Getting a Dallas builders risk quote shouldn’t feel overwhelming. You’re protecting a significant investment, and the right policy makes all the difference between smooth construction and financial disaster.

We at Brooks Cannon Insurance Group help contractors and builders navigate this process every day. This guide walks you through comparing quotes and selecting coverage that actually fits your project.

What Builders Risk Actually Covers

The Foundation of Your Protection

Builders risk insurance protects the physical structure, materials, and equipment on your construction site from damage or loss during the building process. Unlike standard property or homeowners policies, which exclude buildings under construction, builders risk fills that gap entirely. Coverage applies from the moment materials arrive on site or construction begins, continuing until the project reaches completion and becomes occupiable. Texas law doesn’t require builders risk, but construction lenders almost always do-and for good reason.

Why Lenders Demand This Coverage

When you secure a construction loan, the lender becomes a named insured on the policy to protect their financial interest. Without builders risk in place, lenders halt funding until you obtain coverage. This requirement exists because uninsured losses can stall projects for weeks, creating cascading costs that threaten the entire investment.

What Your Policy Actually Protects

The policy covers the structure itself, permanent fixtures, machinery, underground piping, electrical systems, temporary structures like scaffolding, and materials in transit from suppliers to your job site. Standard coverage includes protection against fire, lightning, windstorm, hail, smoke, vandalism, theft, and vehicle or aircraft collisions. Debris removal after a covered loss is included, which matters significantly-cleanup costs on mid-sized projects routinely reach $50,000 or more. You can add optional endorsements to expand protection further, such as soft costs coverage that reimburses architectural fees, permits, and financing charges if a covered event delays your project.

Dallas Weather Elevates Your Risk

Dallas-area construction faces specific weather risks that elevate both exposure and premium costs. North Texas sits directly in Hail Alley, where large hail events damage roofing and exterior finishes regularly. A single hail event can destroy hundreds of thousands of dollars in materials and labor investments without adequate protection. Flood damage is excluded from standard policies, making flood endorsements essential for projects near flood zones or in areas with poor drainage-these endorsements typically cost $1,500 to $5,000 annually but can prevent catastrophic losses.

Additional Coverages That Matter

Equipment breakdown coverage protects HVAC systems, generators, and mechanical equipment against internal damage during installation, addressing a gap many contractors overlook. Inadequate coverage or underestimated protection limits leave you exposed to project delays, stolen materials, weather destruction, and out-of-pocket expenses that consume project profits entirely. Typical builders risk premiums run 1% to 3% of your total construction budget-a $1 million project costs roughly $10,000 to $30,000 annually-making this protection remarkably affordable relative to the financial risk you’re managing. Understanding what your policy covers sets the stage for comparing quotes effectively and identifying which endorsements your specific Dallas project actually needs.

What to Actually Compare in Your Quotes

Set Your Coverage Limit to Match Real Project Costs

Comparing builders risk quotes requires focus on three concrete factors that directly impact your project’s financial protection and your bottom line. First, examine coverage limits against your actual construction budget. Your coverage limit must match the total hard costs of materials, labor, equipment rentals, and subcontractor fees-underinsuring leaves dangerous gaps that you’ll pay out-of-pocket after a loss. Many contractors set limits based on what sounds reasonable rather than calculating actual project spend, then discover mid-project that a theft or weather event leaves them short thousands of dollars. Pull your detailed project budget and cost estimates, then request quotes with limits matching that figure exactly.

Choose Your Deductible Based on Cash Flow, Not Just Premium

Deductibles deserve equal attention because they directly affect both your premium and your cash-flow risk after a loss. A $500 deductible costs significantly more than a $5,000 deductible, but choosing the higher deductible means absorbing that $5,000 from your pocket if debris removal or theft occurs.

For most Dallas contractors managing projects between $500,000 and $2 million, a $2,500 deductible strikes the right balance-it costs roughly 10 to 15 percent more in premium than the $5,000 option but shields your cash reserves from common claim amounts.

Compare Premiums Across Multiple Carriers

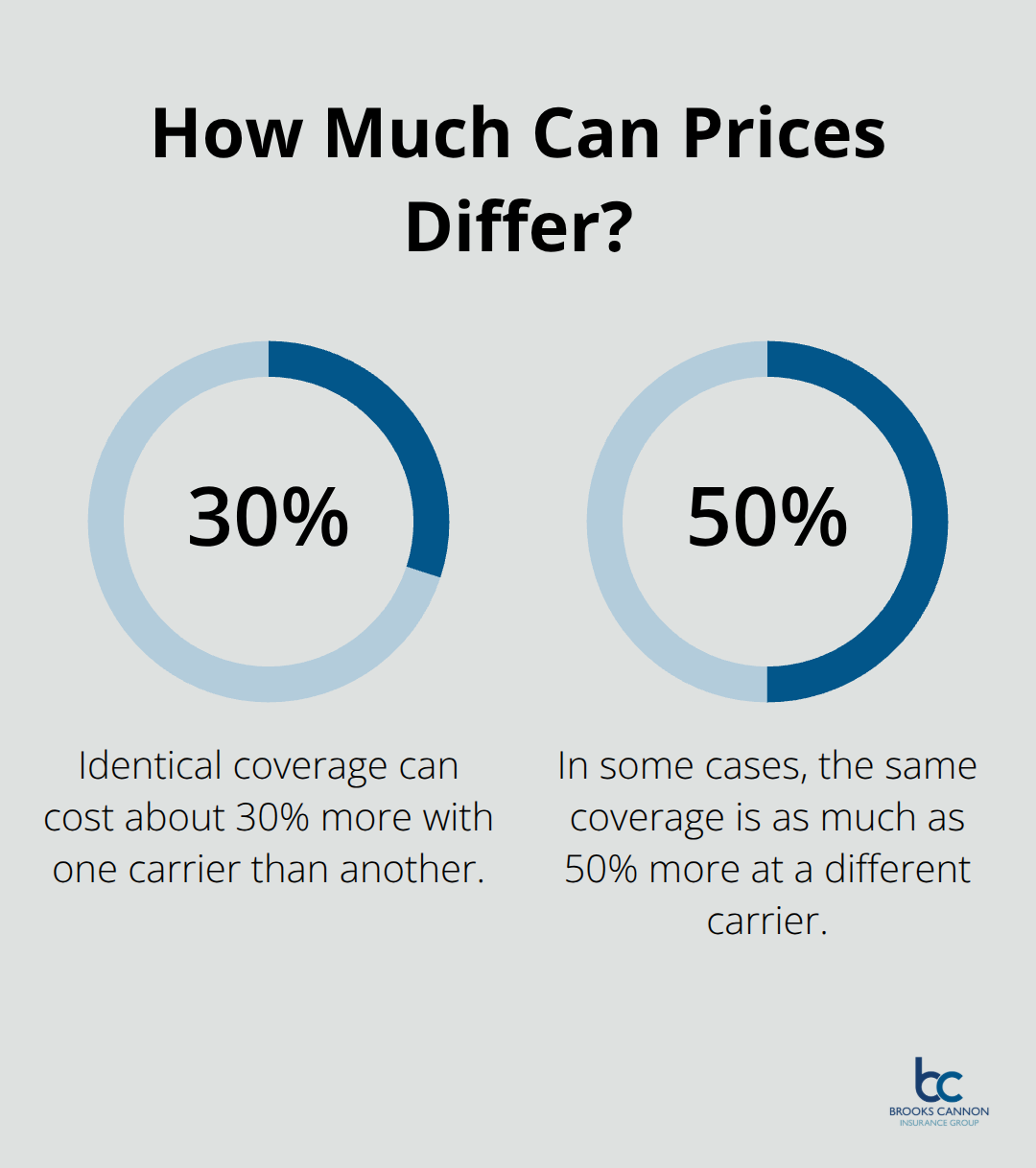

Premium variation across carriers surprises most contractors because identical coverage costs 30 to 50 percent more at one carrier than another. Request quotes from at least three carriers before deciding, because price alone means nothing without understanding what you actually receive. One quote might include debris removal and equipment breakdown while another excludes both, making the cheaper option worthless if either peril strikes your site.

Identify Which Endorsements Your Project Actually Needs

Endorsements become critical when comparing quotes. Soft costs coverage reimburses architectural fees, permits, and financing charges if a covered loss delays your project, and on a $3 million job, even a 30-day delay costs $30,000 to $50,000 in additional financing charges alone. Flood endorsements typically cost $1,500 to $5,000 annually but become mandatory for Dallas projects near flood zones or areas with drainage issues-skipping this coverage on a flood-prone site is financial recklessness. Wind and hail coverage with lower deductibles specifically protects against North Texas weather exposure, and equipment breakdown coverage addresses HVAC and generator damage during installation.

Create a Comparison Spreadsheet to Reveal True Value

When comparing quotes, create a simple spreadsheet listing each carrier’s base premium, deductible, coverage limit, and which endorsements are included or available. Verify each quote includes the same limits and deductibles to ensure apples-to-apples comparison and reveals which carrier actually provides the best value for your specific Dallas project rather than simply choosing the lowest number. Once you’ve narrowed your options based on coverage and cost, the next step involves evaluating which carrier will actually stand behind your claim when you need them most.

Selecting the Right Policy for Your Dallas Project

Your spreadsheet now shows which carriers offer the best price and coverage structure, but price alone won’t protect your project when a hail storm or theft occurs. The next critical step involves assessing whether each carrier will actually pay your claim when you need them most.

Financial Strength and Claims Reputation Matter Most

Financial strength ratings from AM Best, Moody’s, and S&P reveal which insurers can handle large payouts without delay or dispute. Carriers rated A+ or higher by AM Best demonstrate the financial stability to cover major losses, while lower-rated carriers create unnecessary risk that savings in premium won’t justify. Check each carrier’s claims handling reputation through the Better Business Bureau and customer reviews on independent sites like Trustpilot, where Dallas contractors share real experiences about claim approval speed and dispute resolution.

A carrier offering a $500 lower premium means nothing if they delay your claim for weeks while your project stalls or deny coverage based on technical exclusions you didn’t anticipate. Look specifically for carriers with strong performance in construction claims, since residential and commercial builders risk claims differ significantly from standard property claims in complexity and documentation requirements.

Verify Dallas-Specific Weather Claims Experience

Your Dallas project faces weather exposures that contractors in other regions don’t encounter, which means generic coverage recommendations fail your situation. If your project sits within the 50-mile coastal zone vulnerable to hurricanes or near identified flood zones, carriers with strong track records handling weather claims in North Texas matter far more than carriers with national reputation.

Request references from each carrier for recent Dallas construction projects they’ve insured, then contact those contractors directly about claim experience and turnaround time. Ask specifically whether the carrier paid for equipment breakdown claims during installation and how quickly they responded to hail damage assessments. A carrier’s willingness to provide contractor references signals confidence in their service, while refusal to do so suggests they lack recent positive Dallas project experience.

Confirm Coverage Details Match Your Project Needs

Verify that soft costs coverage includes the specific expenses your project requires, since some carriers limit reimbursement to certain fee categories while others provide broader protection. Equipment breakdown coverage specifics matter equally-confirm whether the policy covers your HVAC units, generators, and mechanical systems during installation or only after completion. These details separate adequate protection from policies that leave you exposed when claims occur.

Calculate True Cost, Not Just Premium

Value means cost divided by actual protection for your specific project, not the lowest premium number. A quote $3,000 cheaper annually that excludes flood coverage becomes worthless if flooding occurs near your Dallas site, transforming the apparent savings into a catastrophic loss. Calculate the true cost of each option by adding the premium to the deductible you’d pay after a typical claim, then compare that total against the coverage limits and endorsements included.

The carrier offering the best combination of competitive premium, strong financial ratings, positive Dallas claims experience, and comprehensive endorsements matching your project risks deserves your selection, even if another carrier quotes slightly lower. As an independent agency, Brooks Cannon Insurance Group works with multiple top-rated carriers to identify which combination best protects each client’s unique Dallas project rather than steering clients toward whichever carrier pays the highest commission.

Final Thoughts

Comparing Dallas builders risk quotes requires three concrete actions before construction starts. Match your coverage limits to actual project costs, select a deductible that protects your cash flow, and request quotes from multiple carriers to reveal true price variation. Your spreadsheet comparing premiums, limits, deductibles, and endorsements transforms complexity into straightforward decision-making that protects your investment.

Contact an independent agent at least two weeks before materials arrive on site, since coverage gaps between project start and policy activation leave you completely exposed. Request quotes with your exact coverage limits, preferred deductible, and all endorsements your Dallas project requires based on location and weather exposure. Verify each quote includes debris removal, confirm soft costs coverage reimburses your specific expenses, and confirm equipment breakdown protection covers your HVAC and generator installation.

We at Brooks Cannon Insurance Group compare quotes from numerous carriers to identify which combination delivers the best protection and pricing for your specific Dallas builders risk quote. Our team verifies coverage details match your needs and confirms financial strength ratings before presenting options, so you receive expert guidance from professionals who understand Dallas construction risks and lender requirements. Contact Brooks Cannon Insurance Group to start comparing quotes today and secure the coverage your project requires.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation