One slip-up on a job site can cost your business thousands in medical bills, legal fees, and settlements. Contractor liability protection isn’t optional-it’s the foundation that keeps your company standing when accidents happen.

At Brooks Cannon Insurance Group, we’ve seen contractors in the Dallas area face unexpected claims that could have been prevented with the right coverage strategy. This guide walks you through what general liability actually covers and how to build protection that matches your real job site risks.

What General Liability Actually Covers

General liability insurance protects your contracting business when a third party claims you caused them bodily injury or property damage. If a homeowner trips on your equipment and breaks their leg, or your crew accidentally damages a client’s fence during a roofing job, general liability steps in to cover medical expenses, repair costs, and legal fees. In Texas, where municipalities vary widely in their insurance requirements, general liability is often the first coverage clients demand before you can even bid on a project. Without it, a single accident can deplete your operating capital and force you to shut down.

Medical Bills and Settlement Costs

When someone gets injured on your job site, their medical bills add up fast. General liability covers emergency room visits, ongoing treatment, rehabilitation, and lost wages if the injury prevents them from working. If the case goes to court, the policy also pays for your legal defense-attorney fees, court costs, and expert witness testimony. A single lawsuit can easily cost $50,000 to $150,000 in legal fees alone before any settlement is paid. Adequate coverage limits protect your business from catastrophic losses.

Dallas-area contractors working on residential or commercial projects typically carry per-occurrence limits of $1 million to $2 million, which provides reasonable protection for most job site incidents. Your specific limit should match the scope and value of your projects; larger commercial jobs demand higher limits than small residential repairs.

Third-Party Claims Beyond Direct Actions

General liability also covers claims where you didn’t directly cause the injury but your work created the hazard. If your crew removes safety guardrails during renovation and someone falls, you’re liable even if an employee didn’t push them. If defective materials you installed cause property damage weeks after the job ends, the policy typically covers the claim. This is why selecting adequate coverage limits matters-property damage claims involving structural failures or contamination can reach hundreds of thousands of dollars.

Finding the Right Coverage Limits for Your Trade

An independent insurance agent can help you assess your specific trade and project types to recommend appropriate limits that align with your contracts and client requirements. The risks you face on a roofing job differ significantly from those on a carpentry or HVAC project, and your coverage should reflect those differences. As an independent agency, Brooks Cannon Insurance Group works with multiple top-rated insurance carriers to find the best coverage and pricing for each client’s unique situation. Your agent can review your past projects, current contracts, and growth plans to recommend limits that protect your business without overpaying for unnecessary coverage.

Common Liability Risks Contractors Face

Slip and fall incidents remain the most frequent liability claims on job sites, and they cost contractors heavily. The National Safety Council reports that work injuries cost employers significantly, with total costs reaching $181.4 billion in 2024 when medical care, lost wages, and legal fees combine. A homeowner steps into an unmarked hole on your property, a client’s employee trips over your extension cords, or a visitor slips on debris left behind during demolition-these scenarios happen regularly on Dallas-area job sites. Courts hold contractors accountable for these incidents regardless of intent, which makes site management critical to your liability exposure. General liability covers these claims, but the legal defense alone can reach $50,000 or more even when you ultimately win.

Property Damage Claims That Escalate Quickly

Property damage claims involving client belongings or structural elements demand serious attention from contractors. Your crew accidentally damages a homeowner’s deck while installing new siding, or your equipment punctures a client’s roof during a neighboring job, and repair costs escalate immediately. More problematic are claims where your work causes damage that surfaces months later-a poorly installed window leads to water damage inside walls, or defective roofing materials cause structural rot. These delayed-discovery claims often exceed initial repair estimates and involve disputes over whether your work or pre-existing conditions caused the damage. Courts in Texas frequently split liability between contractors and property owners when evidence remains unclear, meaning you could absorb costs even when shared responsibility applies.

Equipment and Tool-Related Injuries

Equipment and tool-related injuries represent a major exposure that many contractors underestimate. A nail gun misfires and injures a subcontractor’s worker, a circular saw blade shatters and damages someone’s property, or a power tool stored improperly falls and injures a bystander. These incidents involve your equipment but potentially affect people who aren’t directly under your supervision. Your general liability policy covers bodily injury and property damage from these incidents, but only if your coverage limits adequately reflect the severity. A serious equipment-related injury on a commercial job site can easily generate medical bills and settlement demands exceeding $500,000.

Why Coverage Limits Matter for Dallas Contractors

The Dallas construction market has grown significantly, with residential and commercial projects expanding throughout the metro area. More job sites, more workers, and proportionally more exposure to these three liability categories now exist across the region. Your coverage strategy must address each of these real-world scenarios with appropriate per-occurrence and aggregate limits that match your project values and contract requirements. The right limits protect your business when accidents happen, but selecting those limits requires understanding your specific trade and the projects you typically undertake.

How to Strengthen Your General Liability Strategy

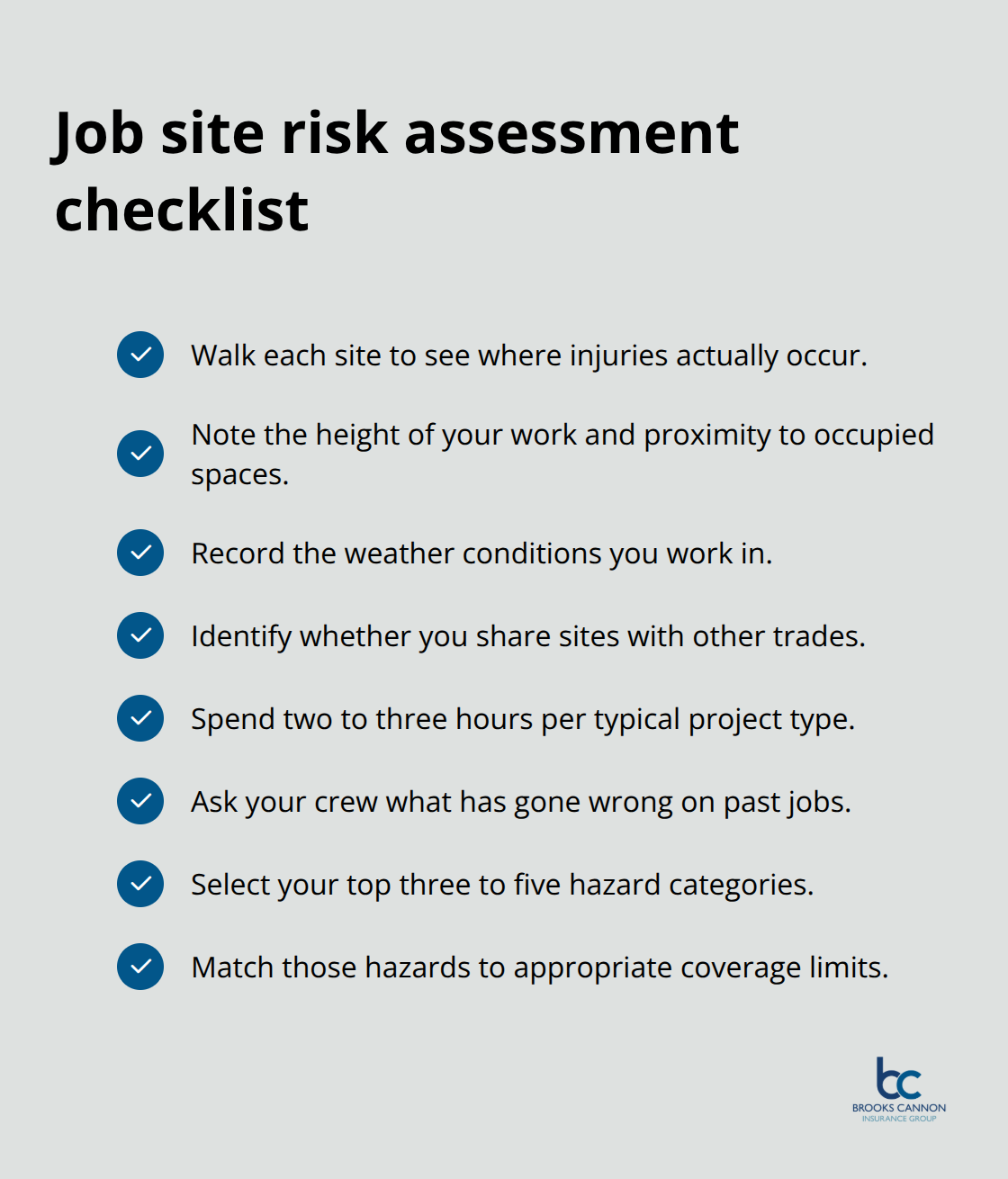

Assess Your Specific Job Site Risks

Walk your job sites and identify where injuries actually occur. Slip and fall incidents dominate contractor claims, but the specific hazards on your sites matter more than industry averages. A roofing contractor faces different exposure than a general contractor doing interior renovations. Document the height of your work, proximity to occupied spaces, weather conditions you work in, and whether you share sites with other trades. This assessment takes two to three hours per typical project type and should include conversations with your crew about what they’ve seen go wrong on previous jobs.

Once you identify your top three to five hazard categories, you can match those risks to appropriate coverage limits.

A contractor handling residential roof repairs might carry $1 million per occurrence, while a commercial general contractor managing multiple subcontractors on larger projects should carry $2 million or higher. The Dallas construction market has expanded significantly, and clients now routinely require proof of specific coverage limits before awarding contracts. A certificate of insurance that shows inadequate limits will cost you jobs, so this assessment directly impacts your ability to bid competitively.

Work with an Independent Agent to Find Adequate Coverage Limits

An independent insurance agent who understands your specific trade and the projects you typically undertake makes a significant difference in your coverage strategy. This is not the time for online quotes alone. An agent can review your past projects, current contracts, and growth plans to recommend limits that actually protect your business rather than simply meeting minimum client requirements. Ask your agent to explain the difference between per-occurrence and aggregate limits, and understand how your specific trade affects pricing.

Roofing contractors, for example, typically pay higher premiums than carpentry contractors because fall risk is greater. Once you have coverage in place, you’ll have the foundation needed to protect your business from catastrophic losses.

Implement Safety Protocols and Risk Management Practices

Safety protocols reduce your actual risk and demonstrate your commitment to loss prevention. The National Safety Council reports that work injuries cost employers significantly, with total costs reaching $181.4 billion in 2024 when combining medical care, lost wages, and legal fees. That figure includes costs that insurance doesn’t cover, such as lost productivity and equipment damage.

Implement daily safety briefings on your job sites, require equipment inspections before use, mark hazards clearly with signage and barriers, and enforce personal protective equipment standards without exception. These practices reduce claims frequency and severity, which insurers recognize through lower renewal premiums. Document your safety efforts with photos, daily logs, and incident reports so you have evidence of your risk management commitment if a claim occurs. This documentation also strengthens your defense in liability disputes where courts evaluate whether you took reasonable precautions to prevent injuries.

Final Thoughts

General liability insurance separates Dallas contractors who survive accidents from those who face financial ruin. A single claim involving serious injury or property damage can exceed $500,000 in medical bills, legal fees, and settlements, and without adequate coverage, that cost falls directly on your business. Proper contractor liability protection demonstrates to clients and municipalities that you operate with professional standards, and this credibility directly impacts your ability to win contracts in the competitive Dallas construction market.

The right strategy combines appropriate coverage limits matched to your specific trade, documented safety protocols that reduce your actual risk, and regular communication with your insurance agent about changes to your business. As your projects grow or your crew expands, your coverage needs change, and an independent agent who understands your work can adjust your limits and endorsements to match your evolving exposure. Contact Brooks Cannon Insurance Group today to strengthen your contractor liability protection and ensure your business stays protected when incidents happen.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation