Most Dallas homeowners think their standard policy covers everything. The truth is far different-gaps in coverage leave families financially exposed when they need protection most.

At Brooks Cannon Insurance Group, we’ve seen too many high-value homes fall short on Dallas high value protection. This guide shows you exactly where your coverage breaks down and how to fix it.

Understanding Your Home’s Real Value

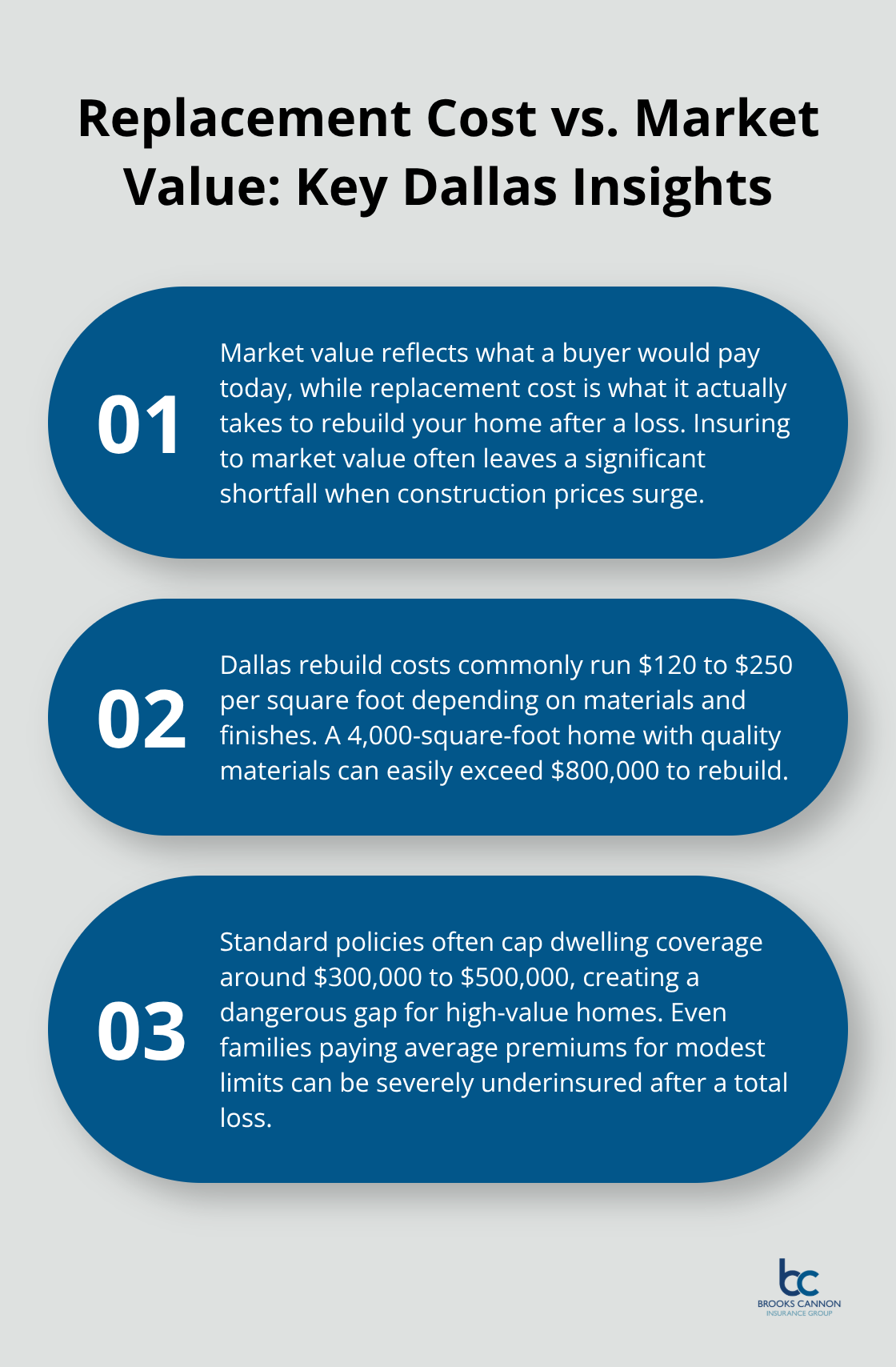

Your home’s market value and its replacement cost are two completely different numbers, and this confusion costs Dallas homeowners thousands in underinsurance every year. A $600,000 home in Highland Park might cost $750,000 to fully rebuild because reconstruction expenses don’t follow real estate prices. Dallas construction costs range from $120 to $250 per square foot depending on materials and finishes, which means a 4,000-square-foot home with quality materials can easily exceed $800,000 to rebuild. Standard homeowners policies typically cap dwelling coverage at $300,000 to $500,000, leaving a massive gap when actual replacement costs run significantly higher. This gap becomes catastrophic after a total loss.

The Texas Department of Insurance and NAIC data show Dallas homeowners pay an average of $3,284 annually for $300,000 in dwelling coverage, yet that same coverage falls short for most luxury properties in the area.

How to Calculate Accurate Replacement Cost

The only way to know your true replacement cost is through a professional appraisal conducted by an insurance appraiser who inspects your home and documents construction materials, custom features, and finishes. This appraisal captures details like whether you have granite or marble counters, hardwood or tile flooring, and custom cabinetry that standard valuations miss entirely. High-value carriers like Westfield, Chubb, and Travelers require these appraisals before issuing policies above $1.5 million in dwelling coverage, and for good reason. Without an appraisal, you’re essentially guessing. An independent agent can coordinate this inspection and help you understand what the appraiser finds. Once you know your true replacement cost, you can set dwelling limits that actually match your home’s value. Guaranteed replacement cost coverage removes the risk that inflation or market changes leave you short if disaster strikes.

Common Underinsurance Issues in Dallas

Hail damage claims rank as the leading cause of home insurance losses in Dallas, with 5 to 8 significant hail events annually between March and June, yet many policies include a separate wind and hail deductible of 1 to 2 percent of dwelling coverage. For a $400,000 home, that means an $8,000 out-of-pocket expense on a single claim. Homeowners see these deductibles and assume their base coverage is adequate, but they’re not accounting for the actual cost to repair or replace what hail damages. Foundation issues and water damage present another blind spot. Standard policies often exclude sewer backup and certain water intrusions, leaving Dallas homeowners exposed to expensive repairs that fall entirely on their shoulders. Roof age compounds the problem. Homes with roofs over 15 years old pay significantly higher premiums, and many insurers won’t renew policies for roofs beyond 20 years, forcing homeowners into specialty markets where coverage costs jump dramatically. A new roof delivers one of the largest premium discounts available, yet most homeowners don’t make this connection until renewal time.

These gaps in coverage-from hail deductibles to water damage exclusions to roof age restrictions-create the conditions where families face unexpected financial strain. The next section reveals which valuable items and personal property limits leave you most exposed when loss strikes.

Protection Gaps Most Dallas Homeowners Miss

Valuable Items and Personal Property Limits

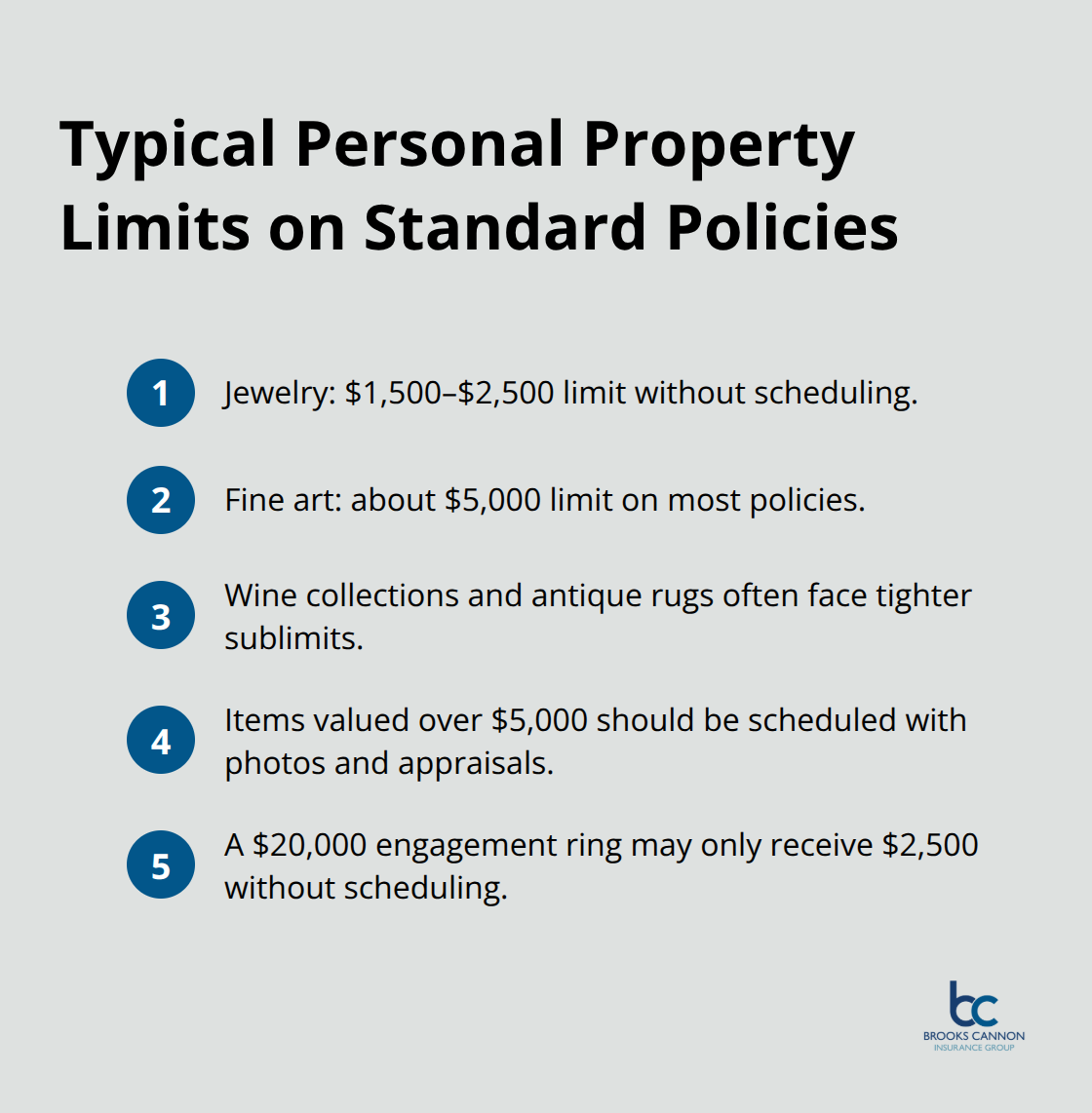

Standard homeowners policies impose strict limits on personal property that make no sense for Dallas homeowners with valuable collections. Jewelry caps out at $1,500 to $2,500 on most standard policies, fine art at $5,000, and specialty items like wine collections or antique rugs receive even tighter restrictions. If you own a single piece of jewelry worth $15,000 or a wine collection valued at $30,000, your standard policy leaves you dramatically underprotected.

High-value carriers remove these artificial ceilings through scheduled personal property coverage, which protects high-value items like jewelry and fine art beyond standard policy limits and often cover accidental loss that standard policies exclude entirely. You need a detailed inventory with photos, receipts, and professional appraisals for items exceeding $5,000. This documentation speeds claims processing and prevents disputes over actual value when loss occurs. Without scheduling, a $20,000 engagement ring becomes a $2,500 claim, and the gap comes directly from your pocket.

Water Damage and Foundation Issues

Water damage and foundation issues represent the second major blind spot we see constantly in Dallas. Standard policies frequently exclude sewer backup, which costs $10,000 to $25,000 to remediate, and most homeowners discover this exclusion only after a basement flood from heavy rain or a sewer line failure. High-value policies include sewer backup protection as standard, plus water damage coverage that extends to foundation issues and moisture intrusion.

Dallas experiences significant spring thunderstorms and occasional flooding, yet most homeowners purchase flood insurance only after a claim denial forces the issue. Flood coverage remains separate from your homeowners policy entirely (whether through the National Flood Insurance Program or private carriers), and waiting to purchase it until you need it often means coverage is unavailable. This timing mistake costs families tens of thousands in uninsured losses.

Liability Exposure and Guest Injuries

Liability exposure presents the third critical gap. Standard policies typically include $100,000 to $300,000 in liability coverage, which sounds adequate until a guest suffers a serious injury on your property or someone sues after an accident at your home. A single lawsuit for $500,000 or more exhausts standard liability limits instantly.

High-value homes require umbrella coverage extending liability to $1 million or higher, which costs far less than most homeowners expect (typically $150 to $400 annually for $1 million in additional coverage). If you employ household staff, gardeners, or contractors regularly, you also need liability coverage for household employees that covers medical expenses and lost wages if someone is injured during work. These three protection gaps-underinsured valuables, excluded water damage, and inadequate liability-account for the majority of claims disputes and financial shortfalls among Dallas families, and addressing them requires a strategic approach that goes beyond standard policy language.

Building a Comprehensive Home Insurance Strategy

Strategic Bundling Across Multiple Carriers

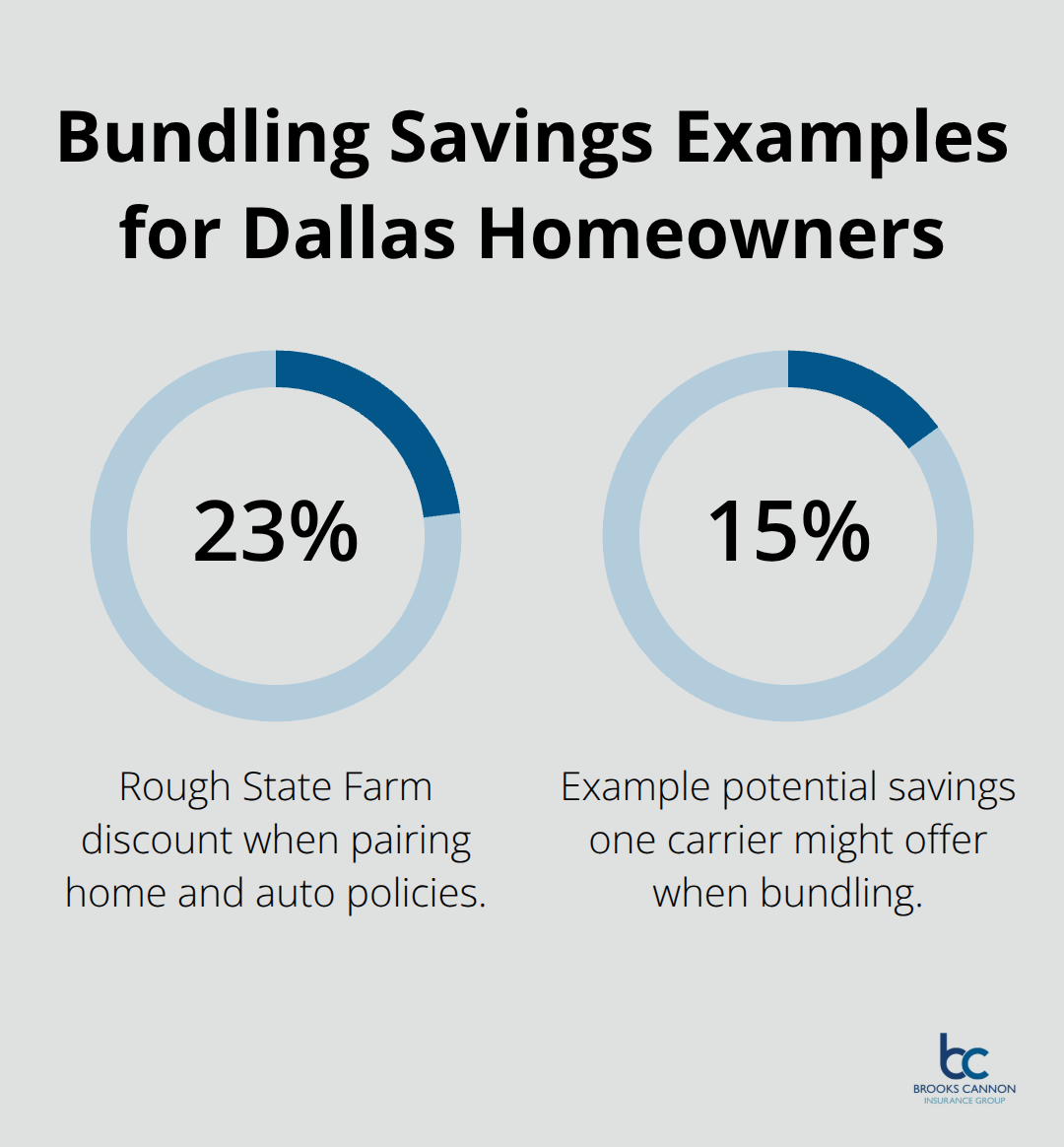

Most Dallas homeowners accept whatever their current carrier offers at renewal time, leaving money on the table and protection incomplete. State Farm reports roughly 23 percent bundling discounts when pairing home and auto policies, which translates to real savings for Dallas families. However, the lowest combined cost isn’t always the best option. An independent agent can compare bundled versus separate policies across multiple carriers to confirm you’re actually saving money while maintaining superior coverage.

A Dallas homeowner might find that bundling with one carrier saves 15 percent on premiums but costs 10 percent more in actual dollars compared to shopping home and auto separately across two different insurers. This comparison matters far more than accepting convenience.

Umbrella Coverage: Your Financial Safety Net

Umbrella liability coverage represents the most underutilized protection tool in Dallas. A one-million-dollar umbrella coverage policy typically costs between $150 and $400 annually, yet most high-value homeowners skip it entirely because they don’t understand the actual risk exposure. A single guest injury claim, a lawsuit from an accident on your property, or a dog bite incident can easily reach $500,000 in damages. Standard homeowners liability coverage maxes out at $100,000 to $300,000, leaving you personally liable for amounts exceeding that limit. Umbrella coverage sits above your homeowners and auto liability limits and protects your personal assets when a claim exceeds underlying coverage. For Dallas families with significant net worth, this protection is non-negotiable.

Annual Policy Reviews That Track Real Changes

Life changes constantly: your home increases in value, you acquire valuable art or jewelry, roof age advances, construction costs inflate, and your family’s circumstances shift. A comprehensive review every 12 months ensures your dwelling limits track actual replacement costs, your personal property scheduling covers new acquisitions, and your liability limits align with your current net worth. This annual discipline prevents the common scenario where homeowners discover coverage shortfalls only after loss occurs, when it’s far too late to adjust. Most carriers send renewal notices that focus on premium changes, not coverage adequacy. An independent agent conducts a true policy review that examines whether your current limits still match your home’s actual replacement cost and your family’s financial exposure. This proactive approach costs nothing and prevents thousands in potential losses.

Final Thoughts

Your home’s true value extends far beyond what your current policy states. The gaps we’ve outlined-underinsured dwelling limits, capped personal property coverage, excluded water damage, and inadequate liability protection-represent real financial exposure that grows every year as Dallas construction costs rise. Assessing your coverage honestly means pulling out your actual policy and comparing dwelling limits to your home’s true replacement cost, not its market value.

An independent agent who understands Dallas high value protection can coordinate professional appraisals to establish accurate replacement costs, compare quotes across multiple carriers to find the best combination of coverage and price, and ensure your personal property scheduling protects items that standard policies ignore entirely. They can also review your liability exposure and recommend umbrella coverage that costs far less than most homeowners expect. This approach puts you in control of your protection strategy rather than accepting whatever your current carrier offers at renewal.

We at Brooks Cannon Insurance Group work with Dallas families to build comprehensive protection that actually matches their homes and their financial situations. Contact our team at brookscannon.com to discuss your coverage and secure the Dallas high value protection your family deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation