Owning rental properties in Dallas comes with real financial exposure. Standard homeowners insurance won’t protect your rental income or liability risks, leaving you vulnerable to costly gaps in coverage.

We at Brooks Cannon Insurance Group work with landlords every day to build Dallas rental property coverage that actually matches their needs. The right policy can be the difference between a manageable setback and a financial crisis.

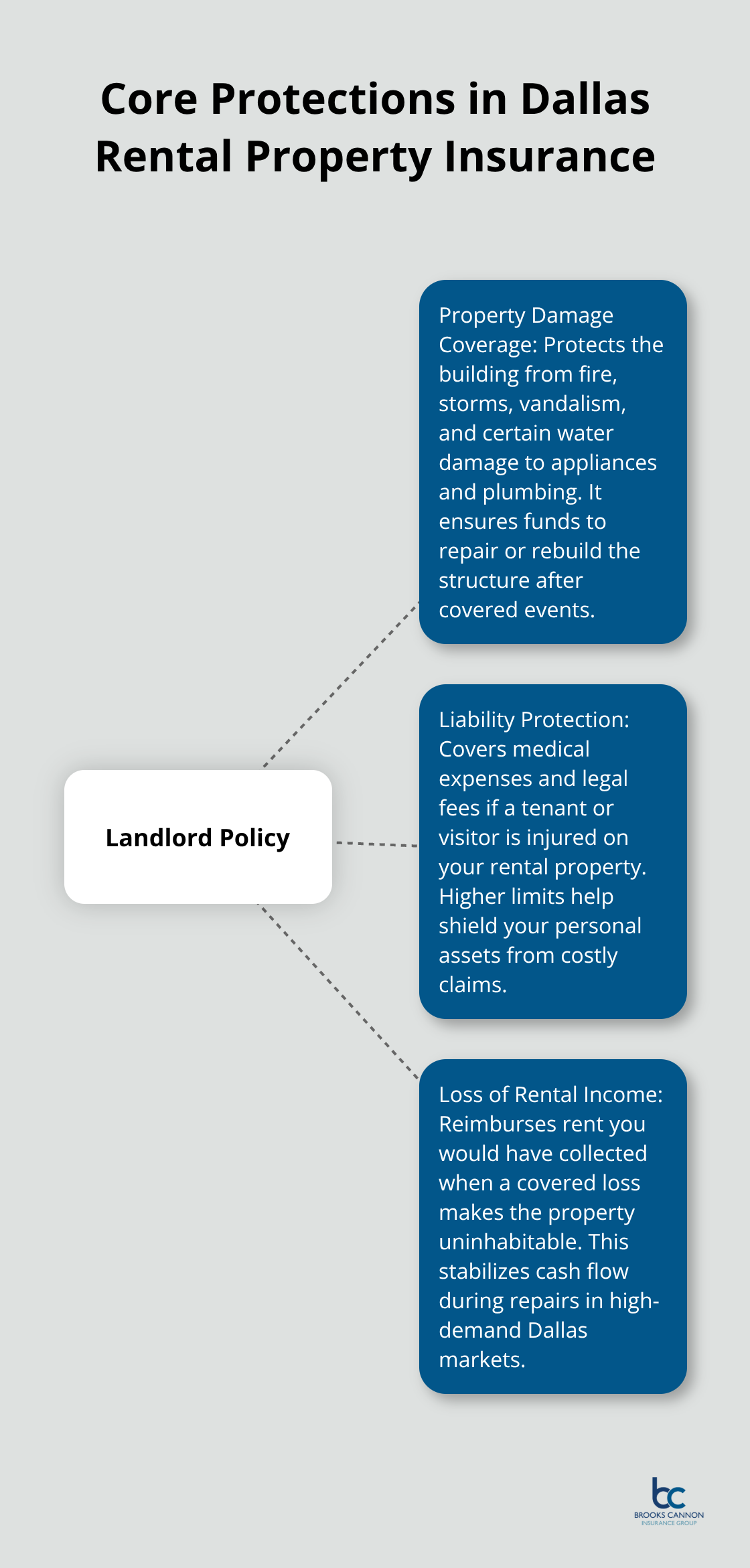

What Landlords Need to Know About Rental Property Insurance

Rental property insurance in Dallas covers three specific areas that standard homeowners policies completely ignore: the physical structure, liability from tenant and visitor injuries, and lost rental income when the property becomes uninhabitable. Property damage coverage protects the building itself from fire, storms, vandalism, and certain water damage to appliances and plumbing, while liability protection covers medical expenses and legal fees if someone is injured on your rental property.

Loss of rental income coverage reimburses you for rent you would have collected during repairs, which matters enormously in Dallas where rental demand remains strong. Standard homeowners policies exclude rental activities entirely and will deny claims for tenant-caused damage, making a dedicated landlord policy non-negotiable if you want actual protection.

Why Your Current Homeowners Policy Won’t Work

Your homeowners policy was designed for owner-occupied homes, not investment properties that generate income. Insurance companies treat rental properties as fundamentally different risks because tenants occupy the space, which creates higher liability exposure and potential income loss that homeowners policies simply do not address. If you rent out a property while maintaining homeowners coverage, your insurer can cancel the policy or deny claims when damage occurs, leaving you completely exposed. Rental properties generate substantially more liability claims than owner-occupied homes, which is exactly why insurers refuse to cover them under standard policies. Dallas landlords who discover this gap after a tenant injury or property damage event face devastating financial consequences that could have been prevented with proper coverage.

Underinsurance and Roof Vulnerabilities in North Texas

Most landlords think they’re protected until something actually happens. Older rental properties in Dallas face particular scrutiny during underwriting because electrical, plumbing, and HVAC systems deteriorate over time, and insurers will either exclude coverage for these systems or charge significantly higher premiums if the property hasn’t been maintained. Roof condition matters tremendously in North Texas because hail and wind damage occur regularly, so insurers examine roof age and material carefully, potentially imposing wind and hail deductibles depending on the property’s vulnerability. Many landlords also fail to calculate adequate replacement cost coverage, which should equal the full reconstruction cost of the building rather than its market value, and underinsurance is common when landlords base coverage on purchase price rather than actual rebuild expense.

Tenant Turnover and Coverage Disruptions

Tenant turnover creates another gap because coverage terms can shift between leases, and vacancy periods may affect your policy’s validity or increase your deductible. Each transition between tenants introduces a window where your protection weakens, and insurers scrutinize occupancy status closely during underwriting. Properties that sit vacant for extended periods often face coverage restrictions or premium increases, so you need to communicate lease changes to your agent immediately. This attention to occupancy details separates landlords who maintain continuous protection from those who discover gaps only after a loss occurs.

Understanding these coverage gaps positions you to make informed decisions about the protection your Dallas rental property actually needs. The next section examines the specific coverage types that address these vulnerabilities and protect both your investment and your income stream.

Protection for Your Investment and Income

Liability Coverage Protects You From Tenant and Visitor Injuries

Liability coverage for rental properties in Texas should start at a minimum of $500,000, and frankly, that’s the bare minimum for Dallas landlords. The Insurance Information Institute reports that rental properties generate substantially more liability claims than owner-occupied homes, which means a single tenant injury or visitor accident can create significant financial exposure. A tenant who slips on your property and requires surgery, or a visitor who suffers a fall and pursues legal action, can generate medical bills, legal defense costs, and settlement amounts that quickly exceed $100,000. Standard homeowners policies cap liability at $300,000 or less, leaving you dangerously underprotected. Landlord policies allow you to set liability limits that match your actual risk, and many Dallas landlords carry $1 million in liability coverage to protect themselves from catastrophic injury claims that could force them to sell their property.

Loss of Rental Income Coverage Replaces Your Cash Flow

Loss of rental income coverage reimburses you for rent during the repair period after a covered loss makes the property uninhabitable. If a fire damages your rental property and repairs take six months, a property renting for $1,500 monthly represents $9,000 in lost income that standard homeowners policies never address. Most landlord policies offer coverage for up to 12 months of lost rent, which protects you if reconstruction takes longer than expected or if you need time to find a new tenant after repairs complete. Dallas rental demand remains strong, but strong demand doesn’t help if you cannot collect rent while your property sits damaged and under repair.

Actual Cash Value Versus Replacement Cost: The Critical Difference

The choice between actual cash value and replacement cost coverage directly affects how much you’ll recover after a loss, and this decision determines whether you can actually rebuild your property or face a financial shortfall. Actual cash value depreciates the building over time, so a 15-year-old rental property with $200,000 in replacement cost might only recover $140,000 under actual cash value coverage because the insurer reduces the payout by depreciation. Replacement cost coverage pays what it actually costs to rebuild the property to its current condition, which in Dallas averages around $120 per square foot for standard construction. A 1,500-square-foot rental property therefore requires approximately $180,000 in dwelling coverage to avoid underinsurance, and that figure needs to increase annually to account for inflation in construction costs.

Texas Department of Insurance data shows that premiums vary significantly by ZIP code and property characteristics, but replacement cost coverage typically costs only 10 to 15 percent more in annual premiums than actual cash value coverage, making it the obvious choice for landlords who want to actually rebuild after a loss rather than absorb a depreciation penalty. Inflation protection that increases your coverage limits by approximately 20 percent annually prevents you from slipping into underinsurance as Dallas construction costs climb, and this protection becomes increasingly valuable over the years you own the property.

Why Underinsurance Leaves You Vulnerable

The difference between these two approaches becomes painfully real after a claim occurs. Landlords who chose the cheaper actual cash value option often discover they cannot afford to complete repairs and must accept a depreciated settlement that leaves their property damaged and unrentable. Your next step involves understanding how to actively reduce your insurance costs and protect your claims through smart tenant screening and maintenance practices that insurers reward with lower premiums.

Managing Risk as a Dallas Landlord

Tenant Screening Reduces Claims and Premiums

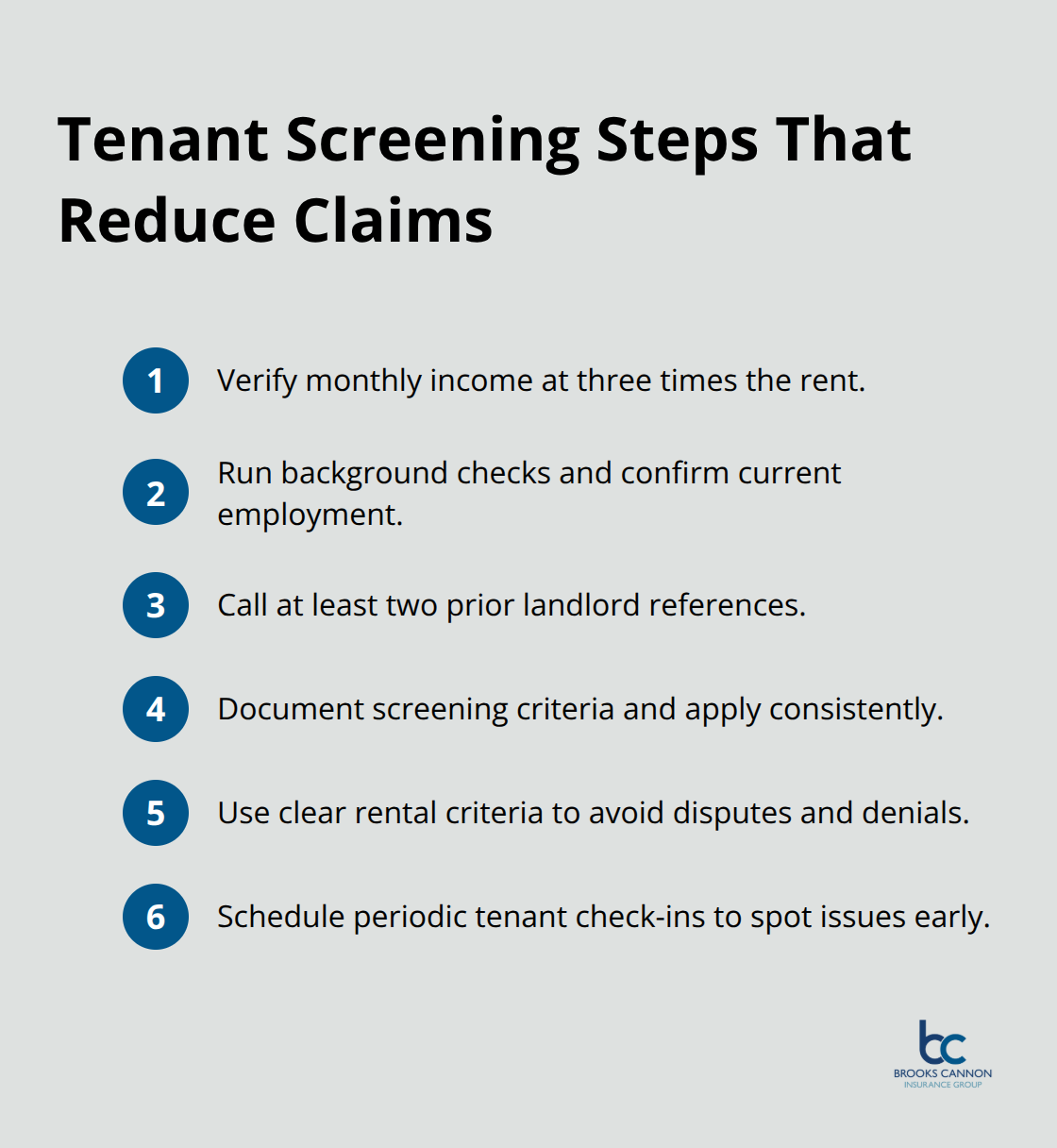

Tenant screening directly affects your insurance premiums and claim frequency, yet most Dallas landlords treat it as an afterthought. Insurers scrutinize your tenant selection process during underwriting because they know that properties with careful screening experience fewer liability claims and less property damage. Run background checks that verify income at three times the monthly rent, check at least two previous landlord references, and confirm employment with current employers.

A tenant earning $4,500 monthly for a $1,500 rent obligation demonstrates financial stability that reduces default risk and signals someone with resources to maintain the property responsibly.

The Insurance Information Institute reports that rental properties generate substantially more liability claims than owner-occupied homes. Dallas landlords who skip thorough screening inevitably face higher premiums, larger deductibles, or coverage restrictions because insurers view inadequate tenant vetting as a predictable path to claims.

Maintenance Practices Lower Your Insurance Costs

Property maintenance practices directly influence your insurance costs in measurable ways. A roof inspection completed within the last three years can reduce your premium by approximately 10 percent because insurers gain confidence that hail and wind damage vulnerabilities have been identified. Electrical, plumbing, and HVAC systems that have been updated within the last decade lower your rates significantly compared to properties with aging infrastructure that creates both damage and liability exposure.

Proximity to a fire station within 1,000 feet yields approximately a 10 percent discount on dwelling coverage, so knowing your property’s distance to emergency services matters when shopping for quotes. Security systems and burglar alarms can reduce premiums by up to 20 percent, making a $300 to $500 investment in alarm monitoring cost-effective when annual savings reach $200 or more.

Documentation Transforms Claims Into Straightforward Payouts

Documentation transforms your claims from disputes into straightforward payouts. Maintain detailed photos of your property taken before tenants move in, showing the condition of walls, flooring, appliances, and fixtures alongside date stamps that establish baseline conditions. When you file a claim after tenant-caused damage, these photos prove what existed before the incident and prevent insurers from denying portions of your claim based on pre-existing conditions.

Keep maintenance records that document roof repairs, HVAC servicing, plumbing work, and electrical updates, organized chronologically so you can quickly demonstrate that your property receives proper care. Lease agreements should specify tenant responsibilities for maintenance and explicitly state that tenants carry renters insurance to cover their personal belongings, which prevents confusion about coverage boundaries after a loss. Store these documents digitally in cloud storage and maintain physical copies in a fireproof safe, ensuring you can access proof of maintenance and property condition even if your rental property itself suffers fire damage.

Insurance companies reward landlords who document their diligence through lower premiums and faster claim resolution because documentation eliminates guesswork about property condition and maintenance history.

Final Thoughts

Dallas rental property coverage protects your investment through three essential components: dwelling protection for your building structure, liability limits that shield you from tenant and visitor injury claims, and loss of rental income coverage that replaces your cash flow during repairs. Most landlords underestimate their liability exposure and default to minimum limits that leave them vulnerable to catastrophic claims exceeding $500,000, which is why we recommend liability limits of at least $1 million for Dallas properties. Replacement cost coverage allows you to actually rebuild after a loss rather than absorb depreciation penalties that make reconstruction financially impossible.

Your next step requires gathering your property details and requesting quotes from multiple independent agencies that access 15 to 20 different carriers. Comparing quotes from three agencies using identical coverage terms takes approximately 15 minutes and can save you $400 or more annually while revealing coverage options you might otherwise miss. Document your property’s condition with photos, maintain records of all maintenance and repairs, and communicate any lease changes to your insurance agent immediately so your coverage stays aligned with your actual occupancy status.

We at Brooks Cannon Insurance Group work with Dallas landlords every day to build Dallas rental property coverage that matches your specific property risks and financial situation. As an independent agency, we access multiple top-rated carriers to find the best coverage and pricing for your rental properties rather than limiting you to a single company’s options. Contact us to discuss your coverage needs and receive a personalized quote that protects both your investment and your income stream.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation