Construction projects in Texas face unique risks that standard insurance policies simply don’t address. Whether you’re building a residential home or a commercial structure, Texas builders risk coverage protects your investment from theft, weather damage, and on-site accidents.

At Brooks Cannon Insurance Group, we help builders across Dallas and beyond understand how national standards shape their coverage needs. This guide walks you through what builders risk insurance covers, how it differs from other policies, and how to select the right protection for your project.

What Builders Risk Actually Protects on Your Texas Site

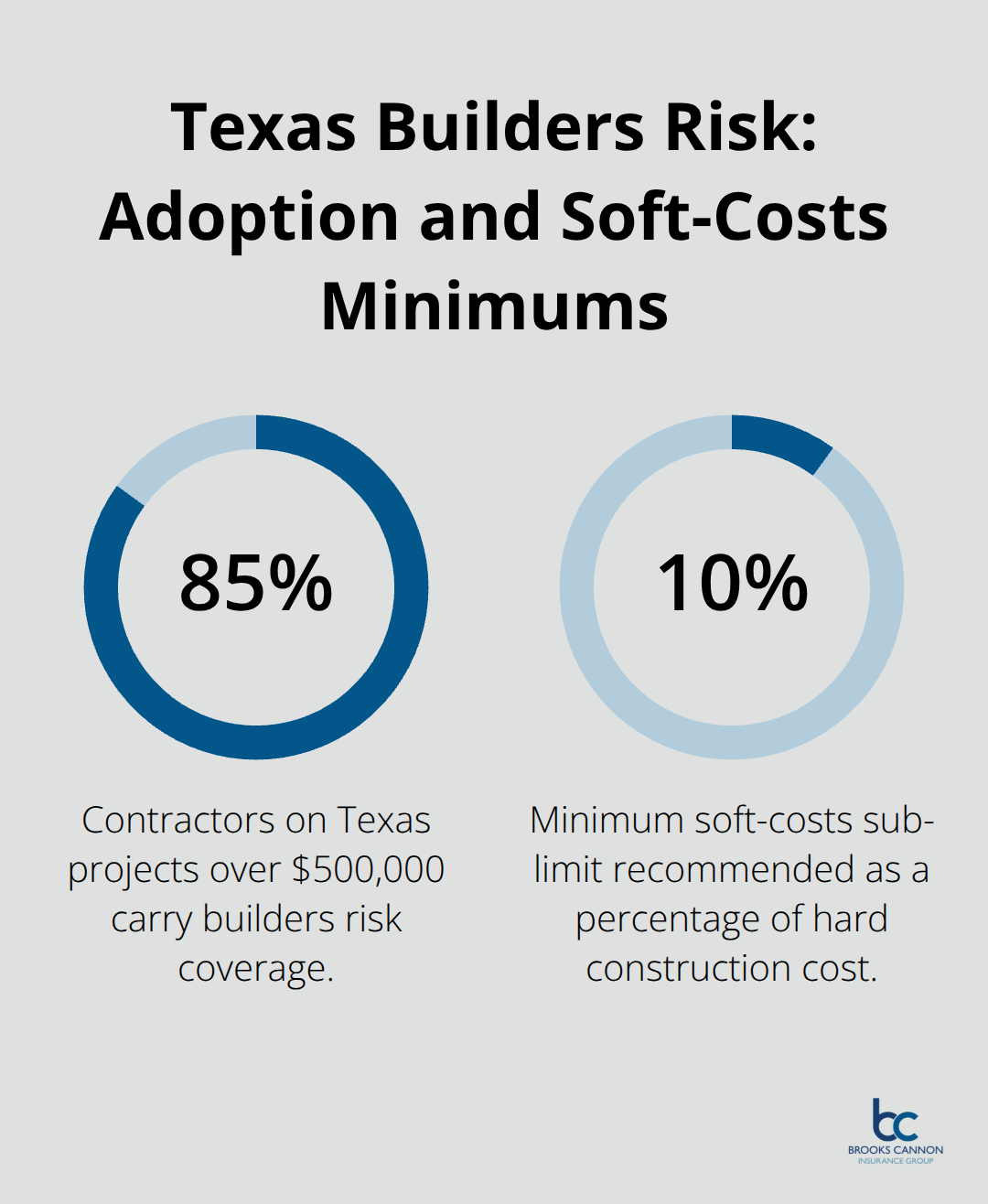

Builders risk insurance covers direct physical loss to the structure under construction, materials staged on site, fixtures ready for installation, and temporary structures like scaffolding and forms. In Texas, the Associated General Contractors of America reports that 85% of contractors on projects over $500,000 carry this coverage, underscoring how standard it has become for financing and risk management. The policy activates when materials arrive on site or construction begins and terminates when the project reaches occupancy readiness or receives a certificate of occupancy. Coverage extends beyond the building itself-materials in transit to the job and stored off-site are included, which matters because Texas experiences significant construction theft.

North Texas sits in Hail Alley, and tornadoes struck Texas regularly, and a single 2023 Texas storm caused over $500 million in construction-related damages. Your policy protects against fire, wind, theft, and vandalism during these events. However, standard builders risk excludes worker injuries (that requires workers’ compensation), employee theft, faulty workmanship, normal wear and tear, earthquake, flood, and penalties unrelated to covered losses. Soft costs-extended loan interest, design fees, permit expenses-are usually optional add-ons that require a separate sub-limit, yet a six-month project delay can generate $50,000 to $250,000 in soft costs depending on project size. This gap catches many Texas builders off guard.

Who Actually Needs This Coverage

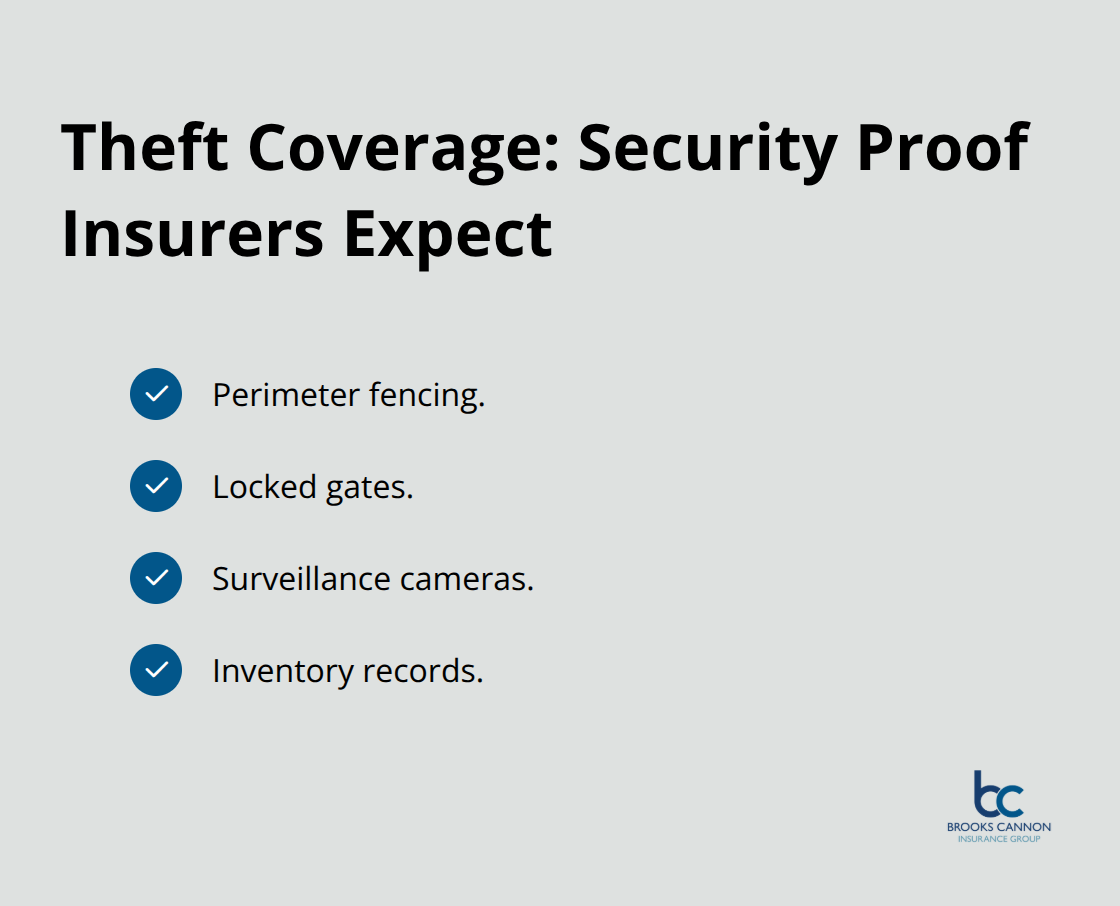

Your lender almost certainly requires it. If you finance construction, the lender won’t release funds without proof of builders risk in place. Contractors typically purchase the policy, though some owners buy it to protect their investment directly, and subcontractors are usually added as additional insureds. If you are a homeowner undertaking a major renovation, you need it because standard homeowners policies exclude buildings under construction. If you are a commercial developer, a general contractor, or a subcontractor managing materials on site, this coverage is non-negotiable. Texas law does not mandate builders risk, but lenders, bonding companies, and project contracts do. The contract often specifies who pays-usually the contractor passes the cost through in the bid. Typical policies run three months for small renovations, six months for residential construction, and twelve months for larger commercial projects. Costs range from 1% to 3% of total construction budget, translating to roughly $1,000 to $5,000 per $100,000 in construction spending. Your specific premium depends on project size, building type, location within Texas, project duration, on-site security measures, and your claims history. Theft coverage requires documented security (perimeter fencing, locked gates or containers, lighting, cameras, and inventory records) to trigger claims payouts.

How Builders Risk Differs From General Liability

Builders risk covers physical damage to the project itself. General liability covers third-party bodily injury and property damage-if someone is injured on your site or their vehicle is damaged, general liability responds. Both are typically required on the same project because they protect different exposures. Mixing them up costs money. A contractor who relies only on general liability to cover theft of materials on site will face a claim denial. One who skips general liability thinking builders risk covers injuries to visitors will face catastrophic exposure. Texas contractors often believe their general liability policy covers construction damage, then face denial when fire destroys a partially framed building. They are separate tools for separate jobs, and understanding this distinction protects your project from costly gaps in protection.

What Texas Builders Must Know About Statewide and National Insurance Standards

OSHA Compliance and Premium Impact

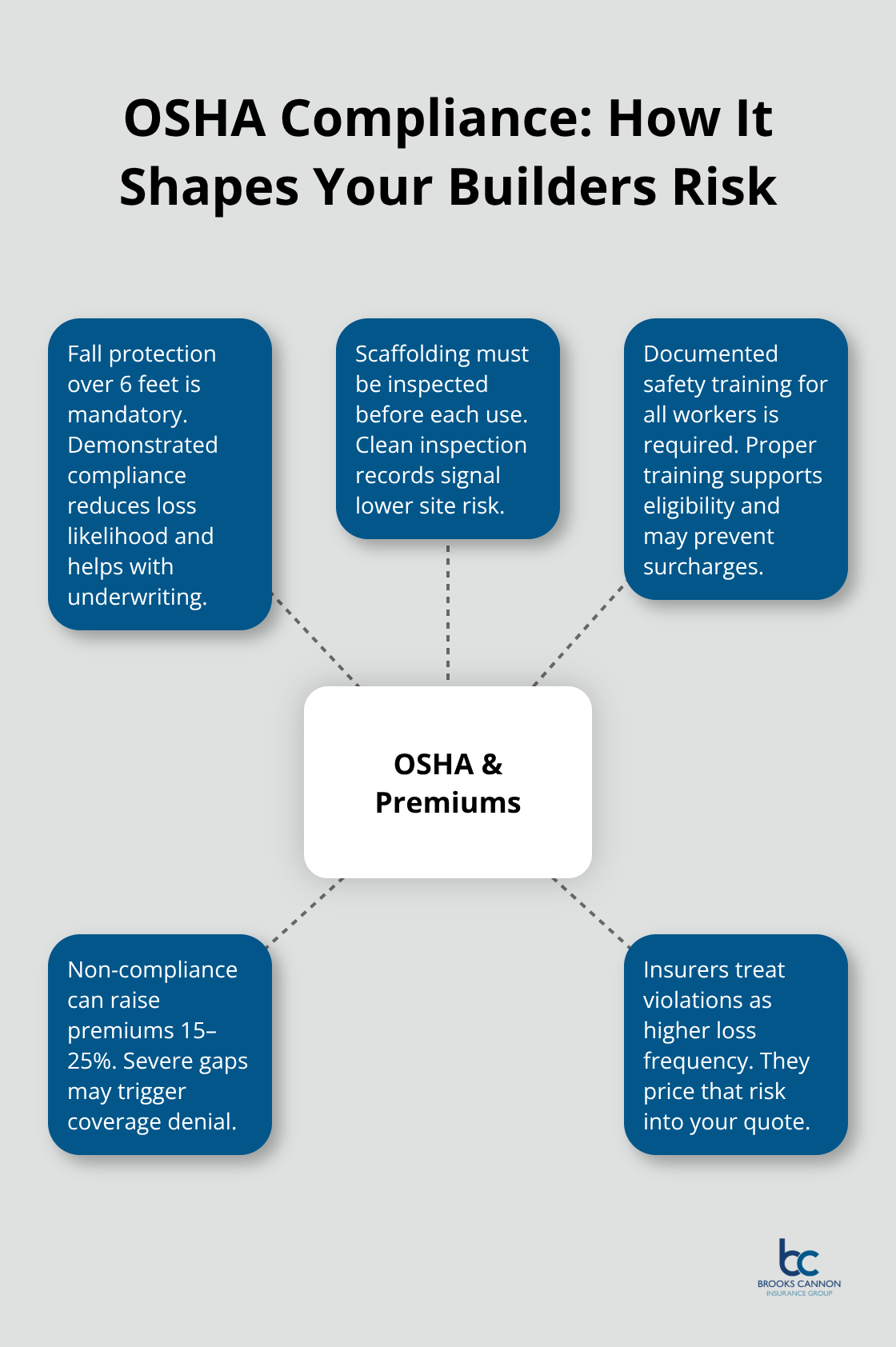

OSHA regulations mandate fall protection at heights over 6 feet, scaffolding inspections before each use, and documented safety training for all workers on site. These requirements directly affect your builders risk policy because insurers factor in your safety compliance when calculating premiums and determining coverage eligibility. A project without documented OSHA compliance can face premium increases of 15–25% or outright coverage denial. Insurers view safety violations as indicators of higher loss frequency, so they price that risk accordingly.

Your compliance record becomes part of your underwriting profile, and carriers review it before binding coverage.

Texas Building Code Requirements and Coverage Implications

Texas Building Code, adopted from the International Building Code, establishes construction standards that vary by project type and location within the state. Commercial projects in Dallas must meet specific wind-load requirements due to North Texas severe weather exposure, which translates into higher insurance costs and stricter underwriting scrutiny. Residential projects typically face lower compliance costs but still require municipal inspections at framing, electrical, and final stages. Your builders risk policy covers the cost of rebuilding to code if damage occurs, but only if the original construction meets current code standards. Non-compliant work creates coverage gaps that surface during claims.

State-by-State Insurance Variations

Texas insurance requirements differ significantly from other states, which matters if your company operates across state lines. While Texas does not mandate builders risk by law, your lender will require it before releasing construction funds, and bonding companies will demand proof of coverage before issuing payment bonds. Other states like California and New York impose stricter mandatory coverage thresholds and higher minimum limits. If you operate in multiple states, coordinate your national coverage strategy with an independent agent who understands state-by-state variations rather than assuming one policy template works everywhere.

Carrier Financial Ratings and Texas Department of Insurance Compliance

The Texas Department of Insurance publishes carrier financial ratings and complaint ratios that directly influence which insurers can write builders risk in the state. Carriers rated below A– by AM Best face restrictions or exclusion from Texas markets entirely. When comparing quotes, verify that your carrier maintains an A– rating or better and has filed all required forms with the Texas Department of Insurance. This protects you from coverage disputes if your carrier faces financial difficulty mid-project. An independent agent can verify these ratings quickly and present only carriers with solid financial footing. Your next step involves assessing your specific project risks and understanding how these statewide standards translate into the coverage limits and endorsements your Texas construction site actually needs.

Selecting the Right Builders Risk Policy for Your Texas Project

Calculate Your Total Project Cost and Soft Costs Exposure

Start with your total project cost, not just the hard construction budget. Hard costs-labor, materials, equipment-form your base, but soft costs account for 20–30% of the total project value. If your construction budget is $1 million, soft costs could add $200,000 to $300,000. These include extended loan interest during delays, permit and design fees, and insurance premiums that accumulate if the project stalls. Most Texas builders underestimate soft costs, then face coverage gaps when a weather delay pushes the timeline. Request a soft costs sub-limit equal to at least 10% of your hard construction cost. For a $500,000 project, that means a $50,000 soft costs limit minimum.

Protect Materials On-Site and In Transit

Examine your materials exposure carefully. Copper wiring, HVAC units, appliances, and lumber disappear from Texas job sites regularly. If your project stores materials off-site or transports them in open trucks, request off-site storage coverage and in-transit protection with documented security requirements. The policy will demand proof: perimeter fencing, locked gates, surveillance cameras, and inventory records. Carriers like Nationwide, rated Best Builders Risk for General Contractors in 2026, offer streamlined underwriting for projects that meet these security standards.

Add Price Escalation and Weather Endorsements

Price escalation endorsements protect you when material and labor costs spike during construction. Since 2020, Texas has seen volatile pricing, and a six-month delay can trigger 10–15% cost increases. Activate price escalation endorsements at 5–10% inflation thresholds to keep your coverage limits aligned with actual rebuilding costs. For North Texas projects specifically, wind and hail coverage with lower deductibles is not optional-it is essential. Hail Alley storms have caused billion-dollar losses, and standard deductibles of $10,000 or higher leave significant gaps. Request wind and hail endorsements with deductibles between $2,500 and $5,000 to match the actual exposure.

Compare Declarations Pages and Exclusions Across Carriers

Comparing quotes requires more than price alone. Request declarations pages from at least three carriers and verify that sub-limits match across policies before comparing premiums. A $2 million builders risk policy with a $25,000 soft costs sub-limit is not equivalent to another $2 million policy with a $100,000 soft costs sub-limit, even if the base premium is lower. The second policy costs more upfront but protects you far better. Check the exclusions section carefully-post-Uri freeze exclusions, hot work exclusions, and faulty workmanship carve-outs vary by carrier. Some carriers exclude freeze damage entirely between November and March, while others offer endorsements to restore coverage for a modest additional premium. If your project runs through winter months, that exclusion matters.

Accelerate Approval With Complete Project Documentation

Turnaround time matters on construction schedules. Most brokers deliver quotes within 24 hours, but same-day binding is possible if you provide project details upfront. When requesting a quote, include your project description, construction hard cost budget, schedule, site plan, contract documents, and details of any existing property on site. If you can provide geotechnical or soils reports, carriers underwrite faster and may offer better terms. An independent agent can help you gather these documents and coordinate with underwriters to accelerate approval, so coverage activates before materials arrive on site rather than weeks into construction.

Final Thoughts

Texas builders risk coverage protects your construction investment from the moment materials arrive on site until occupancy is achieved. A single weather event, theft, or project delay can cost tens of thousands of dollars without proper protection, and national standards combined with state-specific requirements shape what coverage you actually need. Verify your limits match your total project cost including soft costs, add endorsements for your specific risks, and confirm your carrier maintains solid financial ratings with the Texas Department of Insurance.

Request declarations pages from multiple carriers and compare sub-limits and exclusions side by side before making your decision. Provide complete project documentation to accelerate underwriting, and same-day binding becomes achievable when you work with an independent agent who understands Texas construction risks. Price escalation endorsements, wind and hail coverage with appropriate deductibles, and off-site storage protection address the exposures that catch most Texas builders off guard.

We at Brooks Cannon Insurance Group work with multiple top-rated insurance carriers to find the best coverage and pricing for your construction project. Our team of licensed experts reviews your project details, identifies coverage gaps, and presents options that protect your investment without unnecessary cost. Contact us today to discuss your project specifics and receive a competitive quote tailored to your actual exposure.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation