Running a lawn care business in Dallas means managing equipment, crews, and client properties every single day. One accident-a damaged fence, an injured customer, or property damage from your equipment-can quickly become a financial disaster.

General liability insurance for lawn care protects you from these costly situations. At Brooks Cannon Insurance Group, we help lawn care operators understand exactly what coverage they need and why it matters for their bottom line.

What Your General Liability Policy Actually Covers

Three Major Categories of Protection

General liability insurance for lawn care businesses protects you against three major categories of claims that occur regularly in Dallas. Property damage claims arise when your equipment or service causes damage to a client’s property-a string trimmer hits a fence, a mower strikes a window, or chemicals damage landscaping. These claims cost thousands to repair, and without coverage, you pay directly from your business account. Bodily injury liability covers medical expenses and lost wages when someone gets hurt on a job site-a customer trips over equipment, a bystander sustains injury from debris, or an employee gets hurt during work. General liability also covers your legal defense costs and court settlements if a claim reaches litigation.

Standard Coverage Limits in Dallas

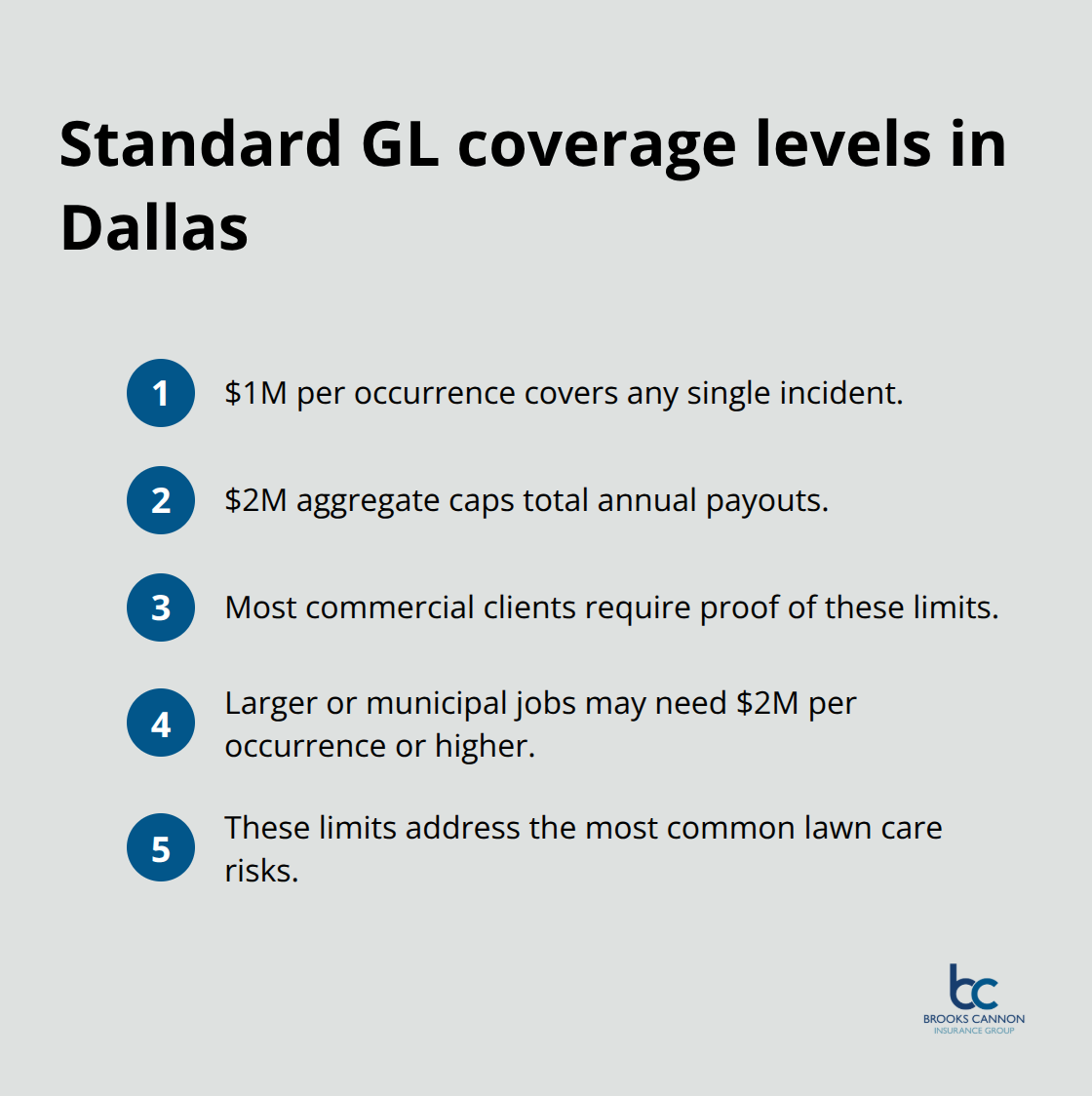

Industry standards call for $1 million per occurrence with a $2 million aggregate, which means you receive protection up to $1 million for any single incident and $2 million total in a policy year. Most commercial clients in Dallas demand this coverage level before signing a contract-larger properties or municipal work sometimes require $2 million per occurrence or higher. This standard protects your business from the most common scenarios you’ll face in lawn care operations.

Real Claims Happen More Often Than You Think

A Dallas landscaper operates a leaf blower near a parked car, equipment vibration damages irrigation lines, or accidental chemical overspray affects a neighbor’s property-these real scenarios trigger claims regularly. Coverage typically runs $100–$290 per month depending on your revenue, number of employees, and risk profile. Skipping coverage exposes your personal assets to lawsuits that could exceed six figures. When you add workers’ compensation, commercial auto, and equipment coverage, annual premiums for a small to mid-sized operation usually run $1,500 to $5,000 (a fraction of what a single uninsured claim could cost).

Why Your Coverage Needs Change as You Grow

Your liability exposure increases as your business expands. Higher earnings and expanded crews mean more accidents and liability risk. You should review your policies annually as revenue and services grow to confirm your coverage keeps pace with your operation. This proactive approach prevents gaps that could leave you vulnerable when you need protection most.

Why You Actually Need This Coverage

The Real Cost of Going Uninsured

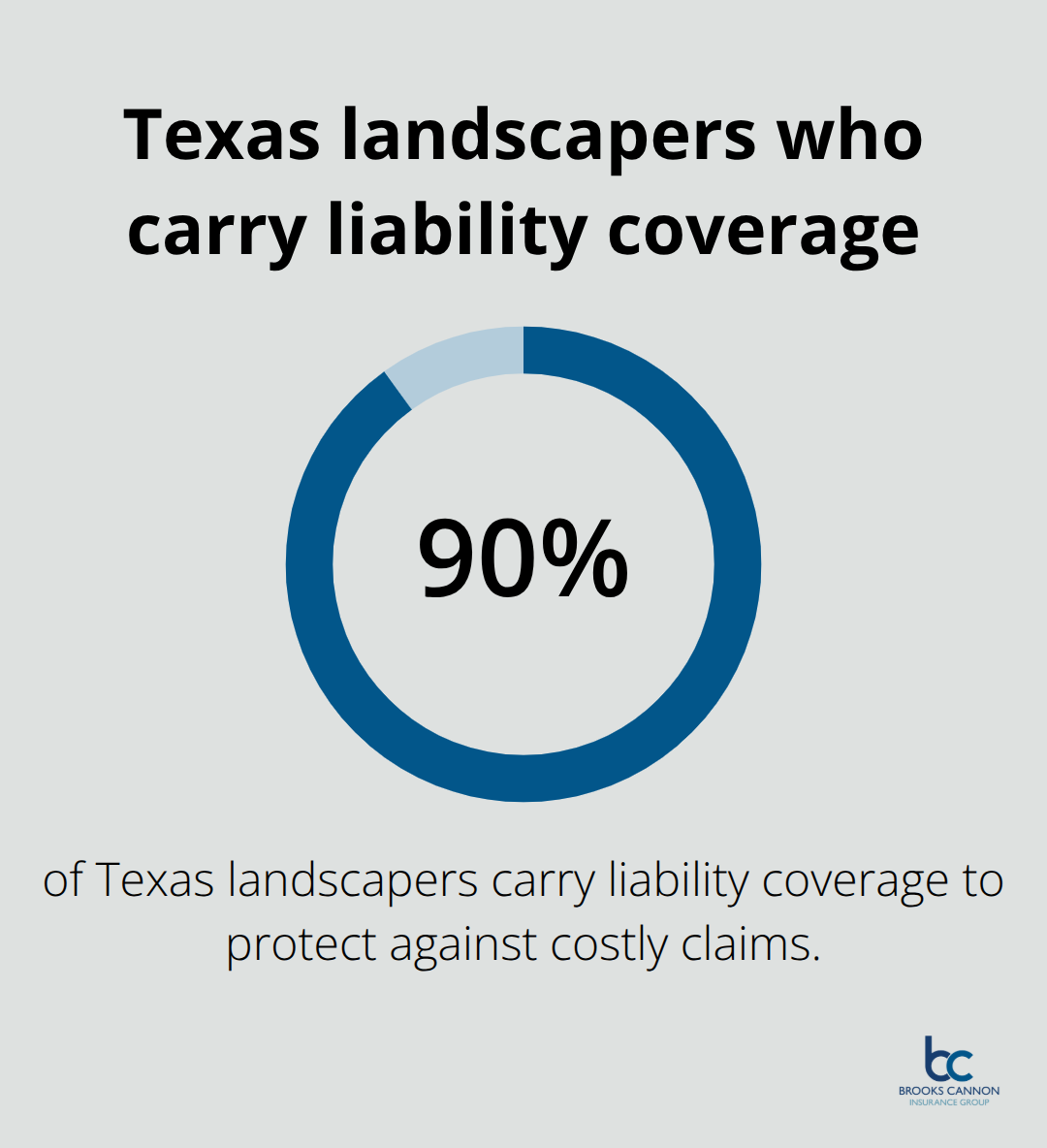

Uninsured liability claims in lawn care aren’t theoretical-they happen constantly in Dallas and the surrounding areas. A single property damage incident costs $5,000 to $15,000 in repairs, and bodily injury claims often exceed $20,000 when medical expenses and legal fees accumulate. Without general liability insurance, you write these checks from your business account or personal savings, which drains cash flow and can force you to shut down operations entirely. Most lawn care operators cannot absorb even one moderate claim without serious damage to their business. About 90 percent of landscapers in Texas carry some form of liability coverage because they understand that one accident destroys years of profit.

Client Requirements That Block Your Revenue

General liability insurance is a hard requirement for winning commercial contracts in the Dallas area. Property managers, HOAs, and commercial clients routinely demand proof of $1 million coverage before they hire you, and many won’t even accept a bid without seeing a certificate of insurance. Municipal contracts and larger residential properties often require higher coverage limits, including $30,000 in bodily injury liability per person and $60,000 in bodily injury liability to more than one person. Without this coverage in place, you lose access to higher-paying work that would actually grow your business. Contractors who skip insurance lose 40 to 60 percent of potential revenue because clients simply won’t work with them.

How Coverage Protects Your Reputation

Your business reputation takes a hit if you cause damage and lack coverage to pay for it; word spreads fast in Dallas neighborhoods and commercial circles. Carrying proper coverage signals to clients that you’re professional, financially stable, and serious about protecting their property. This distinction matters when clients choose between contractors-they trust someone with insurance far more than someone without it. The difference between being a contractor people actively recommend and one they avoid often comes down to whether you carry the right coverage.

Moving Forward With Confidence

Understanding why you need coverage is the first step. The next decision involves selecting the right policy limits and deductibles for your specific operation, which depends on your revenue, crew size, and the types of clients you serve.

How to Choose the Right General Liability Policy for Your Lawn Care Business

Your revenue and crew size determine how much general liability coverage you actually need, and this is where most Dallas lawn care operators make expensive mistakes. A solo operator earning $50,000 annually needs a $1 million per occurrence limit with a $2 million aggregate, which costs roughly $40–$70 monthly. A mid-sized company with five employees and $500,000 in annual revenue should carry that same $1 million per occurrence standard, but your premium climbs to $100–$200 monthly because more staff creates more exposure to accidents. The critical insight is that your coverage limits should match your actual financial risk, not what costs the least. Municipal contracts and larger commercial properties in the Dallas area frequently demand $2 million per occurrence or even $5 million aggregate coverage, which means you cannot bid on that lucrative work without higher limits in place.

When to Add Umbrella Coverage

Adding an umbrella policy on top of your base $1 million coverage is far more cost-effective than raising your primary limits across the board. A $1 million umbrella typically costs $200–$400 annually and protects you against catastrophic claims that exceed your underlying policy. This approach lets you maintain affordable base coverage while still protecting yourself against worst-case scenarios that could destroy your business. Most Dallas contractors overlook umbrella policies because they focus only on their primary limits, but this strategy leaves them vulnerable to claims that exceed their standard protection.

Deductibles and How They Affect Your Real Costs

Raising your deductible from $500 to $2,500 can reduce your annual premium by 10–20 percent, but this only works if you can actually absorb that deductible out of pocket when a claim happens. A Dallas landscaper with steady cash flow can safely take a $1,000 or $2,500 deductible and pocket the premium savings. A newer operator or someone with irregular income should stick with a $500 deductible because paying out-of-pocket for a claim could create cash flow problems. Your claims history matters enormously-a single liability claim increases premiums 25–50 percent and narrows your carrier options, so avoiding claims through solid safety practices and documented procedures protects your rates far better than chasing deductible savings. When you request quotes from independent agents in Dallas, compare the same deductible levels across carriers so you’re actually comparing apples to apples. Some carriers offer preferred pricing for businesses with documented safety training, incident logs, and inspection checklists, which can offset the cost of implementing these practices within months.

Endorsements Your Clients Will Actually Demand

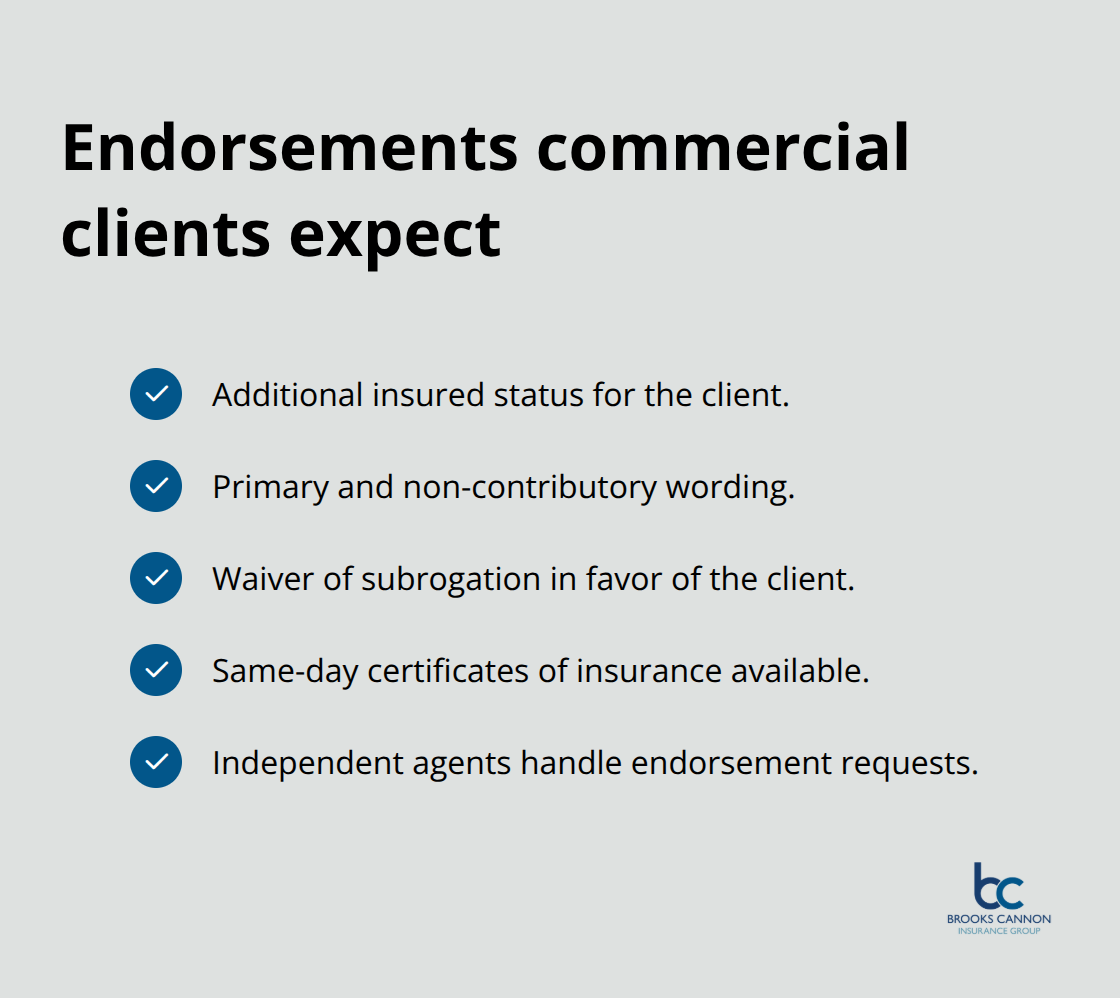

Additional insured status is the endorsement clients request most often, and you should plan on providing it at no extra cost through your policy. This means the client’s name gets added to your certificate of insurance, which signals to them that your coverage protects their interests if something goes wrong on their property. Many commercial clients also require primary and non-contributory language, meaning your insurance pays first if a claim arises, and waiver of subrogation, which prevents your insurer from suing the client to recover claim costs. These endorsements rarely cost anything but they are absolute deal-breakers for commercial contracts-without them, property managers and HOAs simply will not hire you. When you work with an independent agent, they handle these endorsements as part of their quote process so you know exactly what’s included before you bind coverage. Some Dallas contractors miss out on jobs because they don’t understand that certificates of insurance can be issued same-day after your policy is bound, which means you can provide proof of coverage immediately when bidding on work.

How Independent Agents Compare Carriers for You

An independent agent shops multiple carriers and compares coverage options, pricing, and endorsements so you don’t have to contact each insurer individually. This approach saves time and helps you identify the best value rather than settling for the first quote you receive. Independent agents understand local Dallas market conditions and which carriers offer the best rates for lawn care operations in your specific zip code. They also know which carriers are most flexible with endorsements and which ones have the fastest claims processes, information that matters when you need to resolve a problem quickly.

Final Thoughts

General liability insurance for lawn care protects your business from the financial devastation that one accident can cause. Property damage claims, bodily injury lawsuits, and legal defense costs drain cash flow fast, and most Dallas lawn care operators cannot absorb even a moderate claim without serious damage to their operation. About 90 percent of Texas landscapers carry coverage because they understand that skipping it costs far more in lost revenue and personal liability than the monthly premium ever will.

Selecting the right policy requires matching your coverage limits to your actual business size and client base rather than simply choosing the cheapest option available. Your revenue, crew size, and contract types determine whether a $1 million per occurrence limit suffices or whether you need umbrella protection for larger municipal and commercial work. Deductible selection, endorsement requirements, and carrier flexibility all affect both your costs and your ability to win contracts that demand proof of general liability insurance for lawn care.

We at Brooks Cannon Insurance Group work with multiple top-rated carriers to find the best coverage and pricing for your specific situation. Our licensed experts understand the risks lawn care operators face in Dallas and help you build a policy that protects your business without overpaying. Contact us today to get a quote and protect what you have built.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation