Carpenter general liability insurance protects your business when accidents happen on job sites. One slip, one injury, or one damaged client property can cost you thousands-or even shut down your business.

We at Brooks Cannon Insurance Group work with carpenters across Dallas to find coverage that actually fits their work. This guide walks you through what you need to know and how to get protected.

What General Liability Actually Covers for Carpenters

Two Core Protections Every Carpenter Needs

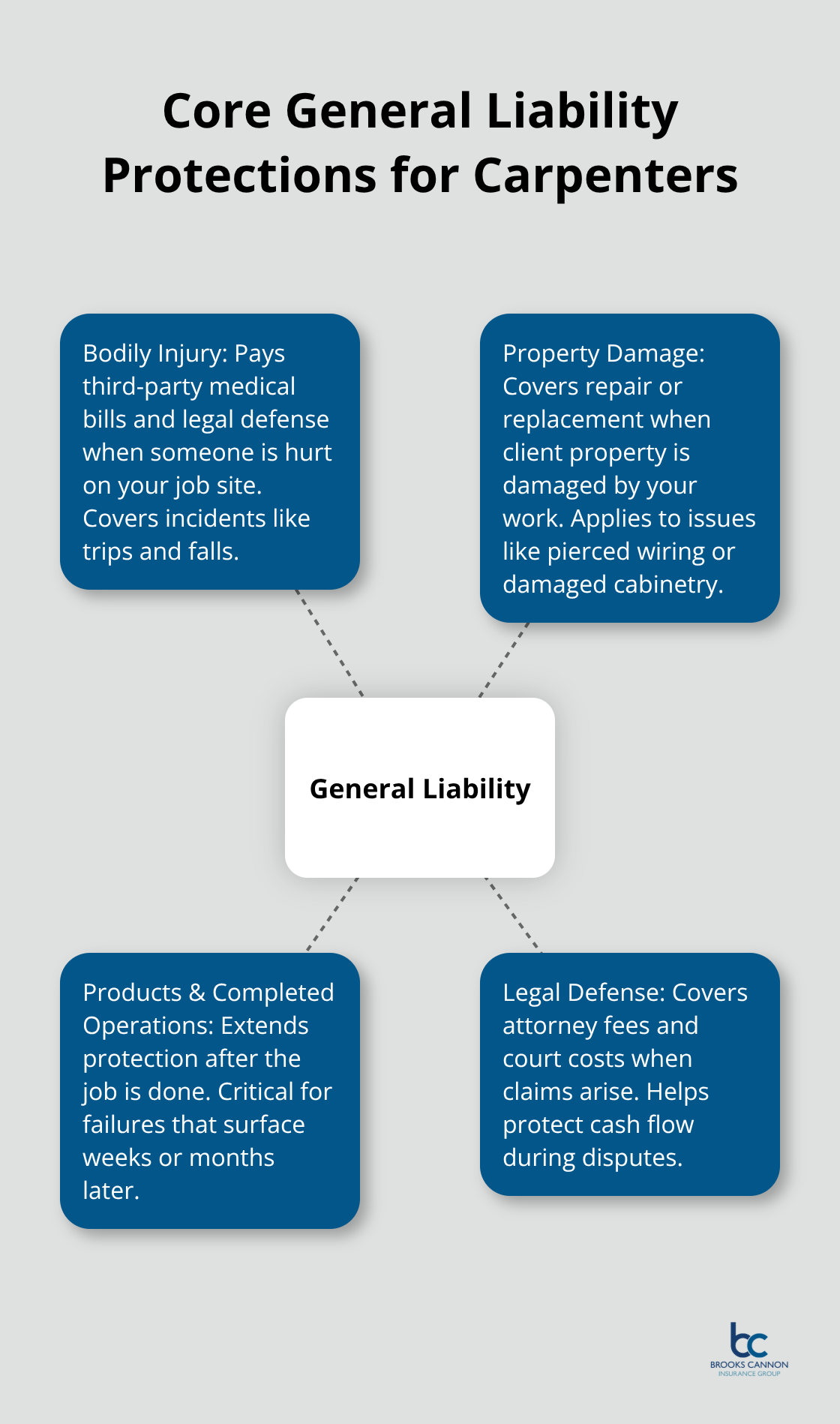

General liability insurance pays for two things carpenters face constantly on job sites: bodily injury to someone else and damage to someone else’s property. If a client trips over your tools and breaks their arm, general liability covers their medical bills and legal costs if they sue. If you accidentally drive a nail through a client’s electrical wire or damage their kitchen cabinets during installation, the policy pays for repairs or replacement. These are not theoretical scenarios-they represent the exact losses that shut down carpentry businesses every year.

Why Property Damage Claims Hit Carpenters Hard

Carpenters face higher liability risk than many other trades because your work happens inside clients’ homes and businesses where people live and work. A mistake in framing, cabinetry, or finish work can cause injuries weeks or months after you leave the job site. This is why Products and Completed Operations coverage matters so much-it protects you if cabinets fail or stairs become unsafe after project completion.

Coverage Limits and Dallas Requirements

Most general contractors and property owners in Dallas won’t hire you without proof of coverage, and many require minimum limits of $1,000,000 per occurrence and $2,000,000 aggregate. Dallas building permits often require proof of general liability insurance with limits between $300,000 and $1,000,000 before inspectors will approve your work. Without this protection, a single accident wipes out your personal savings and forces you out of business.

What Coverage Actually Costs

The cost for adequate coverage runs between $1,000 and $1,450 annually for small carpentry businesses, far less than the cost of defending a single liability claim without insurance. Unlike electricians or plumbers who typically work on isolated systems, your carpentry touches the structural integrity and livability of entire spaces. This protection is not optional if you want steady work in the Dallas market.

Now that you understand what general liability covers and why it matters, the next step is figuring out exactly how much coverage you need and which carriers offer the best rates for your specific carpentry work.

Steps to Get Carpenter General Liability Insurance

Audit Your Work Type and Project Scope

The first mistake carpenters make is buying insurance without knowing what they actually need. You cannot walk into this decision blind. Start by auditing your actual work. Are you doing rough framing on new construction, or finish carpentry in occupied homes? Rough framing carries significantly higher risk premiums because of fall hazards and structural liability, while finish work like cabinetry or trim typically costs less to insure. Next, calculate your typical project value and the size of spaces you work in. A $50,000 kitchen remodel inside a client’s home demands different coverage than a $500,000 commercial build-out.

Understand Dallas Permit and Client Requirements

Dallas permit requirements typically demand coverage, but your actual needs may exceed those minimums depending on the scope of work you bid. Most general contractors and property owners in Dallas won’t hire you without proof of coverage, and many require minimum limits of $1,000,000 per occurrence and $2,000,000 aggregate. Before you request quotes, verify what your specific clients and local permit offices require-this prevents you from over-insuring or under-protecting your business.

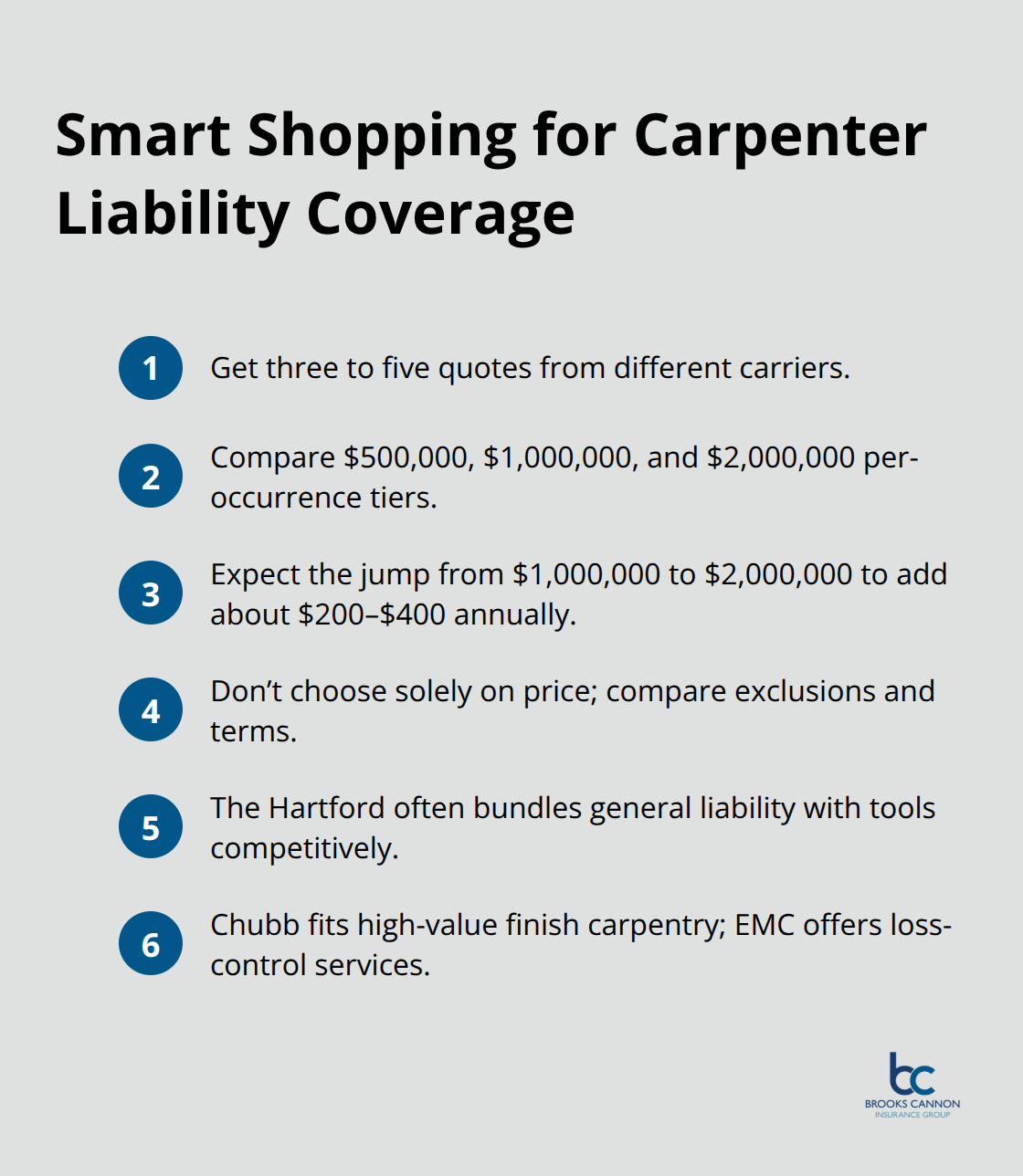

Compare Multiple Carriers and Coverage Tiers

Talk to three to five carriers directly and request quotes for different coverage levels-$500,000, $1,000,000, and $2,000,000 per occurrence. The price difference between these tiers is often smaller than carpenters expect, and jumping from $1,000,000 to $2,000,000 might only cost an extra $200 to $400 annually. Do not assume the cheapest quote is the best deal.

The Hartford bundles general liability with tools coverage competitively, while Chubb offers stronger terms for finish carpenters handling high-value installations. EMC Insurance’s Artisan Contractors program includes loss-control services that can actually lower your premiums over time if you implement their safety recommendations.

Work with an Agent to Close Coverage Gaps

An independent agent can pull quotes from multiple carriers simultaneously and explain exactly what each policy excludes or limits. This matters because standard policies sometimes exclude coverage for defective workmanship or design flaws-gaps that can wreck you financially. An independent agent also verifies that any subcontractors you hire carry their own general liability, protecting you from exposure if they cause damage. When you request a quote, have your business revenue, payroll figures if you have employees, and a description of your typical projects ready. Most carriers ask for these specifics because a carpenter earning $150,000 annually with no employees pays roughly $1,000 to $1,450 per year, while one earning $500,000 with five employees pays significantly more.

Activate Your Policy and Obtain Certificates

Request certificates of insurance from your chosen carrier immediately after purchase-many Dallas job sites require proof of coverage before you can start work, and digital certificates can be issued within hours of policy activation. Once your policy activates, you can present proof of coverage to clients and permit offices, removing a major barrier to landing projects. With your general liability in place, you now need to address the coverage gaps that liability alone cannot fill.

What General Liability Doesn’t Cover

General liability insurance stops short of protecting your tools, your workers, and specialized project risks that carpenters face constantly. A $1,000,000 general liability policy sounds comprehensive until a client’s site gets broken into and thieves steal your $15,000 trailer full of equipment, or one of your employees gets hurt and files a workers compensation claim you’re not prepared to handle. These gaps destroy carpentry businesses faster than any liability claim because they hit your ability to work immediately.

Tools and Equipment Need Separate Protection

Your tools and equipment need dedicated protection because general liability explicitly excludes coverage for your own business property. If your truck gets broken into on a job site and thieves take your power tools, saws, and nail guns worth $12,000, general liability pays nothing. Inland Marine coverage protects tools in transit and at job sites, and for a small carpentry operation with typical equipment, annual costs run between $180 and $360.

The Hartford and other carriers bundle this coverage into Business Owner’s Policies, which often costs less than buying liability and tools separately.

Workers Compensation Protects Your Team and Your Business

Workers compensation is not optional if you have employees-Texas does not require it statewide for most contractors, but every general contractor in Dallas requires proof of workers compensation before hiring subcontractors, and most clients write it into their contracts. For a small operation with $150,000 in payroll, workers compensation runs $3,000 to $4,800 annually and covers medical bills, lost wages, and rehabilitation costs if someone gets hurt on your job. Without it, you cannot legally work for major GCs or property owners in the Dallas market.

Project-Specific Riders Close Critical Gaps

Project-specific riders address gaps that standard policies leave open-completed operations coverage extends your liability protection for months or years after job completion, which matters enormously for finish carpentry and cabinetry where failures often appear later. Design defect exclusions in standard policies can leave you exposed if a client claims your design or installation caused damage, so verify with your agent that your policy covers defective workmanship claims. Subcontractor liability is another gap: if you hire a subcontractor who causes damage, your general liability may not cover their work unless you add contractual liability coverage to your policy.

Bundle Coverage for Better Pricing and Protection

Request quotes that bundle general liability with tools coverage and workers compensation-carriers like EMC Insurance’s Artisan Contractors program price these combinations competitively and include loss-control services that can lower your premiums if you implement their safety recommendations. An independent agent can help you identify which riders matter most for your specific carpentry work and which carriers offer the best terms for your situation.

Final Thoughts

Carpenter general liability insurance protects your business when accidents happen on job sites, and the Dallas market demands proof of coverage before you step on any project. A single injury claim or property damage incident can wipe out years of profit without this protection, forcing you to shut down operations. When you combine general liability with tools coverage and workers compensation, you build a protection system that lets you focus on carpentry instead of financial ruin.

We at Brooks Cannon Insurance Group work with carpenters across Dallas to find coverage that fits your actual business. As an independent agency, we partner with multiple top-rated carriers so you access different options and pricing rather than getting locked into one choice. Our licensed experts identify gaps in your coverage, explain what each policy includes and excludes, and help you avoid paying for protection you don’t need while securing the limits that matter.

Request a quote for carpenter general liability insurance and the additional coverages your business needs-the process takes minutes and costs nothing. We pull options from multiple carriers, explain the differences, and help you activate coverage fast so you present certificates to clients and permit offices immediately.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation