Owning rental property in Dallas comes with real financial exposure. Tenant injuries, property damage, and income loss can drain your profits fast if you’re not properly protected.

A Dallas rental property policy is built specifically for landlords-it covers what homeowners insurance won’t. We at Brooks Cannon Insurance Group help property owners across the Dallas area understand exactly what coverage they need and why it matters.

What Rental Property Coverage Actually Covers

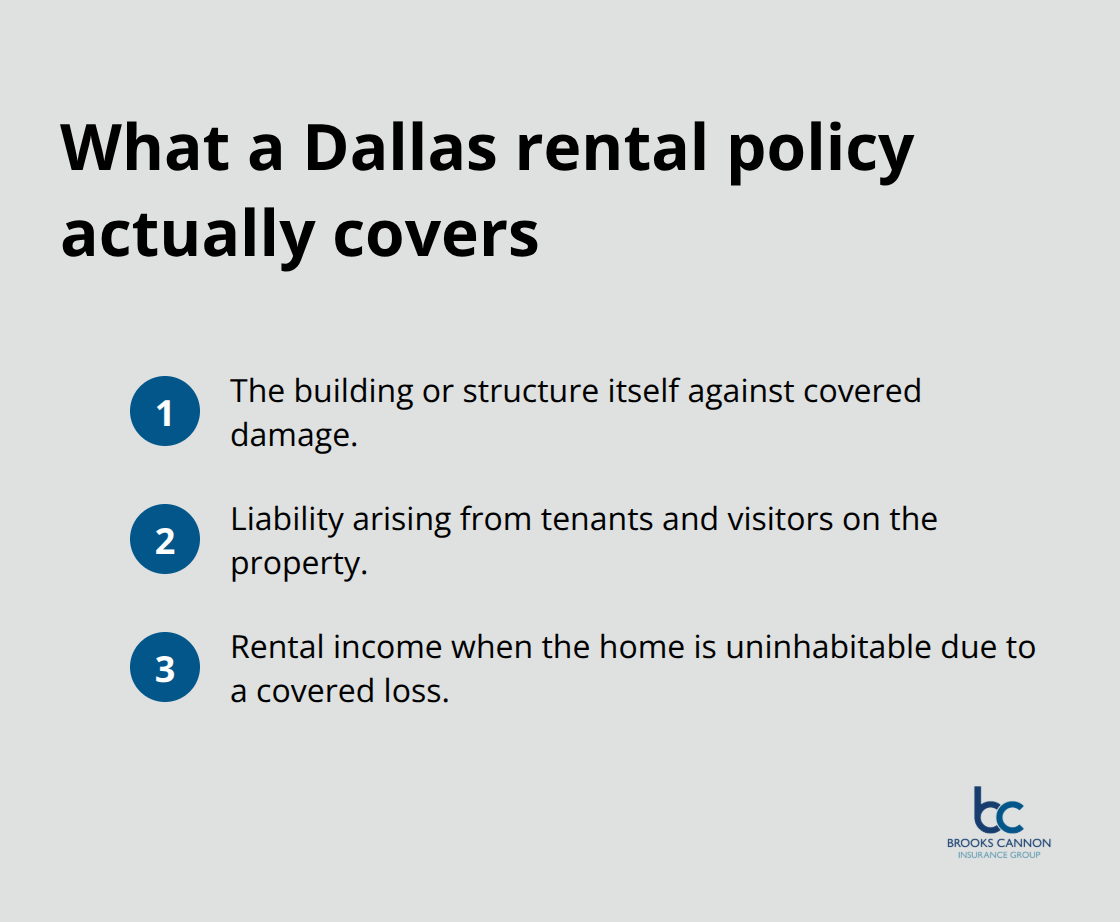

A Dallas rental property policy protects three specific areas that standard homeowners insurance completely ignores: the building structure itself, liability exposure from tenants and visitors, and your rental income when the property sits empty or becomes uninhabitable. This isn’t optional coverage for landlords in Dallas-it’s the foundation of your financial protection. The policy typically uses what’s called a Dwelling Fire (DP) form, either DP2 or DP3, depending on your property’s age and value.

DP2 offers broad named-peril coverage with replacement-cost payout, while DP3 covers all perils unless specifically excluded, which makes sense for newer or higher-value Dallas properties. The average annual cost for landlord insurance in Dallas runs around $1,555 or higher, but this protects you against the real risks that can devastate your cash flow.

The Building and What It Actually Covers

Your dwelling coverage reimburses the cost to rebuild or repair your property after damage from fire, wind, hail, vandalism, or other covered events. This is replacement-cost coverage, not actual cash value, which matters enormously in Dallas where rebuild costs have climbed significantly. Many landlords make a critical mistake here: they base their coverage limits on what they paid for the property years ago, not what it would cost to rebuild today. If you purchased a Dallas rental home for $250,000 five years ago but today’s rebuild cost is $320,000, your old limit leaves you $70,000 short. Update your dwelling limit every two to three years using your carrier’s replacement-cost calculator or a professional valuation. Storm damage in North Texas is particularly common-the Gulf Coast region has recorded hundreds of billions in weather-disaster losses since 1980-so your coverage limit must reflect actual current rebuild expenses.

Liability Coverage Protects Your Assets

Liability coverage pays medical bills, legal defense costs, and settlements when a tenant or visitor is injured on your rental property and you’re found responsible. A single serious injury claim can exceed $500,000 in medical and legal costs, which is why standard liability limits of $100,000 to $300,000 often fall short for Dallas landlords. Try starting at $300,000 minimum, with $500,000 to $1,000,000 preferred if you own multiple properties or have features that increase risk (like pools or decks). Medical payments coverage within your liability protection pays minor injuries up to roughly $1,000–$5,000, which helps prevent small-claim lawsuits before they escalate.

Loss-of-Rent Coverage Protects Your Income

Loss-of-rent coverage reimburses your monthly rental income when a covered event-fire, severe weather, or vandalism-forces tenants to vacate or makes the property uninhabitable during repairs. If you collect $2,000 monthly rent, you should plan for six to twelve months of potential income loss, not just a few months. This coverage typically costs about $200–$400 per year but protects your cash flow when you need it most. Texas state law doesn’t mandate landlord insurance, but your mortgage lender almost certainly does if you financed the property. Lenders protect their investment by requiring proof of coverage and typically specify minimum liability limits and covered perils you must maintain throughout the loan term.

Why Standard Homeowners Policies Fall Short

Standard homeowners insurance explicitly excludes rental activity, leaving you exposed if you try to use that policy for a rental property. The coverage gaps are substantial: homeowners policies don’t cover loss of rent, don’t protect against tenant-related liability claims, and don’t account for the different occupancy risks that rental properties present. A Dwelling Fire policy (DP2 or DP3) fills these gaps and addresses the specific exposures landlords face in Dallas. As an independent agency, we at Brooks Cannon Insurance Group work with multiple top-rated carriers to find the right DP form and coverage limits for your property type and risk profile. The next section covers the mistakes landlords make most often-and how to avoid them.

What Coverage Limits Actually Protect Your Dallas Rental

Dwelling Coverage Must Match Today’s Rebuild Costs

Your dwelling limit forms the foundation of your rental property protection, and it must reflect what your property costs to rebuild today, not what you paid for it years ago. Dallas rebuild costs have climbed substantially over the past five years, driven by labor shortages and material inflation. If your policy limit sits at $250,000 but today’s replacement cost runs $340,000, you’re gambling with $90,000 of your own money after a total loss.

Pull your declarations page right now and compare your dwelling limit to a current replacement-cost estimate. Most carriers provide free online calculators, or you can request a professional valuation from a local appraiser for roughly $300–$500. This single step catches the coverage gap that destroys landlords’ finances.

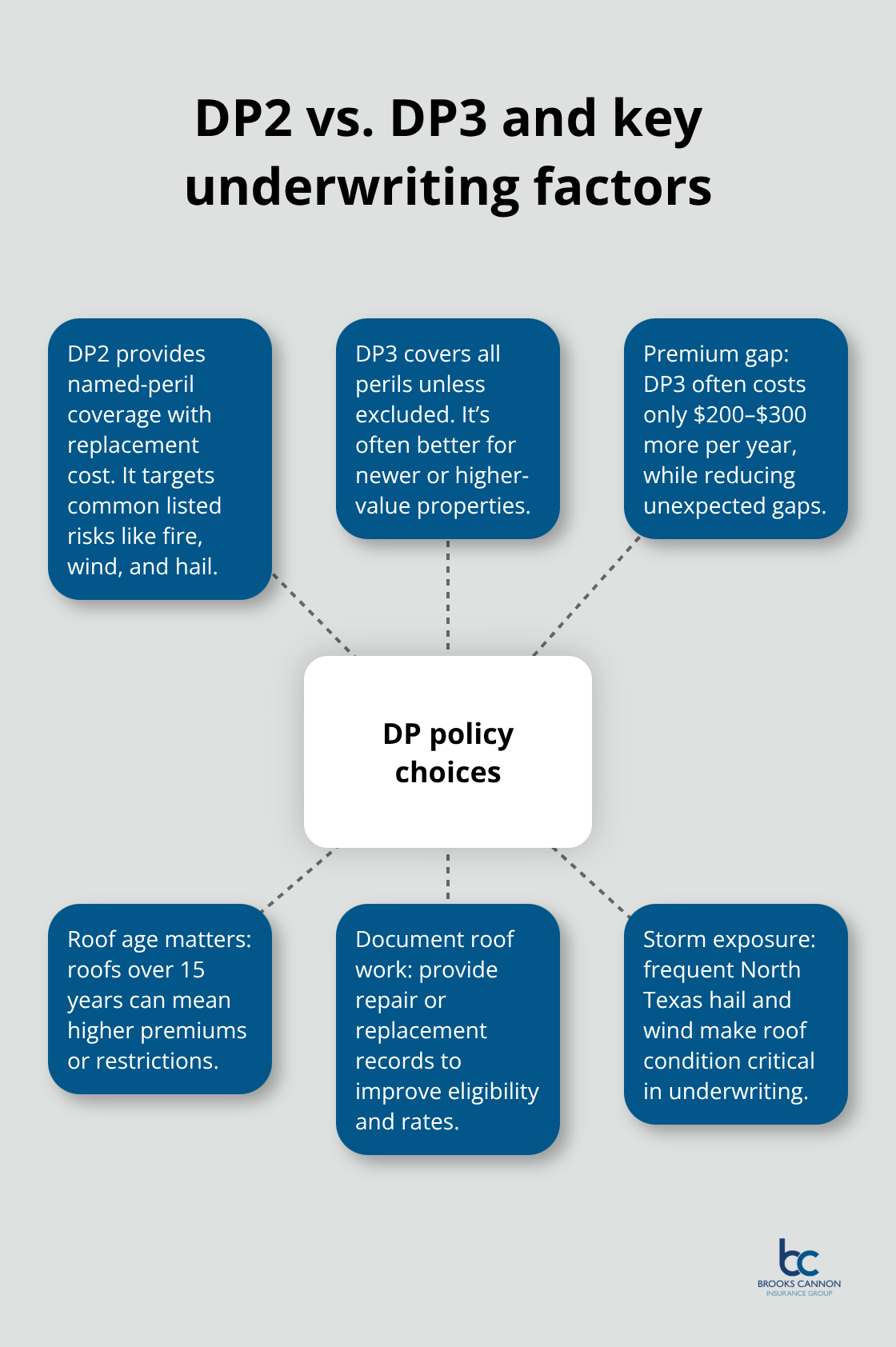

DP2 vs. DP3: Which Form Protects You Better

DP2 policies offer replacement-cost coverage on named perils like fire, wind, and hail, while DP3 extends that to all perils unless specifically excluded. For newer Dallas properties or those worth over $400,000, DP3 makes financial sense because the premium difference rarely exceeds $200–$300 annually, yet it eliminates gaps from unexpected damage types.

North Texas hail storms and wind events hit rental properties regularly, so your roof condition matters enormously. Insurers scrutinize roof age, material, and past damage when underwriting DP policies. If your roof is over 15 years old, expect higher premiums or coverage restrictions. Document any roof repairs or replacements and provide those records when quoting with new carriers, as this directly impacts your rates and eligibility.

Liability Coverage Protects Your Personal Assets

Liability coverage for rental properties in Dallas must start at a minimum of $300,000 per occurrence, but $500,000 to $1,000,000 is far smarter if you own multiple units or your property has liability magnets like pools, trampolines, or multi-unit layouts. Medical and legal costs from tenant or visitor injuries routinely exceed $400,000 in Texas courts.

One slip-and-fall case with a broken hip and subsequent infection can generate $600,000 in hospital bills alone, plus legal defense costs if the tenant sues. Your liability coverage pays those bills and your legal defense, protecting your personal assets from judgment. Medical payments coverage, embedded within your liability protection, covers small injuries up to $5,000 regardless of fault, which prevents minor incidents from escalating into lawsuits.

Loss-of-Rent Coverage Protects Your Monthly Income

Loss-of-rent coverage reimburses your actual monthly rent when a covered event forces tenants out or makes the property uninhabitable during repairs. If you collect $2,500 monthly rent, a fire that requires three months of reconstruction means $7,500 in lost income. Most Dallas landlords should carry 6 to 12 months of rent coverage.

Calculate this straightforwardly: multiply your monthly rent by six or twelve, then verify your loss-of-rent limit meets that number. This coverage typically costs $200–$400 annually and protects your cash flow when property damage creates temporary vacancy. Without this protection, you still owe your mortgage while collecting zero rent-a financial squeeze that forces many landlords into crisis mode.

The right coverage limits depend on your specific property, its current replacement value, and your liability exposure. Your next step is to review your current policy declarations against these standards and identify any gaps before they become expensive problems.

Mistakes That Cost Dallas Landlords Thousands

The gap between what landlords think they’re covered for and what their policy actually pays sits at the heart of most rental property insurance disasters. Three mistakes dominate this landscape, and each one drains money from your pocket or leaves you exposed when damage strikes.

Underinsuring Your Property’s Replacement Value

The first mistake happens when landlords lock in a coverage limit based on their original purchase price and never update it. Dallas property values and rebuild costs have climbed faster than rent increases over the past five years, meaning a home you bought for $280,000 in 2019 might cost $370,000 to rebuild today due to labor shortages and material inflation. If your dwelling limit still sits at $280,000, you’re personally liable for that $90,000 gap after a total loss.

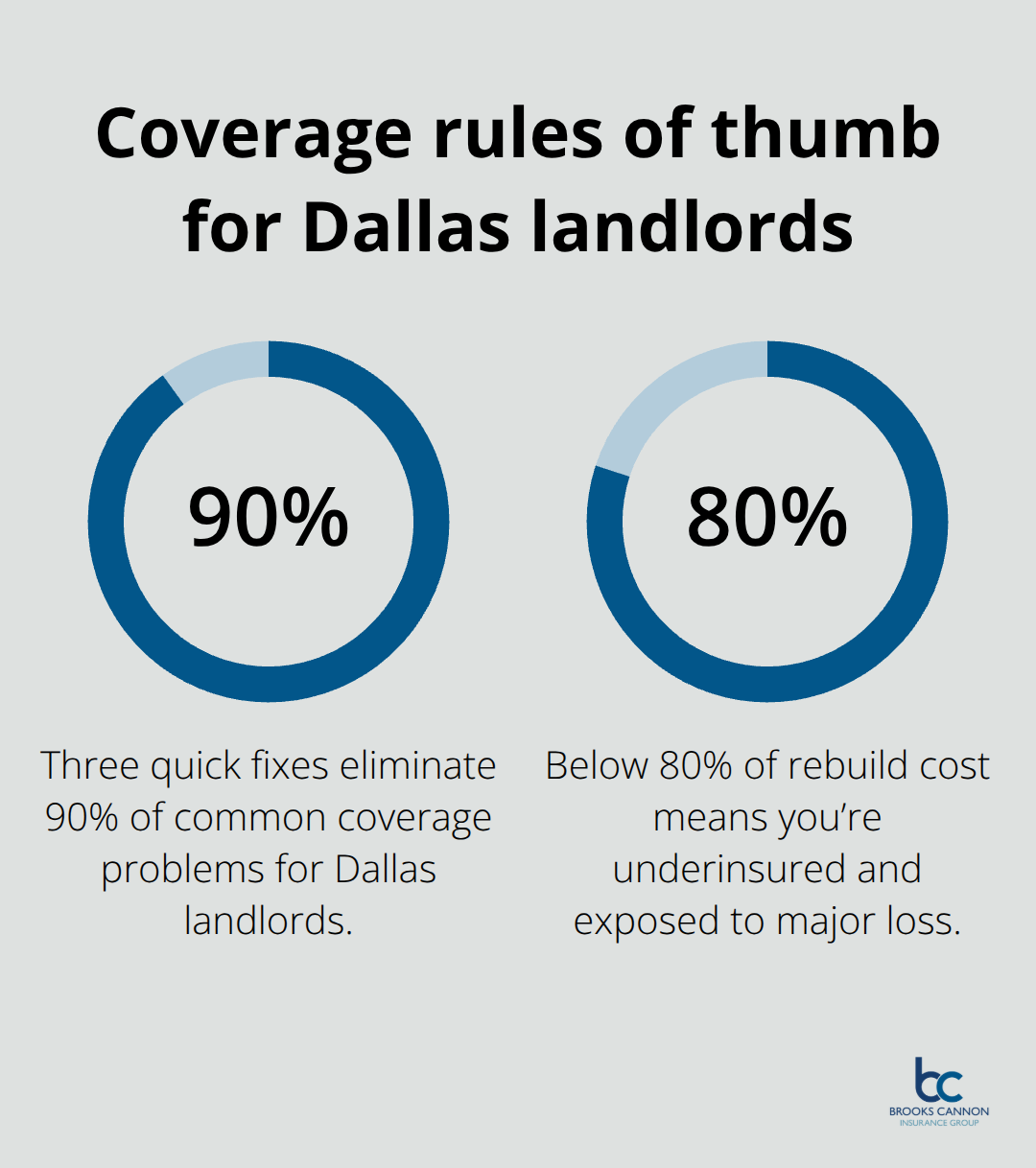

This isn’t theoretical-it’s the single biggest financial mistake Dallas landlords make, and it’s entirely preventable. Pull your declarations page and get a current replacement-cost estimate from your carrier’s online calculator or a professional appraiser. If your limit falls below 80 percent of the rebuild cost, you’re underinsured and exposed to catastrophic loss.

Confusing Homeowners Policies with Rental Coverage

The second mistake occurs when landlords treat a standard homeowners policy as adequate coverage for a rental property. Standard homeowners policies explicitly exclude rental activity, which means they won’t pay loss-of-rent claims, won’t cover tenant liability exposure, and won’t address the occupancy risks unique to rentals. A Dallas landlord who tries to insure a rental property on a homeowners policy discovers this gap only after filing a claim, at which point the denial letter arrives and the damage comes out of pocket.

You need a Dwelling Fire policy, either DP2 or DP3, specifically designed for rental properties. This form covers what homeowners policies won’t and protects your income stream when tenants must vacate due to covered damage.

Carrying Inadequate Liability Coverage

The third mistake involves carrying inadequate liability coverage or failing to understand what additional insured requirements your lease or mortgage lender actually imposes. Many Dallas landlords carry $100,000 in liability coverage because it’s cheap, without realizing that a single serious injury claim easily exceeds $500,000 in medical and legal costs. Your mortgage lender likely requires you to name them as additional insured on your policy, which your current agent may not have done correctly.

Verify this on your declarations page-check that your lender appears under the additional insured section. If it doesn’t, contact your agent immediately because lender non-compliance can trigger loan violations and leave your lender unprotected (which they won’t tolerate). Try starting with a minimum of $300,000 in liability coverage, with $500,000 or higher preferred for multiple properties or high-risk features like pools.

How to Fix These Three Gaps Today

The solution is straightforward: review your policy declarations today against the standards outlined in the previous section. Confirm your dwelling limit matches current rebuild costs, verify your liability limit sits at minimum $300,000 with $500,000 or higher preferred, and confirm your lender is named additional insured. These three actions eliminate 90 percent of the coverage problems Dallas landlords face.

As an independent agency, we at Brooks Cannon Insurance Group work with multiple top-rated carriers to help landlords identify and close these exact gaps before they become expensive problems.

Final Thoughts

Your Dallas rental property policy protects your investment only when it reflects your actual property value and liability exposure, not outdated limits from years past. Pull your current declarations and compare your dwelling limit to a current replacement-cost estimate today. If your limit falls short or your liability coverage sits below $300,000, contact Brooks Cannon Insurance Group for a no-obligation review.

We at Brooks Cannon Insurance Group understand the specific risks Dallas landlords face, from hail and wind damage to tenant-related liability claims and income loss during repairs. Our licensed experts review your property details, your current coverage, and your financial exposure to recommend the right Dwelling Fire form, liability limits, and loss-of-rent protection for your situation. We work with multiple top-rated insurance carriers to find coverage that actually protects your investment and your cash flow.

Start by reaching out to our team and let us help you close the coverage gaps before they become expensive problems. We’ll identify gaps in your coverage, explain what each protection actually covers, and provide quotes from carriers that specialize in rental property insurance. Your next step is simple: contact us today.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation