Fine art collectors in Dallas face a unique challenge: standard homeowners insurance rarely covers the true value of valuable paintings, sculptures, and collectibles. We at Brooks Cannon Insurance Group understand that protecting your collection requires specialized fine art insurance Dallas tailored to your specific pieces.

This guide walks you through the essential steps to safeguard your investment, from proper valuation and documentation to selecting the right coverage and securing your collection.

How to Value Your Fine Art Correctly

Get a Professional Appraisal from a Certified Expert

An accurate appraisal is non-negotiable. A certified appraiser with credentials from the American Society of Appraisers or International Society of Appraisers will evaluate your pieces based on current market conditions, not what you paid for them years ago. In Dallas, appraisers who specialize in fine art should follow USPAP standards and ISA Ethical Standards to hold up during a claim. An experienced appraiser typically charges between 0.5% to 2% of the item’s appraised value-an investment that protects you from significant losses if your collection is undervalued.

The appraiser will document the artist, provenance, condition, size, materials, and comparable sales data. This documentation becomes your insurance foundation and protects you during disputes about value. Many collectors use the purchase price as their insured value, which leaves them exposed. A painting purchased for $5,000 ten years ago might be worth $15,000 today, or it might be worth $2,000. Markets shift. Artists’ reputations change. You need current market value, not historical cost. Search for a qualified ISA appraiser to evaluate your collection.

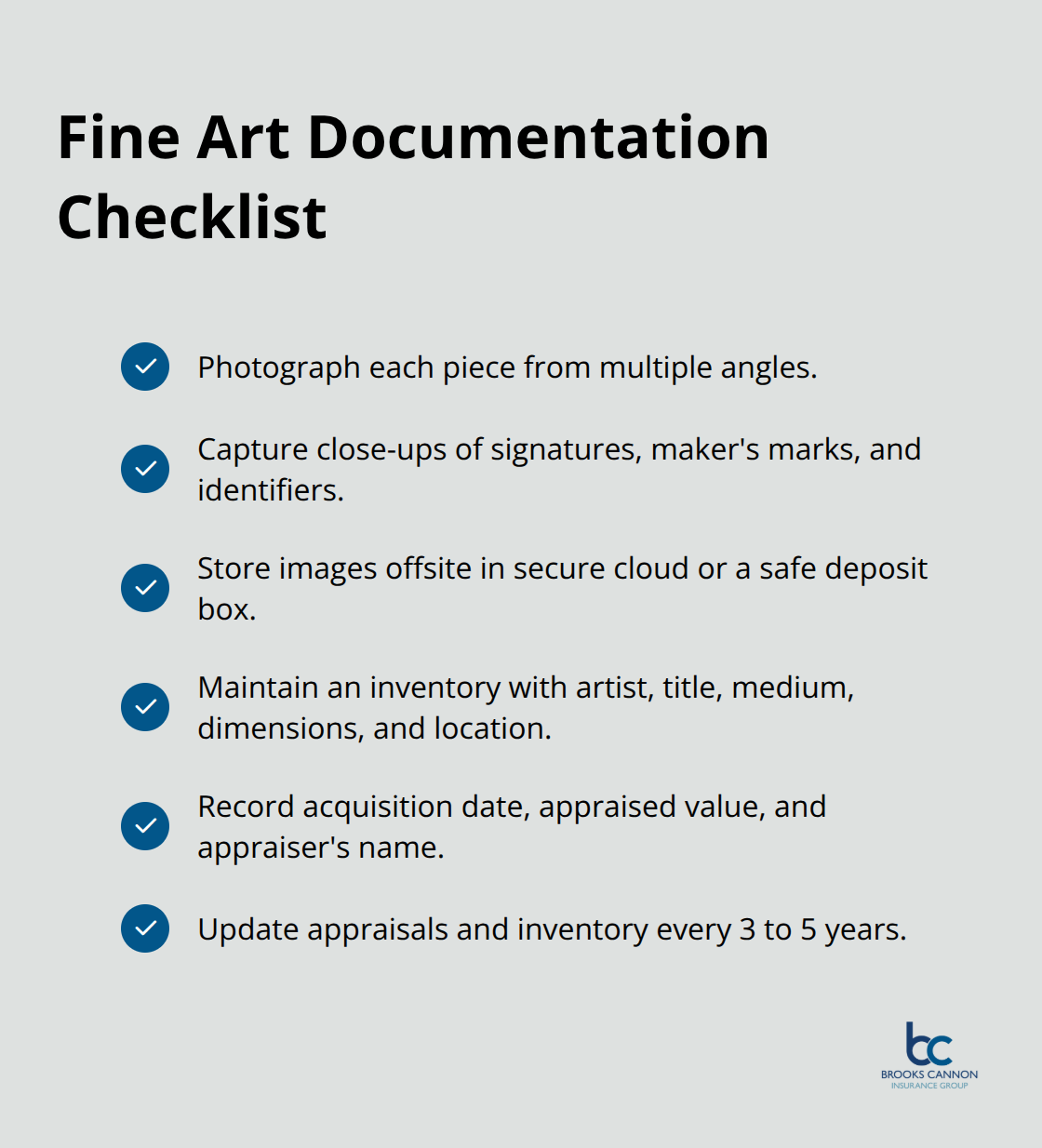

Document Each Piece with Photographs and Detailed Records

After appraisal, photograph each piece from multiple angles under proper lighting. Include close-ups of any signatures, maker’s marks, or identifying features. Store these photos separately from your home-use cloud storage or a safety deposit box.

Create a detailed inventory spreadsheet that includes the artist name, title, medium, dimensions, acquisition date, appraised value, location in your home, and the appraiser’s name.

If you own rare books, coins, or collectibles, add specific details like edition numbers or serial numbers. This inventory is what insurance adjusters request when you file a claim. Without it, you rely on memory during an already stressful situation. Update your appraisals every three to five years, especially for pieces by living artists or those in volatile market segments. The market volatility in contemporary art means values can shift significantly depending on the artist’s career trajectory and exhibition history.

Keep Your Insurance Policy Aligned with Current Values

Your insurance policy should reflect current reality, not outdated valuations. When you work with an independent insurance agent in Dallas, they will help you select coverage that matches your appraisals. This alignment protects you from underinsurance and ensures your collection receives the protection it deserves. The next step involves understanding which coverage options actually work for fine art collections.

Choosing the Right Coverage Type

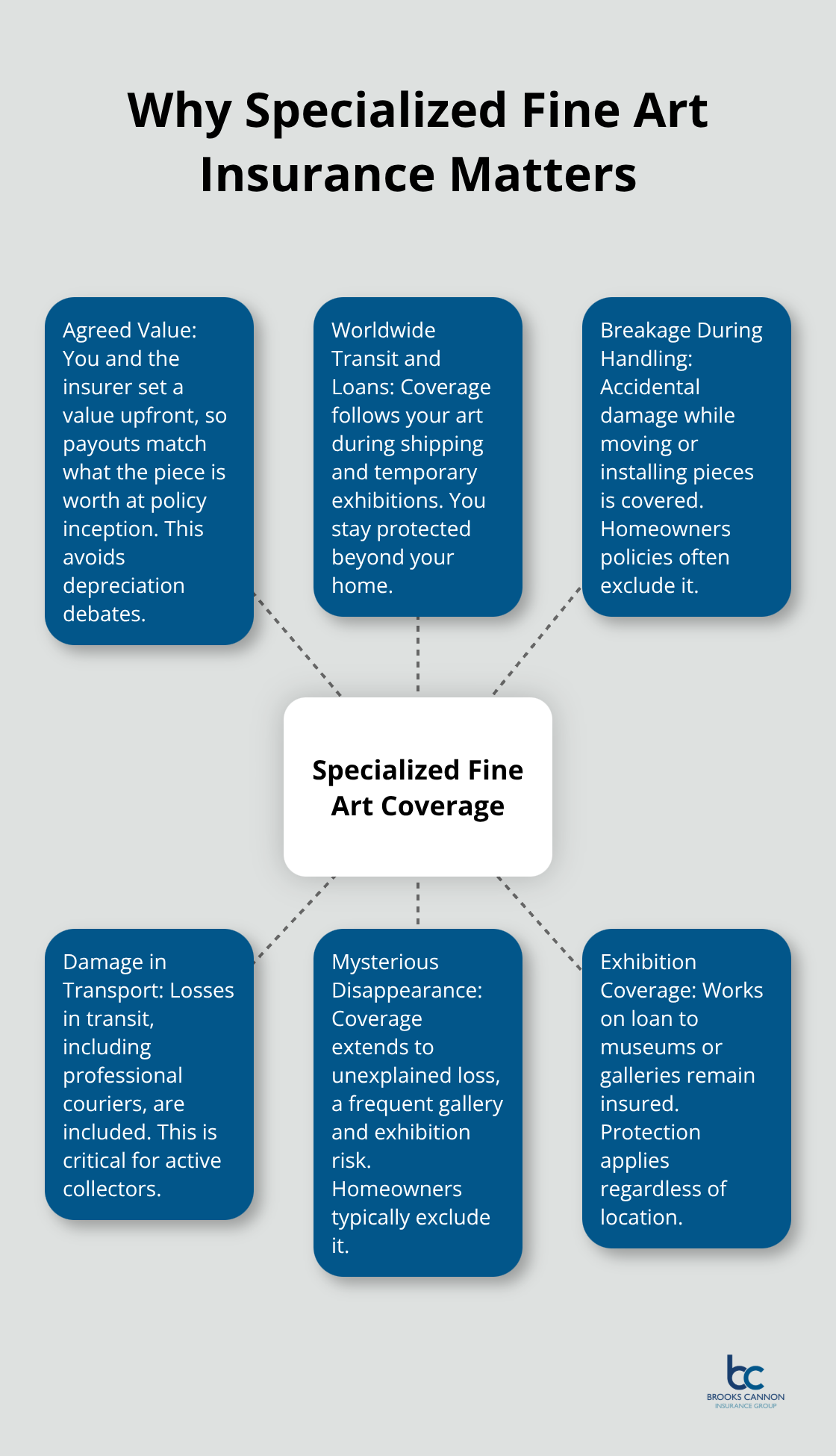

Standard homeowners insurance typically caps fine art coverage at $2,500 total, which is catastrophically low for serious collectors. Many clients discover this limitation only after a loss, and by then it’s too late. Specialized fine art insurance exists precisely because your collection deserves protection that matches its actual value.

How Valuation Methods Protect Your Collection

The fundamental difference between homeowners and fine art policies comes down to how they handle valuation. Homeowners policies use replacement cost or actual cash value, meaning they depreciate your pieces and cap payouts at arbitrary limits. Fine art policies use agreed value or current market value, meaning you and your insurer agree upfront on what each piece is worth, and that’s what you receive if a loss occurs.

This distinction matters enormously. A homeowners policy might offer $2,500 for a collection worth $150,000. A specialized fine art policy can cover the full $150,000 with no artificial ceiling. Beyond valuation, specialized fine art insurance covers risks that homeowners policies exclude entirely. Mysterious disappearance, breakage during handling, damage during transport, and loss during temporary loans or exhibitions all fall under fine art coverage.

Homeowners policies typically exclude these scenarios or severely limit them.

If you loan a painting to a Dallas museum for a six-month exhibition, your homeowners policy likely provides zero protection during that loan period. A fine art policy covers it worldwide, protecting your investment regardless of location.

Blanket Coverage versus Itemized Policies

Blanket coverage protects your entire collection under one valuation without requiring you to list every single piece. This approach works well if you own fifty items valued at $200,000 total but don’t want to document each one individually. The policy pays up to the blanket limit regardless of which specific pieces are damaged or stolen.

Itemized or scheduled coverage requires you to list high-value pieces separately with their individual appraisals and valuations. This approach costs more in underwriting time but provides clarity on exactly what’s protected. Most Dallas collectors benefit from a hybrid approach: blanket coverage for lower-value pieces under $5,000 each, and scheduled coverage for your most valuable works. For pieces valued above $10,000, always schedule them individually.

Additional Riders and Coverage Options

The riders available within fine art policies address specific scenarios you may face. Transit coverage protects pieces while they’re in shipment between your home, galleries, exhibitions, or storage facilities. Frame and crate coverage reimburses the cost of specialized packing materials and display equipment. Some policies offer coverage for pieces you’re acquiring or considering purchasing before they’re formally appraised.

When you work with an independent insurance agent to structure your fine art protection, they assess your specific collection composition, your display and storage practices, and your plans for lending or traveling with pieces. This assessment determines whether blanket, scheduled, or hybrid coverage makes sense for your situation and budget. The right coverage structure protects your investment while keeping your premiums reasonable. Once you’ve selected your coverage type, the next critical step involves how you physically protect your collection through proper security and environmental controls.

Protecting Your Collection from Environmental and Physical Threats

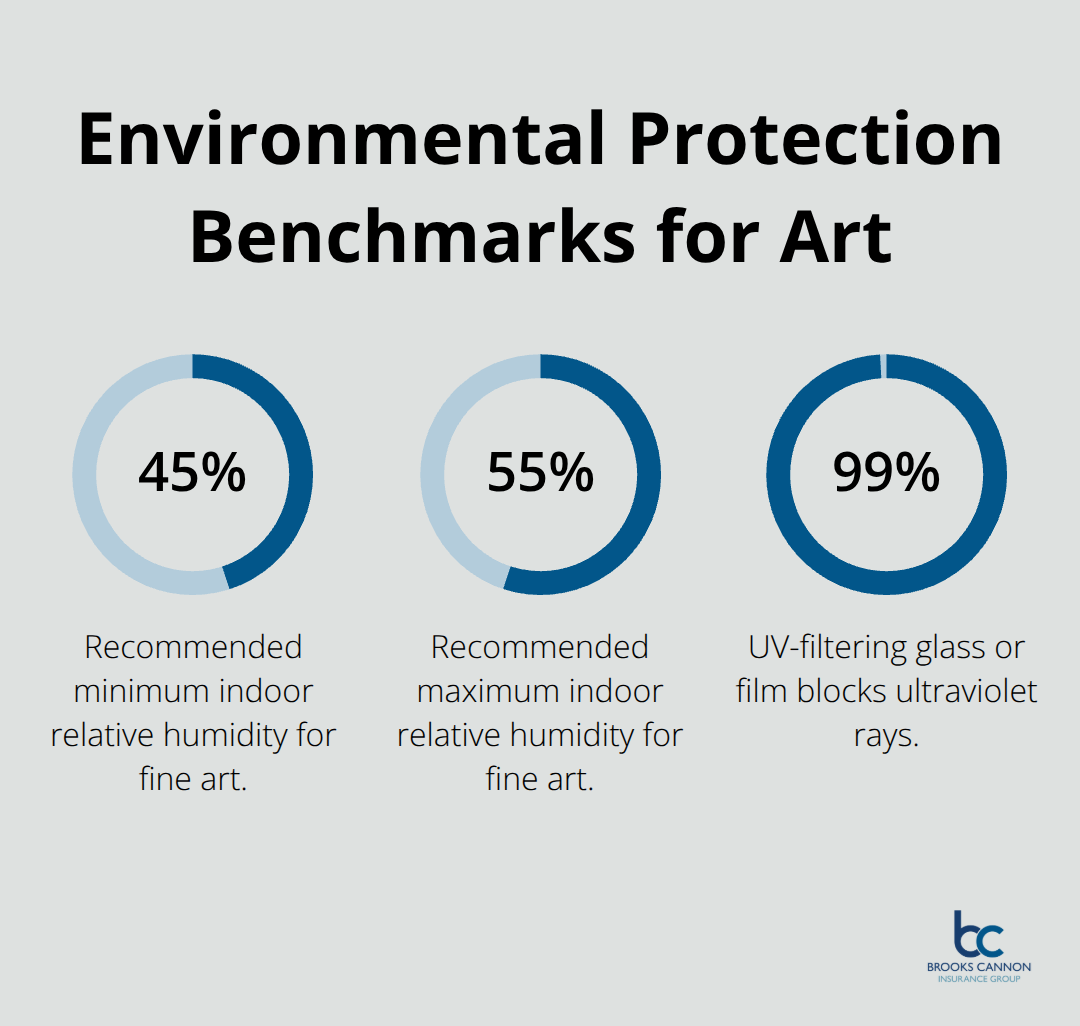

Fine art deteriorates when exposed to fluctuating temperature and humidity levels. Most Dallas collectors don’t realize that a single season of temperature swings causes permanent damage to paintings, photographs, and wooden frames. You should maintain optimal climate conditions for fine art storage with humidity levels between 45 and 55 percent year-round. This consistency prevents wood from warping, paint from cracking, and paper-based works from becoming brittle. Install a dedicated HVAC system or upgrade your existing one with a humidity control feature if you display pieces in a main living area. For high-value collections stored in a separate room or vault, invest in a standalone climate control unit with a digital monitoring system. These systems typically cost between $2,000 and $8,000 installed, but they protect collections worth far more. Check your climate readings monthly and maintain a log-insurance adjusters request this documentation during claims, and it demonstrates that you took reasonable precautions to prevent loss.

Display Location Affects Both Risk and Insurance Costs

The location of your displayed pieces determines both insurance costs and actual loss risk. Pieces hung in high-traffic areas near windows face greater risk from sunlight damage, accidental impact, and theft. Direct sunlight fades pigments and degrades paper fibers, sometimes irreversibly. If you must display valuable works near windows, install UV-filtering glass or window film that blocks 99 percent of ultraviolet rays. The cost runs $15 to $25 per square foot, but it preserves your collection’s condition and can lower your insurance premiums.

Insurance underwriters specifically ask about display locations because they correlate directly with loss frequency. A painting displayed in a secure study away from main traffic patterns presents lower risk than the same piece hanging in an entryway visible from the street. Position high-value pieces where only you and invited guests see them, not where anyone passing by a window can view them. Install motion-sensor lighting around displayed collections so that anyone entering that space triggers illumination-this deters theft and demonstrates active security measures to your insurer.

Storage Conditions Require Climate Control

Pieces not currently displayed need proper storage conditions that match your display environment. A temperature-controlled storage unit in a climate-controlled facility costs $100 to $300 monthly, depending on size and location in the Dallas area. This investment is non-negotiable for collections valued above $50,000. Standard home closets, attics, and basements expose pieces to seasonal temperature swings that cause damage. Never store art in attics where summer heat exceeds 100 degrees or basements where humidity fluctuates with groundwater. If you store pieces at home despite these warnings, use archival-quality storage boxes and acid-free tissue paper to minimize deterioration. Store paintings vertically, never stacked horizontally, to prevent warping. For long-term storage of multiple pieces, a dedicated fine art storage facility with 24-hour security, climate monitoring, and fire suppression systems provides comprehensive protection. These facilities charge premium rates but include insurance considerations in their design. When your fine art insurance policy covers pieces in transit or stored off-site, the insurer requires documentation of the storage facility’s security measures, climate controls, and fire prevention systems. Provide your agent with these specifications upfront so coverage reflects actual conditions. This transparency prevents coverage disputes and protects your pieces throughout their storage period.

Final Thoughts

Protecting your fine art collection requires three interconnected actions: accurate valuation through certified appraisals, appropriate insurance coverage matched to your collection’s actual value, and physical safeguards through climate control and security measures. Standard homeowners policies fail collectors because they cap fine art coverage at $2,500 total, while specialized fine art insurance Dallas provides protection that matches your investment’s true worth. The appraisals, photographs, and detailed inventory you maintain become your foundation for both coverage and claims resolution.

Your display and storage decisions directly impact both your collection’s condition and your insurance costs. Climate-controlled environments, proper positioning away from direct sunlight, and secure storage facilities prevent deterioration while demonstrating to insurers that you take reasonable precautions. These investments in environmental protection often reduce your premiums because they reduce loss frequency and show responsible stewardship of valuable pieces.

An independent insurance agent who understands fine art specifically can assess whether blanket coverage, scheduled policies, or hybrid approaches work best for your situation. Contact Brooks Cannon Insurance Group to discuss how we structure protection that actually covers what matters to you, and schedule a review every three to five years as your collection and market values shift.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation