One lawsuit can drain your business savings in weeks. General liability coverage protects you from the financial devastation of bodily injury claims, property damage lawsuits, and medical expenses.

We at Brooks Cannon Insurance Group help small business owners in Dallas understand what coverage they actually need. This guide walks you through the essentials so you can protect your business with confidence.

What General Liability Coverage Actually Protects

Three Core Areas of Protection

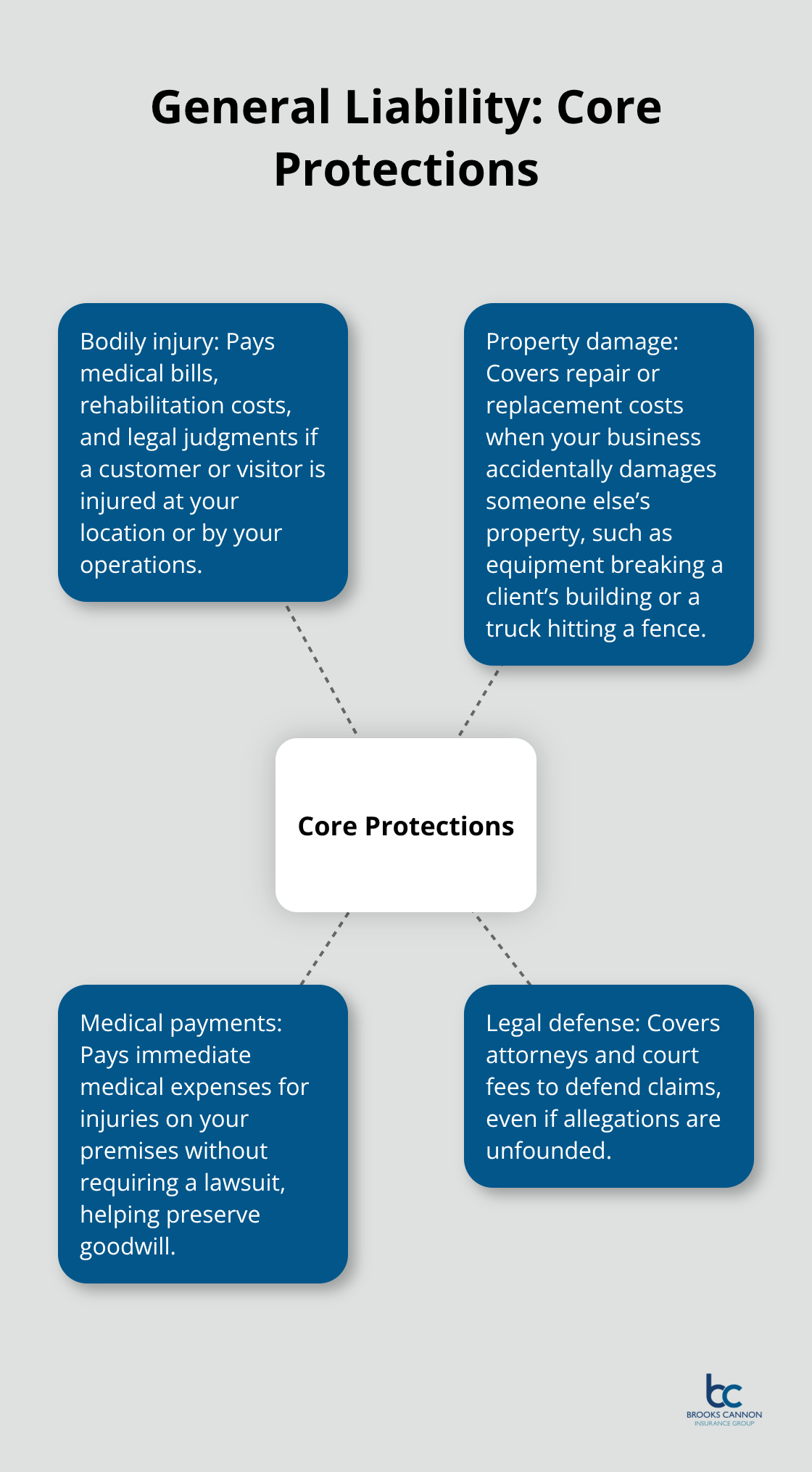

General liability insurance covers three distinct areas that protect your business when someone gets hurt or property gets damaged because of your operations. Bodily injury protection pays medical bills, rehabilitation costs, and legal judgments if a customer or visitor is injured at your location or by your business activities. Property damage coverage handles the cost of repairing or replacing someone else’s property that you accidentally damage-like if your equipment breaks a client’s building or your delivery truck hits their fence. Medical payments coverage is separate and pays immediate medical expenses for injuries on your premises without requiring a lawsuit, which speeds up resolution and protects goodwill. Legal defense costs are included in your policy limits, meaning your insurer pays attorneys and court fees to defend you against claims, whether they’re legitimate or not.

Why Legal Defense Costs Matter in Dallas

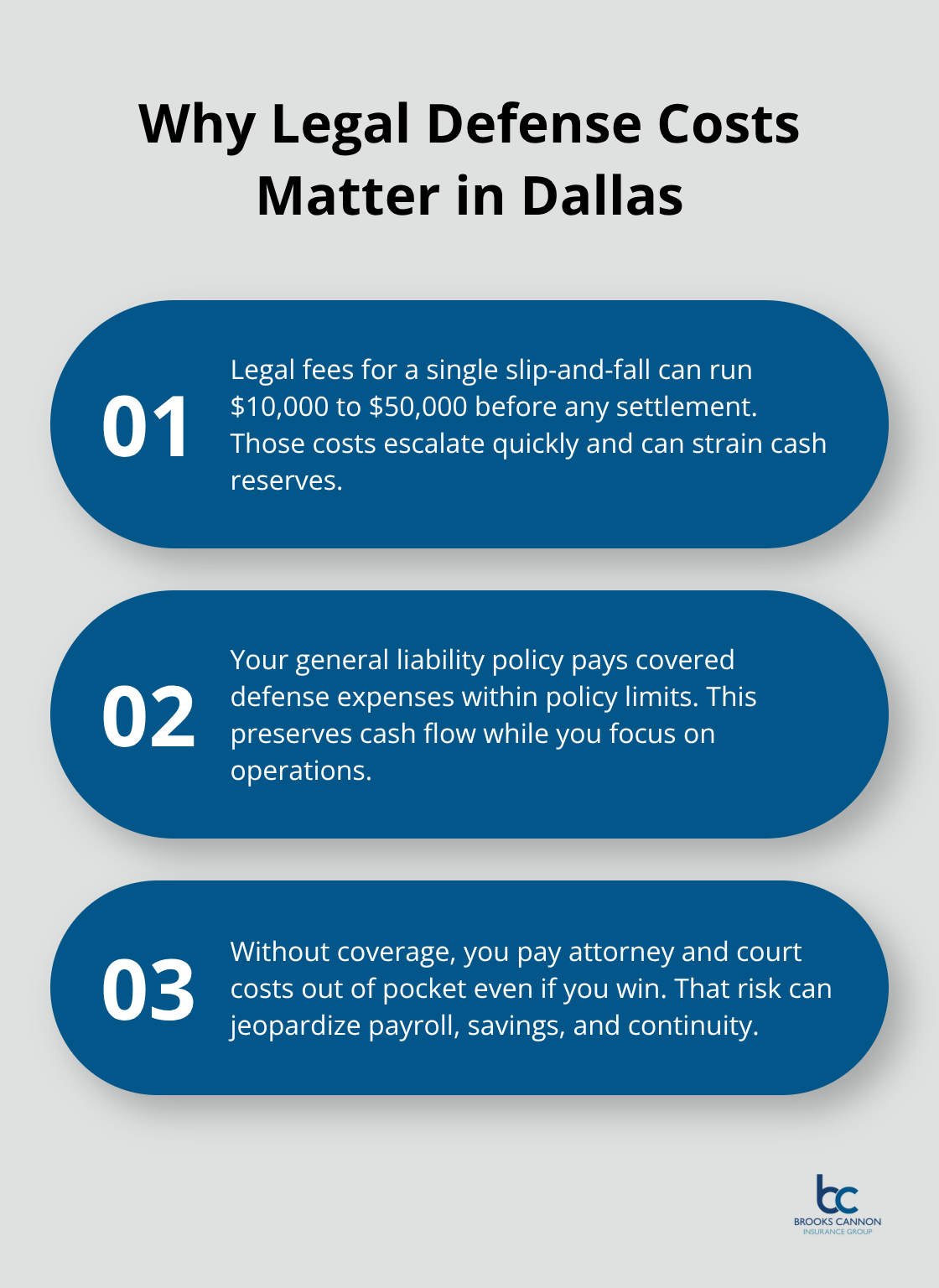

For small businesses in Dallas, this matters because a single slip-and-fall lawsuit can cost $10,000 to $50,000 in legal fees alone before any settlement. Your policy covers these expenses, which protects your cash flow when you face unexpected litigation. Without this protection, you absorb attorney fees and court costs out of pocket, even if you win the case.

Understanding Coverage Limits and What They Mean

The coverage limits you choose directly impact what your policy actually protects. A standard starting point is $1 million per occurrence and $2 million aggregate, which means your insurer pays up to $1 million for any single incident and $2 million total for all claims in a year. If a claim exceeds your per-occurrence limit, you pay the difference out of pocket, and your aggregate limit shrinks accordingly. Texas data shows small businesses typically pay around $65 to $90 per month for general liability with $1 million coverage, but contractors and high-risk industries pay significantly more.

How Your Industry Affects Coverage Needs

The cost depends on your industry type, number of employees, annual revenue, and claims history. Retailers and contractors benefit most from this coverage because they have frequent customer interaction and work on other people’s property. Professional service providers like consultants and designers should pair general liability with professional liability insurance, which covers mistakes in your work rather than accidents on a job site. Understanding your specific risk profile helps you select appropriate limits that actually match your exposure.

Why Your Business Needs General Liability Insurance

The Real Cost of a Single Lawsuit

A slip-and-fall lawsuit in your Dallas storefront costs you $25,000 to $100,000 in legal defense and settlement expenses, even if you’re partially at fault. Without general liability coverage, that money comes directly from your business account or personal savings. Most small business owners lack that kind of cash sitting around, which means a single incident forces you to take out loans, delay payroll, or worse. General liability insurance transforms that financial catastrophe into a manageable claim your insurer handles. Your policy pays the medical bills, the legal fees, the settlements-everything up to your coverage limits. This protection matters if you have customers, clients, or employees on your premises or working at client locations.

Lease Requirements and Contract Demands

Dallas commercial leases almost always require proof of general liability insurance before you sign. Clients bidding on contractors demand certificates of insurance showing active coverage with specific limits, typically $1 million per occurrence. If you’re a consultant, designer, or service provider working at client sites, many contracts won’t move forward without documented liability protection. Your landlord or business partner won’t accept verbal assurances-they need written proof that your policy covers their interests. Without this documentation, you lose the opportunity to secure the lease or land the contract, regardless of how solid your business fundamentals are.

Financial Protection You Actually Need

Even if coverage isn’t legally mandated for your specific business, the financial exposure from a single claim is so severe that skipping this coverage is reckless. Texas data shows small businesses pay $65 to $90 monthly for solid $1 million coverage, which is far cheaper than absorbing even a modest lawsuit out of pocket. That monthly investment (roughly $810 to $1,080 per year) protects your personal assets, your business savings, and your ability to operate. The real question isn’t whether you can afford general liability insurance-it’s whether you can afford not to have it.

What Happens When You Choose the Right Coverage

When you select appropriate coverage limits based on your industry and risk profile, you eliminate the anxiety of facing a lawsuit alone. Your insurer handles the claim process, covers legal representation, and pays settlements within your policy limits. This allows you to focus on running your business instead of managing litigation. As an independent agency, we at Brooks Cannon Insurance Group work with multiple top-rated carriers to find coverage that fits your specific situation and budget.

Now that you understand why general liability coverage protects your business, the next step is selecting the right policy limits and comparing your options to find competitive rates that match your needs.

Selecting Coverage Limits That Match Your Actual Risk

Identify Your Business’s Real Exposure

Start by identifying what your business specifically exposes you to, not what a generic template suggests. A hair salon faces different risks than a construction contractor, yet many small business owners apply one-size-fits-all coverage limits. Walk through a typical day at your business and document where injuries or property damage could realistically occur. If you work at client locations, that exposure is higher than if customers visit you. If you handle products, product liability becomes relevant. If you employ staff, your premises liability exposure increases. Texas data shows contractors typically need higher limits than service providers because they work on other people’s property, where a single incident can cause substantial damage.

Check Your Lease and Contract Requirements

Talk to your landlord about what limits they require in your lease, and ask major clients what their contracts demand. Most lease agreements require tenants to carry liability insurance with a specified limit of liability, such as $1,000,000 for each occurrence, but some larger clients or municipal contracts require $2 million. These requirements aren’t negotiable-your landlord and clients won’t move forward without documented proof that your coverage meets their standards. Understanding these demands upfront prevents you from purchasing inadequate coverage that fails to satisfy your business obligations.

Choose Your Deductible Strategy

Your deductible choice directly impacts your monthly premium and out-of-pocket costs when a claim happens. A $500 deductible costs less monthly than a $1,000 deductible, but you pay $500 out of pocket before coverage kicks in. Small businesses with stable cash flow and low claims history typically benefit from higher deductibles because they lower monthly costs significantly (sometimes by 15 to 25 percent according to industry data). However, if your business operates on thin margins or experiences frequent minor incidents, a lower deductible protects your cash flow when claims occur.

Calculate Total Cost of Ownership

The real strategy is comparing total cost of ownership, not just the premium. A policy costing $60 monthly with a $1,000 deductible might cost you less annually than a $75 monthly policy with a $500 deductible if you never file a claim. But if you file one claim per year, the lower deductible saves money overall. Multiple carriers offer different combinations of premiums and deductibles, so comparing these trade-offs shows you what you’re actually paying (both in premiums and potential out-of-pocket costs). An independent agency can present these options side by side so you understand the financial impact of each choice before you commit to a policy.

Final Thoughts

General liability coverage protects your Dallas business from the financial devastation of a single lawsuit, and most lease agreements and client contracts demand proof of coverage before you proceed. The monthly cost of protection (typically $65 to $90) is far less than the legal fees and settlements you’d pay out of pocket without it. Your business faces real risks every day, whether from customer injuries, property damage you cause, or legal defense costs that drain cash flow.

Start by reviewing your lease agreement and major client contracts to identify required coverage limits, then assess your specific industry exposure by walking through your typical operations and documenting where injuries or damage could realistically occur. Compare deductible options alongside premium costs to understand your total financial commitment, since a higher deductible lowers your monthly payment but increases out-of-pocket costs when a claim occurs. Multiple carriers offer different combinations, so side-by-side comparisons show you the real cost of each option before you commit.

We at Brooks Cannon Insurance Group work with multiple top-rated carriers to find general liability coverage that matches your specific situation and budget. Our licensed team understands Dallas business risks and can help you select appropriate limits, compare deductible strategies, and secure competitive rates so you can focus on running your business with confidence.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation