Owning rental property in Dallas comes with real financial exposure. Liability claims, property damage, and lost rental income can quickly drain your profits if you’re not properly protected.

We at Brooks Cannon Insurance Group work with landlords every day who discover gaps in their coverage too late. The right rental property policy Dallas protects your investment and your bottom line.

What Rental Property Insurance Actually Covers

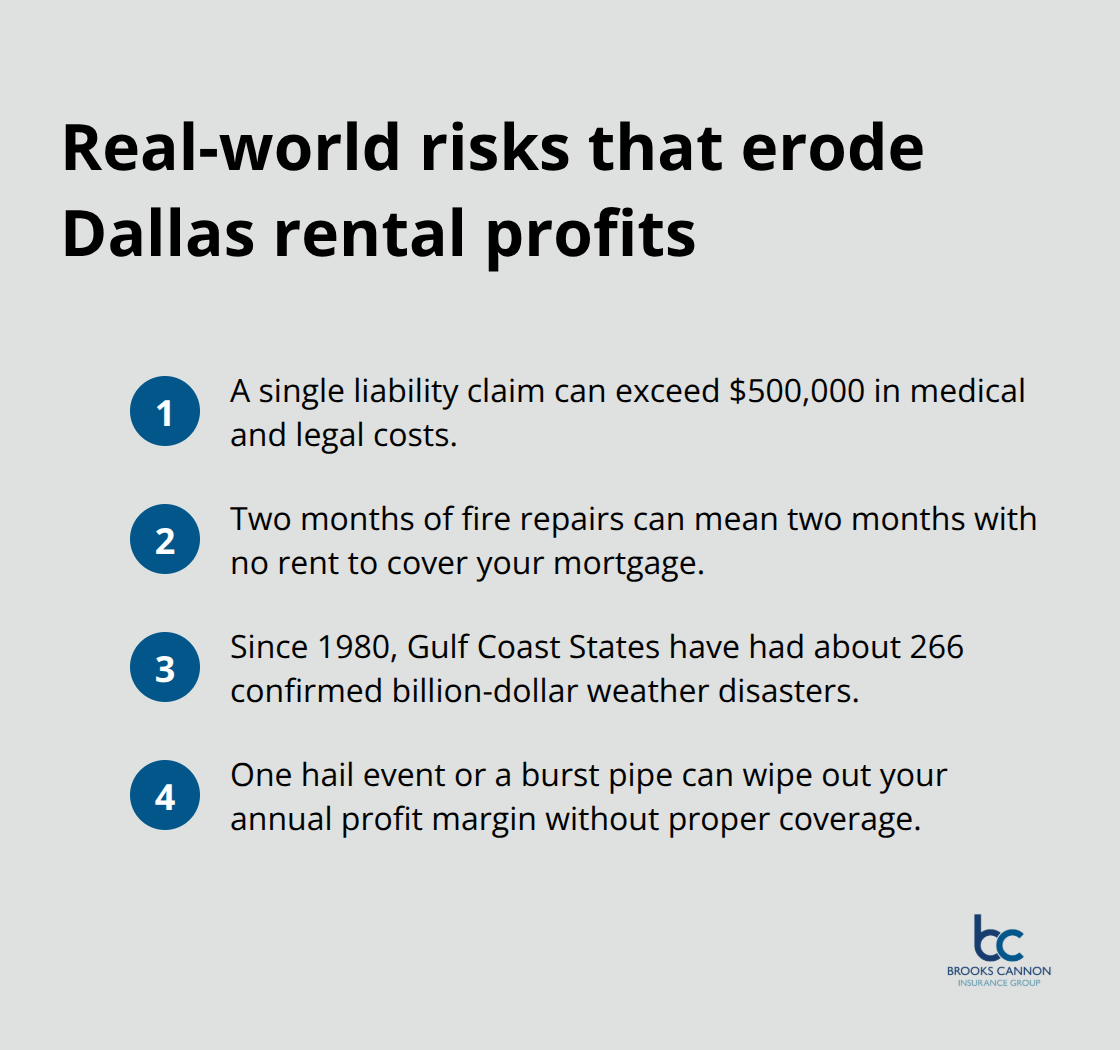

Rental property insurance in Dallas protects three critical areas that standard homeowners policies ignore: your building structure, liability exposure from tenants and visitors, and lost rental income when the property becomes uninhabitable. Standard homeowners insurance explicitly excludes rental properties, which means renting out a home without a dedicated landlord policy leaves you with zero protection. Texas law doesn’t require landlord insurance, but your mortgage lender almost certainly does. More importantly, the financial consequences of being uninsured are severe. A single liability claim where a tenant is injured on your property can exceed $500,000 in medical and legal costs. A fire that takes two months to repair means two months of lost rent with no income to cover your mortgage. Dallas experiences severe weather regularly-Gulf Coast States have endured about 266 confirmed billion-dollar weather disasters since 1980. One hail event or burst pipe can wipe out your entire profit margin for the year without proper coverage.

Why Standard Homeowners Insurance Fails Landlords

Your homeowners policy was written for owner-occupied properties. The moment you start collecting rent, that policy becomes invalid. Insurance companies view rental properties differently because tenant-occupied homes carry higher risk. Tenants have less incentive to maintain the property carefully, and your liability exposure increases dramatically when strangers live in your building. If a tenant’s guest slips on your icy stairs in winter and sues you for $100,000 in medical bills, your homeowners policy will deny the claim. You need a Dwelling Fire Policy (DP2 or DP3 form) specifically designed for rental properties. In Dallas, landlord insurance typically costs $1,555 or more per year for standard coverage, which is far cheaper than one uninsured claim.

What Happens When You Skip Coverage

Landlords often assume their homeowners policy covers rental income or believe liability claims won’t happen to them. Then reality hits. A water leak from burst pipes damages the structure and makes the unit uninhabitable for 60 days. Your tenant moves out. You still pay the mortgage, property taxes, and maintenance costs, but you collect zero rent. Loss of rent coverage would reimburse that income. Without it, you absorb the entire loss. Similarly, if your tenant’s visitor is injured and sues, your personal assets face risk. Liability coverage pays the medical costs, legal defense, and settlements up to your policy limits, protecting your savings and other property from judgment creditors.

The Real Cost of Underinsurance

Many Dallas landlords purchase the cheapest policy available and assume they’re protected. DP1 policies (the most basic option) offer only named-peril coverage and pay actual cash value rather than replacement cost, often leaving you significantly underinsured. A hail storm damages your roof, and the insurer pays you $8,000 based on the roof’s depreciated value. The actual cost to replace that roof runs $15,000. You cover the $7,000 gap out of pocket. DP2 and DP3 policies pay replacement cost, meaning the insurer covers what it actually costs to fix or rebuild the property today, not what it was worth five years ago. This matters enormously in Dallas, where construction costs have risen sharply and severe weather claims are common.

How Loss of Rent Coverage Protects Your Cash Flow

Loss of rent coverage reimburses your rental income when a covered event makes the property uninhabitable. A pipe bursts in January, flooding the unit and requiring 45 days of repairs. Your tenant cannot occupy the space, so you receive no rent. Loss of rent coverage pays you the monthly rent amount for those 45 days, helping you cover your mortgage and other expenses while repairs happen. Without this coverage, you face a cash flow crisis. Many landlords carry mortgages on their rental properties, and losing two months of income can mean missing payments or draining savings. This coverage is inexpensive compared to the financial protection it provides, typically adding just $200 to $400 annually to your policy.

Moving Forward With Proper Coverage

The right rental property policy Dallas protects your investment and your bottom line. Understanding what your current coverage includes-and what it excludes-is the first step toward real protection. As an independent insurance agency, we at Brooks Cannon Insurance Group work with multiple top-rated carriers to find coverage that matches your specific property and risk profile. The next section examines the specific coverage types every Dallas landlord should carry and how to determine whether your current limits are adequate for your situation.

Three Coverage Types That Actually Protect Your Dallas Rental

Dwelling Fire Policies: Building Protection That Matches Your Property

Dwelling fire policies form the foundation of rental property insurance, but most Dallas landlords misunderstand how these actually work and what limits they truly need. DP2 and DP3 policies pay replacement cost rather than actual cash value, which matters significantly when hail or wind damage strikes your property. A DP2 policy offers broad named-peril coverage and costs less than DP3, making it the practical choice for most Dallas rentals unless your property sits in a high-risk flood or windstorm zone. DP3 provides all-peril coverage (everything is covered unless specifically excluded) and works best for newer properties or those worth over $300,000.

In Dallas, where hail damage claims spike annually and 2024 recorded more hailstorms than any other state, the difference between DP2 and DP3 can mean thousands in out-of-pocket costs after a major event. A hail storm damages your roof, and a DP1 policy pays you $8,000 based on the roof’s depreciated value. The actual cost to replace that roof runs $15,000. You cover the $7,000 gap out of pocket. With replacement cost coverage, you receive what it actually costs to fix or rebuild the property today, not what it was worth five years ago.

Liability Coverage: Protecting Yourself From Injury Claims

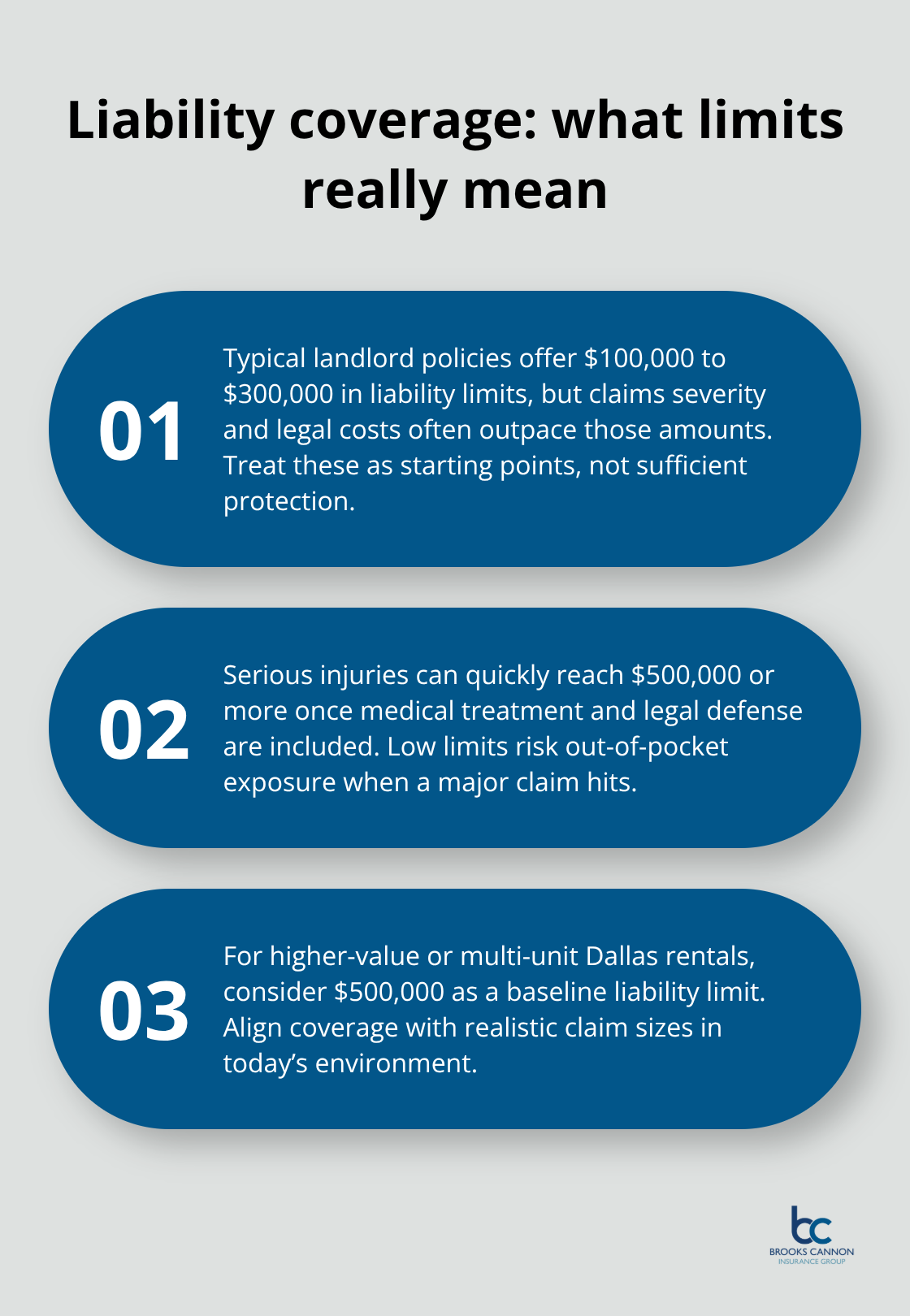

Liability coverage protects you when a tenant’s guest slips on your stairs or a visitor is injured on the property and sues. Standard policies typically offer $100,000 to $300,000 in liability limits, but that range often falls short. A serious injury claim easily reaches $500,000 or more in medical bills and legal defense costs. Many Dallas landlords with high-value properties or multiple units should consider $500,000 in liability coverage as a baseline, not a luxury.

Medical payments coverage, which is separate from liability, covers minor injuries up to $1,000 to $5,000 without requiring fault. This coverage helps you avoid lawsuits for small incidents. If your tenant’s guest trips on a loose step and breaks an arm, medical payments coverage pays the hospital bills directly, preventing a formal claim and potential litigation.

Loss of Rent Coverage: Protecting Your Cash Flow During Repairs

Loss of rent coverage reimburses your monthly rental income when a covered event makes the property uninhabitable. A pipe bursts in January, flooding the unit and requiring 45 days of repairs. Your tenant cannot occupy the space, so you receive no rent. Loss of rent coverage pays you the monthly rent amount for those 45 days, helping you cover your mortgage and other expenses while repairs happen.

Most landlords fail to purchase adequate limits for this coverage. If you collect $2,000 monthly rent, your loss of rent coverage should reimburse that full amount for at least 6 to 12 months of potential repairs. Many policies limit loss of rent to 6 or 9 months, which sounds reasonable until your roof needs complete replacement and the contractor books a three-month wait. You face months of zero income while waiting for repairs to start. Calculate your actual monthly rent, multiply by the number of months repairs realistically take in your area, and ensure your policy matches that figure. Adding loss of rent coverage typically costs $200 to $400 annually but prevents catastrophic cash flow problems when disaster strikes your Dallas investment.

Determining Your Actual Coverage Needs

The right coverage limits depend on your specific property, rental income, and risk profile. A single-family home renting for $1,500 monthly requires different limits than a four-unit apartment building generating $8,000 in monthly income. Your liability exposure also varies based on property features (pools and trampolines increase risk significantly) and tenant demographics. An independent insurance agent can review your property details and help you select DP types and limits that actually match your situation rather than forcing you into a one-size-fits-all package.

The next section examines the gaps that appear in most Dallas rental policies and the specific endorsements that fill those holes before a claim forces you to pay out of pocket.

Coverage Gaps That Cost Dallas Landlords Thousands

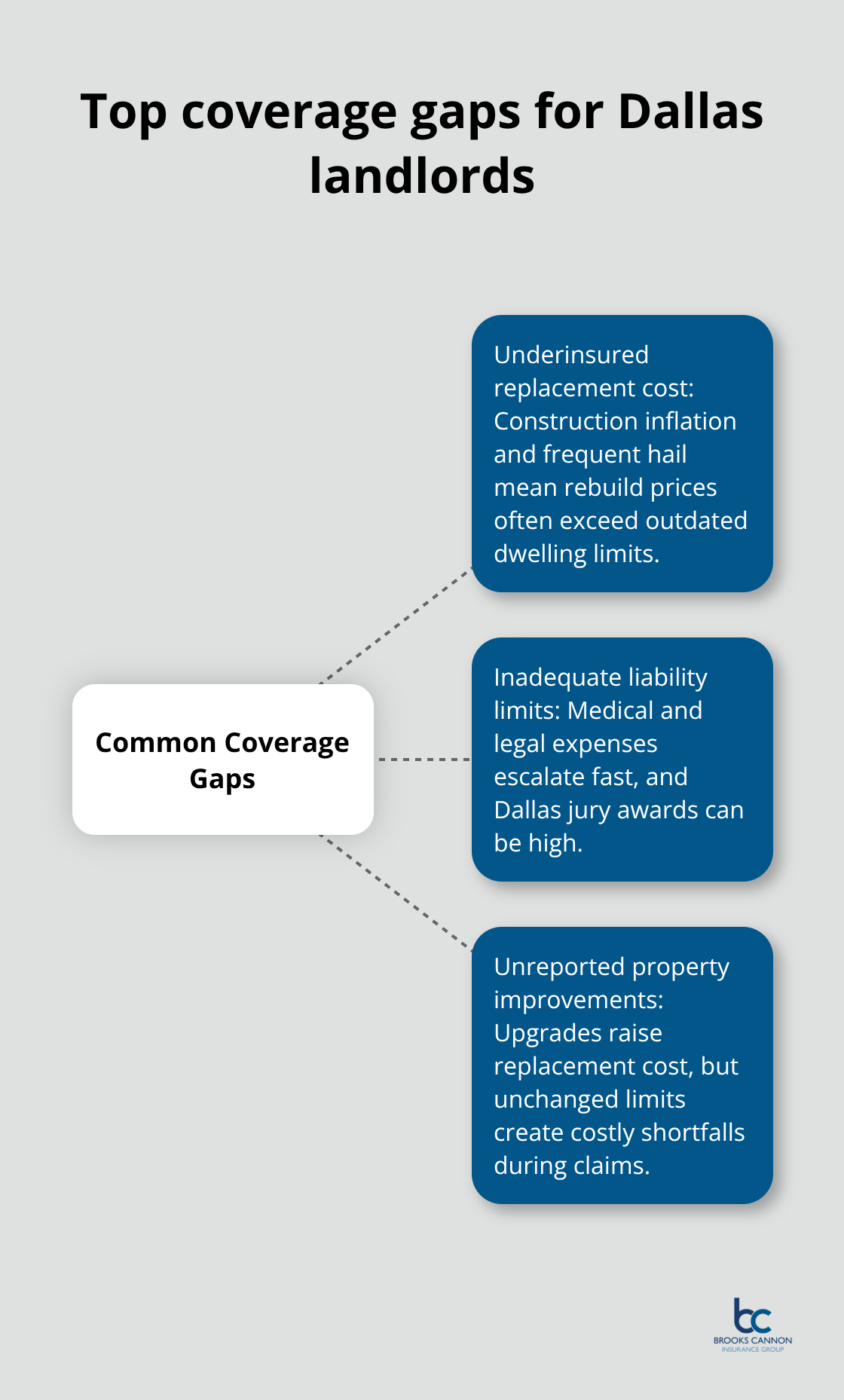

Most Dallas landlords discover their policy gaps only after a claim strikes. You selected dwelling fire coverage and liability protection, but your policy still contains exclusions that leave you exposed to major losses. The three most damaging gaps appear consistently across rental properties in our market: underinsuring the actual replacement cost of your building, carrying liability limits that sound adequate until a serious injury claim arrives, and failing to update your coverage when you invest in property improvements. These gaps rarely matter until disaster strikes, then they become catastrophically expensive.

The Replacement Cost Trap That Catches Most Landlords

Replacement cost coverage sounds straightforward until you actually price repairs in Dallas. Construction costs have climbed sharply over the past three years, and hail claims spike annually in our region. Many landlords set their dwelling coverage limit based on what they paid for the property five or ten years ago, assuming that figure represents their actual exposure. A rental home purchased for $250,000 in 2015 might cost $380,000 to fully rebuild today, yet the owner still carries a $250,000 coverage limit.

When a major hail event damages the roof, foundation, and siding simultaneously, the $250,000 limit disappears quickly. The contractor estimates $75,000 for roof replacement alone, $45,000 for foundation repairs, and $30,000 for siding and exterior damage. Your coverage runs out at $100,000 of actual damage, leaving you responsible for the remaining $50,000. This scenario happens regularly in Dallas because property values shift faster than owners update their insurance limits.

Calculate your property’s actual replacement cost every two to three years, not the price you paid when you bought it. Many carriers offer replacement cost calculators on their websites, or an independent agent can order a professional valuation. If your property would cost $350,000 to rebuild completely from the foundation up, your dwelling coverage should match that figure, not the original purchase price.

Liability Limits That Fail When You Need Them Most

A $100,000 liability limit feels substantial until your tenant’s guest suffers a serious injury on your property. Medical costs for a broken leg requiring surgery, hospital stay, and physical therapy easily reach $80,000 before legal fees and pain-and-suffering damages enter the claim. A more severe injury-spinal cord damage, permanent disability, or death-generates claims exceeding $500,000 regularly.

Dallas juries award significant damages in injury cases, and your liability coverage must reflect that reality. Many landlords set limits years ago and never revisited them, unaware that inflation and rising medical costs have eroded their actual protection. A $300,000 limit from 2018 provides roughly $260,000 in real purchasing power today. If a guest drowns in your property’s pool or suffers a head injury from a fall, your $300,000 limit evaporates within weeks of the claim.

High-risk property features amplify this exposure dramatically. Pools, hot tubs, stairs, balconies, and properties in older buildings with outdated electrical systems attract higher injury claims. Dallas landlords with these features should carry minimum $500,000 in liability coverage, with $1,000,000 preferred if you own multiple properties or high-value units. The cost difference between $300,000 and $500,000 in liability coverage typically runs $30 to $50 annually-negligible protection for the actual exposure you face.

Umbrella policies provide additional liability coverage beyond your primary policy limits, typically offering $1,000,000 in extra protection for around $383 per year. This coverage becomes essential if you own multiple rental properties or carry significant personal assets that a judgment could threaten.

Property Improvements That Aren’t Covered

Most landlords upgrade their rental properties to attract better tenants or maintain competitiveness-new HVAC systems, updated electrical wiring, kitchen renovations, or bathroom upgrades. These improvements increase your property’s replacement cost, yet many owners fail to notify their insurance company. Your policy still covers the building at the original limit, now significantly below the actual replacement cost.

A $250,000 dwelling limit that was adequate before you invested $40,000 in upgrades now leaves you $40,000 underinsured. This gap compounds over time as you make multiple improvements. A new roof ($15,000), electrical panel upgrade ($8,000), and plumbing replacement ($12,000) total $35,000 in property improvements. If you never update your coverage limit, you face a $35,000 shortfall when a major claim occurs.

Some carriers automatically adjust your coverage limits based on inflation, but this adjustment rarely keeps pace with actual replacement costs in a rising market like Dallas. Notify your insurance agent whenever you complete substantial property improvements. Document the improvements with receipts and photos, then request a coverage limit review. This conversation takes fifteen minutes and prevents tens of thousands in underinsurance exposure. Dallas landlords should schedule this review annually, particularly if you’re actively upgrading your rental properties to remain competitive in our market.

Final Thoughts

Your rental property policy Dallas protects your investment only when it matches your actual exposure. The coverage gaps we outlined-underinsured dwelling limits, inadequate liability protection, and outdated limits after property improvements-cost landlords thousands annually. These gaps surface when a hail storm damages your roof, a tenant’s guest suffers a serious injury, or a pipe burst forces months of repairs, and the financial damage hits hard at that point.

Pull out your declarations page this week and verify three specific numbers: your dwelling coverage limit, your liability limit, and your loss of rent coverage amount. Compare your dwelling limit to what it would actually cost to rebuild your property today, not what you paid for it years ago. If you’ve made property improvements since purchasing your policy, add those costs to your replacement value calculation, and check whether your liability limit reflects the actual injury exposure on your property.

Schedule a conversation with an independent insurance agent who represents multiple carriers, since different insurers price rental property coverage differently based on their underwriting criteria. We at Brooks Cannon Insurance Group work with landlords throughout Dallas to review existing coverage, identify gaps, and find policies that actually protect your investment without overpaying for unnecessary features. Contact Brooks Cannon Insurance Group to review your current coverage and strengthen your protection before the next hail storm or injury claim forces you to pay out of pocket.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation