Construction projects in Dallas face real risks from day one. Weather damage, theft, and liability claims can derail timelines and budgets before a single wall goes up.

New build coverage protects what matters most during construction. At Brooks Cannon Insurance Group, we’ve seen too many builders skip proper insurance only to face devastating losses they could have prevented.

Why Your Dallas Construction Project Needs Protection Before Day One

Dallas County experienced over 50 tornadoes in the past decade, and that statistic alone explains why standard homeowners insurance leaves construction projects completely exposed. When you build in Dallas, your materials sit vulnerable to hail, wind, theft, and vandalism from the moment they arrive on site. A standard homeowners policy won’t cover construction-phase risks at all-it only activates after you move in. This gap between breaking ground and occupancy is exactly where financial disasters happen. Builders risk insurance fills this void by protecting the physical structure, construction materials, equipment, and tools from day one until the final inspection. Without it, a single hail storm or theft of copper wiring can cost thousands out of pocket.

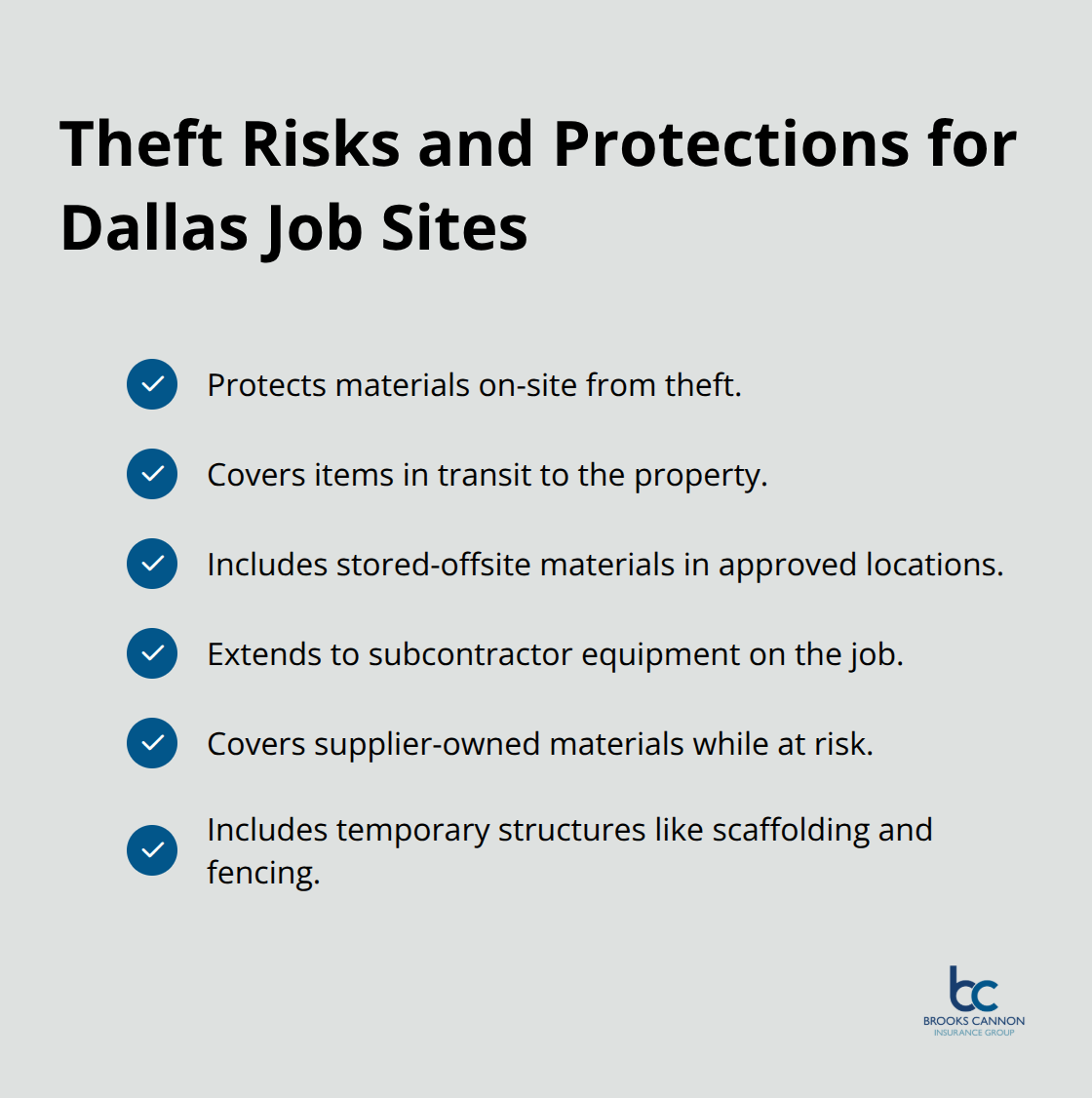

Materials and equipment face real theft risk

Construction site theft isn’t rare in Dallas-it’s predictable. Materials sit unattended, especially high-value items like copper piping, electrical components, and appliances, which attract opportunistic thieves. Builders risk coverage protects materials on-site, in transit to the property, and in storage, which means your investment stays protected throughout the entire supply chain.

The policy also covers subcontractor equipment and materials owned by suppliers, so you won’t face liability if someone else’s tools or goods get stolen. Many contractors assume their own insurance handles this, but it often doesn’t, leaving you exposed. Coverage typically extends to temporary structures like scaffolding and fencing (which are expensive to replace and frequently targeted).

Transition periods create dangerous coverage gaps

The space between when construction ends and you move in is a critical vulnerability. Your builders risk policy expires at completion, but your homeowners policy won’t activate until you occupy the home. During this gap-sometimes weeks-the finished structure sits unprotected against vandalism, weather damage, and theft of fixtures. Extended replacement cost coverage and careful policy timing can bridge this gap, but only if you plan for it in advance. Many builders in Dallas simply don’t address this transition, assuming nothing will happen in those final weeks. That assumption costs money when copper theft or storm damage occurs.

What happens next matters as much as what happens now

The decisions you make before construction starts determine whether you face financial exposure or complete protection. Builders risk policies require careful attention to coverage limits, material inventory, and timeline coordination with your homeowners insurance. Your next step involves understanding exactly what your builders risk policy covers and identifying any gaps that could leave your project vulnerable.

What Builders Risk Actually Covers

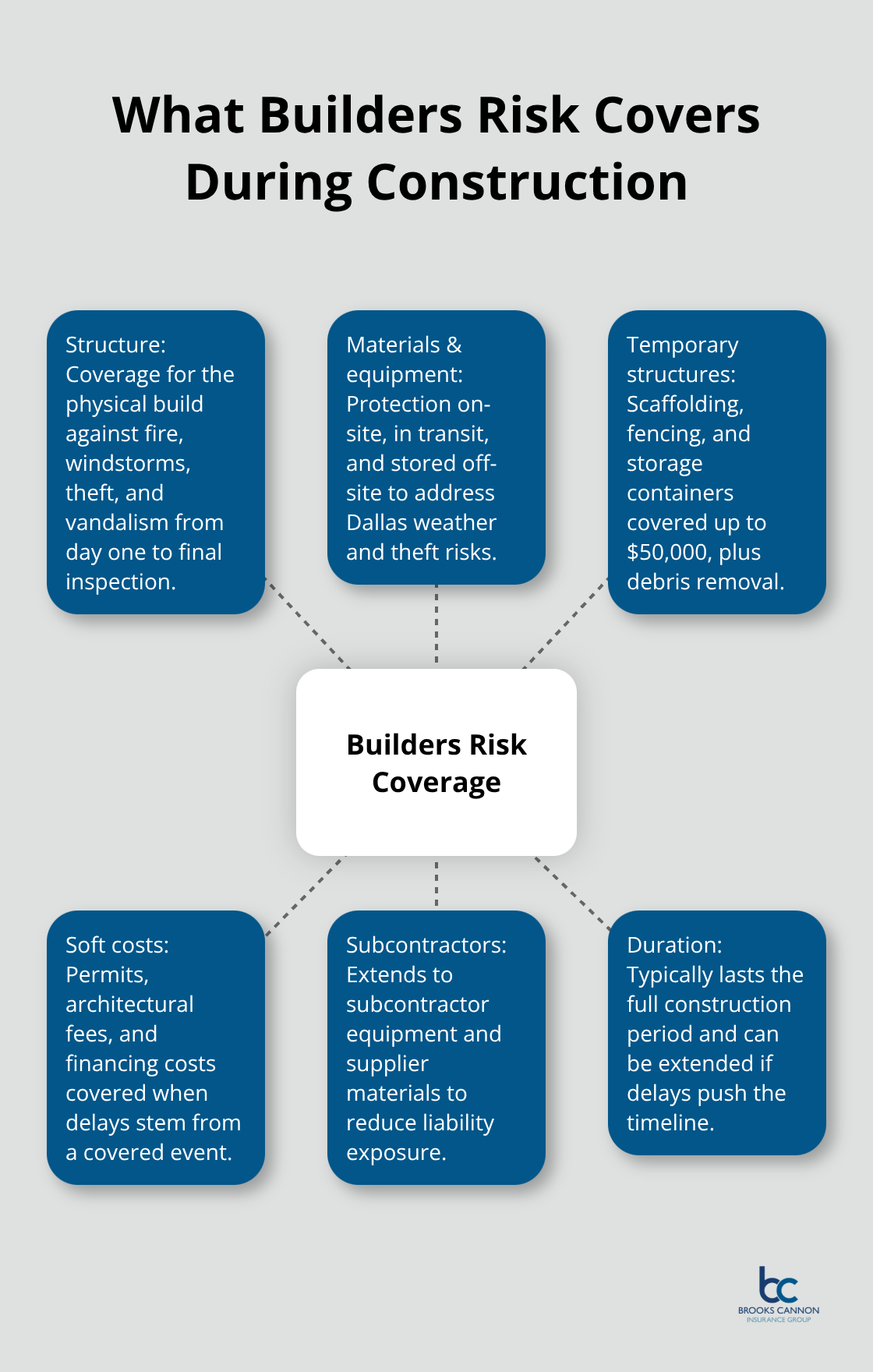

Builders risk insurance protects three distinct areas that standard homeowners policies completely ignore. The physical structure under construction receives coverage against fire, windstorms, theft, and vandalism from day one until final inspection. Materials and equipment on-site, in transit, or stored off-site gain protection, which matters enormously in Dallas where construction sites face weather exposure and theft risk. Temporary structures like scaffolding, fencing, and storage containers up to $50,000 in value are included, along with debris removal costs. Soft costs such as permits, architectural fees, and financing costs receive coverage if delays stem from a covered event, protecting your budget timeline.

The policy extends protection to subcontractor equipment and supplier materials, so you won’t face liability exposure for losses outside your direct control. Coverage typically lasts for the full construction duration and can be extended if unexpected delays push your timeline.

Liability Protection Shields You From Construction Accidents

Liability protection during construction covers bodily injury and property damage claims that arise from construction activities on your project. This protection stands separate from the structure itself and shields you if someone is injured on site or if construction work damages neighboring properties. Dallas construction sites operate in dense neighborhoods where property damage claims happen frequently, making this coverage essential. Your liability limits should match your project scope and local building density to avoid underinsurance.

Completed Work Coverage Prevents Phase Gaps

Completed work coverage ensures that finished portions of your home stay protected as construction progresses, preventing gaps between when one phase completes and the next begins. Weather can strike between phases in Dallas, and you need continuous protection during those vulnerable windows. After construction ends, transition coverage bridges the gap until your homeowners policy activates at occupancy. Many Dallas builders skip this transition planning and leave their completed home vulnerable for weeks.

Coordination With Your Homeowners Policy Matters

Your policy should specify exact end dates and coordinate with your homeowners policy start date to eliminate any unprotected period. Work with your agent to confirm that coverage limits match your actual project value, not an estimate, because underinsurance creates serious exposure if losses occur. This coordination step determines whether you face gaps or maintain seamless protection from groundbreaking through move-in day. Getting this timing right requires attention to detail and advance planning with your insurance provider.

Common Gaps in Construction Insurance

Inadequate Coverage Limits Leave You Exposed

Most Dallas builders dramatically underestimate what their projects actually cost to rebuild, then set coverage limits based on that flawed number. The median home value in Dallas sits around $339,000, but construction costs often exceed market value significantly, especially when accounting for labor, materials, and unforeseen expenses that arise during the build. If you insure a $400,000 project with only $300,000 in coverage limits, a major loss leaves you paying tens of thousands out of pocket.

Contractors quote a project value, builders accept it without verification, and then reality hits when materials cost more than anticipated or scope changes increase expenses. Your coverage limits must reflect actual rebuild costs, not estimates from six months ago. Get a detailed cost breakdown from your builder or contractor and verify it independently before finalizing your policy.

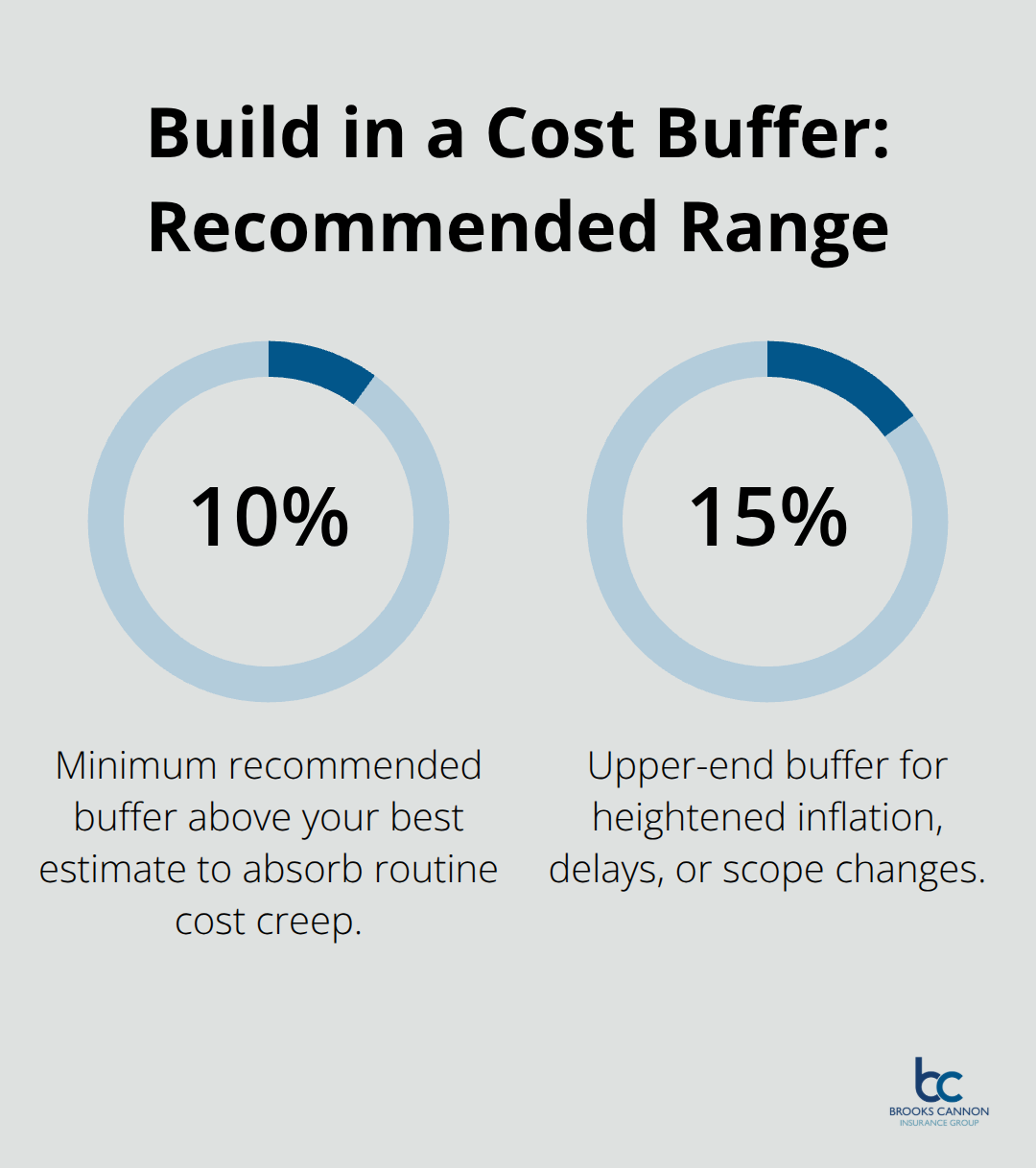

Many Dallas projects face price inflation mid-construction due to supply chain delays and labor shortages, which means your initial estimate becomes obsolete quickly. Set your coverage limits 10 to 15 percent higher than your best estimate to account for cost creep that inevitably occurs. Standard exclusions like flood, earthquake, and poor workmanship create additional gaps where claims get denied, so review your policy exclusions carefully.

Inadequate limits create a false sense of security-your policy appears active, but it won’t actually cover a major loss.

Transition Periods Leave Your Finished Home Unprotected

Transition gaps between builders risk expiration and homeowners policy activation represent a critical blind spot that Dallas builders routinely ignore. Your builders risk policy ends at final inspection or occupancy, but your homeowners policy may not activate until you physically move in, creating a window where the finished structure sits completely unprotected. During this gap (sometimes lasting weeks), vandalism, weather damage, copper theft, and fixture removal happen regularly in Dallas neighborhoods.

You need explicit coordination between your insurance agent and your lender to eliminate zero days without coverage. This timing coordination determines whether you face exposure or maintain seamless protection through move-in day. Many Dallas builders simply skip this transition planning and leave their completed home vulnerable for weeks.

Subcontractor Work Creates Hidden Liability Exposure

Subcontractor work creates exposure that many project owners fail to address adequately because they assume the contractor carries sufficient liability insurance. That assumption fails when a subcontractor’s insurance limits fall short or when their policy excludes the specific type of damage that occurs. If a subcontractor’s electrician causes a fire during rough-in work, or if a plumber’s equipment damages neighboring property, you face potential liability if the subcontractor’s coverage proves inadequate.

Require proof of insurance from every subcontractor before they start work, verify that their limits match your project scope, and confirm that your builders risk liability coverage extends to their activities. Dallas County’s high tornado frequency and hail risk mean that subcontractor equipment left on-site faces real exposure, and you need clarity on who bears the cost if that equipment gets damaged during a severe weather event. Equipment damage claims often exceed initial expectations, and unclear responsibility between you and the subcontractor creates disputes that delay claims and increase costs.

Final Thoughts

New build coverage protects your Dallas construction project from financial exposure that standard homeowners insurance completely ignores. Weather damage, material theft, liability claims, and transition gaps between construction phases create genuine financial exposure that catches builders off guard. Your builders risk policy addresses these specific construction-phase risks with coverage limits, liability protection, and coordination that homeowners policies simply cannot provide.

Professional guidance from someone who understands Dallas construction risks makes the difference between complete protection and expensive exposure. We at Brooks Cannon Insurance Group work with multiple top-rated insurance carriers to find the coverage and pricing that matches your specific project. Our licensed experts understand Dallas weather patterns, local building codes, material costs, and the transition timing that protects your investment from groundbreaking through move-in day.

Your next step involves contacting an insurance professional who can review your specific project details and confirm that your coverage limits match actual rebuild costs. Verify that your builders risk policy coordinates with your homeowners policy to eliminate transition gaps, and request proof of insurance from every subcontractor to confirm that their liability limits align with your project scope. Brooks Cannon Insurance Group can help you secure comprehensive new build coverage that protects what matters most during construction.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation