Owning rental property in Dallas comes with unique risks that standard homeowners insurance won’t cover. Property damage, tenant injuries, and lost rental income can cost thousands without proper protection.

We at Brooks Cannon Insurance Group see landlords face these expensive surprises regularly. Landlord insurance fills the gaps that leave rental property owners financially exposed.

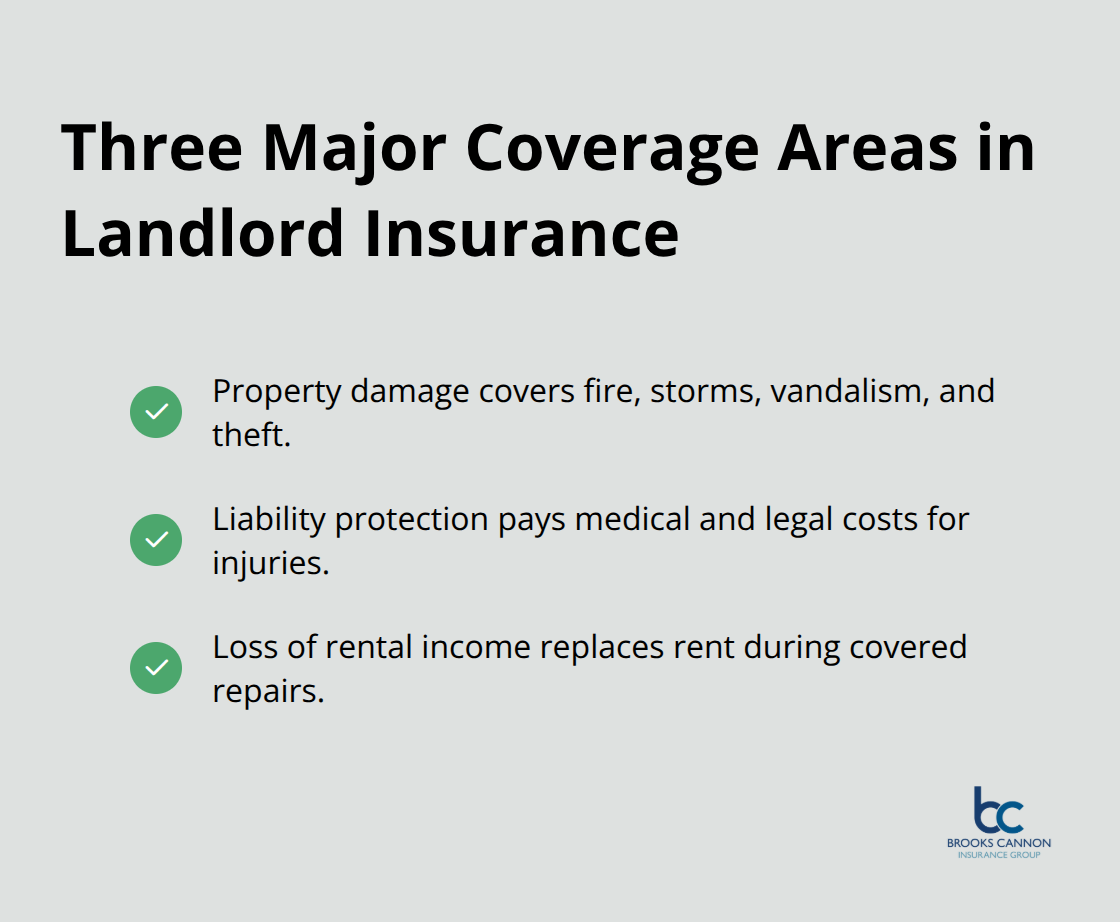

What Landlord Insurance Covers

Landlord insurance protects your rental property through three major coverage areas that homeowners insurance completely ignores. Property damage coverage handles destruction from fire, storms, vandalism, and theft, with dwelling protection typically covering 100% of your property’s replacement cost. Texas landlords face significant weather risks, with the state experiencing federally declared disasters beginning in 1953 according to FEMA records, making this coverage essential for Dallas area properties.

Property Structure and Contents Protection

Your policy covers the building structure, permanently attached fixtures, and any appliances you provide to tenants. Most carriers include coverage for detached structures like garages or storage sheds up to 10% of your dwelling coverage limit (typically around $20,000 for a $200,000 property). Smart landlords also add coverage for loss of rental income, which pays your monthly rent for up to 12 months when covered damage makes your property uninhabitable.

Liability Coverage That Protects Your Assets

Liability protection covers medical expenses and legal costs when tenants or visitors get injured on your property. Standard policies provide $100,000 in coverage, but we recommend $500,000 minimum for rental properties due to higher lawsuit risks. This coverage also handles property damage claims if your tenant accidentally causes damage to neighboring properties, such as water damage from an overflowing bathtub.

Loss of Rental Income During Repairs

Loss of rental income coverage compensates you when covered damage forces tenants to vacate temporarily. This protection typically covers fair rental value for the time needed to complete repairs, usually capped at 12 months. Texas landlords pay an average of $2,919 annually for comprehensive coverage, but losing six months of rent on a $1,500 monthly property costs $9,000 in lost income alone (making this coverage pay for itself quickly).

These coverage areas work together to protect your investment, but landlord insurance differs significantly from standard homeowners policies in ways that many property owners don’t realize.

Key Differences Between Landlord and Homeowners Insurance

Homeowners insurance explicitly excludes rental activities and leaves property owners completely exposed to tenant-related risks and liability claims. Standard homeowners policies contain business exclusions that void coverage when you collect rent, which means a $50,000 fire damage claim gets denied simply because you rent the property. Insurance companies classify rental properties as commercial ventures that require specialized coverage, and homeowners policies cannot be modified to bridge this gap.

Coverage Gaps That Homeowners Policies Leave for Rental Properties

Homeowners insurance fails to address the unique risks that rental properties face daily. Standard policies exclude tenant damage, vandalism by renters, and malicious destruction of property. When tenants cause water damage by leaving faucets running or damage walls during move-out, homeowners insurance denies these claims entirely. Rental properties also face higher theft risks since multiple people have access to keys, yet homeowners policies price theft coverage based on single-family occupancy assumptions.

Higher Liability Limits Required for Investment Properties

Homeowners insurance typically provides $100,000 to $300,000 in liability coverage, but rental properties need minimum $500,000 protection due to higher lawsuit frequency. The median settlement in Texas is $12,281, though the average reaches $826,892 due to multi-million-dollar cases. Rental properties generate 40% more liability claims than owner-occupied homes according to Insurance Information Institute data, yet homeowners policies price liability based on personal residence risks only.

Additional Living Expenses Not Covered for Rental Properties

Homeowners insurance pays your temporary housing costs when covered damage displaces you, but this protection vanishes for rental properties since you don’t live there. Instead, landlord policies provide loss of rental income coverage that replaces your monthly rent payments during repairs. A typical Dallas rental that generates $1,800 monthly rent loses $10,800 during six months of storm repairs (money homeowners insurance will never reimburse). This coverage difference alone justifies the switch to proper landlord insurance.

The right property insurance policy requires careful evaluation of your specific property risks and coverage needs to protect your investment adequately.

How to Choose the Right Landlord Insurance Policy

Property location determines your insurance costs more than any other factor, with Dallas area landlords paying premiums that vary by $800 annually based on ZIP code alone. Urban properties in downtown Dallas average $1,800 in premiums while suburban properties in Plano or Frisco cost around $1,400 annually according to Texas Department of Insurance data. Coastal properties near Galveston face hurricane risks that push premiums to $2,500, but Dallas landlords benefit from lower weather-related risks that keep costs reasonable.

Property Risk Factors Impact Your Rates

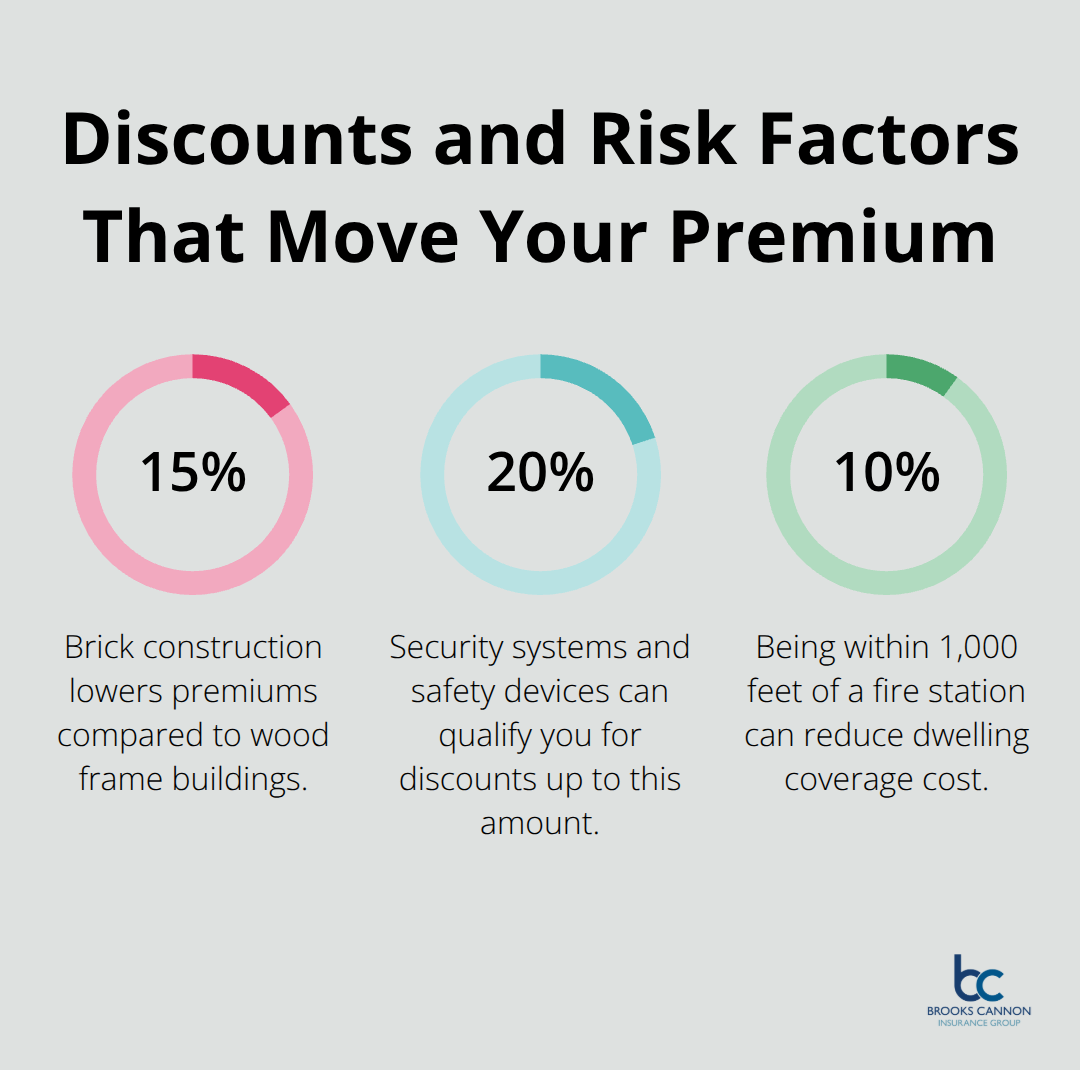

Age and construction type significantly impact your rates, with older properties having higher insurance rates due to outdated structural, electrical, and plumbing systems, which increase the risk of damage. Brick construction reduces premiums by 15% compared to wood frame buildings, while properties with security systems, smoke detectors, and burglar alarms qualify for discounts up to 20%. Swimming pools increase liability premiums by $300 annually, but properties within 1,000 feet of fire stations receive 10% discounts on dwelling coverage.

Calculate Coverage Amounts Properly

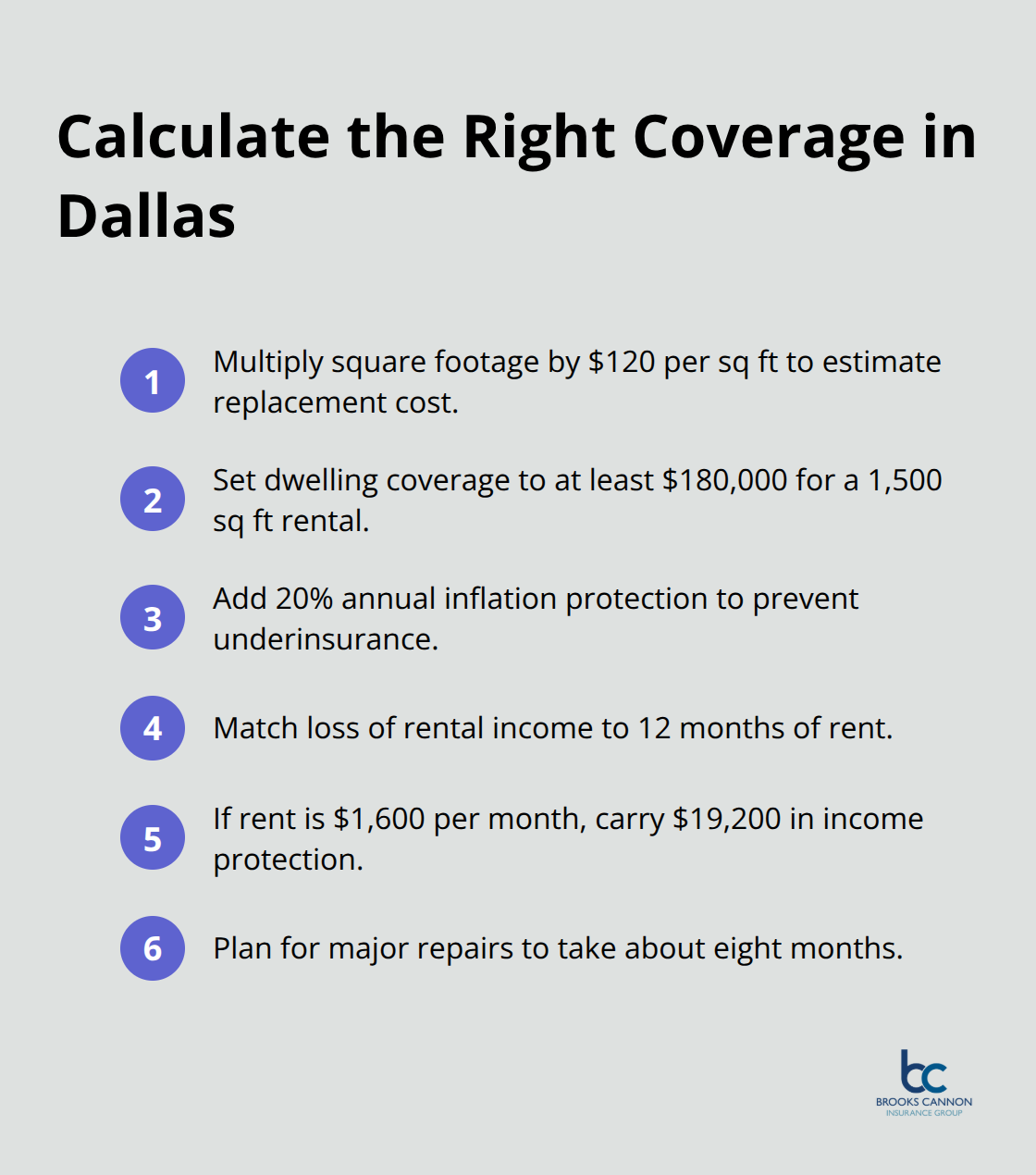

Calculate replacement cost when you multiply your property’s square footage by local construction costs, which average $120 per square foot in Dallas according to RSMeans construction data. A 1,500 square foot rental needs minimum $180,000 dwelling coverage, but inflation protection adds 20% annually to prevent underinsurance. Loss of rental income should equal 12 months of rent since major repairs average 8 months completion time (a $1,600 monthly rental requires $19,200 in income protection coverage).

Independent Agents Offer Better Options

Independent agents access 15-20 insurance carriers compared to captive agents who sell single company products, which results in savings that average $400 annually on landlord policies. We at Brooks Cannon Insurance Group compare rates from multiple A-rated carriers to find optimal coverage combinations that captive agents cannot offer. Request quotes with identical coverage limits from three independent agencies, then negotiate based on the lowest premium since coverage terms remain standardized across carriers.

Final Thoughts

Dallas rental property owners face financial risks that standard homeowners insurance won’t cover, which makes landlord insurance a necessity rather than an option. The average annual premium of $2,919 in Texas protects against losses that easily exceed $50,000 when property damage, liability claims, and lost rental income combine during a single incident. Without proper coverage, a tenant injury lawsuit that averages $826,892 in Texas could destroy your investment portfolio overnight.

Fire damage that requires six months of repairs costs $10,800 in lost rent alone on a $1,800 monthly property, while liability claims from slip-and-fall accidents start at $12,281 in median settlements. Smart landlords recognize that they pay $243 monthly for comprehensive protection that prevents catastrophic financial losses which could force property sales or bankruptcy. The math favors insurance coverage when potential losses exceed annual premiums by 1,000% or more (making the investment decision straightforward).

Quote requests take 15 minutes and comparison of options from multiple carriers saves an average of $400 annually. We at Brooks Cannon Insurance Group work with top-rated carriers to find competitive rates for Dallas area rental properties. Request quotes today to protect your investment before expensive surprises strike your bottom line.