wine collections, and antiques typically hit coverage caps in standard policies, often limited to just 10 percent of your dwelling coverage for jewelry or 5 percent for art. A single painting or jewelry piece worth $500,000 receives virtually no protection under these generic limits. High-value policies address this through scheduled personal property coverage, which insures individual items at their full appraised value without arbitrary percentage restrictions.

Built-In Amenities and Extended Coverage

Luxury homes frequently include built-in amenities like pools, guest houses, wine cellars, or custom home theaters that standard policies either exclude or undervalue. Extended replacement cost coverage becomes critical here because construction costs have risen substantially over recent years. A policy that covers only your initial estimate leaves you exposed when contractors quote higher prices mid-project. Construction labor shortages and premium material availability have pushed rebuild costs upward across the Dallas market, making this protection essential for homeowners with distinctive properties.

Next Steps for Your Coverage Assessment

Your luxury property requires a comprehensive evaluation to identify protection gaps before a loss occurs. An agent experienced in high-value homes can assess your specific situation and recommend appropriate coverage limits and endorsements tailored to your assets and architectural features.

How Luxury Policies Actually Protect You Better

Standard homeowners insurance and luxury policies operate on fundamentally different principles, and the gap widens dramatically when claims happen. A standard policy reimburses based on actual cash value, meaning your five-year-old roof gets depreciated before payment. Luxury policies use guaranteed replacement cost coverage, which pays what it actually costs to rebuild with equivalent materials and craftsmanship, regardless of what you originally paid. For Dallas homeowners with $2 million-plus properties, this difference translates to tens of thousands of dollars in real money when you file a claim. Construction costs in Texas have risen approximately 8-10 percent annually over the past three years according to the Turner Construction Cost Index, making replacement cost language non-negotiable for protecting your investment.

If your home requires custom stone imported from Italy or hand-carved millwork from specialized artisans, a standard policy’s depreciation approach leaves you personally funding the difference between what insurance pays and what actual restoration costs.

When Your Home Becomes Uninhabitable

Additional living expenses coverage in luxury policies reflects the reality that affluent homeowners cannot simply move into an average hotel during reconstruction. Standard policies typically cover hotel and meal costs up to a percentage of your dwelling coverage, capped at amounts suitable for temporary displacement. Luxury coverage extends to maintaining your lifestyle during extended repairs, covering upscale rental properties, household staff wages, club memberships, and other expenses that keep your life functioning at its normal standard. If your home requires six months of restoration, a luxury policy recognizes you need appropriate accommodations, not budget alternatives. This protection matters because temporary housing in Dallas’s premium neighborhoods runs $3,000-$6,000 monthly for properties comparable to luxury homes.

Dedicated Support When Loss Strikes

Claims handling separates luxury insurers from standard carriers. Your policy includes access to dedicated account managers and loss prevention specialists who understand high-value properties. These professionals arrange inspections by contractors experienced with luxury materials, coordinate with architects familiar with historic or custom features, and handle the complex documentation that high-value claims require. Loss prevention support goes further by conducting pre-loss risk assessments, identifying vulnerabilities in security systems, water detection, and structural maintenance before problems develop. Some carriers offer coverage for implementing these improvements, essentially paying you to reduce future risk. This proactive approach costs far less than reactive claims handling and demonstrates why specialized expertise matters for properties where details determine outcomes.

What This Means for Your Coverage Strategy

The protection gap between standard and luxury policies becomes impossible to ignore once you understand how each responds to loss. Your high-value home demands carriers and agents who recognize that replacement cost, not market value, determines adequate coverage. As your property’s complexity and asset value increase, the need for specialized expertise in claims handling and loss prevention becomes equally important as the coverage limits themselves. Understanding these differences positions you to make informed decisions about which policies actually protect your investment and which leave dangerous gaps.

Protecting Your Most Valuable Possessions

Your luxury home contains assets that standard homeowners insurance simply cannot adequately protect. Fine art, jewelry, wine collections, and specialized smart home systems each demand distinct coverage approaches, and treating them as generic personal property guarantees significant underinsurance. Standard policies typically cap jewelry coverage at 1-2 percent of your dwelling limit, which means a $3 million home receives only $30,000-$60,000 in jewelry protection regardless of your actual collection value. A single engagement ring or watch worth $150,000 sits completely exposed under this arrangement. Scheduled personal property coverage solves this problem by insuring individual items at their full appraised value without percentage restrictions. This approach requires appraisals from certified professionals, and that investment pays immediate dividends because insurers pay replacement cost rather than depreciated value when loss occurs. For Dallas homeowners with significant collections, the difference between generic limits and scheduled coverage often amounts to hundreds of thousands of dollars in actual protection.

Fine Art and High-End Jewelry

Fine art and jewelry require separate appraisals from specialists recognized by major insurance carriers. An art appraiser certified by the American Society of Appraisers carries weight that general property appraisals cannot match, and most luxury insurers demand this credential for items exceeding $25,000. Jewelry appraisals should come from American Gem Society certified gemologists who document stone quality, metal composition, and current market value. These appraisals typically cost $200-$500 per item but protect against underinsurance disputes during claims. Scheduled coverage for art and jewelry operates independently from your home’s main dwelling limit, meaning a $500,000 painting claim does not reduce your structural coverage. This separation matters enormously because comprehensive replacement cost coverage for specialized items prevents the gap between what your insurer values items at and what actual replacement costs run. Dallas luxury homeowners frequently discover that items purchased years ago have appreciated significantly, making current appraisals essential rather than optional.

Wine, Collectibles, and Specialized Storage

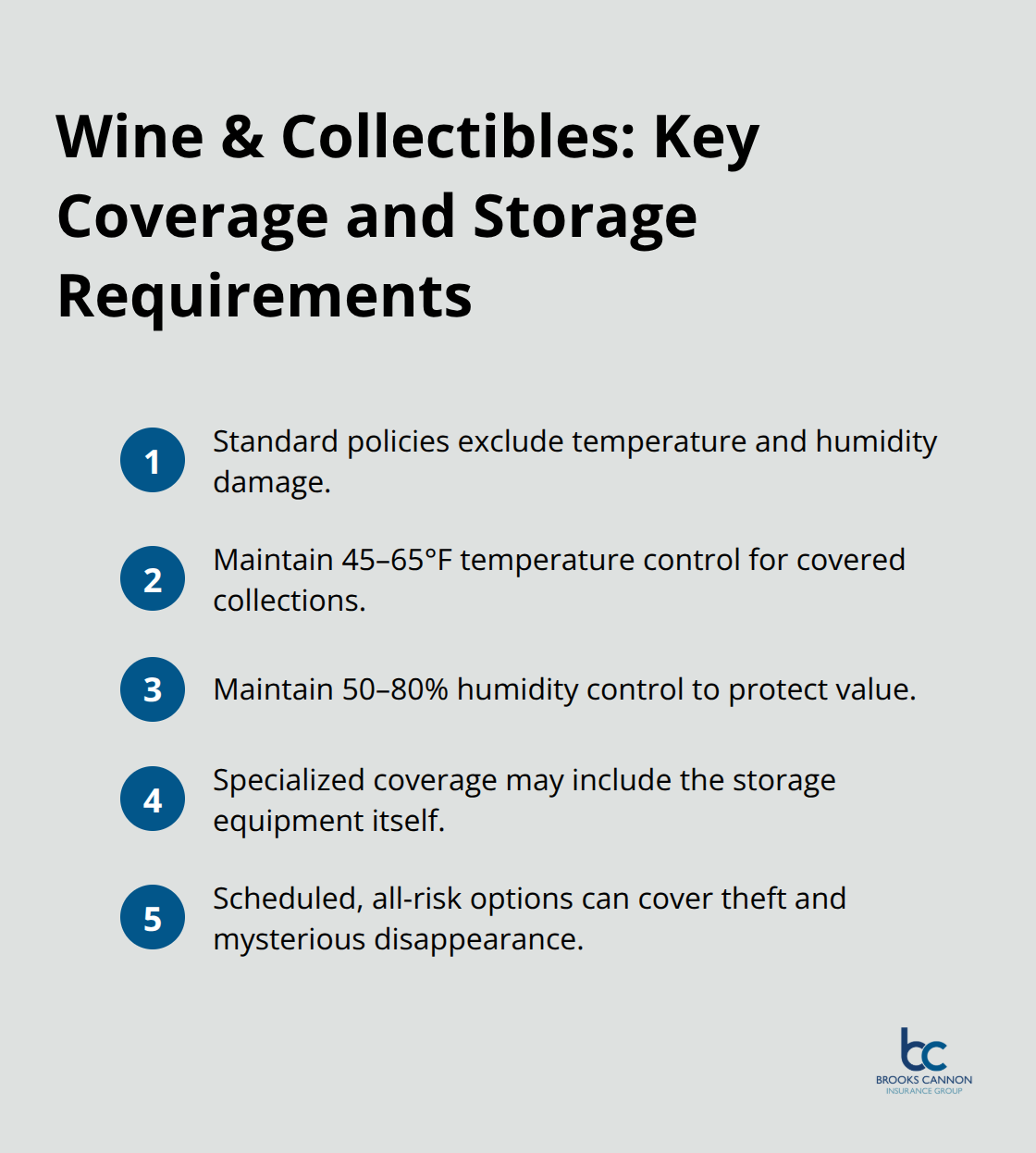

Wine collections and other valuables demand coverage that recognizes both the items themselves and their storage environment. Standard policies exclude temperature and humidity damage, which means a wine collection stored in improper conditions receives no coverage despite being insured. Specialized wine and collectibles coverage requires documentation of proper storage systems, typically including temperature control maintaining 45-65 degrees Fahrenheit and humidity control between 50-80 percent. This requirement actually benefits you because proper storage preserves your collection’s value independent of insurance considerations. Coverage extends beyond the wine itself to include the specialized storage equipment, making this investment deductible from your overall protection strategy.

Antiques, vintage furniture, and other collectibles follow similar patterns where specialized endorsements provide higher limits and broader coverage than standard policies allow. Many luxury carriers now offer all-risk coverage for scheduled collectibles, protecting against damage, theft, and mysterious disappearance without requiring proof of how loss occurred.

Smart Home Systems and Advanced Security

Modern luxury homes increasingly include sophisticated smart home technology and security systems that standard policies either exclude or severely limit. Advanced water detection with automatic shut-off systems, 24/7 monitored security, and integrated smart home platforms represent significant investments that deserve dedicated coverage. Some luxury carriers offer coverage for these systems as standalone endorsements, recognizing that the cost to replace smart home integration across a high-end property can reach $50,000-$150,000 depending on system sophistication. More importantly, insurers increasingly require these systems as loss prevention conditions for coverage, meaning your premium may decrease substantially once you implement recommended protections. This creates a direct financial incentive to invest in technology that reduces your risk profile. Dallas homeowners should discuss specific system requirements with their agent before purchasing, because carriers have different standards regarding monitoring, integration, and maintenance. Some policies even cover the cost of upgrades, essentially paying you to implement risk reduction measures that benefit both your property and the insurer’s loss exposure.

Final Thoughts

Luxury home insurance protects what standard policies cannot, and the difference becomes starkly apparent when loss occurs. Your Dallas-area home worth $1 million or more demands coverage that recognizes replacement cost rather than market value, accounts for specialized materials and custom features, and protects valuable collections that standard policies leave exposed. Standard policies depreciate your roof, cap jewelry coverage at a fraction of its actual value, and leave you personally funding the gap between what insurance pays and what genuine restoration costs-luxury policies eliminate these gaps through guaranteed replacement cost coverage and scheduled personal property protection.

Choosing the right luxury home insurance policy requires working with agents who understand high-value properties and the carriers that specialize in them. Your agent should conduct a thorough assessment of your home’s replacement cost, evaluate your collections and personal property, and identify coverage gaps before loss strikes. This process involves detailed conversations about your architectural features, built-in amenities, security systems, and asset values so your policy reflects your actual situation rather than generic assumptions.

Contact Brooks Cannon Insurance Group to schedule a comprehensive coverage review of your luxury home. Our licensed experts understand Dallas-area luxury properties and the specialized protection they require, and we work with multiple top-rated insurance carriers to find the best coverage for your unique situation. Protecting your luxury home properly costs far less than recovering from underinsurance after loss occurs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation