Construction projects face unique risks that standard insurance policies don’t cover. Materials can be stolen, weather can cause damage, and accidents happen during building phases.

We at Brooks Cannon Insurance Group see contractors and property owners in Dallas struggle without proper builders risk insurance protection. This specialized coverage fills the gaps that general liability and property policies leave behind.

What Is Builders Risk Insurance

Builders risk insurance protects construction projects from the moment materials arrive on-site until the building reaches completion. This specialized coverage addresses the unique vulnerabilities that construction projects face, from material theft to weather damage. The Texas construction industry generated $200 billion in 2023, which makes this protection absolutely necessary for contractors and property owners in Dallas.

Coverage During Active Construction

The policy activates when materials hit your construction site and continues through project completion. Materials, fixtures, equipment, and the structure itself receive protection against theft, vandalism, fire, windstorm, and debris removal. The construction industry has shown steady growth, with the Associated General Contractors reporting positive job additions in recent months. The coverage extends to soft costs like architect fees and permits when construction delays occur from covered events. Projects valued up to $75 million qualify for residential and commercial builders risk policies.

Key Differences From Standard Insurance

General liability insurance covers bodily injury and property damage to third parties, while builders risk insurance protects your actual construction project and materials. Your standard property insurance won’t cover structures under construction, which leaves massive gaps in protection. Workers compensation handles employee injuries, but builders risk insurance focuses solely on physical damage to the project itself. The Insurance Information Institute reported that Texas faced $10 billion in claims in 2023, highlighting why contractors need this specialized coverage rather than relying on inadequate general policies.

Cost Structure and Investment Protection

Builders risk insurance costs typically range from 1% to 4% of total construction value, which makes it affordable protection for substantial financial exposure. A $1 million construction project could incur builders risk insurance costs of $10,000 to $30,000 annually. The average starting cost for builders risk insurance policies is approximately $375 in most states. These costs pale in comparison to potential losses – a 2011 storm caused $30 billion in damage from uninsured projects alone.

Understanding who needs this protection becomes the next critical consideration for construction stakeholders.

Who Needs Builders Risk Insurance

Lenders and Financial Requirements

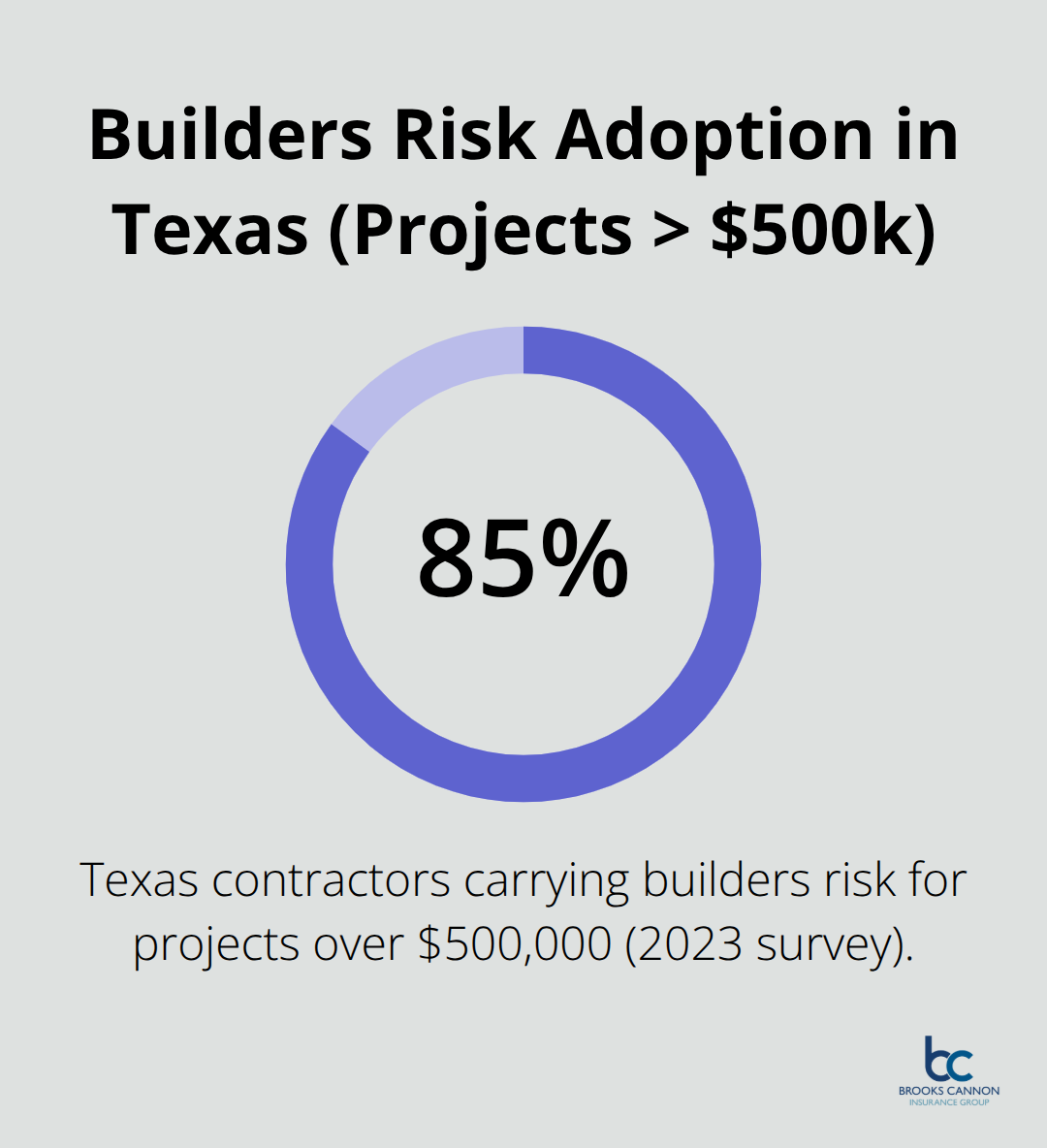

Construction financing requirements make builders risk insurance mandatory for most projects exceeding $500,000. Financial institutions demand this protection to secure their loan investments, which means general contractors face zero negotiation room on coverage decisions. A 2023 survey by the Associated General Contractors of America showed 85% of Texas contractors carry this insurance for projects over $500,000. Lenders require proof of coverage before they release construction funds, making this protection a prerequisite rather than an option for contractors who seek project financing.

Property Owners and Developers

Property owners who undertake major renovations or new construction face substantial financial exposure without builders risk coverage. Standard homeowners policies contain significant gaps during construction phases, leaving owners vulnerable to theft, vandalism, and weather damage. Construction sites face various risks throughout the building process, and homeowners who rely solely on their standard policies during construction may face unexpected risks and associated costs that could devastate their project budgets.

General Contractors and Subcontractors

Subcontractors who work on large projects typically need their own coverage or must be named insureds on the general contractor’s policy. Trade contractors who install specialized systems like HVAC, electrical, or plumbing equipment face particular risks during installation phases (especially when expensive materials sit exposed on-site). Construction projects in Texas face weather-related challenges throughout the year, which makes coverage essential for maintaining project timelines and budgets when covered events occur.

The specific risks these stakeholders face require comprehensive protection that standard policies simply cannot provide. For business insurance needs beyond standard coverage, specialty insurance products offer tailored solutions for unique construction risks.

What Does Builders Risk Insurance Actually Cover

Theft and Vandalism Protection

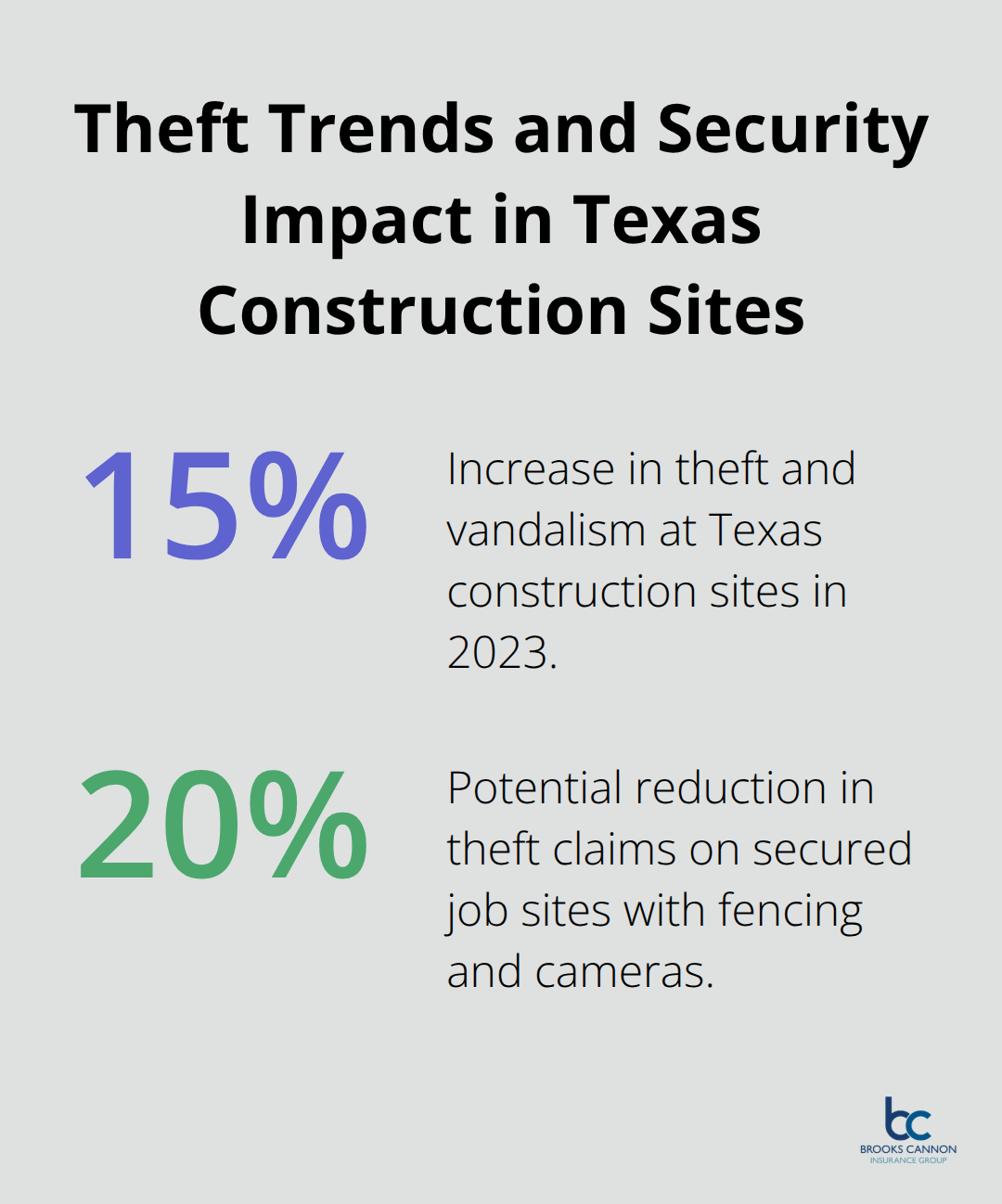

Builders risk insurance protects against theft and vandalism, which increased by 15% at Texas construction sites in 2023. Materials and equipment face constant exposure to theft, especially copper piping, electrical components, and power tools that criminals target for quick resale. Vandalism coverage protects against intentional damage to structures, materials, and equipment on-site. Secured job sites with fencing and cameras can reduce theft claims by up to 20% according to a 2023 Texas study, but coverage remains essential even with security measures in place.

Weather Damage and Natural Disasters

Texas faces significant tornado activity, which makes weather protection vital for construction projects. Standard coverage includes fire, windstorm, hail, and lightning damage to structures and materials. Projects face 15-20 weather-related delays per year in Texas, which can trigger soft cost coverage for architect fees and permit renewals when delays result from covered weather events. Flood and earthquake coverage requires separate endorsements (particularly important for coastal areas and regions with higher natural disaster risks). Projects in riskier locations like flood zones face higher insurance costs but receive protection against region-specific threats.

Materials and Equipment Coverage

The policy covers materials, fixtures, and equipment from the moment they arrive on-site until project completion. Coverage extends to property in transit to the construction site and temporary storage locations. Debris removal after a covered loss receives protection up to $100,000 for projects over $5 million. Change orders during construction can increase total project value, and builders risk insurance typically allows for additional coverage for these changes up to 30% of the original project value.

Critical Exclusions That Catch Contractors Off Guard

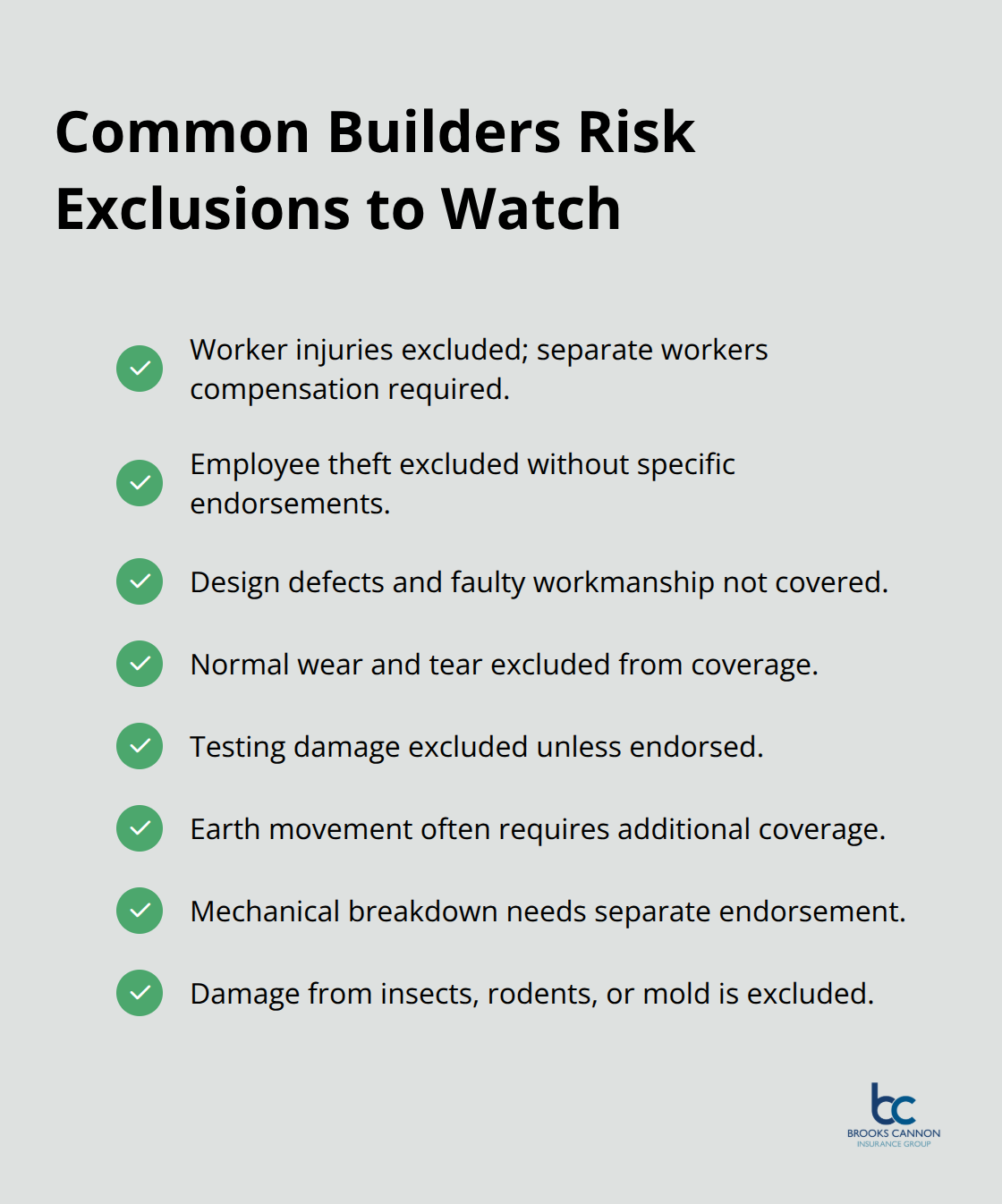

Builders risk policies exclude worker injuries, which requires separate workers compensation coverage. Employee theft falls outside standard coverage (internal theft by workers needs specific endorsements). Design defects, faulty workmanship, and normal wear and tear receive no protection under standard policies. Testing damage gets excluded unless contractors add specific testing endorsements to their coverage.

Earth movement, including landslides and settling, typically requires additional coverage. Mechanical breakdown of equipment needs separate endorsements, and standard policies won’t cover damage from insects, rodents, or mold.

Final Thoughts

Builders risk insurance provides non-negotiable protection for construction projects in Texas. The $200 billion construction industry in our state faces constant threats from theft, weather damage, and vandalism that standard policies cannot address. This specialized coverage fills critical gaps that leave contractors exposed to devastating financial losses.

Cost considerations make this coverage remarkably affordable when measured against potential losses. At 1-4% of total project value, builders risk insurance delivers comprehensive protection that far exceeds its modest investment. A $1 million project faces annual premiums of $10,000 to $30,000 (which represents minimal cost compared to the $30 billion in uninsured storm damage from 2011).

Policy selection requires careful attention to coverage limits, exclusions, and endorsements. Projects need accurate valuations to avoid coinsurance penalties, while additional endorsements for equipment breakdown provide extra protection layers. We at Brooks Cannon Insurance Group help contractors navigate policy complexities and secure competitive rates for comprehensive coverage.