Running an online business in the Dallas area comes with distinct challenges that brick-and-mortar stores simply don’t face. Cyber attacks, payment fraud, and product liability issues can threaten your operation overnight.

At Brooks Cannon Insurance Group, we’ve helped countless e-commerce business owners understand what insurance for online business owners actually means in practice. The right coverage protects your revenue, your customer data, and your reputation when things go wrong.

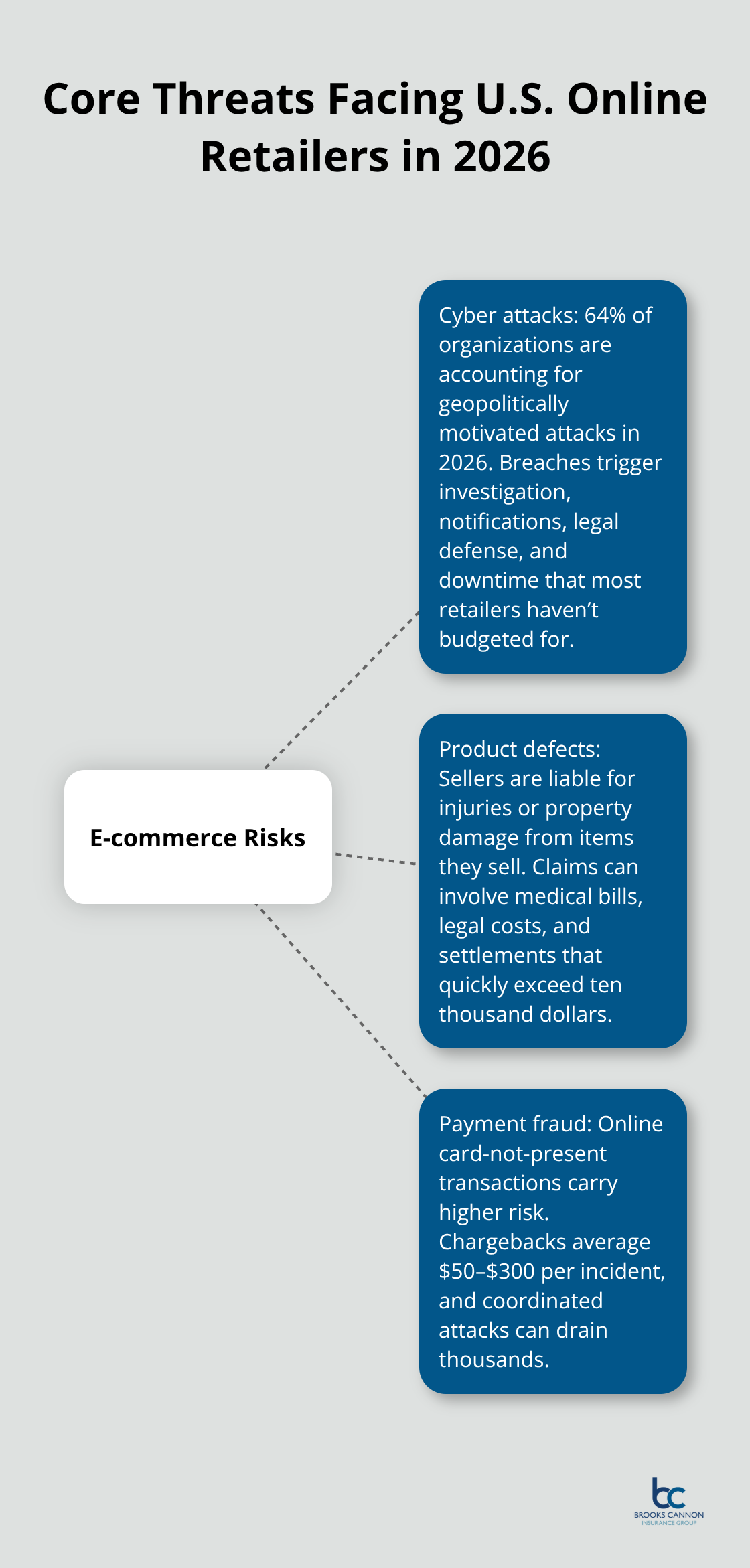

What Threatens Your Online Business Most

Cyber attacks pose the biggest operational risk

64% of organizations are accounting for geopolitically motivated cyberattacks in 2026, making cyber threats a critical concern for online retailers. More than 11 million U.S. e-commerce stores operate today, generating over 1.2 trillion dollars in annual sales, making them attractive targets for criminals.

A data breach that exposes customer payment information can halt your operations for weeks while you manage notifications, credit monitoring, and regulatory compliance. The costs spiral quickly: forensic investigation, customer notification, credit monitoring services, legal defense, and potential settlements create expenses that most online businesses haven’t budgeted for. Cyber liability insurance covers breach response costs, customer notifications, legal expenses, and business interruption losses that your general liability policy won’t touch.

Product defects create serious financial exposure

When you sell physical products online, you become liable for injuries or property damage those products cause. A defective item that reaches a customer in Dallas or anywhere else becomes your legal responsibility. Someone purchases a faulty electrical device from your store that causes a fire, or a product with inadequate safety warnings injures a child. Product liability claims involve medical bills, legal defense costs, and potential settlements that quickly exceed ten thousand dollars. Many online retailers underestimate this risk because they believe their marketplace listing or supplier bears the responsibility-they don’t. You’re the seller, and you’re accountable. Standalone product liability insurance or a comprehensive Business Owner’s Policy protects you from these claims. Carriers specifically recommend product liability as essential for online retailers selling higher-risk items like electronics, sporting goods, or items with heat exposure.

Payment fraud and chargebacks drain cash flow

Payment processing fraud happens constantly in e-commerce. Criminals use stolen credit cards to purchase inventory from your store, leaving you with the chargeback liability and lost merchandise. Your payment processor may hold funds during disputes, freezing cash you need for operations. Unlike physical stores where customers present cards in person, online transactions carry higher fraud risk because you can’t verify the cardholder’s identity in real time. Chargebacks average fifty to three hundred dollars per incident, but a coordinated fraud attack can drain thousands. While general liability and cyber insurance don’t cover fraud losses, you can implement fraud detection tools and maintain detailed transaction records to protect your business. An insurance professional who understands e-commerce operations helps you identify coverage gaps that standard policies overlook-and that’s where the right insurance solutions become essential for your operation.

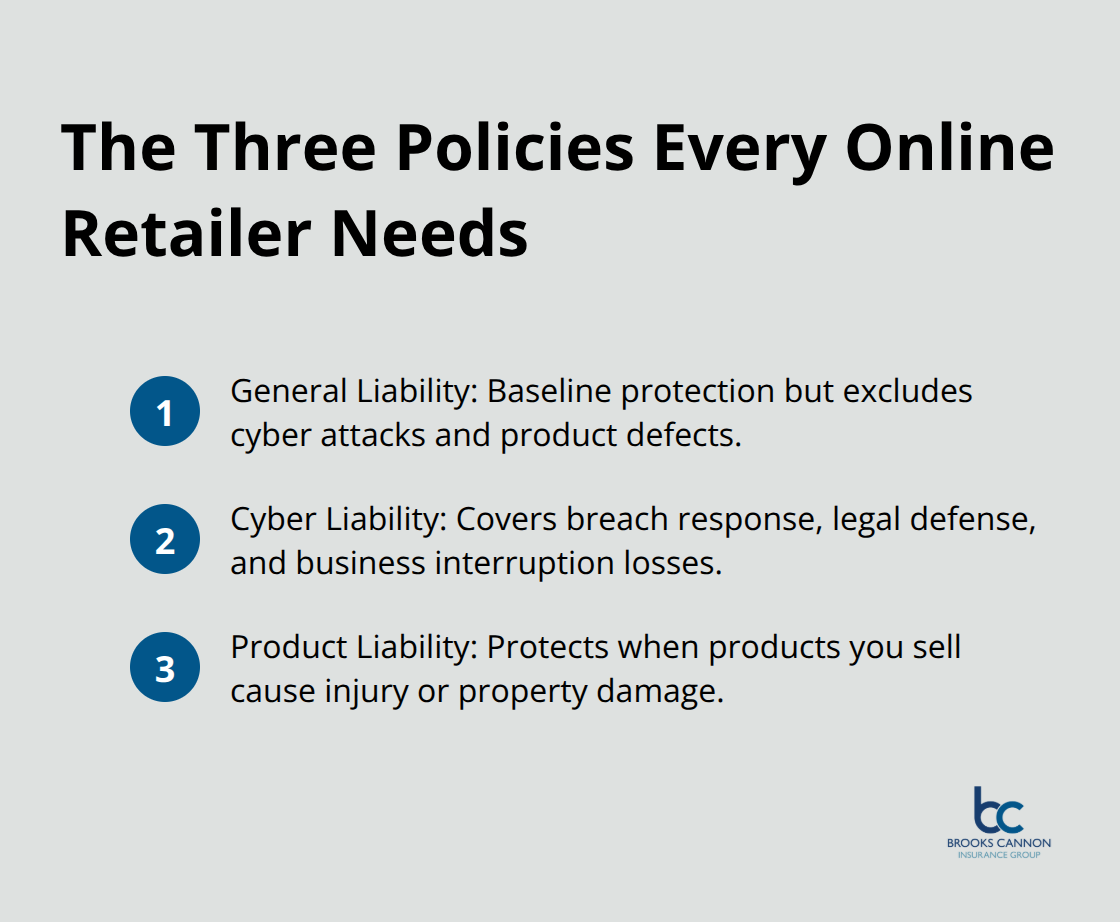

The Three Policies Every Online Retailer Needs

General Liability: Your Foundation Coverage

General liability insurance forms the foundation of your protection, though it cannot stand alone. Most online retailers start here because it costs less and marketplaces like Amazon often require proof of coverage before you list products. This policy protects you against third-party claims when a customer suffers injury on your premises or your advertising harms someone’s reputation. However, it explicitly excludes cyber attacks, data breaches, and product defects-the exact risks that threaten e-commerce operations most. You need this policy, but treating it as your only coverage leaves dangerous gaps.

General liability can cost as little as $19 per month for some businesses, making it an accessible starting point that you should never skip.

Cyber Liability: Protection Against Data Breaches

Cyber liability insurance becomes non-negotiable the moment you handle customer payment information or store personal data. This policy covers the actual costs of a data breach: forensic investigation, customer notification, credit monitoring services, legal defense, regulatory fines, and business interruption losses. Standard general liability policies explicitly exclude these expenses, which means a breach would drain your cash reserves entirely. Since more than 11 million e-commerce stores operate in the U.S., attackers target online retailers constantly. Cyber liability premiums range from five hundred to two thousand dollars annually depending on your revenue, the amount of customer data you store, and your security practices. Carriers reward businesses that implement two-factor authentication, encrypted payment processing, and regular security updates with lower rates.

Product Liability: Accountability for What You Sell

Product liability insurance protects you when items you sell cause injury or property damage, regardless of whether you manufactured them or sourced them from suppliers. A defective smartphone battery that catches fire, a sporting good with inadequate safety warnings, or a children’s toy with toxic materials-you become liable, not your supplier. Product liability claims often exceed twenty thousand dollars when medical treatment and legal defense are involved. Standalone product liability policies typically cost between six hundred and two thousand dollars annually.

Bundling Coverage for Maximum Efficiency

You can bundle all three coverages into a Business Owner’s Policy that combines general liability, commercial property, and business income insurance at a lower total cost than purchasing separately. Most online retailers in the Dallas area benefit from a BOP paired with standalone cyber liability, which provides comprehensive protection without overpaying for redundant coverage. This combination addresses your most pressing risks while keeping your annual insurance costs manageable. As your business grows and your product mix changes, your coverage needs will shift-which is why the next step involves assessing your specific risks and working with an insurance professional to tailor your protection.

How to Choose Your Coverage

Assess Your Specific Business Risks

The gap between what online retailers think they need and what actually protects them widens every day. Start with a risk assessment specific to your operation, not a generic checklist. If you sell electronics or high-heat items like lava lamps, product liability becomes your priority because defect claims in those categories run higher. If you handle customer payment data directly rather than using a payment processor that tokenizes transactions, cyber liability moves to the top. If you store inventory in a warehouse or someone else’s facility, commercial property coverage prevents catastrophic loss.

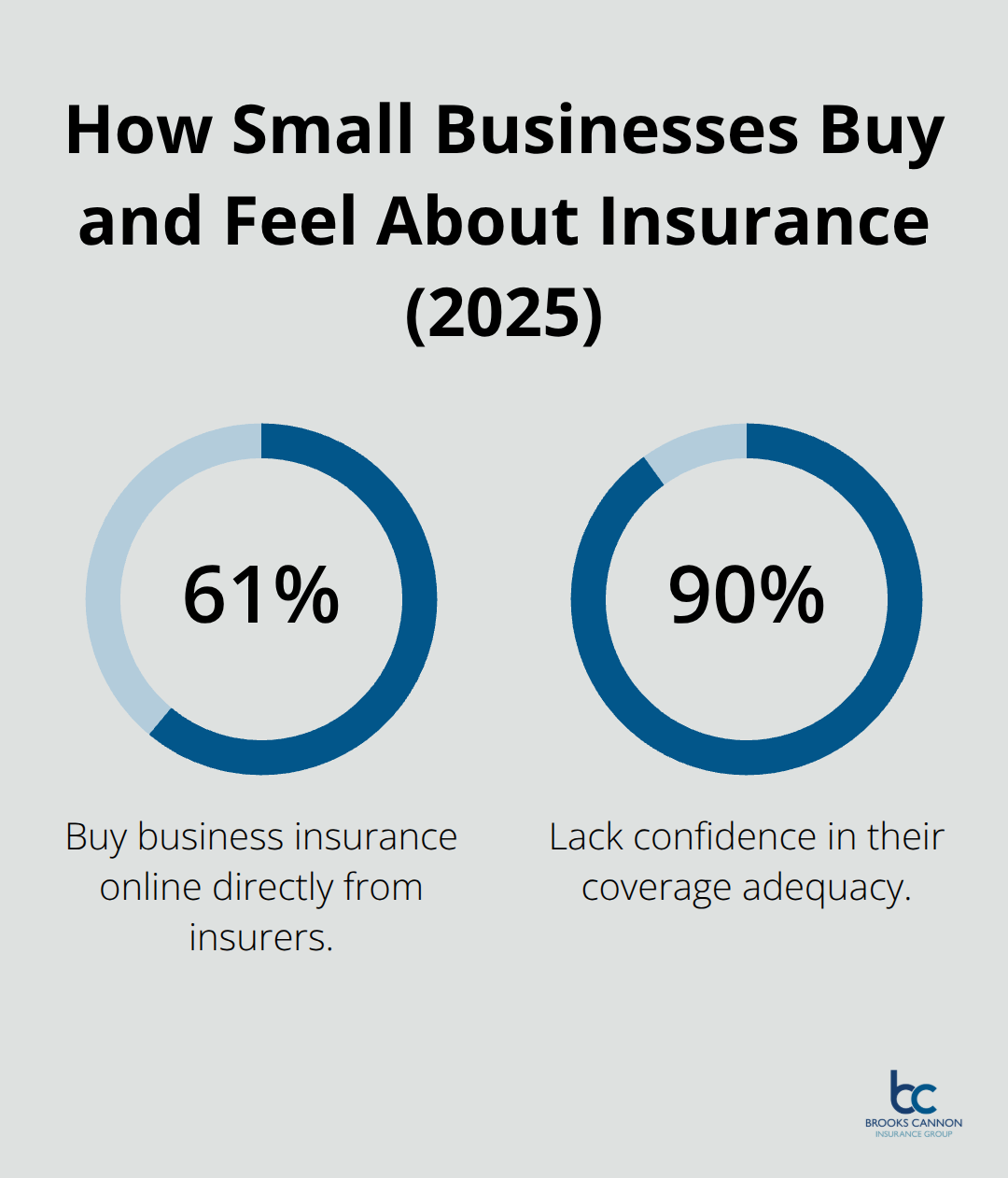

A NEXT survey of 1,500 small business owners in January 2025 found that 61% now buy business insurance online directly from insurers, and 90% of respondents lack confidence in their coverage adequacy. That confidence gap exists because most owners skip the assessment step entirely and buy whatever their marketplace requires or what sounds cheapest.

Your Dallas location matters too: local property values, crime rates, and liability trends affect pricing and coverage recommendations. Document what you actually sell, where you store it, how many employees handle customer data, and whether you ship nationwide or internationally. This documentation becomes your roadmap when comparing quotes.

Compare Coverage Options and Pricing

Once you know your actual risks, pricing becomes straightforward. A Business Owner’s Policy bundled with cyber liability typically costs between one thousand five hundred and three thousand dollars annually for online retailers generating under five hundred thousand dollars in revenue, according to industry data. Raising your deductible from five hundred to two thousand five hundred dollars lowers your monthly premium significantly if you rarely file claims. Carriers reward security investments: implementing two-factor authentication, encrypted payment processing, and regular security updates directly reduces your cyber liability premium.

Get quotes from at least three carriers because pricing varies wildly based on how each insurer underwrites e-commerce risk. When you receive quotes, ask each carrier specifically what product categories they exclude or charge higher rates for, since some insurers won’t cover certain items at standard rates. An insurance professional who understands e-commerce operations identifies coverage gaps that online retailers consistently miss, like the fact that homeowner’s policies explicitly exclude business inventory and that general liability alone leaves you exposed to the exact risks that threaten your revenue most.

Work with an Insurance Professional

As an independent agency based in Dallas, Brooks Cannon Insurance Group works with multiple top-rated carriers to find coverage that matches your actual operation and budget, not a one-size-fits-all template. Our team identifies the specific gaps in your protection and connects you with policies designed for e-commerce retailers. We understand how online operations differ from traditional retail, and we tailor recommendations to your product categories, revenue level, and growth plans.

Final Thoughts

Insurance for online business owners protects your operation from the specific threats that e-commerce retailers face daily. General liability satisfies marketplace requirements and protects against customer injury claims, while cyber liability covers the breach response costs that would otherwise devastate your cash flow. Product liability holds you accountable for the items you sell, regardless of where they came from, and together these policies transform your operation from vulnerable to protected.

Comprehensive coverage delivers benefits that extend far beyond financial protection. When you hold current certificates of insurance, you qualify for contracts and partnerships that uninsured competitors cannot access, and customers trust retailers who demonstrate insurance coverage because it signals stability and accountability. Your ability to win larger accounts, negotiate better terms with suppliers, and expand into new markets all improve when you have documented protection in place.

Document your specific risks, get quotes from multiple carriers, and connect with an insurance professional who understands e-commerce operations. We at Brooks Cannon Insurance Group work with top-rated carriers to find coverage that matches your actual business, and our Dallas-based team identifies the gaps that online retailers consistently miss. Contact us today to discuss your coverage needs and protect your e-commerce business.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation