Construction projects in the Dallas area face real financial risks from weather, theft, and equipment damage. New build project coverage through builders risk insurance protects your investment from day one.

At Brooks Cannon Insurance Group, we help builders and property owners understand why this protection matters. Without it, a single storm or theft can derail your timeline and drain your budget.

What Builders Risk Insurance Actually Covers

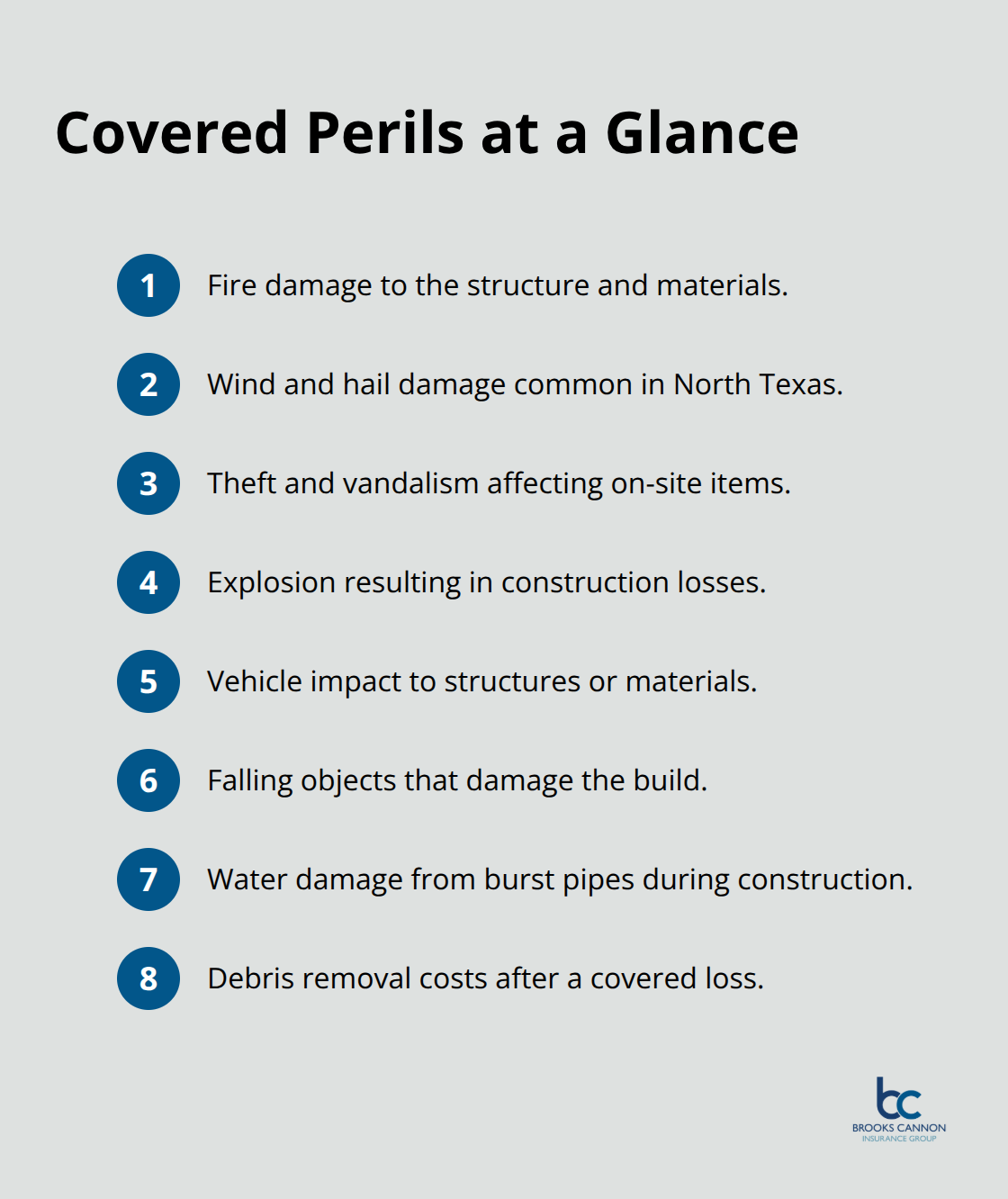

Builders risk insurance protects the physical assets on your construction site from the moment materials arrive until the project reaches completion. The policy covers the structure itself, all building materials stored on-site or in transit, fixtures permanently installed during construction, and equipment like scaffolding or temporary trailers. In Dallas, where North Texas sits in Hail Alley with tornadoes recorded in the region according to NOAA data, this coverage proves especially valuable. A single 2023 Texas storm caused over $500 million in construction-related damages, demonstrating how quickly weather can devastate an uninsured project. Standard builders risk policies include fire, wind and hail damage, theft and vandalism, explosion, vehicle impact, falling objects, and water damage from burst pipes.

The policy also covers debris removal after a covered loss, which can cost anywhere from $10,000 to well over $100,000 after a catastrophic event.

Materials in Transit and Off-Site Storage

Materials in transit receive full protection under builders risk coverage, whether they travel from a supplier to your job site or sit temporarily at off-site storage in approved locations. Theft during transport or at off-site storage can derail your schedule and budget, making this protection essential. Security measures typically required to qualify for theft claims include perimeter fencing, locked gates and storage, adequate lighting, security cameras, and inventory documentation. Failure to maintain these safeguards allows insurers to deny or reduce your claim. One critical detail: employee theft does not receive coverage under standard builders risk policies. If internal theft concerns you, add a separate crime or fidelity bond to your protection plan.

Soft Costs and Delay Coverage

Soft costs coverage, available as an optional add-on, reimburses indirect expenses caused by delays, such as redesign fees, permit and inspection costs, extended loan interest, and delayed openings. This coverage protects your bottom line when a covered loss extends your timeline. Without soft costs protection, you absorb these expenses out of pocket, which can significantly impact project profitability.

Structures and Temporary Installations

The coverage extends to the entire structure under construction, from foundation through framing to final installations. Temporary structures like construction trailers, fencing, and scaffolding receive protection, safeguarding your operational infrastructure during the build. For remodeling projects, you can choose whether to include the existing structure in coverage or exclude it, depending on your project needs. Installation projects with limited scope, such as adding cabinets or flooring to an existing space, also qualify for builders risk protection. Most policies run for 3 months for small renovations, 6 months for residential projects, and 12 months for larger commercial projects. If your project extends beyond the initial timeline, contact your insurer at least 30 days before the policy expires to avoid coverage gaps.

Understanding what your policy covers sets the foundation for protecting your investment. The next step involves recognizing why this protection matters so much for Dallas-area construction projects and how it safeguards you against the specific risks your build will face.

Why Builders Risk Insurance Protects Your Bottom Line

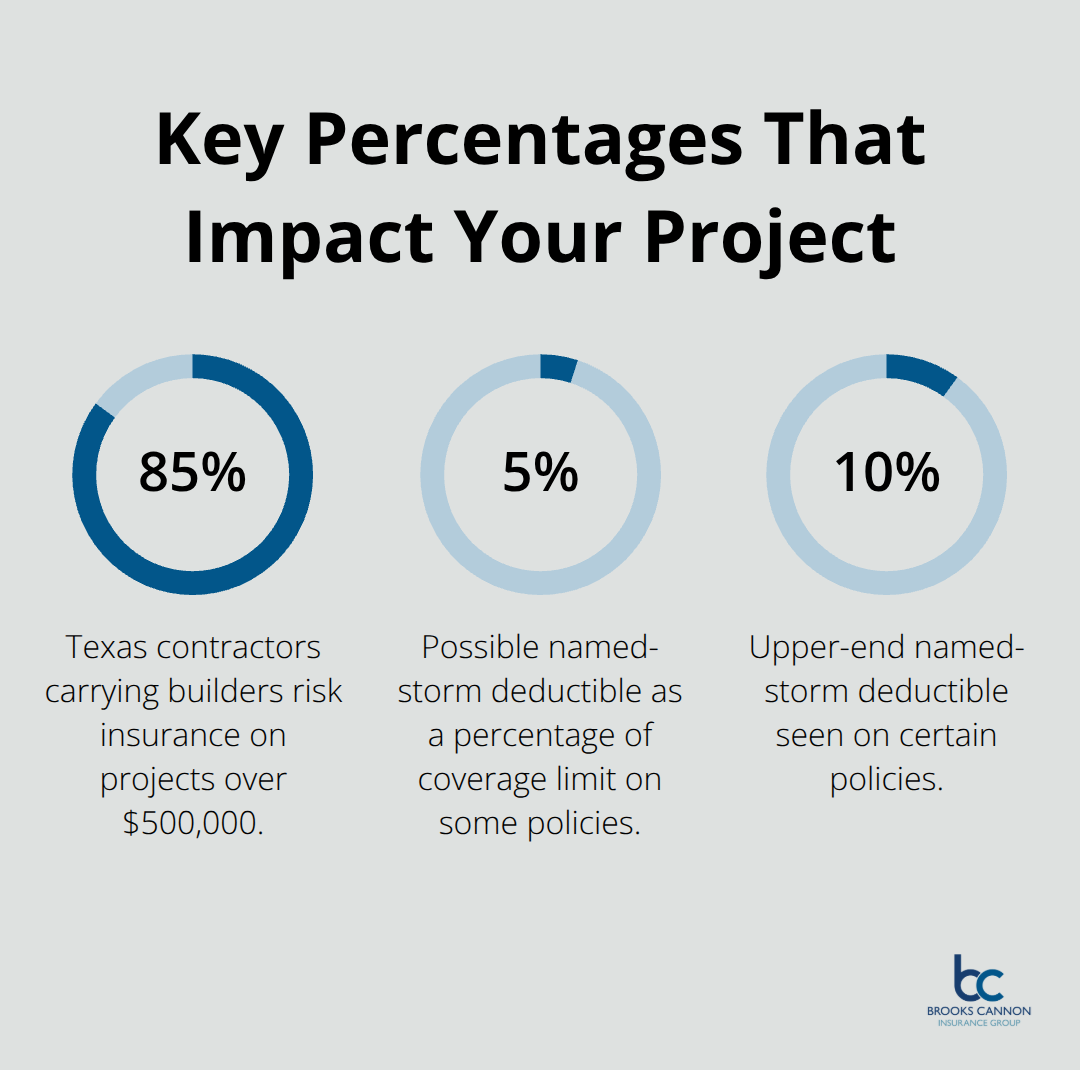

Dallas-area construction projects operate in an environment where financial losses happen fast. North Texas experiences severe weather regularly, with 118 tornadoes recorded across Texas in 2023 alone according to NOAA data. The region sits in Hail Alley, making hail damage a constant threat to job sites. Beyond weather, theft and vandalism drain budgets on active construction sites where materials and equipment sit exposed. According to the Associated General Contractors of America’s Texas chapter, 85% of Texas contractors carry builders risk insurance for projects exceeding $500,000, and for good reason. Without this protection, a single weather event or theft forces you to absorb thousands in replacement costs while your project stalls.

Lenders view builders risk coverage as non-negotiable. Most banks and financing institutions require proof of active coverage before releasing construction funds, making this policy a gateway to project financing in Dallas. Your construction contract likely specifies who carries the insurance responsibility, but either way, the coverage protects the actual assets your project depends on.

Weather Creates Real Financial Exposure

A 2023 Texas storm caused over $500 million in construction-related damages, illustrating how one event can devastate an uninsured project. In Dallas, wind and hail represent your biggest weather threats. Standard builders risk policies cover fire, wind and hail damage, explosion, vehicle impact, and water damage from burst pipes. However, deductibles for named storms vary significantly across carriers, and some policies impose separate wind deductibles that can reach 5% to 10% of the coverage limit. This matters because a $1 million project with a 10% wind deductible leaves you responsible for $100,000 before coverage kicks in. When comparing policies, examine the wind and hail deductible structure carefully. Some carriers offer lower deductibles in exchange for slightly higher premiums, which often makes financial sense for Dallas projects given the frequency of severe weather. Debris removal alone can cost $10,000 to well over $100,000 after a catastrophic loss, and builders risk covers this expense, preventing a secondary financial shock after the initial damage.

Theft and Vandalism Demand Active Security

Construction sites attract thieves because materials and equipment have immediate resale value. Theft coverage under builders risk protects on-site materials, fixtures, items in transit, and equipment stored at approved off-site locations. However, insurers require specific security measures to approve theft claims. Perimeter fencing, locked gates and storage, adequate lighting, security cameras, and inventory documentation are standard requirements. Failure to maintain these safeguards gives the insurer grounds to deny or reduce your claim, even if theft occurs. This means your security spending directly impacts your ability to recover losses. One critical exclusion: employee theft receives no coverage under standard builders risk policies. If internal theft concerns you, add a separate crime or fidelity bond to your insurance program. This distinction matters because contractor crews sometimes steal materials for side jobs, and discovering this loss without proper coverage creates an uninsured gap.

Lender Requirements Shape Your Coverage Decisions

Most construction lenders require active builders risk insurance before they release funds to your project. This requirement protects the lender’s financial interest in your build, but it also protects you by forcing a conversation about adequate coverage limits. Your lender will specify minimum coverage amounts and may require that the lender be named as a loss payee on the policy. These requirements vary by lender and project size, so coordinate with your bank early in the planning process. When a lender mandates coverage, the policy becomes a contractual obligation, not just a prudent business decision. This means you cannot cancel or reduce coverage without the lender’s written consent, which actually works in your favor by preventing gaps in protection during the construction period.

Comparing Deductibles Across Carriers Matters

Deductible selection directly impacts your out-of-pocket exposure when a loss occurs. Standard deductibles typically range from $500 to $2,500 for general perils, but named storm deductibles (wind and hail in Dallas) can reach 5% to 10% of your coverage limit. A higher deductible lowers your premium but increases your financial risk if damage occurs. A lower deductible costs more upfront but provides better protection when weather strikes. For Dallas projects, try selecting a deductible structure that balances premium costs against the likelihood of severe weather claims. Some carriers offer tiered deductibles where you pay one amount for general perils and a higher percentage for named storms. Understanding this structure before you purchase prevents surprises when you file a claim. The right deductible choice depends on your project budget, your risk tolerance, and your lender’s requirements.

Understanding these financial protections sets the stage for the next critical decision: selecting the right policy and carrier for your specific project needs.

Selecting Your Project’s Coverage Based on Real Numbers

Calculate Your True Project Value

Start by calculating your actual project value, not an estimate you hope holds true. The coinsurance clause in builders risk policies penalizes undervaluation severely. If your project is worth $2 million and you insure it for only $1.5 million, a $500,000 loss might result in a claim payout of just $333,000 instead of the full amount because you failed to insure to value. Contractors and property owners often underestimate project costs to reduce premiums, but this strategy backfires when losses occur. Add 10 to 15 percent to your material and labor estimates to account for price fluctuations and unforeseen expenses, then use that higher number as your coverage limit. This conservative approach protects you from coinsurance penalties that can cost far more than the premium savings you sought.

Lock Down Your Project Timeline

Identify your project timeline precisely. A 3-month renovation runs on a standard short-term policy, while a 12-month commercial build requires different underwriting and may qualify for better rates through a full-year commitment. If your timeline is uncertain, select longer coverage rather than shorter, because extending coverage requires 30 days’ notice to your insurer and creates gaps if you miss that deadline. Document when materials first arrive and when you expect final occupancy or certificate of completion, since coverage begins at material arrival and ends at occupancy, not at your preferred endpoint. This documentation prevents disputes with your insurer about when coverage actually applied to your project.

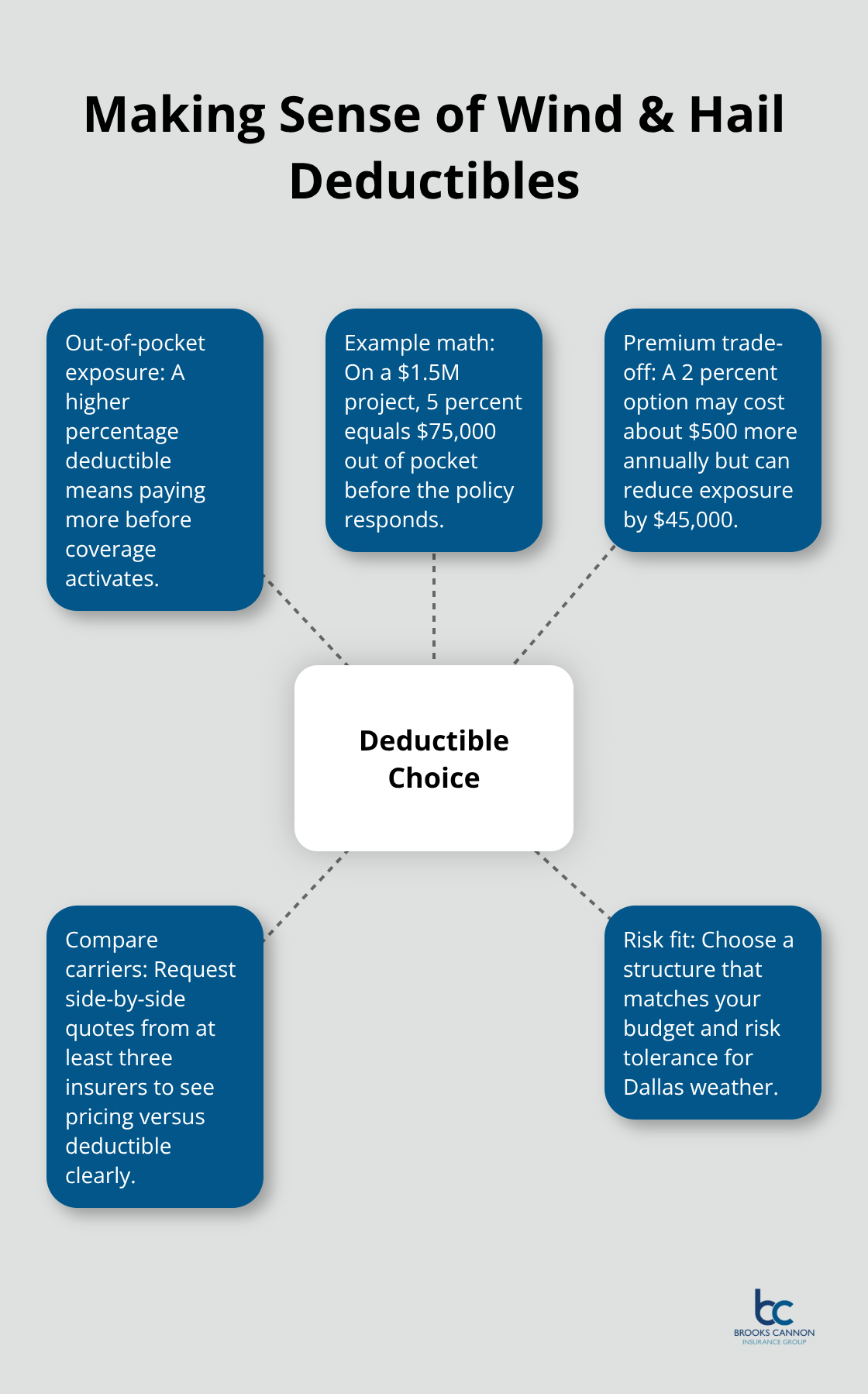

Compare Wind and Hail Deductibles Across Carriers

Wind and hail deductibles determine your actual out-of-pocket exposure during Dallas construction. A $1.5 million project with a 5 percent named storm deductible leaves you responsible for $75,000 before coverage activates, while a carrier offering a 2 percent deductible might cost an extra $500 annually but saves you $45,000 in potential exposure. Calculate whether the premium difference justifies the deductible difference for your specific risk tolerance and project budget.

Many carriers offer online quote tools that show premium and deductible combinations side by side, allowing you to see the trade-off clearly. Request quotes from at least three carriers to establish market pricing, because builders risk premiums vary significantly based on how each insurer views construction risk in your specific Dallas location and project type.

Work with an Agent to Verify Coverage Details

An independent insurance agent who understands Dallas construction reviews your specific contract requirements, identifies whether your lender has mandated coverage provisions, and confirms that all parties who need protection actually receive it. Subcontractors must be listed as additional insureds under your primary policy, and your agent verifies this endorsement exists before your project starts. If your project involves equipment breakdown, testing during startup, or expensive permanently installed machinery, your agent adds these endorsements rather than leaving gaps that create uninsured losses later. Request that your agent provide a detailed policy summary highlighting exactly what your coverage includes, what deductibles apply to each peril, and which exclusions affect your project. Ask whether flood or earthquake coverage can be added through endorsements, since standard policies exclude these perils in most cases. Confirm that soft costs coverage is included if your project financing depends on timely completion, because a weather delay without soft costs protection forces you to absorb redesign fees and extended loan interest personally.

Bind Coverage Before Materials Arrive

Bind coverage at least one week before materials arrive at the job site, giving yourself a buffer in case underwriting questions arise. Same-day or next-day binding is common for straightforward projects, but complex builds may require additional underwriting time. This advance timing prevents coverage gaps that could leave your materials unprotected during the critical early stages of your project.

Final Thoughts

Builders risk insurance stands between your Dallas construction project and financial disaster. When weather strikes North Texas or theft targets your materials, this coverage absorbs the costs that would otherwise drain your budget and delay completion. New build project coverage protects the structure, materials, equipment, and temporary installations your project depends on from day one through final occupancy.

A single hail storm can cost $500,000 or more in repairs and debris removal, while theft of materials and equipment can halt your schedule for weeks. Extended loan interest, redesign fees, and permit costs pile up during delays caused by covered losses, and builders risk coverage prevents these scenarios from becoming your financial burden. Proper coverage also satisfies your lender’s requirements, which means you cannot access construction financing without it.

At Brooks Cannon Insurance Group, we work with multiple top-rated carriers to find the coverage and pricing that matches your specific project needs. Our licensed experts review your contract requirements, verify that all parties receive proper protection, and confirm that your coverage limits account for material price increases and unforeseen expenses. Contact us today to discuss your new build project coverage and secure the protection your Dallas construction project requires.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation