Running a small business in Dallas means protecting yourself from unexpected liability claims. Whether you operate a retail shop, offer services, or run a consulting firm, the right general liability insurance shields your company from costly lawsuits and medical bills.

We at Brooks Cannon Insurance Group help business owners find the best general liability insurance for their specific needs. This guide walks you through what coverage actually protects you, which businesses need it most, and how to pick a policy that fits your operation.

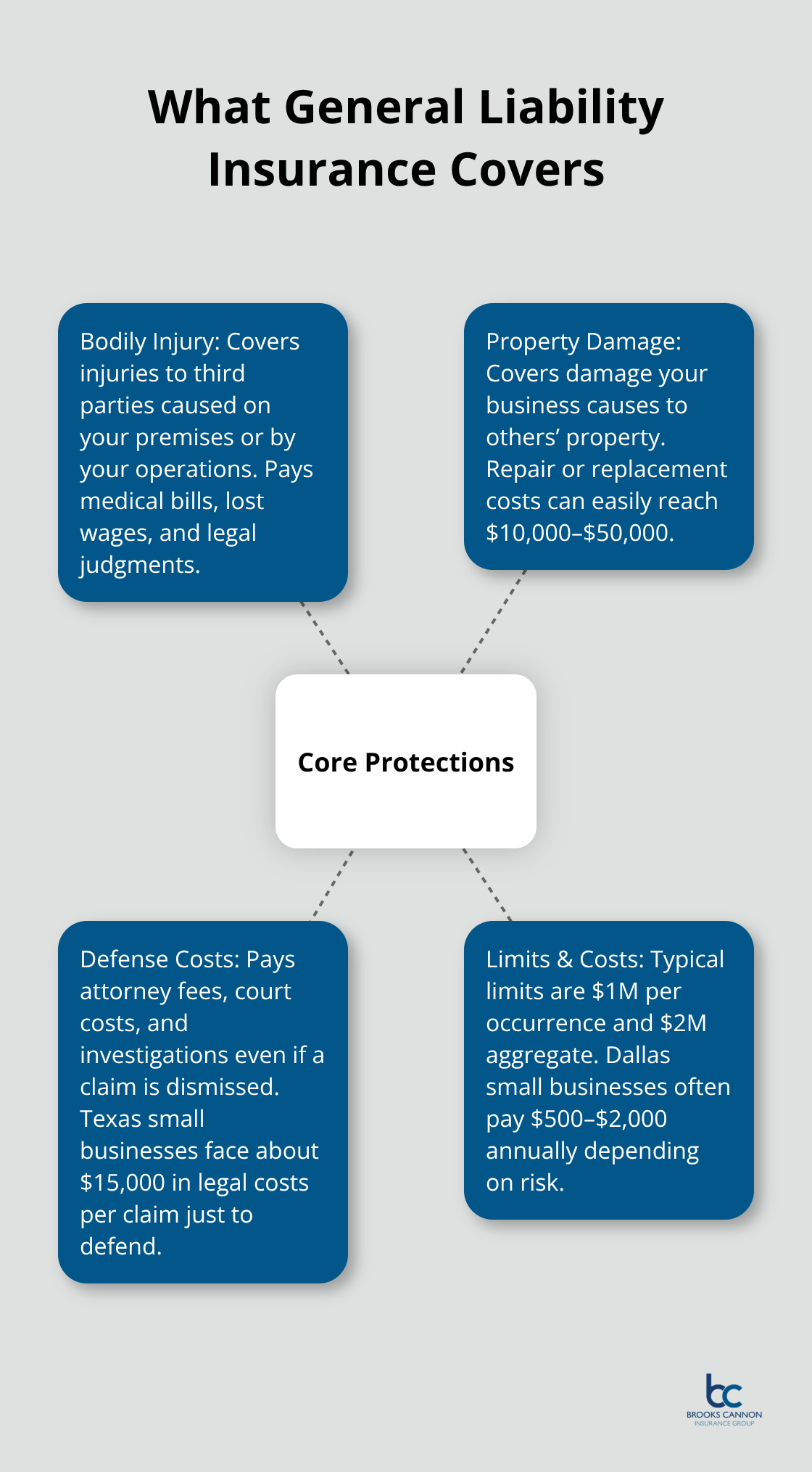

What General Liability Insurance Actually Protects

Bodily Injury Claims Cost More Than You Think

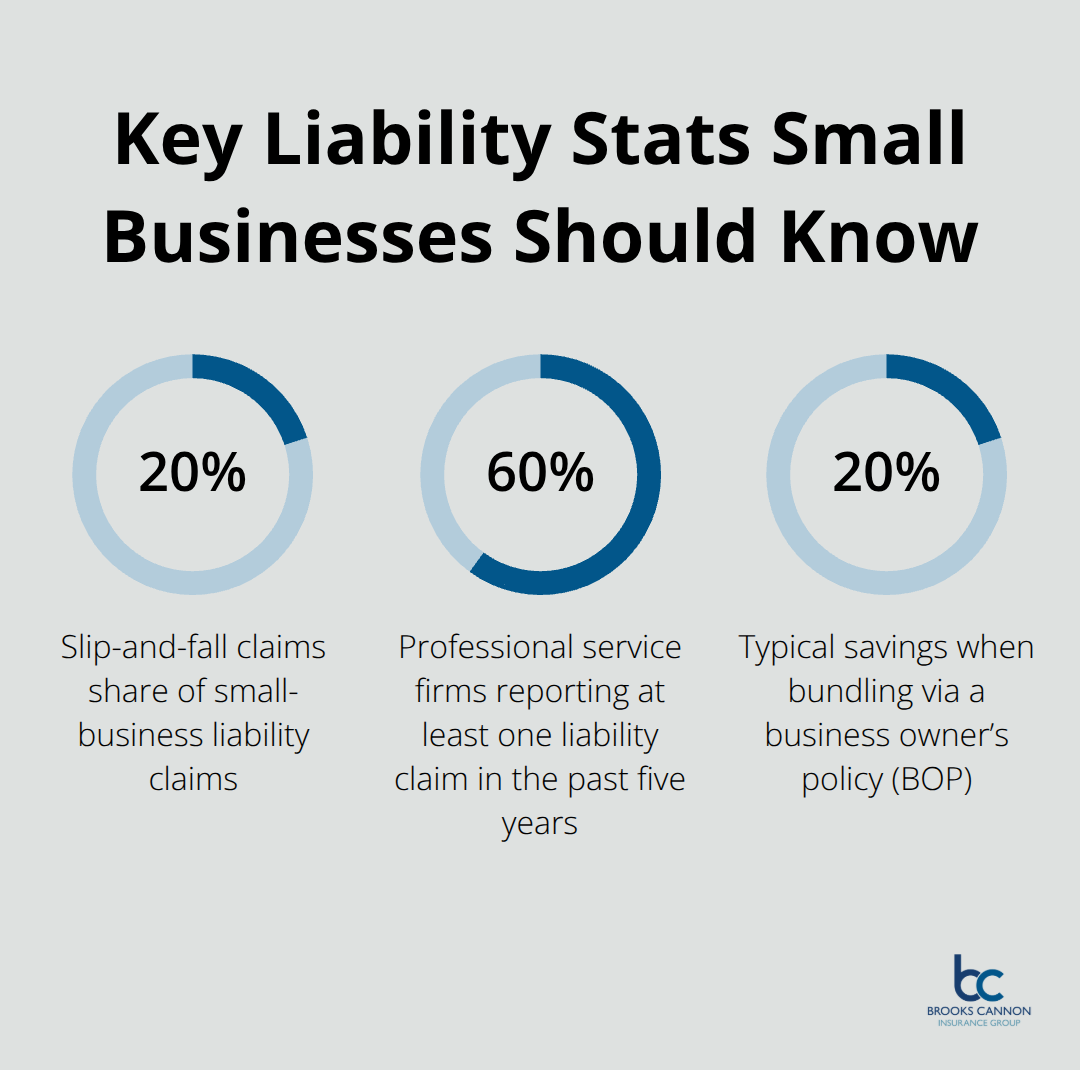

General liability insurance covers three critical areas that can drain your business finances fast. First, bodily injury claims happen when someone gets hurt on your property or because of your business operations. Slip-and-fall injuries account for roughly 20 percent of small-business liability claims, with the average claim hitting around $45,000. If a customer trips in your retail space or a client gets injured during a service call, this coverage pays their medical bills, lost wages, and legal judgments.

Property Damage Liability Protects Your Finances

The second protection is property damage liability, which covers damage your business causes to someone else’s property. This could mean you accidentally damage a client’s equipment, your delivery vehicle hits a parked car, or your operations cause structural damage to a rented space. Without this coverage, you’d pay out of pocket for repairs or replacement costs that easily exceed $10,000 to $50,000 depending on what gets damaged.

Defense Costs Add Up Faster Than Claims Themselves

The third and often underestimated protection is defense costs and legal fees. When someone sues your business, your insurer pays the attorney fees, court costs, and investigation expenses even if the claim gets dismissed. This matters tremendously because a 2024 study shows small Texas businesses face about $15,000 in legal costs per claim just to defend themselves. Many small-business owners think they only need liability insurance if they expect a major incident, but that’s backwards. You need it specifically because lawsuits happen unexpectedly and cost money to fight regardless of who’s at fault.

Coverage Limits and Costs Vary by Industry

General liability policies typically include $1 million per occurrence and $2 million aggregate limits, though you can adjust these based on your risk profile. For Dallas small businesses, typical costs run $500 to $2,000 annually depending on your industry and operations. Construction companies and restaurants pay more because they carry higher risk, while consulting firms and home-based businesses often pay less. The point is straightforward: general liability insurance doesn’t just cover settlements and judgments-it covers the entire legal process that protects your business from financial collapse.

Now that you understand what general liability insurance covers, the next step is identifying whether your specific business type requires this protection and how much coverage fits your operation.

Types of Businesses That Need General Liability Insurance

Every business operating in Dallas needs general liability insurance, but some industries face far greater exposure than others. Retail businesses, service contractors, and professional firms each encounter distinct liability risks that demand specific coverage amounts. Understanding your industry’s actual claim patterns and legal requirements determines whether your current coverage protects you adequately or leaves you dangerously exposed.

Retail and E-Commerce Businesses Face Daily Customer Risk

Retail and e-commerce businesses face constant bodily injury risk because customers interact directly with your space and products daily. A slip-and-fall in your store, a customer injured by defective merchandise, or damage caused by your operations can trigger lawsuits that cost tens of thousands to defend. The Hartford’s 2025 data shows slip-and-fall claims represent about 20 percent of small-business liability claims, averaging $45,000 per incident.

If you operate a retail storefront in Dallas, you should carry at least $1 million per occurrence coverage because landlords and shopping centers typically require proof of insurance before leasing space. E-commerce businesses that ship products face product liability exposure, meaning your general liability policy must explicitly cover products you manufacture or distribute. Many online retailers underestimate this risk and discover too late that standard policies exclude product liability unless specifically endorsed.

Service Contractors and Construction Companies Handle High-Risk Work

Service-based companies and contractors encounter liability from their work itself. A plumber who damages a client’s water line, an electrician whose faulty installation causes a fire, or a cleaning service that breaks expensive equipment all face claims exceeding $50,000. Construction companies face even steeper exposure, with annual general liability costs running $3,000 to $5,000 because the work involves physical hazards and property damage potential. Texas does not require workers’ compensation for most businesses, but if you employ even one person, you should pair general liability with workers’ compensation coverage because employee injuries can trigger lawsuits that exceed standard liability limits. Contractors working on government projects or commercial properties almost always face mandatory insurance requirements, with clients demanding certificates of insurance within 24 hours to meet bid deadlines according to 2024 Dallas Chamber of Commerce data.

Professional Services Firms Need Specialized Coverage

Professional services firms including accountants, consultants, attorneys, and financial advisors need professional liability (errors and omissions) insurance alongside general liability. According to NAIC data, 60 percent of professional service firms reported at least one liability claim in the past five years, with average legal costs around $25,000 per claim. A consultant’s poor advice, an accountant’s missed deduction, or a financial advisor’s unsuitable recommendation can trigger claims that general liability alone will not cover. These firms typically pay $600 to $1,800 annually for professional liability coverage depending on their specialty and revenue. The combination of general liability and professional liability creates a comprehensive protection strategy that addresses both third-party claims and errors in your professional work.

Identifying your industry’s specific risks and coverage requirements sets the foundation for selecting the right policy limits and deductibles that actually match your operation.

How to Choose the Right General Liability Policy

Calculate Your Specific Liability Risk

Your industry determines how much general liability coverage you actually need, and guessing wrong leaves you dangerously exposed. Start with your specific liability risk based on customer interaction, property damage potential, and regulatory requirements rather than picking arbitrary limits. A retail store with high foot traffic and expensive inventory needs far different coverage than a home-based consulting firm. Construction companies should carry at least $2 million per occurrence because a single accident on a job site can easily exceed $1 million in damages and legal costs. Restaurants and food service businesses need $1 to $2 million per occurrence minimum because of slip-and-fall exposure and food contamination claims. Professional services firms should match their coverage limits to their revenue and client contract requirements, typically starting at $1 million per occurrence.

The Texas Department of Insurance recommends reviewing your lease agreements, client contracts, and vendor requirements because most will specify minimum coverage amounts you must carry before they’ll work with you. Many small-business owners discover during contract negotiations that they’re underinsured, forcing them to buy additional coverage mid-year at higher rates. Start this assessment now, not when a potential client asks for your certificate of insurance.

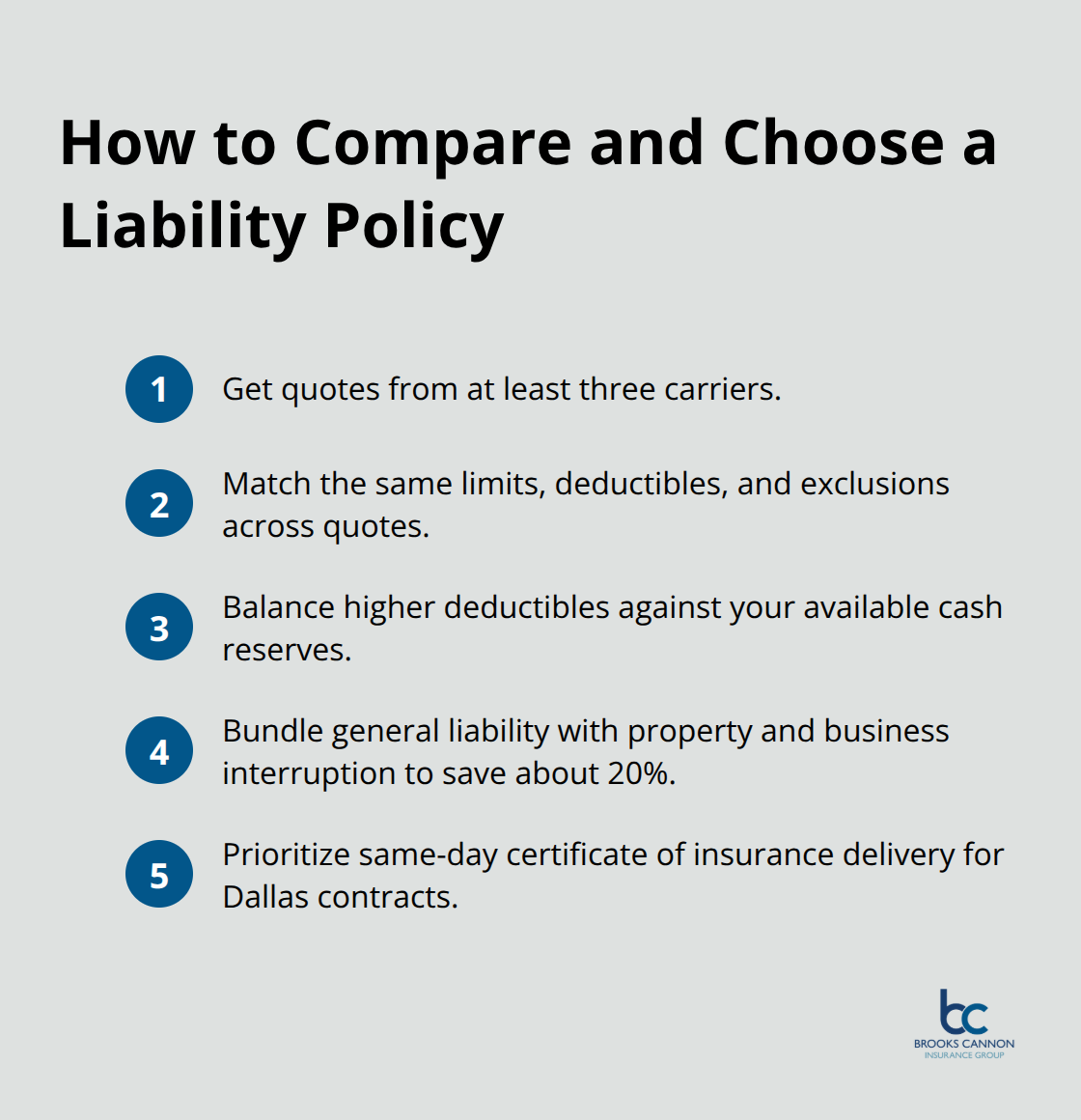

Compare Quotes Across Multiple Carriers

Comparing quotes from multiple carriers matters far more than finding the cheapest option because a lower premium often means reduced coverage or higher deductibles that cost you thousands when a claim happens. Get quotes from at least three carriers and compare the exact same limits, deductibles, and exclusions across all quotes because premium differences of $200 to $500 annually are common for identical coverage. Higher deductibles ($2,500 or $5,000) significantly reduce your monthly premium but increase your out-of-pocket costs when a claim occurs, so balance savings against your ability to pay.

A $1,000 deductible might save you $30 per month compared to a $500 deductible, but that’s only worthwhile if you have $1,000 cash reserves available when you need it. Bundling general liability with commercial property and business interruption coverage through a business owner’s policy typically saves 20 percent compared to buying policies separately, according to industry data.

Prioritize Same-Day Certificate Delivery

Request quotes that include same-day certificate of insurance delivery because Dallas contracts frequently require COIs within 24 hours, and an insurer that can’t meet that timeline creates unnecessary delays. An insurer’s ability to issue certificates quickly determines whether you can respond to bid deadlines and contract opportunities without losing deals to competitors. This operational capability matters as much as the premium itself when you’re competing for Dallas commercial work.

Final Thoughts

Selecting the best general liability insurance for small business requires balancing adequate coverage limits that match your actual risk, affordable premiums that fit your budget, and an insurer capable of delivering certificates quickly when Dallas contracts demand them. Your industry, customer interaction level, and contractual requirements should drive your coverage decisions, not generic recommendations or competitor policies. A retail store needs different limits than a consulting firm, and a construction company needs dramatically more protection than either.

Working with an insurance agent transforms this process from overwhelming to straightforward. We at Brooks Cannon Insurance Group understand Dallas business risks because we work with local companies daily and know which carriers respond fastest to claims and which ones create headaches during the process. An independent agent accesses multiple carriers simultaneously, compares identical coverage across quotes, and identifies which endorsements your specific business actually needs rather than selling you unnecessary add-ons.

Contact Brooks Cannon Insurance Group to discuss your specific business risks and receive quotes from multiple top-rated carriers. Provide details about your industry, number of employees, annual revenue, and any client or landlord insurance requirements so we can recommend appropriate limits and deductibles. Most small-business owners complete this process in one conversation and gain peace of mind knowing their business has the protection it needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation