Construction projects in the Dallas area face real risks-weather damage, theft, and accidents can halt work and drain budgets fast. Builder’s risk insurance protects your investment during construction, but finding the right policy from top builders risk insurance companies requires knowing what you actually need.

At Brooks Cannon Insurance Group, we help contractors and project owners cut through the confusion and find coverage that fits their specific situation.

What Builder’s Risk Actually Covers

Builder’s Risk vs. General Liability Insurance

Builder’s risk insurance and general liability insurance serve completely different purposes, and mixing them up costs contractors and project owners real money. General liability covers injuries to third parties or property damage you cause to someone else’s property. Builder’s risk covers physical damage to the structure you’re building, plus materials and equipment on the job site. If a worker gets hurt, that’s workers’ compensation. If your crane damages a neighbor’s fence, that’s general liability. If a storm destroys the framing you just installed, that’s builder’s risk. You need all three.

Understanding Your Premium Costs

In Texas, builder’s risk premiums typically run 1% to 5% of your total construction cost, which means a $500,000 project might cost $5,000 to $25,000 annually in coverage. That’s not optional insurance-it’s the cost of protecting your actual investment. Your lender almost certainly requires it before releasing construction funds.

What Standard Policies Cover

Standard policies cover fire, lightning, explosion, wind, hail, theft, vandalism, faulty design, flawed materials, negligent workmanship, and labor costs. This matters because these perils account for most construction site losses in the Dallas area. However, standard coverage alone leaves gaps that expose you to significant financial risk.

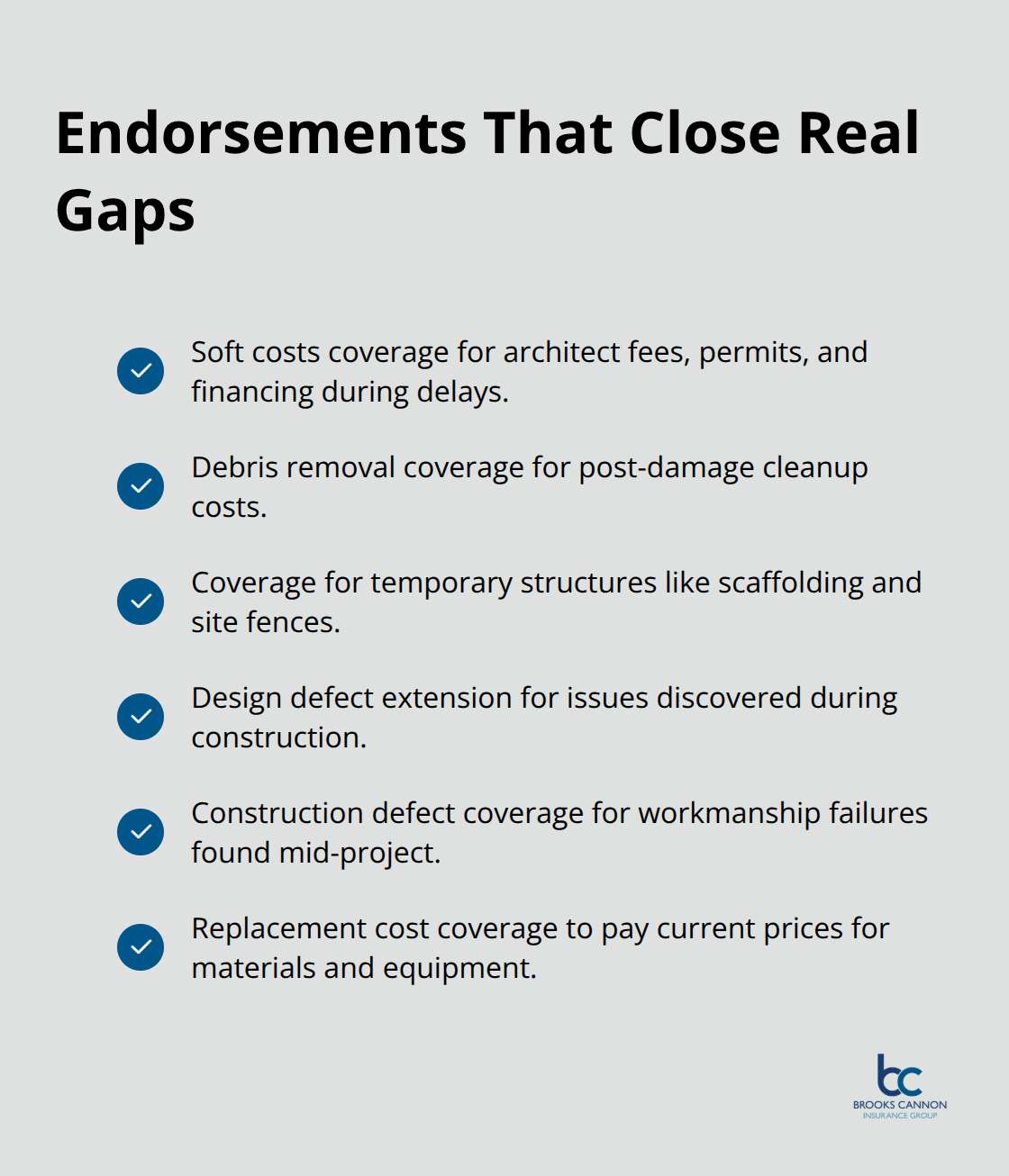

Adding Endorsements That Close Real Gaps

The smart move is adding endorsements that close real gaps. Soft costs coverage reimburses you for architect fees, permit costs, and financing charges if a covered event delays your project-this protects your profit margin when weather or theft pushes your timeline back. Debris removal coverage handles cleanup costs after damage, which can run thousands of dollars and delay your next phase of work. Coverage for temporary structures like scaffolding and site fences prevents gaps when theft or weather hits your setup. Extensions for design defects and construction defects matter more than standard perils because they protect against issues discovered during construction, not just external events. Replacement cost coverage pays actual replacement prices for damaged materials instead of depreciated value, which makes a real difference with lumber and equipment prices.

Skipping these extensions because they cost an extra 0.5% to 1% of premium creates exposure that costs 10 times more when damage happens. Your contract likely specifies who buys builder’s risk, but the owner ultimately pays through the project budget, so choosing the right coverage from the start protects your bottom line. The next step involves evaluating which carriers offer the endorsements and pricing that match your specific project profile-and that’s where comparing top-rated providers becomes essential.

Which Carriers Actually Deliver for Texas Construction Projects

Top Carriers for Dallas-Area Projects

Chubb stands out as the strongest overall choice for builders risk coverage, offering the widest range of tailored policies and the financial muscle to back every claim. AM Best, Moody’s, and S&P rate Chubb at A++, Aa3+, and AA respectively, meaning they maintain capital reserves to pay large claims without delay. Their policies include soft costs coverage, debris removal, and design defect protection as standard endorsements rather than expensive add-ons, which saves money on mid-sized projects. The trade-off is pricing-Chubb typically costs 15% to 25% more than competitors, but their claims team settles disputes faster and pays replacement cost instead of depreciated value, which matters when lumber prices spike mid-project. For Dallas contractors managing projects over $2 million, Chubb’s expertise in complex coverage gaps and their willingness to extend policies beyond standard timelines makes the premium worthwhile.

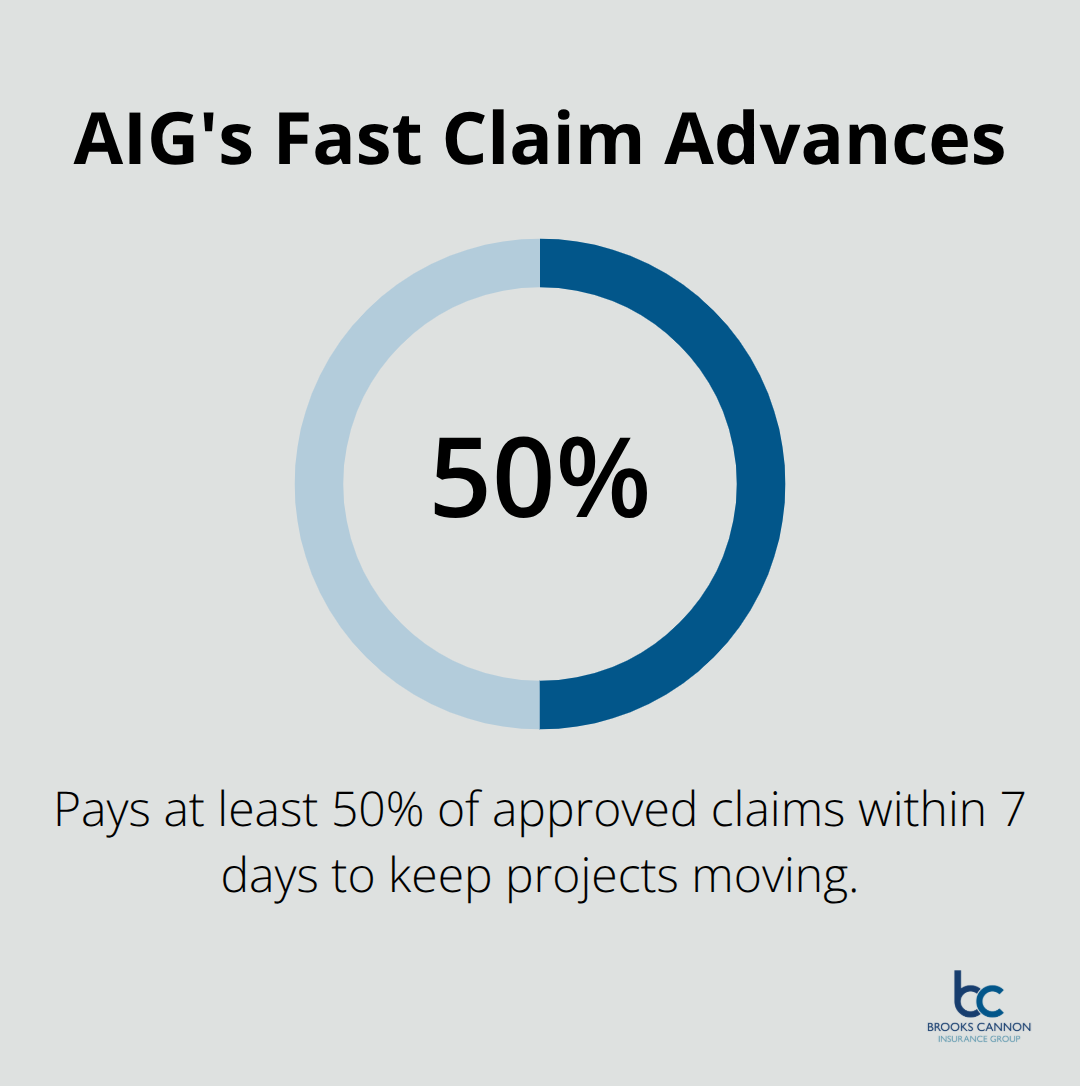

AIG ranks second for commercial developers and large general contractors because they staff an in-house builders risk claims team that understands construction timelines and doesn’t nickel-and-dime on small damage claims. AIG promises to pay at least 50% of approved claims within 7 days, which keeps your project moving when weather or theft hits. Their AM Best rating of A+ and S&P rating of A+ confirm they won’t disappear when you file a major claim.

Complete Coverage Bundles and Specialized Options

Nationwide works best for general contractors who need a complete insurance suite-they bundle builders risk with general liability, inland marine for tools and equipment, business auto, and workers comp into one policy, which simplifies administration and often yields 10% to 15% discounts compared to buying separately. Nationwide’s BBB accreditation and favorable complaint data from the National Association of Insurance Commissioners show they handle disputes fairly without the delays that plague smaller carriers.

State Farm appeals to homeowners and owner-builders because their local agents understand Dallas-area construction and can explain what’s actually covered in plain language, though their pricing transparency varies by agent location. Zurich, available through US Assure, specializes in new home construction and renovations with extensions available up to $75 million in coverage, making them ideal for large residential developments. Their AM Best rating of A+ and Moody’s rating of Aa2 indicate strong financial stability.

Deductibles and Premium Strategy

Deductibles range from $500 to $10,000 on most policies, and here’s where most contractors leave money on the table-they choose the lowest deductible without calculating actual risk. On a $500,000 project, increasing your deductible from $1,000 to $5,000 typically reduces your annual premium by $800 to $1,200, which covers the extra out-of-pocket risk within two years. Try a $2,500 deductible on most Dallas-area projects, as it balances premium savings against realistic loss frequency. Choose the lower deductible only if your project sits in a high-theft area or coastal zone prone to wind damage.

Getting Accurate Quotes and Comparing Carriers

When calling for quotes, specify your exact project timeline, construction cost, location zip code, and whether you need extensions for soft costs or design defects-vague requests generate inflated quotes that don’t reflect real pricing. Direct quotes from underwriters typically run 10% to 15% lower than quotes through brokers because you eliminate the middleman commission, though many carriers require an agent or broker to handle policy administration and claims.

Claims Support That Matters

Claims support matters more than you’d think-call the carrier’s claims hotline before buying and ask how long they typically take to pay debris removal claims, which are the most common claim type on Dallas projects. Carriers that answer within 2 hours and process debris claims in under 10 days deserve serious consideration. Carriers with recorded messages or claims departments that require 24-hour callbacks will cost you time and money when damage happens mid-project. Once you’ve narrowed down carriers based on financial strength, coverage options, and claims responsiveness, the next step involves assessing your specific project needs and determining which policy limits and exclusions actually protect your bottom line.

Matching Coverage to Your Actual Project Risk

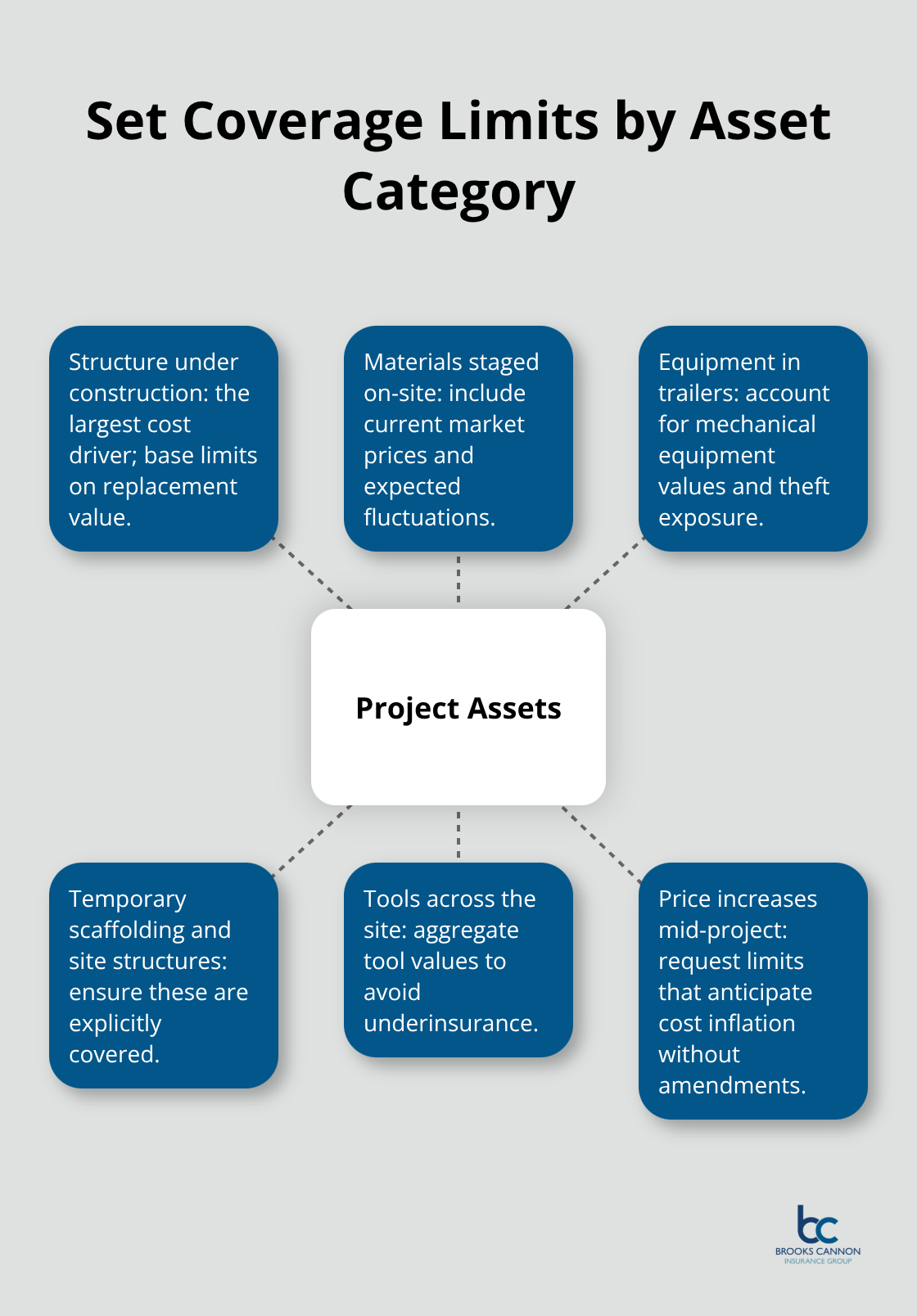

List Every Asset and Set Coverage Limits Correctly

Start with a complete inventory of every asset on your Dallas project and assign a replacement cost to each category. The structure under construction costs the most, but materials staged on-site, equipment in trailers, temporary scaffolding, and tools scattered across the site all need coverage amounts that reflect current market prices. A $1.2 million residential project in Plano might have $800,000 in framing materials, $150,000 in mechanical equipment, $100,000 in temporary structures, and $50,000 in tools. Standard policies cover all of these categories, but your coverage limit must match the total sum, not just the structure cost. Many contractors underbuy coverage by 20% to 30% because they base limits on the building contract price alone, then face partial claim denials when materials cost more than expected.

Request quotes with coverage limits that account for price increases mid-project without forcing you to amend the policy. Your lender requires this anyway, so don’t negotiate down on limits to save premium dollars.

Account for Dallas Weather and Theft Patterns

Dallas contractors face distinct risks that standard coverage alone won’t handle. Wind and hail cause significant damage during spring and early summer, so if your project timeline overlaps April through June, confirm the policy includes hail and windstorm coverage without additional premiums. Theft and vandalism spike on projects in urban Dallas proper, especially around downtown and Uptown, so request quotes that include coverage for theft of materials in transit and off-site storage. Coastal projects within 50 miles of the Gulf face hurricane risk that requires separate windstorm or flood coverage as an endorsement, not standard inclusion. A contractor building near Lake Lewisville should add water damage coverage because standard policies exclude flooding, yet construction site runoff and drainage failures happen regularly. The zip code you provide in your quote request directly affects pricing-a project in Richardson costs less to insure than an identical project in downtown Dallas because theft loss frequency differs by location. State your project location accurately when requesting quotes, as understating risk leads to claim denials later.

Understand What Exclusions Actually Cost You

Read the exclusions section before comparing prices, because two policies at different premiums might cover completely different risks. Standard exclusions include employee theft, earthquakes, war, and pre-construction damage, which don’t matter for most Dallas projects. What does matter is whether the policy covers design defects discovered during construction, which happens when an architect’s plans conflict with actual site conditions. A standard policy denies this claim, but adding design defect coverage costs only 0.3% to 0.5% of annual premium and protects you from $50,000+ in unexpected rework costs. Similarly, construction defect coverage protects against workmanship failures discovered during the project, which your general contractor’s insurance won’t cover. Soft costs coverage reimburses architect fees and financing charges if a covered loss delays your project-this endorsement costs 0.4% to 0.8% of premium but prevents you from absorbing thousands in loan interest if weather stops work for two weeks. Compare three carriers using identical coverage specifications, not just base premium, because a $3,000 annual policy without soft costs and design defect coverage costs far more than a $3,600 policy that includes both. Contact each carrier’s underwriting department and ask which endorsements come standard versus cost extra, then calculate total annual cost for the complete coverage you actually need.

Final Thoughts

Selecting builder’s risk insurance requires three concrete decisions: matching coverage limits to your actual project assets, choosing a carrier with strong financial ratings and fast claims handling, and adding endorsements that close real gaps in standard policies. Financial strength matters because AM Best, Moody’s, and S&P ratings tell you whether a carrier can actually pay large claims without delay. Claims speed matters because debris removal and weather damage claims need processing within days, not weeks, to keep your Dallas project moving.

The top builders risk insurance companies we’ve covered-Chubb, AIG, Nationwide, State Farm, and Zurich-each excel in different situations. Chubb handles complex projects over $2 million, AIG moves claims fast for large contractors, Nationwide bundles coverage efficiently, State Farm works for owner-builders, and Zurich specializes in residential development. Your project profile determines which carrier actually delivers the best value, not marketing claims or brand recognition.

Start by requesting quotes from at least three carriers using identical project specifications: exact timeline, construction cost, location zip code, and required endorsements. Call each carrier’s claims department before buying and ask about debris removal claim processing times. Contact us at https://brookscannon.com to discuss your project timeline and get accurate quotes that protect your investment without overpaying for coverage you don’t need.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation