Texas business owners face unique risks that standard insurance policies often miss. From severe weather events to industry-specific liabilities, your business needs comprehensive protection.

A Business Owners Policy Texas offers bundled coverage that addresses these challenges while saving money compared to separate policies. We at Brooks Cannon Insurance Group help Dallas-area businesses navigate these complex coverage decisions daily.

What Does a Business Owners Policy Cover in Texas

A Business Owners Policy combines three essential insurance components into one streamlined package that Texas businesses rely on for comprehensive protection. This bundled approach addresses the specific challenges that small to medium-sized enterprises face across the state.

Core Coverage Foundation

General Liability Insurance forms the backbone of BOP protection and shields businesses from bodily injury claims, property damage lawsuits, and personal injury allegations. This coverage typically provides $1 million per occurrence and $2 million aggregate limits, which addresses most small business exposures effectively.

Commercial Property Insurance protects physical assets including buildings, equipment, inventory, and supplies against fire, theft, vandalism, and weather damage. Texas businesses particularly benefit from this protection given the state’s exposure to severe weather events and property crimes.

Business Income Insurance completes the core trio and replaces lost revenue while covering ongoing expenses when property damage forces temporary closure. This coverage continues until normal operations resume and handles payroll, rent, loan payments, and other fixed expenses that persist during closure periods.

Enhanced Protection Features

Texas BOPs automatically include several valuable extensions that separate policies often exclude or charge extra fees to provide. Employee dishonesty protection guards against theft by workers, while limited cyber liability coverage addresses data breach exposures (increasingly important as businesses digitize operations). Ordinance and law coverage handles building code upgrades during reconstruction, and most policies extend protection to business personal property temporarily located off-premises.

Coverage Performance Data

The Insurance Information Institute reports that more than one-third of businesses identify economic inflation, cyber incidents, and climate change as their top concerns. Property coverage extends beyond basic perils to include equipment breakdown, spoilage of perishable goods, and debris removal costs.

Understanding these coverage components helps Texas business owners evaluate whether a Business Owners Policy meets their specific operational risks and regulatory requirements.

Why Texas Businesses Need Specialized BOP Coverage

Texas businesses face risks that standard insurance approaches cannot handle effectively. The state leads the nation in severe weather events, with tornado activity varying significantly by year and hail damage that exceeded $2 billion in 2023 alone. These weather patterns create property exposures that require specialized coverage extensions beyond basic commercial policies.

Weather-Related Property Risks

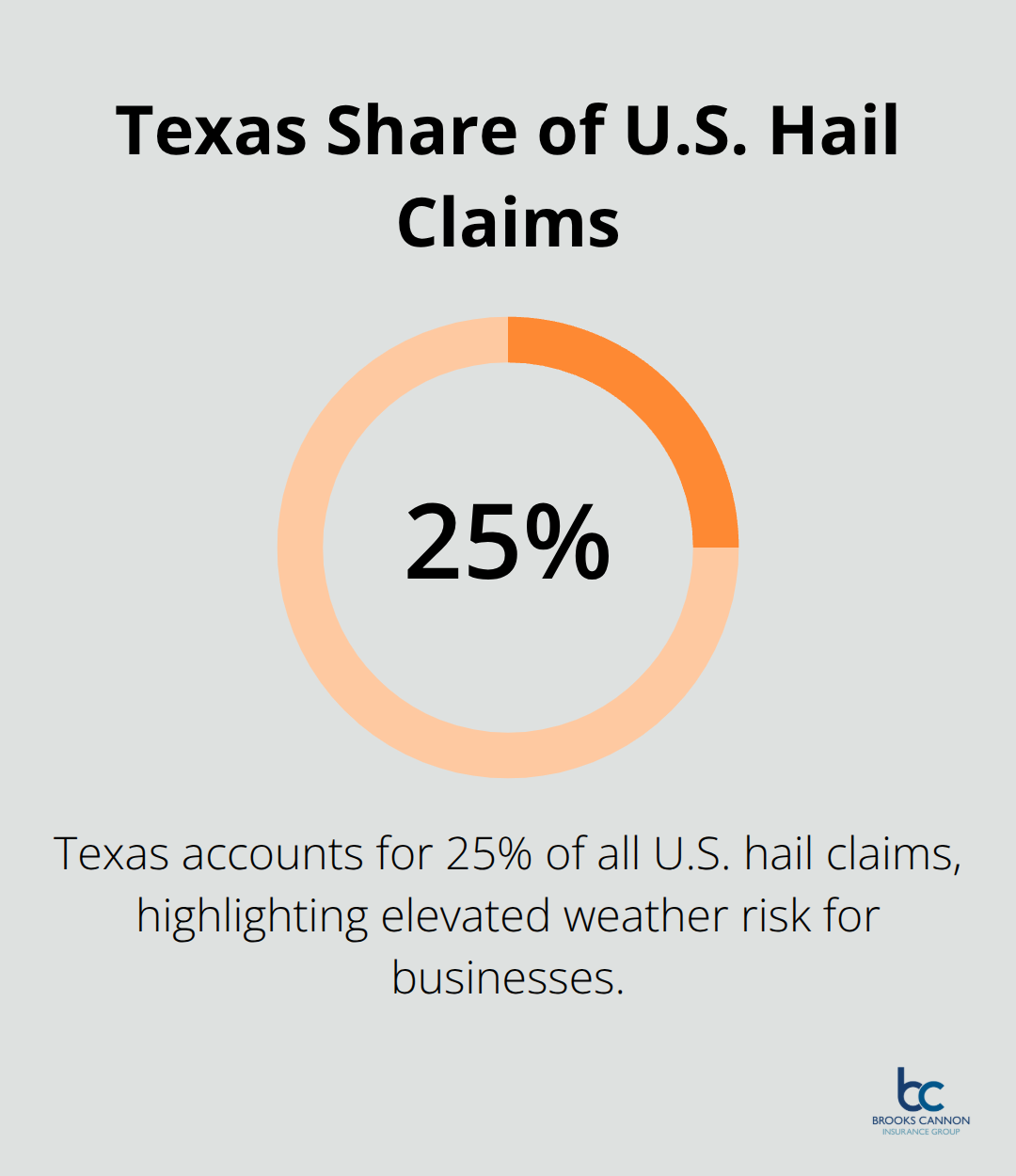

Severe thunderstorms strike Texas more frequently than any other state, with the Insurance Information Institute reporting that Texas accounts for 25% of all U.S. hail claims. Hurricane season brings additional challenges to Gulf Coast businesses, while flash floods affect inland operations throughout the year. Standard property policies often exclude or limit coverage for these perils, making specialized BOP protection essential for Texas operations.

Industry-Specific Liability Exposures

The Texas economy creates unique liability exposures through its dominant industries. Oil and gas operations face environmental regulations that standard policies cannot address. Construction projects deal with specialized equipment risks and contractor liability issues. Agricultural businesses handle chemical exposures and product liability concerns that require enhanced coverage options (particularly for food processing and distribution operations).

For auto repair businesses, specialized insurance policies provide essential protection against industry-specific risks that standard coverage cannot address.

Regulatory Requirements and Cost Benefits

Texas maintains specific insurance regulations that affect coverage requirements and pricing structures. The state does not mandate workers compensation for all employers, but businesses with employees must carry coverage when required by their industry classification. A properly structured BOP addresses these requirements while delivering cost savings of 15-25% compared to separate general liability, property, and business income policies.

The bundled approach proves particularly valuable for Dallas-area businesses where commercial real estate costs and urban liability exposures demand comprehensive risk management. Business owners insurance protects investments from risks by combining property, liability, and business interruption coverage. Understanding these specialized needs helps business owners evaluate which coverage options will provide the most effective protection for their specific operations and budget requirements.

Key Factors When Choosing BOP Coverage in Texas

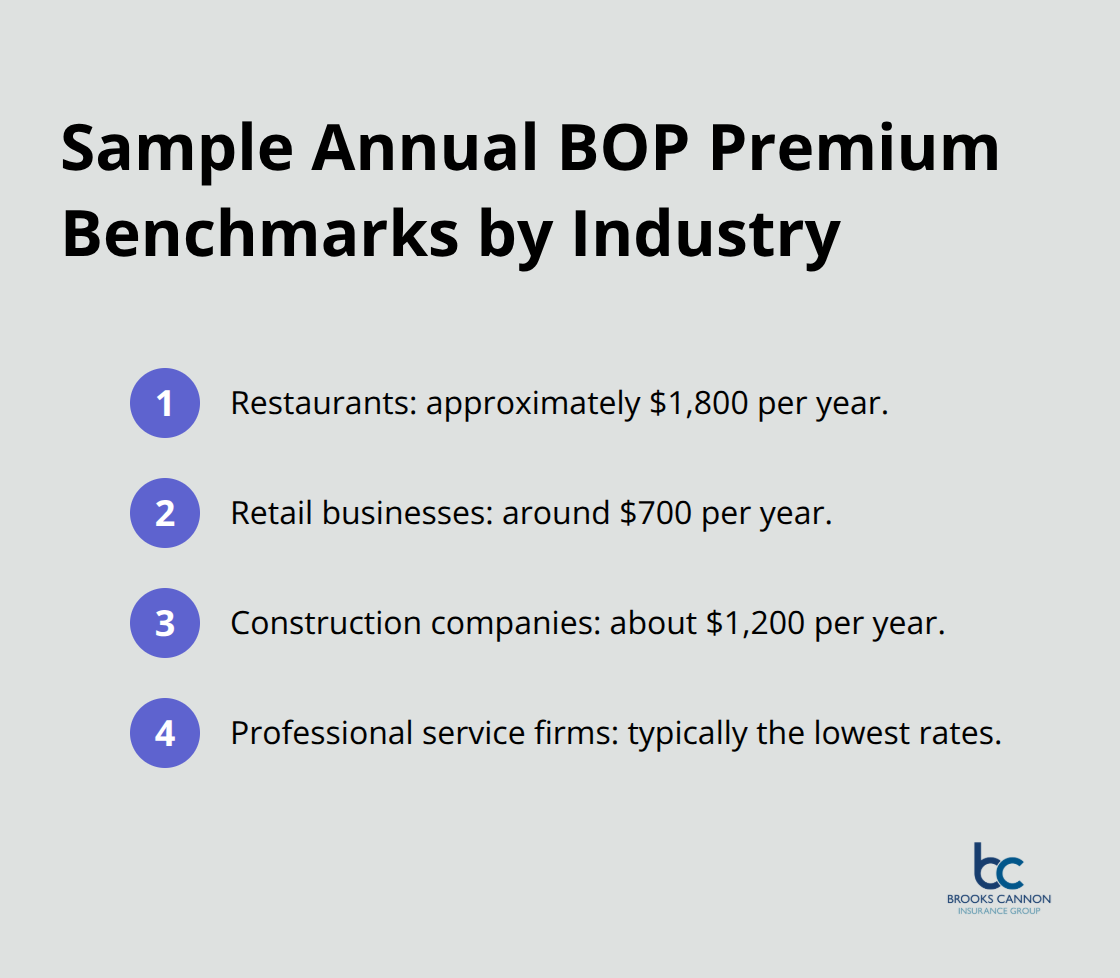

Texas business owners must evaluate several critical factors that directly impact protection levels and premium costs. Industry classification determines baseline risk profiles and available coverage options, with restaurants paying approximately $1,800 annually while retail businesses average $700 per year according to industry data. Construction companies face the highest premiums at around $1,200 annually due to equipment hazards and property damage risks.

Professional service firms typically secure the lowest rates because they present minimal physical liability exposures.

Industry-Specific Coverage Requirements

Different industries face distinct risks that standard BOP policies may not address adequately. Manufacturing businesses need equipment breakdown coverage for specialized machinery, while restaurants require spoilage protection for perishable inventory. Technology companies should add cyber liability endorsements to protect against data breaches and system failures. Healthcare practices need professional liability coverage that most BOPs exclude by default.

Coverage Limits Must Match Actual Exposures

Standard BOP policies provide $1 million per occurrence and $2 million aggregate liability limits, but these amounts prove inadequate for many Texas businesses. Dallas businesses with high foot traffic should consider $2 million per occurrence limits because urban environments generate more frequent claims. Property coverage limits must reflect current replacement costs, not depreciated values, as skilled trades command 4-5% annual wage growth through 2026. Business income limits should cover at least 12 months of operating expenses because weather-related closures often extend longer than anticipated.

Carrier Financial Strength Affects Claim Reliability

Choose carriers with A.M. Best ratings of A- or higher to avoid claim payment delays during major loss events. Texas experiences severe weather that creates simultaneous claims across multiple businesses, testing carrier capacity and financial reserves. Regional carriers may offer lower premiums but lack the financial resources to handle catastrophic losses effectively. National carriers with strong surplus positions provide more reliable claim service when disasters strike multiple policyholders simultaneously.

Deductible Selection Impacts Premium Costs

Higher deductibles reduce annual premiums but increase out-of-pocket expenses during claims. Most Texas businesses benefit from $1,000 to $2,500 property deductibles that balance premium savings with manageable claim costs. Wind and hail deductibles often apply separately and may calculate as percentages of property values rather than flat dollar amounts (typically 1-5% of insured property values).

Final Thoughts

Business owners must evaluate their specific industry risks, coverage limits, and carrier selection to secure proper Business Owners Policy Texas coverage. Start with a thorough risk assessment that identifies property values, liability exposures, and potential business interruption losses. Document inventory, equipment values, and annual revenue to establish accurate coverage limits.

Compare quotes from multiple carriers while you focus on financial strength ratings rather than premium costs alone. Review policy exclusions carefully and identify gaps that require additional endorsements or separate coverage. Consider deductible tolerance and how it affects both premium costs and claim expenses (higher deductibles reduce premiums but increase out-of-pocket costs).

Independent agents provide access to multiple carriers and expert guidance through the selection process. We at Brooks Cannon Insurance Group help Dallas-area businesses navigate complex coverage decisions and secure comprehensive protection that fits their budget and operational needs. Take action now and request quotes to review your current coverage gaps.