Construction projects face real financial risks from weather, theft, and equipment damage. Commercial builders risk coverage protects your investment when these events happen.

At Brooks Cannon Insurance Group, we help Dallas-area contractors understand why this protection matters and how to get the right policy for your specific project.

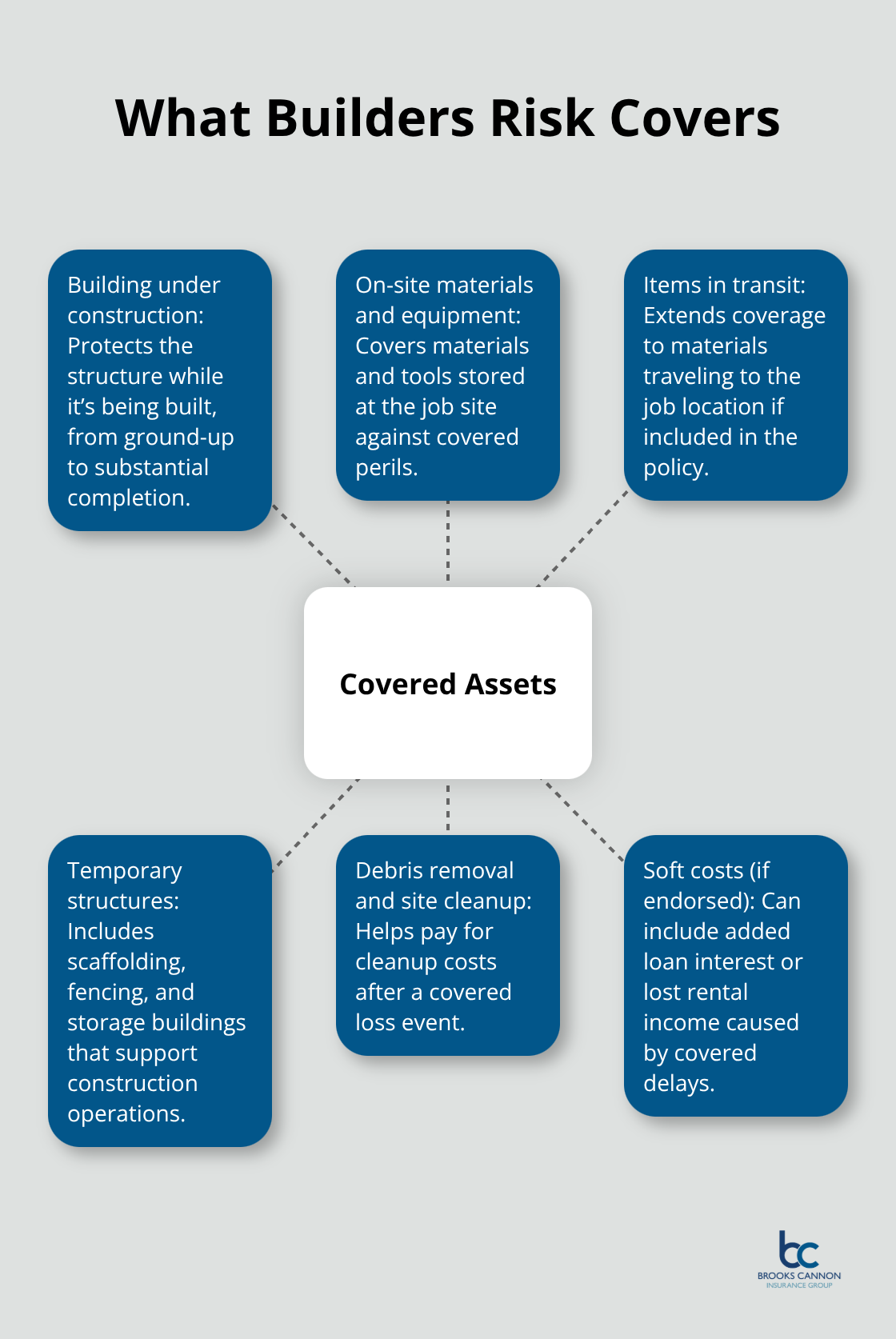

What Builders Risk Actually Covers

Commercial builders risk insurance protects the physical assets on your construction project from specific perils that occur during the building phase. The policy covers the building structure while it’s under construction, materials and equipment stored on-site, and items in transit to your job location. It also covers temporary structures like scaffolding, fencing, and storage buildings that support your operations. Zurich, a major carrier in this space, reports that builders risk policies typically start at around $375 in most states, though costs vary significantly based on project value, location, and construction type.

Coverage activates when you take possession of materials or sign your construction contract, whichever comes first, and continues until the project reaches completion or occupancy. This timing matters because gaps between contract signing and material delivery can leave your project exposed. Fire, lightning, hail, windstorm, theft, and vandalism are standard covered perils under most policies. Debris removal and site cleanup costs are included, which can be substantial after a loss event.

Some policies also cover soft costs like additional loan interest or lost rental income if a covered peril delays your project completion.

Materials in Transit Need Explicit Coverage

Materials traveling to your job site face real risk during transport. Standard builders risk policies cover materials in transit, but you should verify this applies to your specific shipments and routes. If you store materials off-site before bringing them to the job, confirm your policy extends to those locations as well. Installation floater endorsements protect the value of materials that will become permanent parts of the structure, which is essential for high-value fixtures and equipment. Your policy should clearly define what’s covered during each phase of the construction timeline.

Location Determines Your Premium More Than Anything Else

Proximity to fire protection services, flood zones, and coastal wind exposure directly influences what you’ll pay. According to Zurich’s underwriting guidelines, location is the single biggest cost factor for builders risk premiums. A $500,000 residential project in Dallas costs far less to insure than the same project in a high-risk coastal area. Construction type also matters significantly-fire-resistive building materials lower your premium compared to wood frame construction.

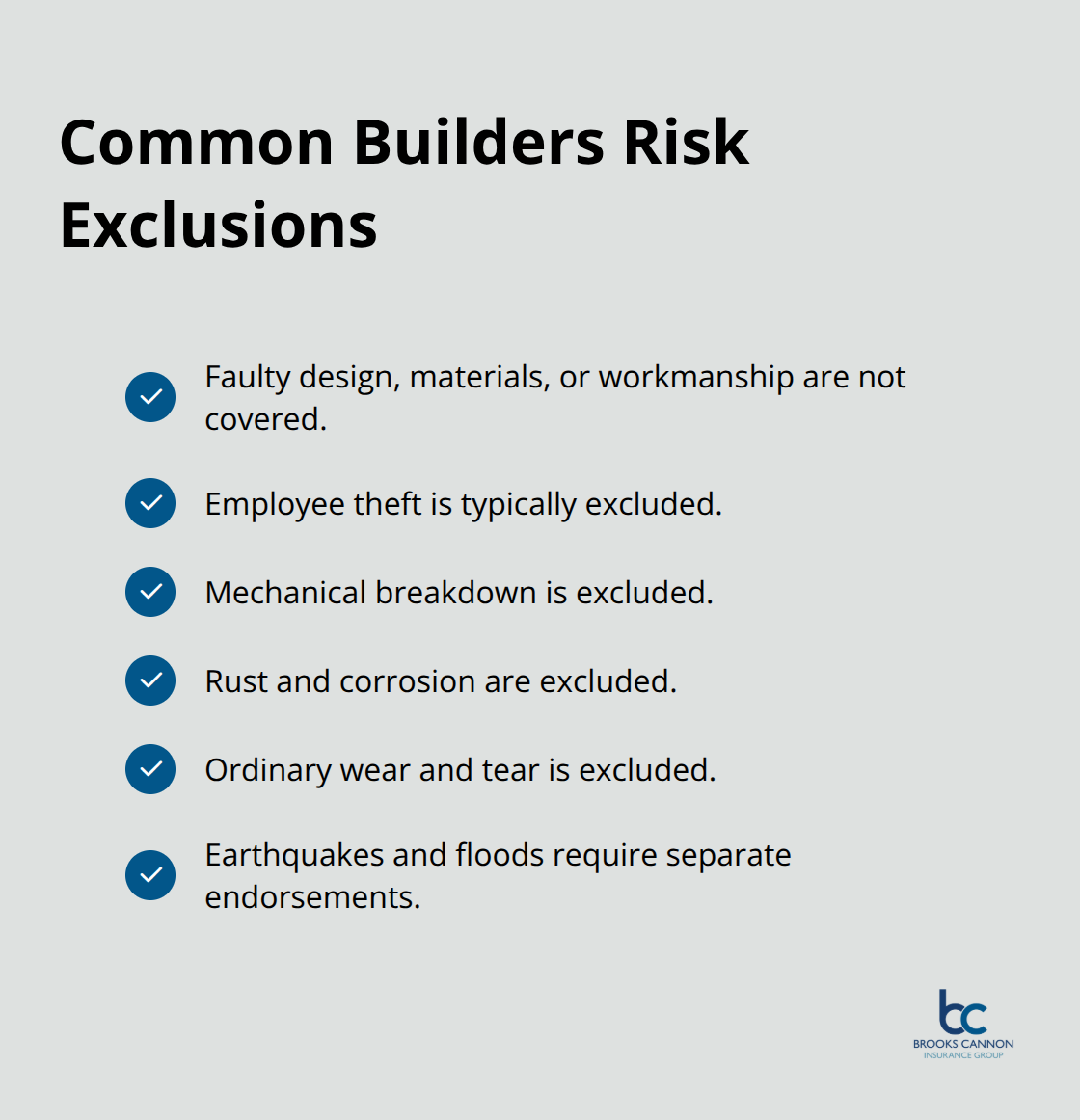

What Builders Risk Explicitly Excludes

Your policy won’t cover faulty design, faulty materials, or faulty workmanship, according to construction insurance guidance from NFP. This gap affects many contractors who overlook it. If a structural defect causes damage, that’s on you, not your insurance. Employee theft by your own staff typically isn’t covered either. Mechanical breakdown, rust, and ordinary wear and tear fall outside coverage.

Earthquakes and floods require separate endorsements and aren’t included in standard policies.

These exclusions mean builders risk is just one piece of your overall construction risk management strategy. Understanding what your policy excludes helps you identify which additional coverages you need to protect your project fully. The next step involves assessing your specific project to determine the right coverage limits and deductibles for your situation.

Why Builders Risk Insurance Matters for Your Bottom Line

Construction projects in the Dallas area operate with razor-thin margins, and a single loss event can erase months of profit. General liability insurance protects you against third-party injuries and damage claims, but it explicitly excludes damage to the building materials and structures you actively construct. This is the protection gap that builders risk insurance fills. Builders risk insurance protects the owner of a construction project for losses caused by many reasons, including fire, explosion, and hurricane. Your general liability policy won’t pay if fire destroys materials on-site, if a thunderstorm damages newly installed HVAC equipment, or if theft removes copper wiring from a partially completed commercial building. According to NFP’s analysis of the construction insurance market, faulty workmanship exclusions in general liability policies create additional gaps that many contractors overlook until a claim denial arrives. Builders risk coverage steps in where general liability stops, protecting the physical assets that represent your actual construction investment.

Lenders and Contract Language Demand This Coverage

Your construction loan won’t close without proof of builders risk insurance. Lenders require this coverage because they have a financial interest in protecting the collateral-your construction project. Most commercial construction contracts in Texas explicitly require the general contractor to maintain builders risk coverage throughout the project timeline, with the lender and project owner named as additional insureds on the policy. This isn’t negotiable language; it’s standard practice. When you bid on projects with developer clients or secure financing, you’ll encounter contractual requirements that mandate specific coverage limits and endorsements. Failing to maintain the required coverage can trigger loan defaults or contract breaches, costing far more than the insurance premium itself. The Texas construction market has become increasingly sophisticated about these requirements, and contractors who understand the insurance demands upfront avoid costly delays and disputes during construction.

Market Conditions Are Pushing Premiums Higher

The construction insurance market tightened significantly in 2025 according to NFP’s analysis of market trends. Carriers are demanding higher retentions, implementing stricter underwriting standards, and charging higher premiums due to inflation, increased litigation, and severe weather events. This means the cost of builders risk insurance has risen across the board, but well-managed construction projects with strong safety records and reasonable risk profiles still qualify for competitive pricing. The cost of not having coverage-or having insufficient limits-far exceeds the premium you’ll pay. A single major loss without adequate builders risk protection can force a contractor out of business.

Finding Competitive Pricing in a Tight Market

Multiple carriers compete for construction business in the Dallas area, and shopping your coverage across several insurers can yield significant savings. Each carrier weighs project risk differently, so a project that one insurer declines may qualify for standard rates with another. Securing quotes before your materials arrive protects both your financial position and your ability to meet contract obligations with lenders and project owners. The timing of your insurance application matters-carriers assess risk based on your project timeline, so early engagement with insurers helps you lock in capacity and favorable terms before the market tightens further on your specific project type.

How to Choose the Right Builders Risk Policy for Your Project

Start with Your Actual Project Costs

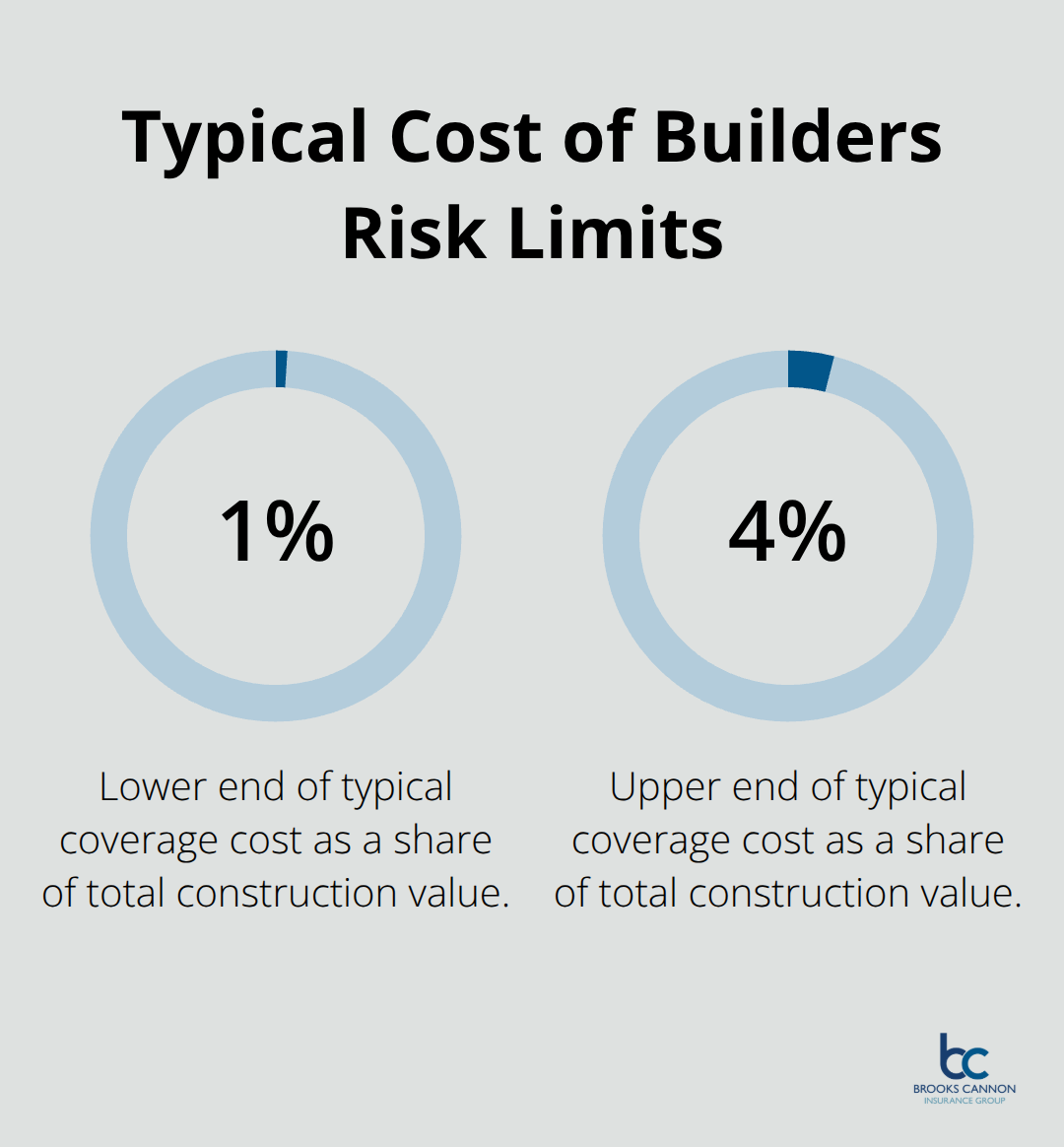

Your builders risk limit must cover your full project value, not rounded estimates. If your commercial construction project costs $1.2 million, your coverage limit should protect that entire amount plus contingency for material price increases and scope changes. Builders risk coverage limits typically cost 1% to 4% of the total construction value. A $250,000 residential project costs substantially less to insure than a $2.5 million commercial project, so your quote reflects your real exposure.

Many contractors underbuy coverage limits to save on premiums, then face partial claim denials when losses exceed their limits. This false economy costs far more than the premium difference. Your deductible choice directly impacts your monthly cost-a $5,000 deductible costs significantly less than a $1,000 deductible, but only select a higher deductible if your company can absorb that loss without financial strain.

Deductibles and Cash Flow Reality

Dallas-area contractors operating with tight cash flow should prioritize lower deductibles over slightly lower premiums. A claim with a $10,000 deductible during project cash flow shortage can disrupt your ability to pay workers and suppliers. Location matters significantly in determining your premium, so obtain quotes specific to your Dallas zip code and surrounding areas where materials stage. A project in downtown Dallas carries different risk than one in the suburbs, and your premium reflects that geographic reality.

Essential Endorsements for Complete Protection

Your coverage must include materials in transit and stored off-site before delivery to the job-this isn’t optional if you stage materials at a warehouse or distribution center. Installation floater endorsements protect high-value fixtures and equipment that become permanent building components. Soft costs endorsements cover additional loan interest and lost revenue if weather or other covered perils delay project completion. These additions strengthen your protection without leaving gaps that could cost thousands during a loss event.

Shop Multiple Carriers for Real Savings

Request quotes from at least three carriers because each underwriter weights risk factors differently. What one carrier charges standard rates for, another may decline entirely. Carriers like The Hartford, Cincinnati, Travelers, AIG, and Chubb actively compete for construction business, so shopping your specific project details across multiple insurers typically reveals significant premium variation for identical coverage.

Timing your insurance application before materials arrive gives carriers time to properly underwrite your risk and lock in capacity. Waiting until your first delivery creates pressure that forces you to accept whatever terms come quickly. Early engagement with an independent agent who understands Dallas-area construction risk helps you navigate carrier appetite and endorsement requirements without guesswork.

Align Your Policy with Contract Requirements

Your contract language with lenders and project owners specifies required coverage limits and additional insureds, so review those documents before requesting quotes and provide them to carriers during underwriting. This alignment prevents quote rejections or coverage gaps that could trigger contract breaches when your policy fails to meet stated requirements. Your lender and project owner need protection too, and naming them as additional insureds on your policy satisfies contractual obligations while keeping everyone’s financial interests protected.

Final Thoughts

Commercial builders risk coverage protects your construction investment from the financial devastation that a single loss event can cause. The protection you secure today determines whether your project survives unexpected damage or whether you absorb catastrophic costs that threaten your business. Your builders risk policy fills the gap that general liability leaves open, covering the materials, equipment, and structures that represent your actual construction value.

Getting covered requires action before your materials arrive on-site. Contact multiple carriers to compare quotes specific to your Dallas-area project, provide your contract documents to verify coverage meets lender and owner requirements, and select deductibles that match your company’s cash flow capacity. Early engagement with underwriters locks in capacity and favorable terms before market conditions tighten further on your project type.

An independent agent who understands Dallas construction risk transforms this process from overwhelming to straightforward. At Brooks Cannon Insurance Group, we work with multiple top-rated insurance carriers to find the best coverage and pricing for your specific project. Our licensed experts review your contract requirements, identify coverage gaps, and secure quotes that protect your financial interests without overpaying for unnecessary coverage.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation