Construction projects in the Dallas area face real financial risks when soft costs aren’t properly covered. Soft costs-like permits, architect fees, and project delays-can quickly drain your budget if something goes wrong on site.

We at Brooks Cannon Insurance Group see builders overlook these expenses all the time, only to face major losses when they’re not protected. This guide walks you through what soft costs are, why they matter, and how builders risk insurance shields your project from unexpected expenses.

Understanding Soft Costs vs. Hard Costs

What Separates Soft Costs from Hard Costs

Soft costs are the indirect expenses tied to your construction project that don’t involve materials or labor. Hard costs cover the physical building-materials, labor, equipment, and site work-while soft costs cover everything else needed to complete the project on time and on budget. In Dallas construction, soft costs typically represent 10 to 25 percent of your total project budget, yet most builders underestimate them or skip coverage entirely. This mistake costs money when delays happen.

Common Soft Cost Categories You’ll Face

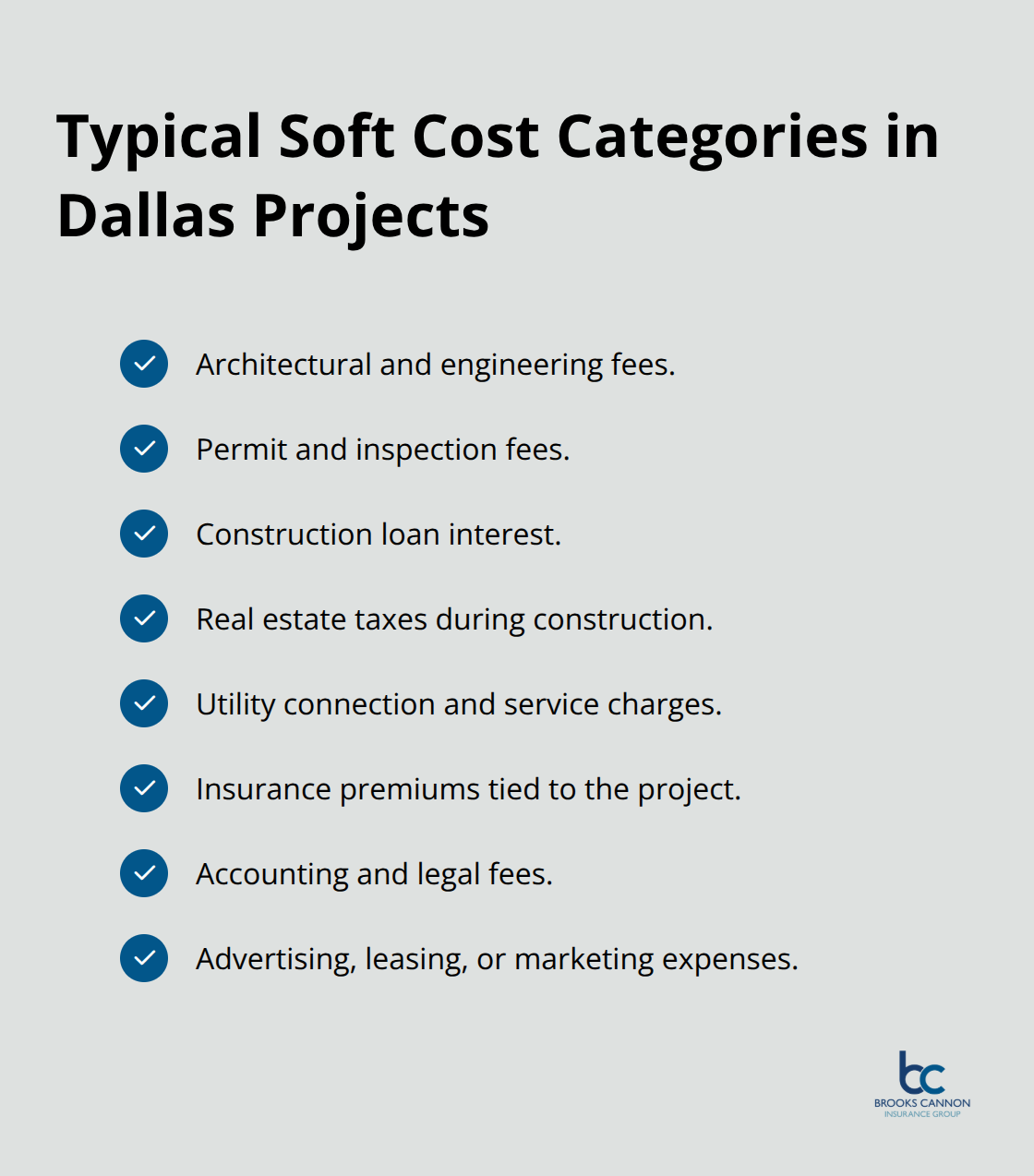

Soft costs include architectural and engineering fees, permit and inspection fees, construction loan interest, real estate taxes, utility connection charges, insurance premiums, accounting and legal fees, and advertising for your project opening. If your project gets delayed due to a covered event like severe weather or fire, these costs keep accruing from your original completion date until work finishes.

A 2,500 square foot residential project with hard costs around $550,000 could easily have soft costs of $82,500 or more. A 5,000 square foot commercial build with hard costs near $1,250,000 might carry soft costs exceeding $187,500. These numbers aren’t theoretical-they’re real expenses that come out of your pocket if your builder’s risk policy doesn’t cover them.

Why Standard Policies Leave You Exposed

Standard builder’s risk policies focus on protecting hard costs and typically exclude soft costs unless you add a specific endorsement. This gap leaves you exposed to significant financial losses during construction delays. The ruling emphasized that soft costs require explicit policy language to be covered.

How Costs Accumulate During Delays

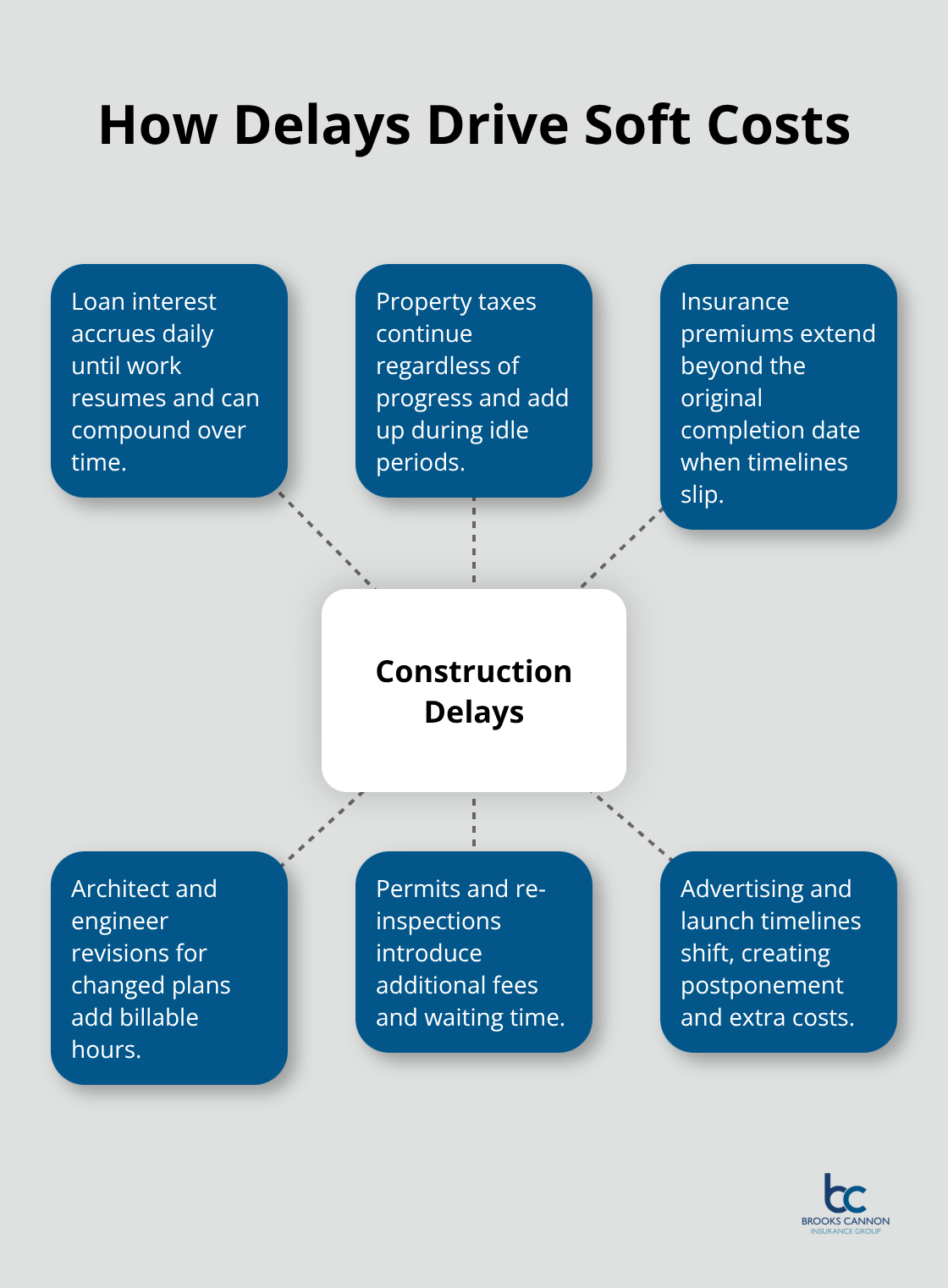

When delays occur, soft costs don’t pause-your architect still bills for revised plans, your lender still charges interest, property taxes still accumulate, and insurance premiums keep coming due. Without soft cost coverage, you absorb these expenses out-of-pocket. A retail expansion delayed by weather triggers costs for extended permits, re-inspection fees, additional architect time, ongoing loan interest, and advertising postponement. A housing development delayed by permit issues faces mounting real estate taxes, utility charges, and construction loan interest that can total thousands of dollars per week. The longer the delay, the worse the financial damage.

Protecting Yourself with Proper Endorsements

Soft cost endorsements typically cover construction overhead expenses and require careful documentation to prove the costs resulted directly from a covered loss. Most policies include a waiting period of around 30 days before soft cost coverage activates, meaning short delays won’t trigger claims but extended delays will hit hard. Your actual project budget determines the soft cost limits you need-inadequate limits create coverage gaps that could undermine your entire financial plan. The next section shows you exactly how to calculate these limits and work with an insurance agent to lock in the right protection.

Why Soft Costs Drain Your Project Budget

The Real Cost of Construction Delays

Soft costs drain your project budget faster than most builders expect, and the damage multiplies when delays occur. In Dallas construction, a 30-day delay on a $1.25 million commercial project costs roughly $15,000 to $25,000 in soft costs alone-loan interest, real estate taxes, insurance premiums, and extended architect fees accumulate while you wait for permits or weather to clear.

A residential project delayed by weather or inspection failures faces similar pressure: your construction lender charges interest daily, property taxes accumulate regardless of progress, utility connections get postponed, and advertising for your opening gets pushed back. Without soft cost coverage, these expenses come directly from your profit margin or your personal savings.

How the Numbers Add Up

The math is brutal. If soft costs represent 15 percent of your total project budget and a delay extends your timeline by eight weeks, you lose roughly 3 percent of your entire project cost to delay-related overhead. For a $750,000 residential build, that equals $22,500 gone. For a $2 million commercial project, you face $60,000 in uncovered soft costs. Most builders risk policies do not automatically include soft cost protection, which means you absorb this hit unless you specifically added an endorsement beforehand.

Real Dallas Construction Delays Show the Danger

Real construction delays in the Dallas area reveal exactly how dangerous this gap becomes. A retail center expansion delayed by permit processing accumulated $8,000 monthly in real estate taxes, $6,000 in extended loan interest, and $3,500 in re-inspection fees before construction resumed-totaling $34,000 over a four-month delay. A residential development facing unexpected utility connection issues ran up $12,000 in additional architect fees for revised site plans, $9,500 in property taxes during the delay, and $7,200 in extended insurance premiums. Without soft cost endorsements, the developer paid every penny out-of-pocket.

Why Waiting Periods and Coverage Limits Matter

The waiting period on most soft cost endorsements-typically 30 days-means short delays will not trigger coverage, but extended delays create serious financial exposure. Your actual soft cost limits matter tremendously because inadequate limits create coverage gaps that leave you partially exposed. If you budgeted $85,000 in soft costs but your policy only covers $40,000, you remain personally liable for the remaining $45,000 when delays occur. This is why calculating soft costs accurately during project planning and securing appropriate endorsement limits before construction starts separates builders who survive unexpected delays from those who face financial crisis. The next section walks you through the exact steps to calculate your soft cost exposure and work with an insurance agent to lock in the right protection for your specific project.

Securing Soft Cost Coverage Before Construction Starts

Request Detailed Quotes with Clear Endorsement Language

Soft cost protection requires moving beyond standard builder’s risk policies and adding specific endorsements that match your project’s actual expenses. Most insurance carriers offer soft cost endorsements as add-ons to basic coverage, but the specifics vary significantly between policies. Request a detailed builders risk quote that explicitly lists what soft costs are covered, what waiting periods apply, and what documentation you’ll need to file a claim. Many policies include a 30-day waiting period, meaning delays under one month won’t trigger coverage, but this threshold makes endorsements critical for projects with tight timelines or seasonal pressures. The endorsement should specify covered items like architectural and engineering fees for revised plans, extended loan interest, real estate taxes during delays, permit and re-inspection fees, insurance premiums, and accounting or legal costs tied directly to the delay.

Some carriers exclude certain soft costs or cap coverage at specific amounts, so comparing endorsement language across multiple quotes prevents expensive gaps. A retail expansion project in Dallas discovered mid-construction that their policy capped soft cost coverage at $25,000 when actual delay expenses totaled $47,000, leaving them personally liable for the difference. This happens because builders often accept the first quote without reviewing the fine print. Demand clarity on sub-limits for individual cost categories, waiting periods, and the exact documentation required to prove causation between the covered loss and your soft cost expenses. Your insurance agent should walk you through every line item and explain how each endorsement provision protects your specific project.

Calculate Soft Costs with Detailed Line-Item Documentation

Soft cost calculation requires itemizing every indirect expense from project start through expected completion, then updating those numbers as your project evolves. Start with architectural and engineering fees, which in Dallas typically range from 5 to 10 percent of hard costs for residential projects and 8 to 12 percent for commercial work. Add permit and inspection fees, which Dallas charges based on project valuation and complexity, plus contingency for expedited processing or re-inspection costs if delays occur. Construction loan interest deserves careful attention because it accrues daily and compounds quickly; if your lender charges 8 percent annually on a $600,000 construction loan, each month of delay costs roughly $4,000 in interest alone. Include real estate taxes on your property during construction, utility connection charges, extended insurance premiums beyond your original completion date, accounting and legal fees for project management, and advertising or leasing costs if you build for rent or resale. A 2,500 square foot residential project with $550,000 in hard costs might carry $8,000 in permits, $27,500 in architect fees, $4,000 monthly in loan interest, $2,100 in quarterly property taxes, $1,800 in extended insurance, and $3,600 in accounting fees, totaling roughly $82,500 across the typical nine-month construction timeline. Document these costs in a spreadsheet that separates hard costs from soft costs and shows your calculations clearly, because insurers will request this documentation when you file a claim. Update your soft cost worksheet quarterly as projects progress, because scope changes, permit delays, or market conditions often increase your exposure beyond initial estimates.

Match Endorsement Limits to Your Actual Project Exposure

Your insurance agent should review your soft costs coverage documentation together with you before you sign the policy so your endorsement limits match your actual project exposure. This step prevents the coverage shortfalls that force builders to absorb thousands in unexpected costs. Inadequate limits create gaps that leave you partially exposed when delays occur, and the financial consequences mount quickly on larger projects.

Final Thoughts

Soft costs in builders risk insurance represent the financial difference between a protected project and one that drains your savings when delays occur. Standard builder’s risk policies exclude these indirect expenses unless you add specific endorsements, leaving most Dallas builders exposed to thousands in uncovered costs. A 30-day delay on a commercial project costs $15,000 to $25,000 in soft costs alone, while longer delays can exceed $60,000 on larger builds.

Protecting your project requires three concrete actions before construction starts. Request detailed builders risk quotes that explicitly define soft cost endorsements, waiting periods, and covered items specific to your build, then calculate your actual soft cost exposure by itemizing architectural fees, loan interest, property taxes, permits, and insurance premiums across your entire timeline. Match your endorsement limits to those calculations so coverage gaps don’t leave you partially exposed when delays happen.

We at Brooks Cannon Insurance Group work with Dallas builders and developers to identify these gaps and secure the right coverage before construction starts. Our licensed experts understand Dallas construction risks and the specific endorsements that prevent financial disasters when unexpected delays occur, and we partner with multiple top-rated insurance carriers to find builders risk solutions that protect your project. Contact us today to discuss your soft cost exposure and lock in the protection your build deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation