Your engagement ring, heirloom necklace, and luxury watch deserve protection that goes beyond what a standard homeowners policy offers. Most basic home insurance policies cap jewelry coverage at $1,500 to $2,500, leaving high-value pieces dangerously underprotected.

At Brooks Cannon Insurance Group, we see Dallas residents lose thousands in jewelry claims every year because they assumed their homeowners policy had them covered. The good news is that fine jewelry coverage options exist to fill those gaps and protect what matters most to you.

Why Your Homeowners Policy Leaves Jewelry Unprotected

Your homeowners policy has a jewelry problem, and it’s probably worse than you think. Most standard homeowners policies in Texas cap jewelry coverage at $1,500 total, regardless of what you actually own. If you have an engagement ring worth $8,000, a vintage watch valued at $3,500, and heirloom pieces totaling another $5,000, your policy covers only a fraction of that loss. Dallas residents often discover this gap only after filing a claim, and by then it’s too late. The policy language is clear: scheduled items like jewelry fall under the broader category of personal property, which means they’re subject to strict limits and exclusions that don’t apply to your home’s structure.

The Real Limits on Jewelry Claims

Standard homeowners policies treat jewelry the same way they treat clothing or kitchen appliances. You receive a flat sublimit, meaning the insurer won’t pay more than that threshold for all jewelry combined, even if individual pieces are worth significantly more. A $10,000 engagement ring and a $15,000 watch collection both hit your policy’s jewelry limit. Additionally, many policies exclude coverage for jewelry lost outside the home or taken during travel. If your diamond ring slips off your finger at a restaurant in Dallas or disappears while you’re traveling, your homeowners policy likely won’t cover it. Mysterious disappearance-one of the most common ways people lose jewelry-is typically excluded entirely from standard homeowners coverage.

Exclusions That Leave You Exposed

Beyond the dollar limits, homeowners policies contain exclusions specifically designed to avoid covering high-value items. Loss due to mysterious disappearance, accidental damage during normal wear, and theft from vehicles all remain commonly excluded. Some policies won’t cover jewelry left with a jeweler for repair or appraisal, creating a gap precisely when your pieces are most vulnerable. Damage from normal wear and tear isn’t covered either, which means if a prong loosens and a stone falls out, you pay for that repair yourself. These exclusions exist because standard homeowners policies weren’t built to protect valuable jewelry-they were built to cover household basics.

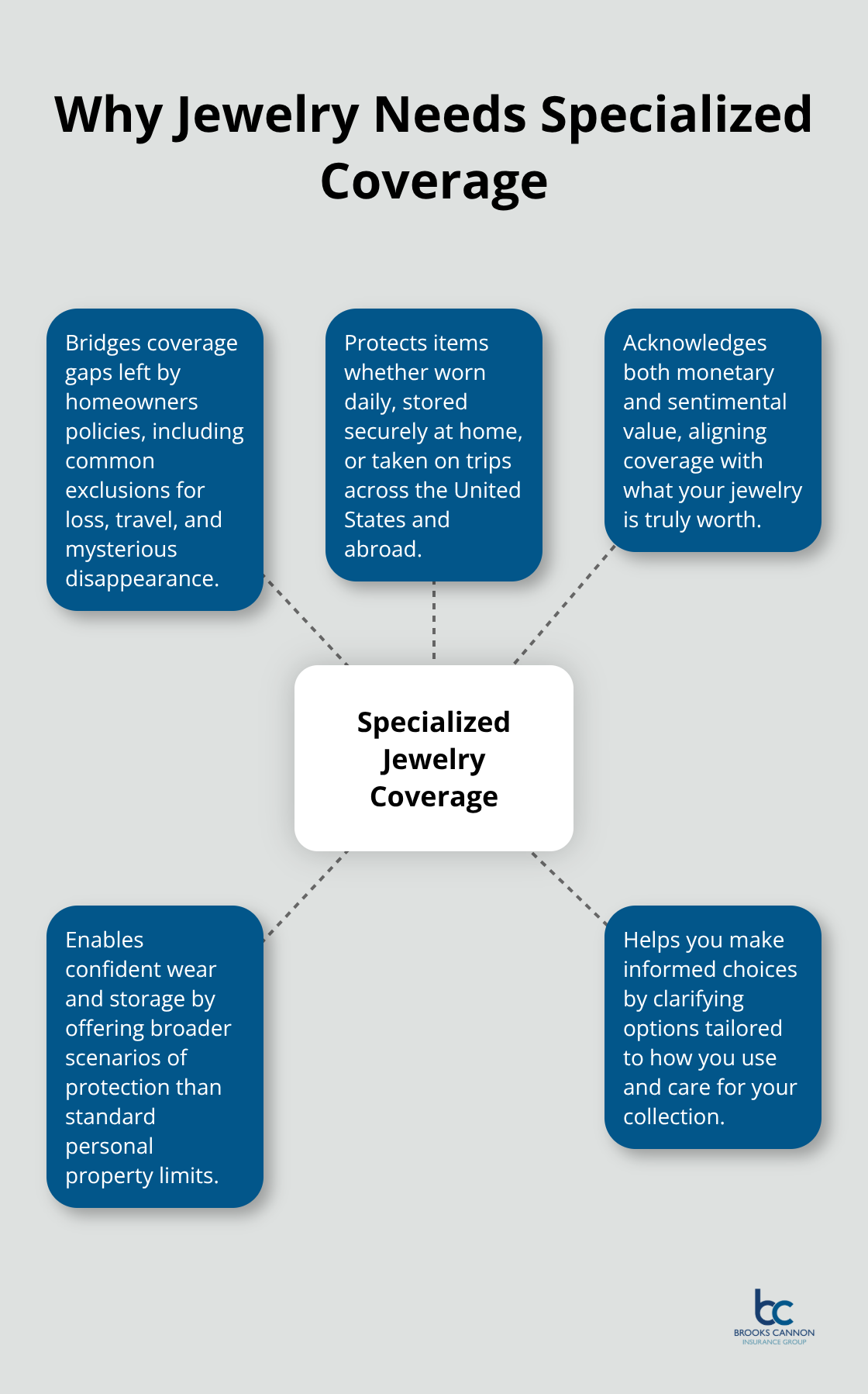

Why Jewelry Needs Different Protection

Jewelry requires a different approach, one that acknowledges both the monetary and sentimental value of these pieces. Specialized jewelry coverage fills the gaps that homeowners policies leave wide open. The right policy protects your collection whether you wear it daily, store it safely, or travel with it across the country. Understanding what specialized coverage options exist helps you make an informed decision about protecting your most treasured possessions.

Types of Fine Jewelry Coverage Available

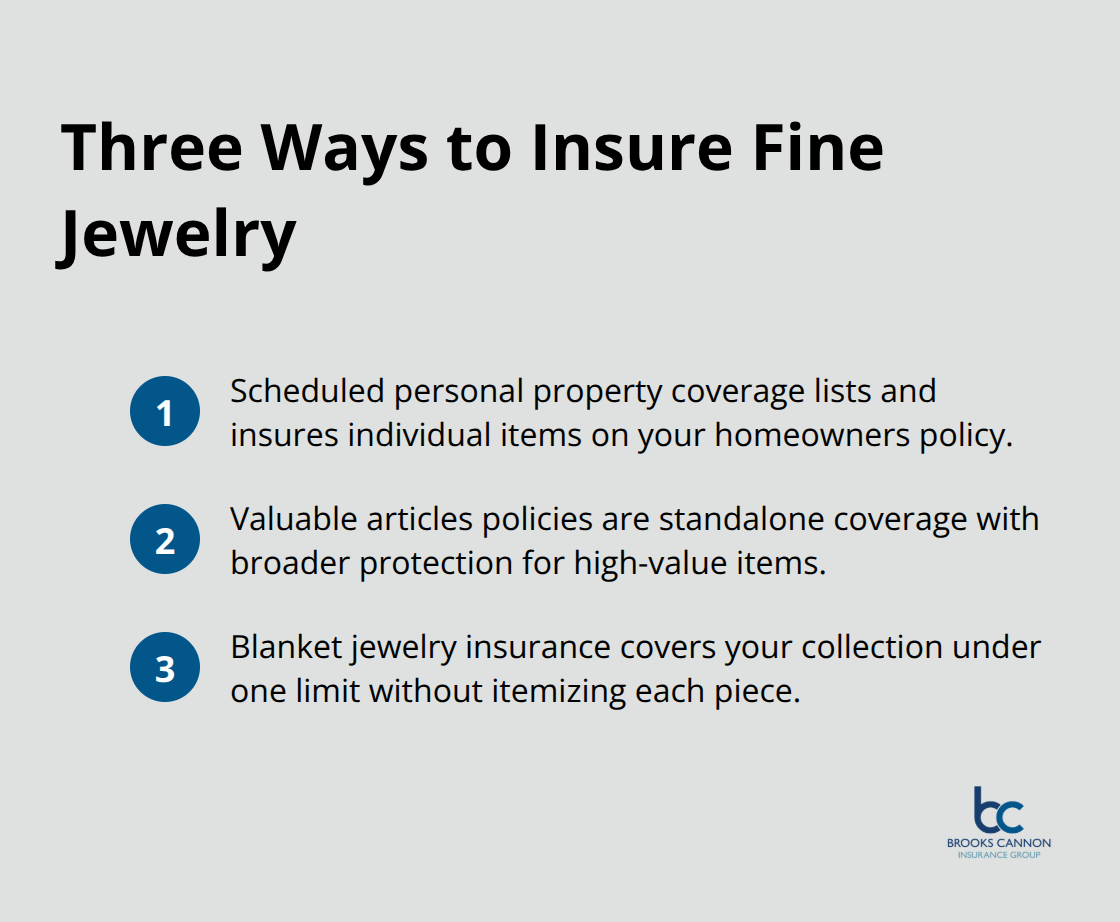

When your homeowners policy won’t cover the full value of your jewelry, three main options exist to fill that protection gap. Scheduled personal property coverage adds specific items to your homeowners policy with their individual values listed and insured separately. Valuable articles policies work similarly but operate as standalone coverage specifically designed for high-value items like jewelry, fine art, and collectibles. Blanket jewelry insurance covers your entire collection under one policy limit without requiring you to list each piece individually.

Each approach offers distinct advantages depending on your collection’s size, value, and how actively you wear your pieces.

Scheduled Personal Property Coverage

Scheduled personal property coverage typically costs around 1 to 2 percent of the jewelry’s value annually, according to Jewelers Mutual Insurance Group. A $5,000 engagement ring costs approximately $50 to $100 per year in additional premiums. This option requires a professional appraisal for each piece you want to schedule, and you’ll need to provide documentation showing the item’s value and description. The major advantage is that scheduled coverage provides greater protection for your most valued belongings. You must update your schedule whenever you acquire new pieces or have items professionally revalued every two years, since jewelry values fluctuate and underinsurance becomes a real risk.

Valuable Articles Policies

Valuable articles policies operate on the same principle as scheduled coverage but typically offer broader protection. They include mysterious disappearance, worldwide travel protection, and the ability to choose your own jeweler for repairs. These policies often include preventive maintenance coverage that pays for prong re-tipping, stone tightening, and clasp replacement without requiring you to file a claim. The comprehensive nature of valuable articles policies makes them attractive for collectors who want maximum protection across multiple scenarios (travel, daily wear, and storage).

Blanket Jewelry Insurance

Blanket jewelry insurance provides a simpler approach if you prefer not to itemize everything. Instead of scheduling individual pieces, you select a total coverage limit that applies to your entire collection, and you’re protected whether you own five pieces or fifty. This option works well for people with diverse collections where individual items fall below $2,000 in value, though it requires honesty about your total collection value when applying. The trade-off is that blanket coverage sometimes comes with slightly higher premiums than scheduled options, and you won’t have the same level of documentation for each piece during a claim.

Choosing the Right Coverage for Your Situation

The best option depends on your specific needs and collection characteristics. If you own several high-value pieces that you can document and appraise, scheduled or valuable articles coverage protects each item to its full value. If your collection consists of many smaller pieces or you prefer simplicity, blanket coverage offers straightforward protection. As an independent insurance agency based in Dallas, we work with multiple top-rated carriers to help you find the coverage that matches your jewelry’s value and your lifestyle. The next step involves taking concrete action to protect what you own, starting with professional appraisals and proper documentation.

How to Protect Your Jewelry Collection

Get Professional Appraisals and Documentation

Professional appraisals form the foundation of proper jewelry protection, and waiting until after a loss to obtain one costs you thousands. Jewelers Mutual Insurance Group recommends updating professional appraisals every two to three years because jewelry values fluctuate and you risk underinsurance if valuations fall behind market reality. A formal appraisal costs between $50 and $150 per piece from a GIA-certified gemologist, which sounds expensive until you consider that a $10,000 engagement ring underinsured by just $3,000 leaves you absorbing that loss out of pocket. When you apply for scheduled personal property coverage or valuable articles policies, insurers require documentation showing each piece’s value, description, and condition.

Gather receipts from original purchases, professional appraisals with gemstone specifications, photographs from multiple angles, and any certificates of authenticity for high-value stones. Maintain copies in a cloud-based service that survives house fires or theft, alongside physical copies stored separately. Photograph your jewelry against a neutral background in natural light, capturing details like hallmarks, maker’s marks, and any unique characteristics that distinguish your pieces from similar items.

Store Items Safely and Securely

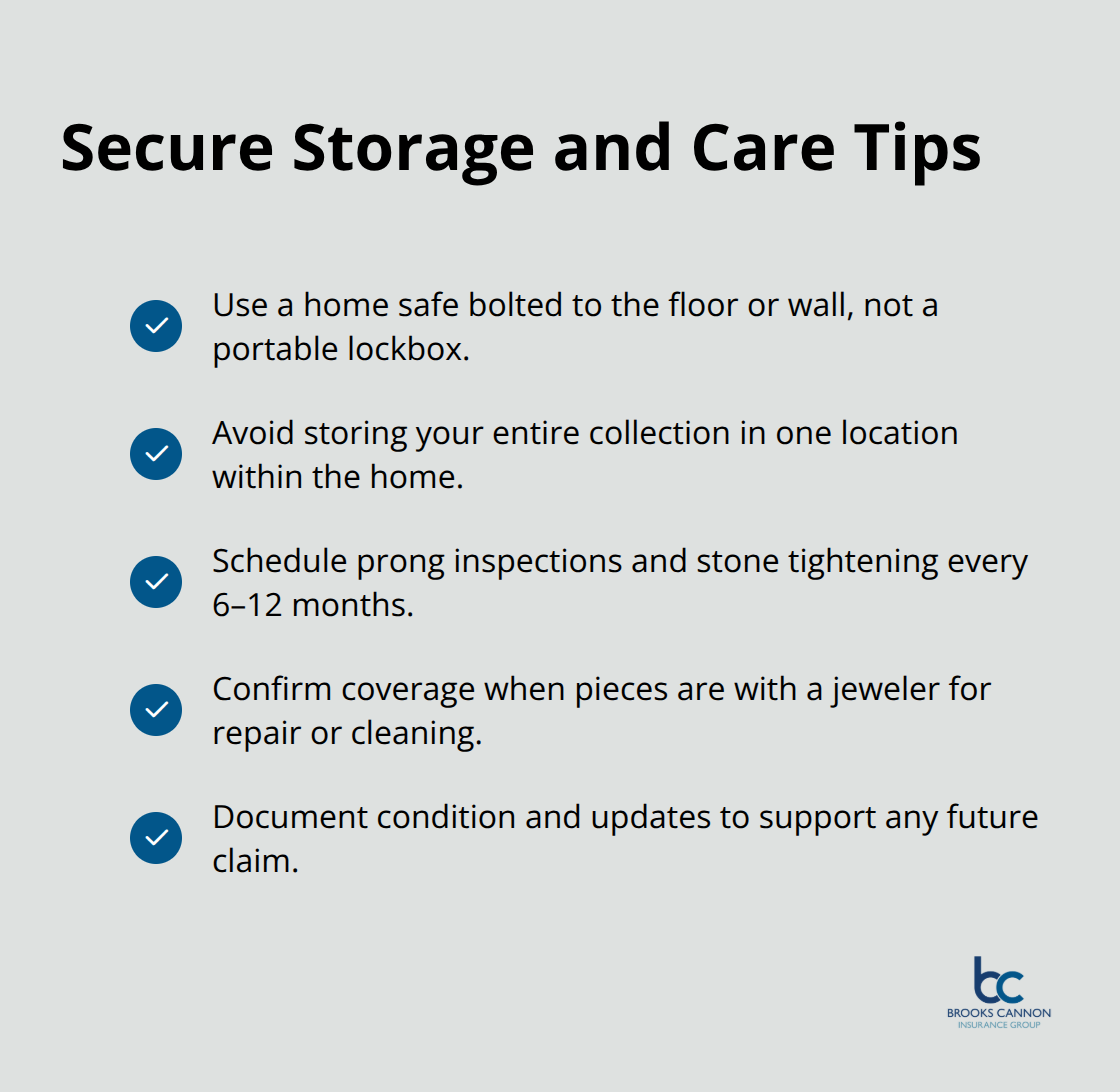

Storage and everyday handling practices directly impact your ability to file successful claims, making location and condition central to your protection strategy. Store valuable pieces in a home safe bolted to the floor or wall rather than a portable lockbox that thieves can remove entirely, and avoid keeping everything in one location where a single break-in eliminates your entire collection. If you wear high-value pieces daily, understand that damage from normal wear and tear receives no coverage under most policies, so schedule regular maintenance visits to your jeweler for prong inspection and stone tightening every six to twelve months.

When pieces leave your home for repair or professional cleaning, confirm that your insurance covers them while in the jeweler’s possession, since some standard policies create coverage gaps during these periods. This protection matters most when your jewelry is most vulnerable.

Review and Update Coverage Regularly

Review your current homeowners or renters policy annually and compare what it actually covers against what you own, then discuss gaps with an agent who can recommend appropriate specialized coverage. Dallas residents with jewelry collections exceeding $5,000 in total value should strongly consider standalone jewelry insurance rather than relying solely on homeowners coverage, since the cost of dedicated policies typically runs $50 to $100 annually for every $5,000 in coverage. As an independent agency based in Dallas, we work with multiple top-rated carriers to help you find the coverage that matches your jewelry’s value and your lifestyle.

Final Thoughts

Your jewelry collection represents more than monetary value-it holds memories, milestones, and moments that matter. Standard homeowners policies treat these treasures like everyday possessions, capping coverage at $1,500 or $2,500 regardless of what you actually own. That gap between what your policy covers and what your jewelry is worth creates real financial risk that grows every year.

Fine jewelry coverage exists specifically to close that gap. Whether you choose scheduled personal property coverage that protects individual pieces, valuable articles policies that offer comprehensive protection including mysterious disappearance and worldwide travel, or blanket jewelry insurance that simplifies the process, options exist to match your collection’s value and your lifestyle. The right coverage means you wear your jewelry with confidence instead of anxiety, knowing that loss, theft, or damage won’t devastate your finances.

Contact Brooks Cannon Insurance Group today to discuss your jewelry protection needs and receive a personalized recommendation based on your specific situation. As an independent agency based in Dallas, we work with multiple top-rated carriers to find fine jewelry coverage that fits your collection and your budget. Your treasures deserve protection that goes beyond standard homeowners coverage, and we’re here to make that happen.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation