One accident on a job site can cost your contracting business thousands of dollars in legal fees and settlements. That’s why commercial general liability insurance for contractors isn’t optional-it’s a business necessity.

We at Brooks Cannon Insurance Group help Dallas-area contractors understand their coverage options and protect what they’ve built. This guide walks you through what’s covered, why you need it, and how to select the right limits for your operation.

What Your Coverage Actually Protects

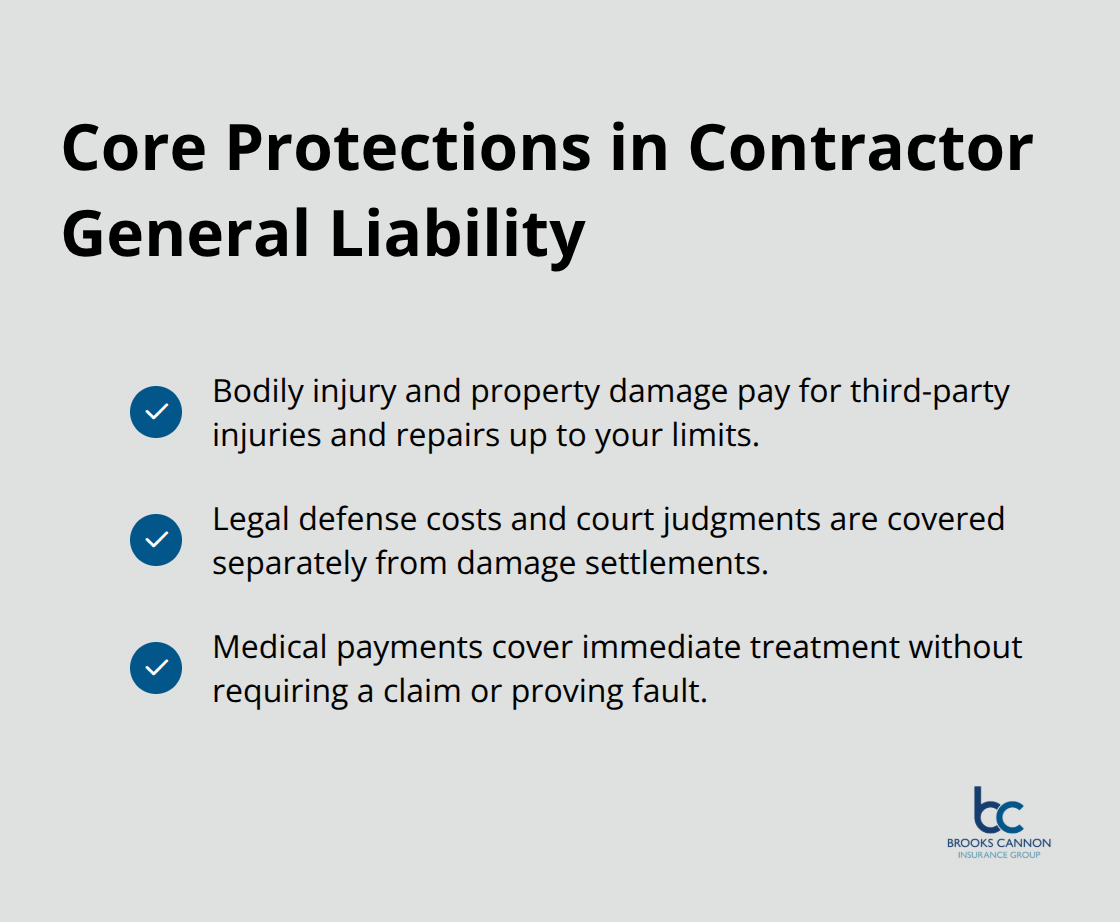

Bodily Injury, Property Damage, and Medical Payments

Commercial general liability insurance covers three distinct areas that matter most when accidents happen on job sites. First, bodily injury and property damage claims protect you when a client, visitor, or bystander gets hurt or their property gets damaged because of your work. If a worker accidentally injures someone while installing HVAC equipment, or a tool falls through a customer’s roof, this coverage pays for their medical bills and repair costs up to your policy limits. Second, the policy covers your legal defense costs and court judgments, which is where most contractors get blindsided. Legal defense fees can easily exceed $50,000 before a case even reaches trial, and many contractors don’t realize their policy covers these expenses separately from the damage settlement itself. Third, medical payments coverage handles immediate medical expenses for injured parties without requiring them to file a claim or prove fault, which often prevents small incidents from turning into lawsuits.

Understanding Per-Occurrence and Aggregate Limits

Here’s what separates contractors who understand their coverage from those who don’t: the per-occurrence limit applies to both bodily injury and property damage combined, not separately. If your policy has a $300,000 per-occurrence limit, that single number covers everything in one incident-whether it’s a serious injury, property destruction, or both. Your aggregate limit is the total amount your policy will pay across all claims during the policy period, so a $600,000 aggregate means once you hit that number, you’re paying out of pocket for additional claims.

Why Completed Operations Coverage Matters

Completed operations coverage deserves special attention because it protects you against claims that arise after a project finishes-like a roof leak discovered six months post-installation or structural failure discovered later. Most contractors underestimate this risk, but post-project claims are common in construction work and can be expensive to defend. Understanding these three coverage areas helps you assess whether your current limits match your actual exposure. The next section walks you through how to evaluate your specific project size and risk level to determine the right coverage limits for your contracting operation.

Why Your Business Needs This Coverage

The Real Cost of Construction Accidents

One construction accident can bankrupt a contractor who lacks adequate liability protection. OSHA reports that 1 in 10 construction workers suffer injuries each year, and those injuries don’t stay confined to the job site-they often result in third-party claims against your business. A single lawsuit costs $50,000 or more in legal defense fees alone, before any settlement is paid. This isn’t theoretical risk; it’s the reality Dallas-area contractors face every year. Without commercial general liability insurance, you become personally responsible for these expenses, which means your personal assets, savings, and business equipment become targets when someone files a claim.

Client and Lender Requirements

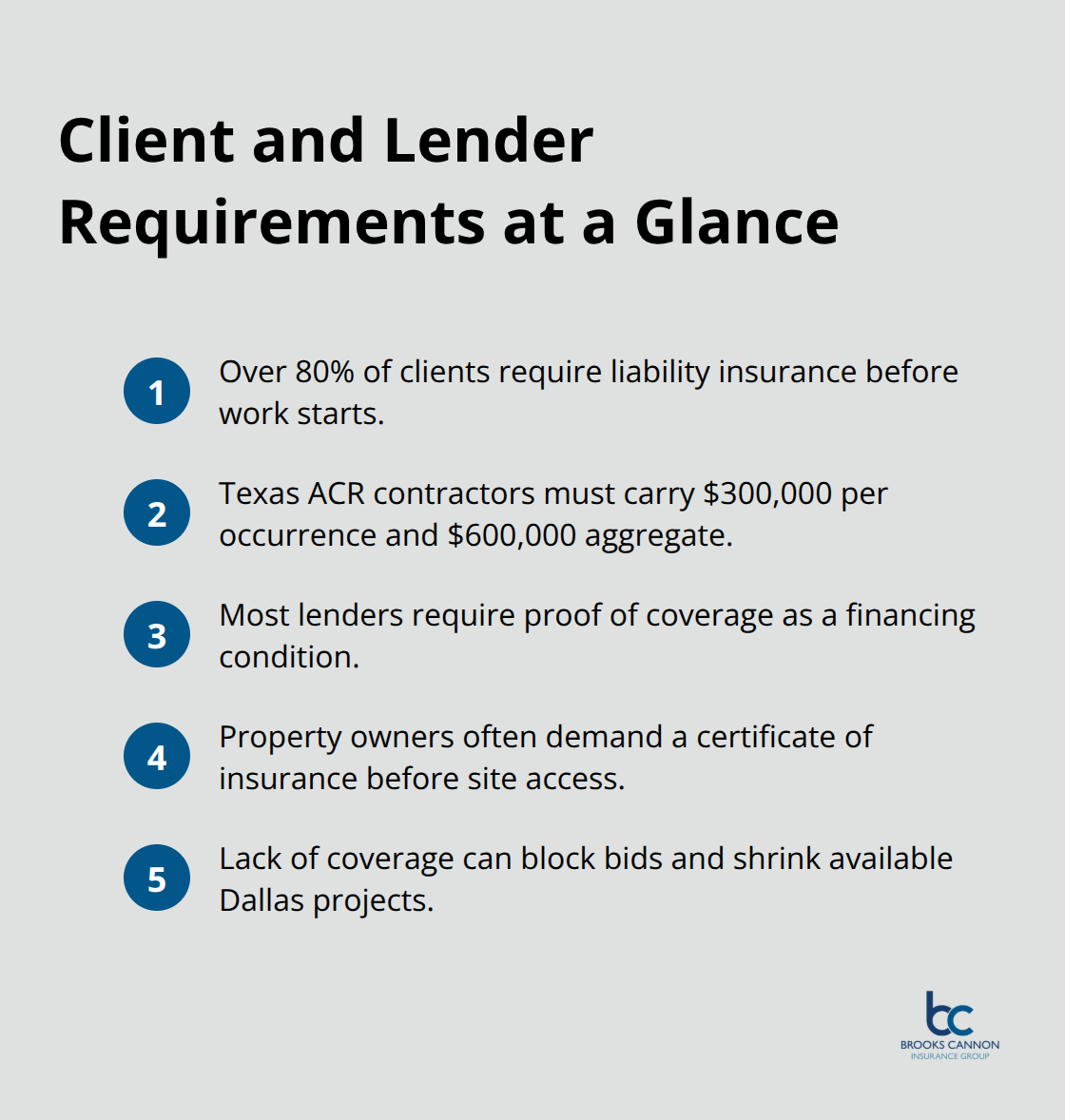

Clients and lenders won’t work with you without proof of coverage. Over 80% of clients require liability insurance before allowing a contractor to start work, and most lending institutions require it as a condition of financing. Texas air conditioning and refrigeration contractors must maintain commercial general liability coverage with minimums of $300,000 per occurrence and $600,000 aggregate to meet state licensing requirements.

If you bid on residential or commercial projects worth more than a few thousand dollars, the property owner’s insurance company will demand to see your certificate of insurance before you set foot on the property. Lenders view contractors without coverage as unacceptable risks and simply won’t fund projects. This means inadequate or missing insurance doesn’t just expose you to lawsuits-it eliminates your access to the majority of available work in the Dallas market.

Protecting Your Business Assets and Reputation

Your business reputation depends on demonstrating that you take risk seriously. Contractors who carry appropriate coverage signal professionalism and financial stability to prospects, which makes them more competitive when bidding against other firms. Insurance also protects your business assets from judgment liens. If someone sues and wins a settlement you can’t pay, the court can place a lien against your equipment, vehicles, and business property. General liability coverage prevents your hard-earned business assets from being seized to satisfy someone else’s claim.

Finding the Right Coverage for Your Operation

The financial protection and market access that liability insurance provides make it essential for any contractor operating in Dallas. Understanding what coverage you actually need requires an honest assessment of your project types, the size of your operations, and the specific risks your work creates. The next section walks you through how to evaluate your project size and risk exposure to determine the right coverage limits for your contracting operation.

Selecting Coverage Limits That Match Your Actual Risk

Assess Your Project History and Exposure

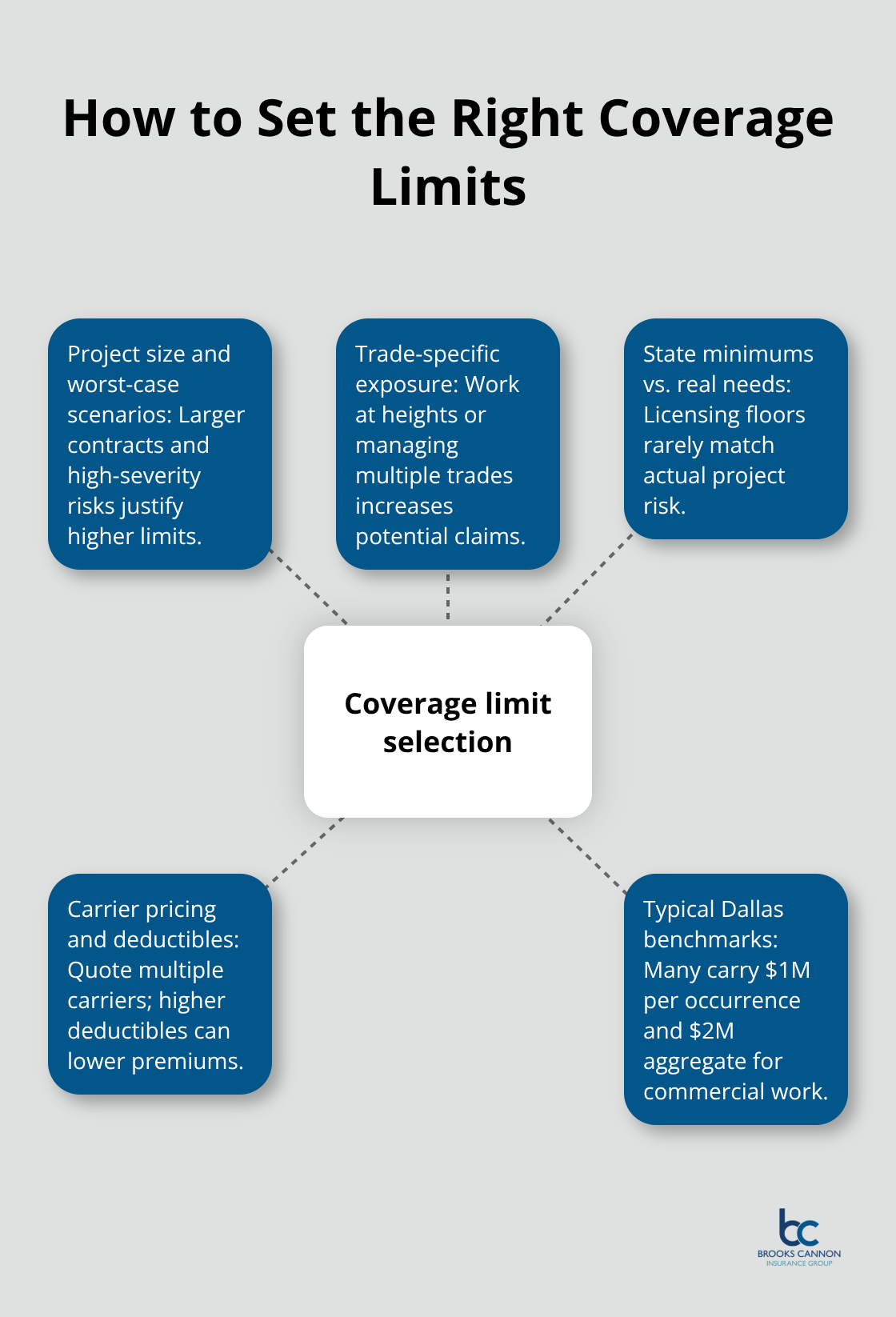

The biggest mistake contractors make is selecting coverage limits based on what sounds reasonable rather than what their actual work demands. A $300,000 per-occurrence limit works fine for small residential jobs, but if you install a commercial HVAC system in a Dallas office tower, one incident could easily exceed that threshold. Start by examining your recent project history: what is the typical contract value, how many workers are on site, and what is the worst-case scenario if something goes wrong? A roofing contractor working at heights faces different exposure than a plumber, and a general contractor managing multiple trades simultaneously carries more risk than a specialized subcontractor.

Understand State Minimums and Industry Standards

Texas air conditioning and refrigeration contractors must maintain at least $300,000 per occurrence and $600,000 aggregate to meet state licensing requirements under 16 Tex. Admin. Code § 75.40, but these minimums are floor requirements, not targets. If your typical project value exceeds $500,000, carrying only $300,000 in coverage leaves you massively underprotected. Many Dallas contractors working commercial projects carry $1 million per occurrence and $2 million aggregate as a baseline, with some moving to $2 million per occurrence for larger operations. The cost difference between a $300,000 and $1 million policy typically runs $40 to $150 per month depending on your trade and claims history, making the upgrade inexpensive relative to the protection it provides.

Compare Quotes from Multiple Carriers

Carrier pricing varies wildly based on how they classify your work and assess your risk. An independent agent can access quotes from 80 or more carriers and typically saves contractors $500 to $1,500 annually compared to online quote tools by finding carriers that specifically want your type of work. When you request quotes, provide consistent information across all carriers: annual revenue, number of employees, specific trades performed, and your complete claims history from the past five years. Deductible selection dramatically affects your premium; choosing a $1,000 deductible instead of $500 can reduce your annual cost by 10 to 15 percent.

Avoid Underpricing and Coverage Gaps

Don’t chase the lowest price at the expense of coverage adequacy. A carrier offering an unusually cheap quote may be pricing based on incomplete information or may have a reputation for denying legitimate claims. Your agent should explain why they recommend specific limits, help you understand what completed operations coverage costs, and clarify whether your coverage actually matches the work you perform in the Dallas market. This conversation prevents costly gaps later and ensures your policy protects your business.

Final Thoughts

Commercial general liability insurance for contractors protects your business from the financial devastation that one accident can cause. Your policy must cover bodily injury, property damage, and completed operations claims, with per-occurrence and aggregate limits that match your actual project exposure rather than just meeting state minimums. Most Dallas contractors working commercial jobs carry $1 million per occurrence and $2 million aggregate as a baseline, and the premium difference between minimal and adequate coverage runs only $40 to $150 monthly.

Selecting the right coverage requires comparing multiple carriers through an independent agent who accesses 80 or more options and typically saves you $500 to $1,500 annually compared to online tools. When you request quotes, provide consistent information about your annual revenue, employee count, specific trades, and claims history, since deductible selection also matters-moving from $500 to $1,000 can reduce your annual premium by 10 to 15 percent. Your legal defense costs must be covered separately from damage settlements, since litigation expenses alone can exceed $50,000 before trial.

We at Brooks Cannon Insurance Group work with top-rated carriers to find commercial general liability insurance for contractors that fits your operation and budget. Our licensed experts understand the Dallas contracting market and explain why specific limits make sense for your business. Contact us today to discuss your coverage needs and receive a quote tailored to your contracting operation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation