Luxury homes worth $1 million or more need specialized protection that standard homeowners policies can’t provide. High net worth home insurance offers the comprehensive coverage affluent homeowners require.

We at Brooks Cannon Insurance Group understand that protecting significant assets demands more than basic coverage limits and standard policy features.

Why Standard Policies Fall Short for Million-Dollar Homes

Standard homeowners insurance caps dwelling coverage at $500,000 according to the Insurance Information Institute, which makes it inadequate for luxury properties. High net worth home insurance addresses this gap with dwelling limits that reach $10 million or more, plus extended replacement cost coverage that pays 125% to 150% above policy limits when reconstruction costs exceed estimates.

Personal Property Protection That Matches Your Assets

Standard policies limit personal property to 50% of dwelling coverage and often cap jewelry at $2,500 and art at $5,000. High net worth policies provide automatic jewelry coverage of $50,000 to $100,000 and blanket personal property protection without individual item limits. Wine collections worth $100,000, art pieces valued at $500,000, and antique furniture require agreed value coverage to avoid depreciation disputes when claims occur. Professional appraisals every 3-5 years maintain accurate valuations for these high-value items.

Liability Limits That Protect Your Wealth

Affluent homeowners face higher liability exposure due to their visible wealth and attractive properties for litigation. Standard policies typically offer $300,000 liability limits, which proves insufficient for high net worth individuals. High-value policies start at $1 million liability coverage and can extend to $10 million or more. Personal umbrella policies add another $5 million to $100 million in protection. With average verdicts in Texas reaching $826,892 for personal injury lawsuits, inadequate coverage threatens accumulated wealth and future income streams.

Additional Living Expenses for Luxury Lifestyles

Standard policies provide additional living expenses equal to 20% of dwelling coverage, which typically amounts to $100,000 for most homes. Luxury homeowners may face monthly expenses of $15,000 to $50,000 when their residences become uninhabitable. High-value policies cover living expenses up to 50% to 100% of dwelling limits, which accommodates more luxurious temporary housing needs and maintains your lifestyle during reconstruction periods.

These enhanced coverage features form the foundation of proper high net worth protection, but selecting the right coverage amounts requires careful evaluation of your specific assets and risk exposure.

Key Coverage Features for Affluent Homeowners

Guaranteed Replacement Cost Protection

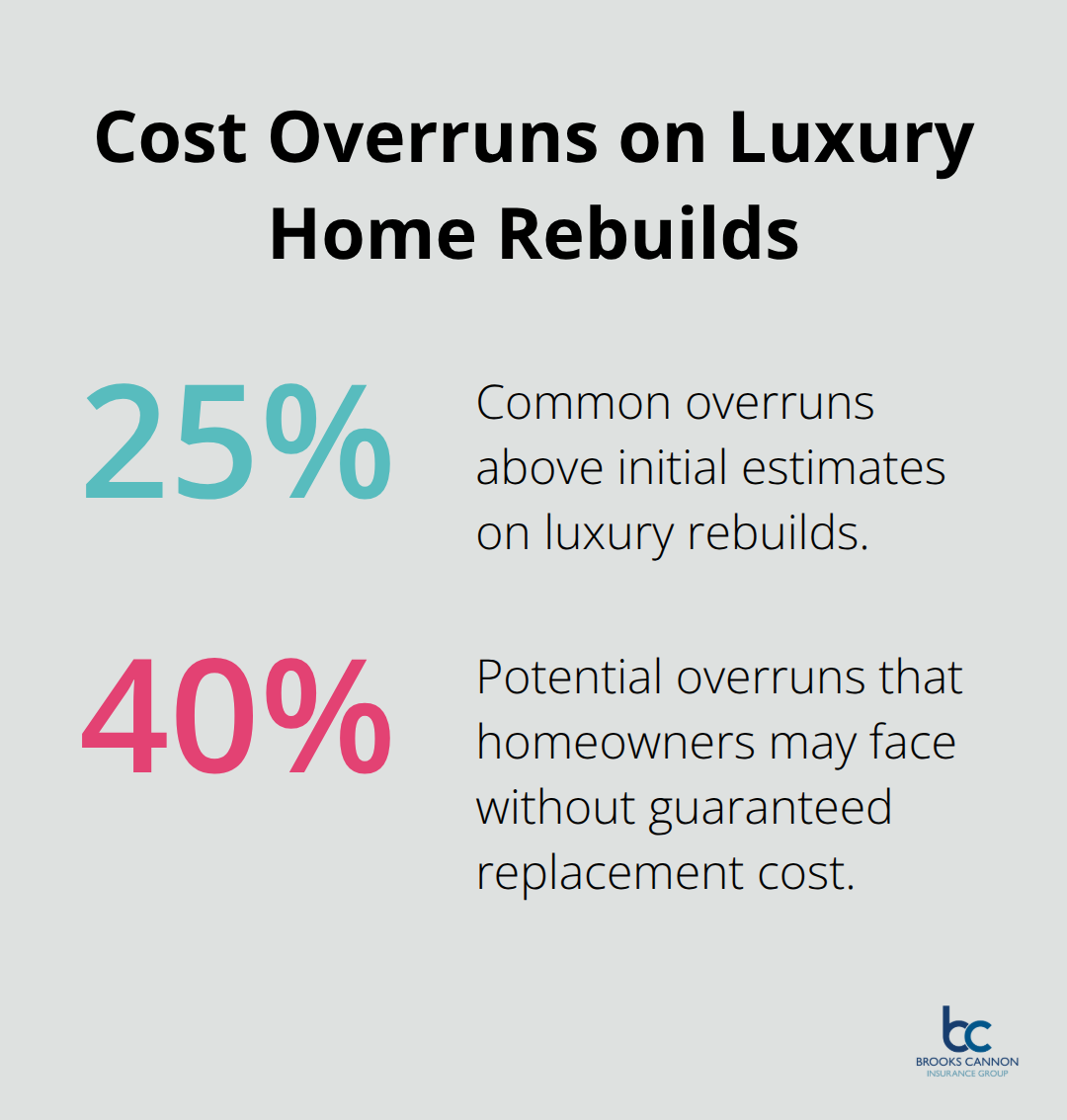

Guaranteed replacement cost coverage removes the guesswork from reconstruction estimates and stands as the most important feature for affluent homeowners. This coverage pays whatever amount is necessary to rebuild your home to its original condition, regardless of the policy limit. The National Association of Home Builders reports reconstruction costs for luxury homes average $400 to $800 per square foot, but unique architectural features and custom materials push costs much higher. Standard replacement cost coverage caps payments at policy limits and leaves homeowners responsible for cost overruns that commonly reach 25% to 40% above estimates.

Blanket Personal Property Coverage

Blanket personal property protection eliminates the process of scheduling individual items and provides automatic coverage for new acquisitions. This feature covers all personal property up to the policy limit without separate limits for categories like electronics, clothing, or furniture. Most high-value policies offer blanket coverage that starts at $500,000 and extends to $2 million or more. The key advantage lies in flexibility – you can replace a $50,000 watch collection with $50,000 worth of art without policy modifications. Standard policies force homeowners to list expensive items individually and update coverage each time they purchase valuable items.

Extended Displacement Coverage

Additional living expenses coverage becomes essential when luxury home reconstruction takes 18 to 36 months rather than the 6 to 12 months typical for standard homes. High-value policies provide unlimited time periods for additional living expenses, while standard policies often limit coverage to 12 to 24 months. Monthly luxury living costs can reach $30,000 to $75,000 when you rent comparable properties and maintain your lifestyle (including temporary housing, storage, restaurant meals, and other necessary expenses). This coverage operates without the time restrictions that could force you to accept substandard living conditions during extended reconstruction periods.

The right coverage features protect your assets, but selecting the appropriate insurance provider requires careful evaluation of their expertise and specialization in high-value properties.

How Do You Select the Right High Net Worth Insurer

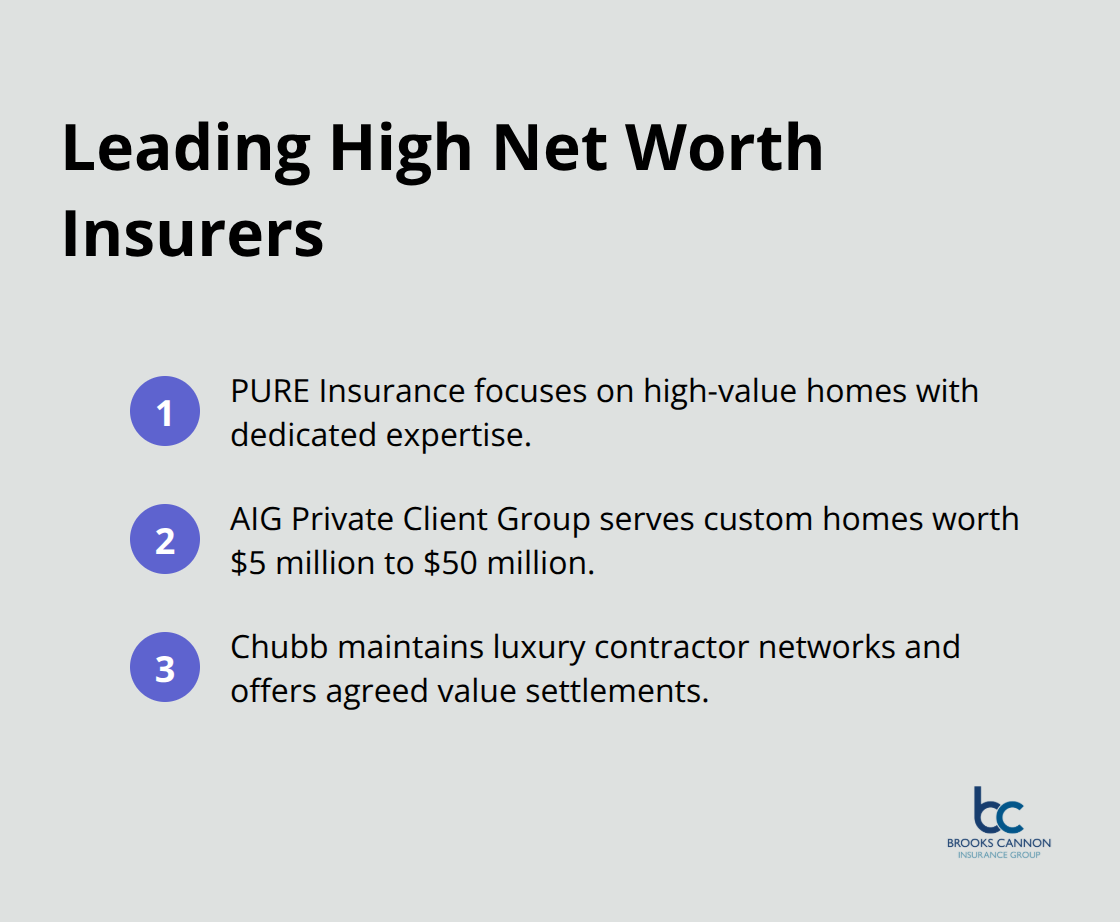

You need to work with carriers that specialize exclusively in luxury property protection rather than companies that treat high-value homes as add-ons to standard policies. PURE Insurance, AIG Private Client Group, and Chubb lead the market with dedicated high-value divisions that understand reconstruction complexities for custom homes worth $5 million to $50 million. These specialized carriers maintain relationships with luxury contractors, employ claims adjusters trained in high-end materials, and offer agreed value settlements that prevent disputes over replacement costs.

Standard insurers like State Farm and Allstate lack the expertise to handle claims for properties with imported marble, custom millwork, or smart home systems worth $200,000.

Professional Appraisals Drive Accurate Coverage

Professional home appraisals form the foundation of proper coverage limits. Appraiser qualification includes multiple licensing levels, college degree, appraisal education and experience hours, and standardized tests. Appraisers certified in luxury properties document architectural details, imported materials, and custom features that standard assessments miss. Wine cellars, home theaters, and elevator systems require specialized valuation methods that general appraisers cannot provide. You should update appraisals every three to five years and immediately after renovations that exceed $100,000 to maintain accurate replacement cost estimates.

Agent Expertise Determines Coverage Success

High net worth insurance agents typically require minimum annual premiums of $25,000 to take on new accounts, which reflects their specialized knowledge and limited client capacity. These agents understand coverage gaps that affect luxury homeowners, such as ordinance and law coverage for homes in historic districts or coverage for detached structures like pool houses worth $500,000. Agents without high-value experience often recommend inadequate coverage limits or miss essential endorsements that protect against unique risks affluent homeowners face.

Risk Assessment and Property Evaluation

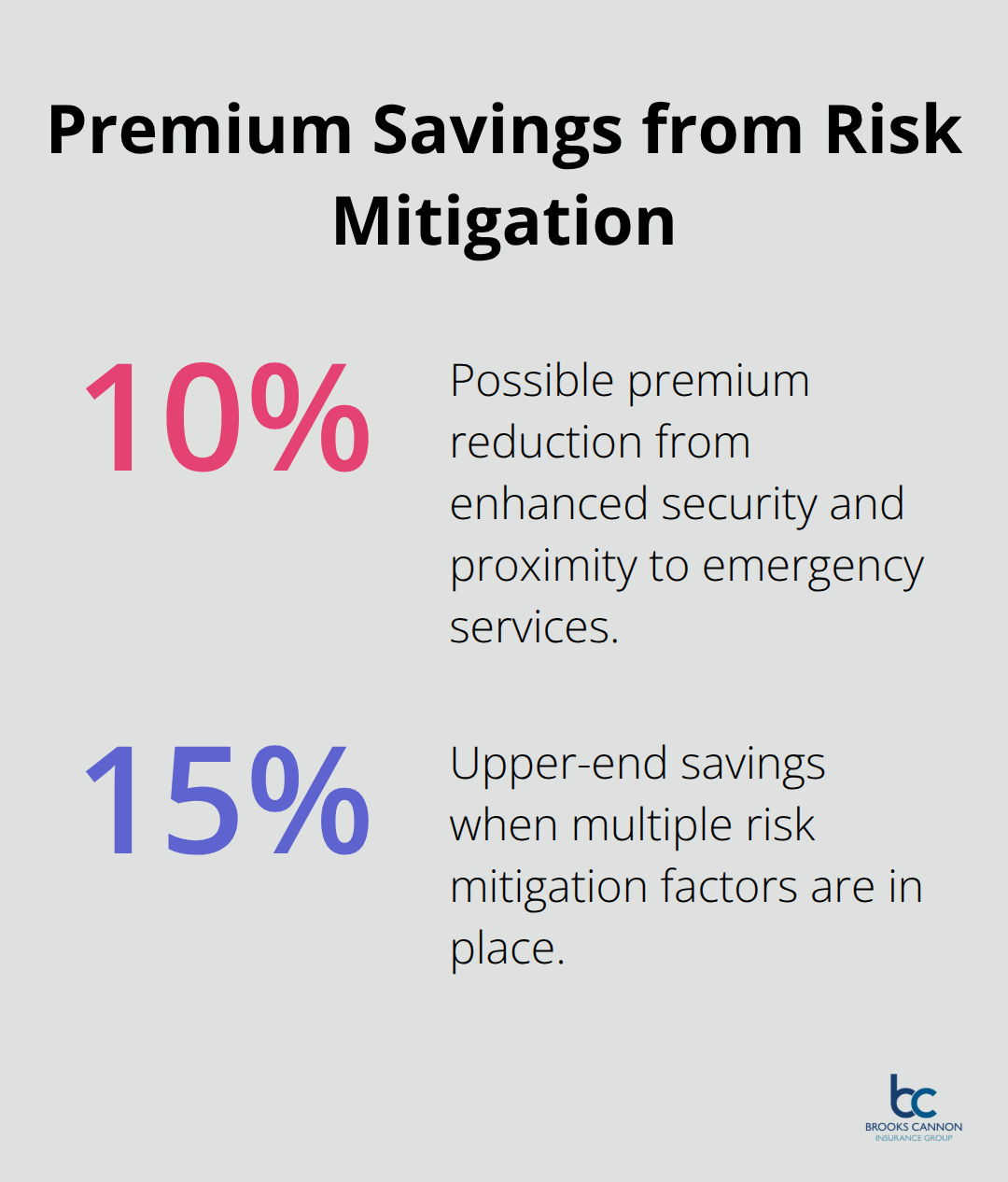

Specialized carriers conduct comprehensive risk assessments that examine factors beyond basic property values. They evaluate security systems, fire suppression equipment, and proximity to emergency services (which can reduce premiums by 10% to 15%). These assessments identify potential vulnerabilities like aging electrical systems or inadequate drainage that could lead to significant claims.

The evaluation process includes detailed photography and documentation of custom features that standard carriers often overlook or undervalue.

Final Thoughts

High net worth home insurance provides the specialized protection that affluent homeowners need to safeguard their significant investments. Standard policies simply cannot match the coverage limits, specialized features, and expert service that luxury properties require. Annual premiums of $15,000 to $25,000 for comprehensive high-value coverage represent a small fraction of your property value while they protect against potentially devastating financial losses.

Specialized carriers and experienced agents make the difference between adequate protection and coverage gaps that could cost millions. Professional appraisals, guaranteed replacement cost coverage, and blanket personal property protection form the foundation of proper high net worth insurance programs. These components work together to address the unique risks that luxury homeowners face (from custom architectural features to valuable collections worth hundreds of thousands of dollars).

We at Brooks Cannon Insurance Group help clients find optimal coverage for their unique situations. Our team understands the complexities of luxury property insurance and provides the advocacy you need when you protect your most valuable assets. Contact us today to review your current coverage and explore comprehensive high-value insurance solutions.