Cyber attacks hit businesses every 39 seconds, making digital protection more important than ever. What is cyber liability insurance? It’s specialized coverage that protects your business from the financial devastation of data breaches and cyber crimes.

We at Brooks Cannon Insurance Group see Dallas businesses facing increasing cyber threats daily. Traditional insurance policies leave massive gaps in cyber protection, putting your company at serious financial risk.

What Does Cyber Liability Insurance Actually Cover

Cyber liability insurance protects your business when digital disasters strike, covering three major areas that traditional policies ignore. Data breach coverage handles the immediate costs when hackers steal customer information, including notification expenses that average $740,000 for mid-sized companies according to IBM research. The policy covers forensic investigations, credit monitoring for affected customers, and legal fees from class-action lawsuits.

Business Interruption and Revenue Protection

Business interruption protection kicks in when cyber attacks shut down your operations, replacing lost income and covering extra expenses to restore normal business functions. A ransomware attack that paralyzes your systems for just three days can cost a Dallas business over $200,000 in lost revenue alone. The policy compensates for income you lose while systems remain offline and pays for temporary workarounds that keep operations running.

Legal Defense Against Mounting Cyber Claims

Regulatory fines represent the fastest-growing cyber expense, with Texas businesses facing significant penalties under state privacy laws when they violate the Texas Data Privacy and Security Act. Your cyber policy covers defense costs against regulatory investigations and civil lawsuits from customers whose data was compromised. The policy also handles crisis management expenses, including public relations support to protect your reputation after a breach (without this coverage, legal defense costs alone can exceed $500,000 for a single data breach incident).

Network Security Failure Protection

System damage repair coverage addresses the technical costs of rebuilding compromised networks and recovering corrupted data. This includes hiring cybersecurity experts to identify vulnerabilities, restore infected systems, and implement stronger security measures. The policy covers ransom payments when businesses face legitimate threats, though payment decisions require careful consideration of FBI recommendations against encouraging criminal activity.

These comprehensive protections become even more valuable when you consider the rising frequency of cyber attacks targeting businesses across all industries.

Why Dallas Businesses Face Mounting Cyber Risks

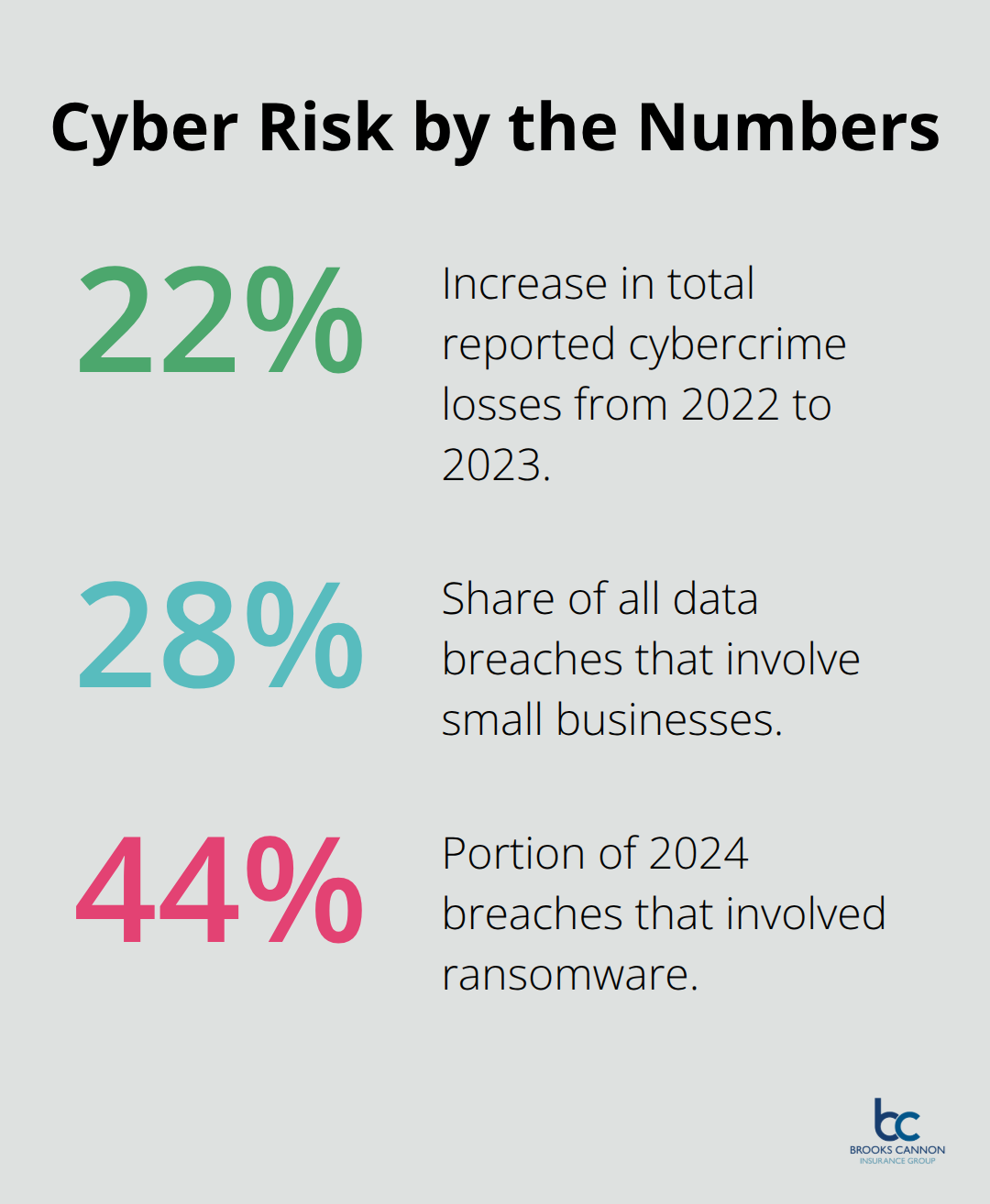

The FBI recorded over 880,000 cybercrime complaints in 2023, with total losses that exceeded $12.5 billion (a 22% increase from 2022). Dallas businesses face particularly severe exposure as Texas ranked third nationally for cybercrime victims and second for financial losses at $115.7 million in 2017. Small businesses account for 28% of all data breaches according to recent studies, yet most owners mistakenly believe their general liability policies provide adequate cyber protection.

General Liability Policies Leave Massive Gaps

Traditional general liability insurance excludes digital risks entirely, which leaves businesses exposed to the average $3.86 million global cost of data breaches. Healthcare companies face even steeper costs at $10.1 million per incident, while U.S. businesses average $9.44 million in breach expenses according to IBM research. Your standard business policy covers physical property damage and bodily injury claims but provides zero protection against ransomware attacks, data theft, or regulatory fines from privacy violations.

Regulatory Penalties Create New Financial Threats

The Department of Justice Civil Cyber Fraud Initiative now targets federal contractors for cybersecurity failures, while state regulations impose heavy penalties on businesses that mishandle customer data. Companies face pressure from class-action lawsuits, with plaintiff attorneys who increasingly target businesses after data breaches. The average breach takes 280 days to identify and resolve, which creates extended periods of legal vulnerability that general liability policies simply do not address.

Attack Frequency Demands Specialized Protection

Ransomware attacks occurred in 44% of all breaches during 2024, with healthcare sectors that experienced the highest incident rates. Identity fraud alone caused $23 billion in losses last year, which demonstrates how cybercriminals target both businesses and their customers simultaneously. Without specialized cyber coverage, Dallas businesses risk complete financial devastation from attacks that traditional insurance policies treat as uninsurable digital events.

These coverage gaps become even more apparent when you examine the specific protections that comprehensive cyber liability policies provide across different risk categories.

What Coverage Components Make Cyber Insurance Effective

Cyber liability policies divide protection into first-party coverage for direct losses your business suffers and third-party coverage for claims others file against you. First-party coverage handles immediate expenses like forensic investigations, data recovery expenses, and business interruption losses during system downtime. This coverage also pays for customer notification costs plus credit monitoring services for affected individuals.

Third-party coverage protects against lawsuits from customers, vendors, or business partners whose data was compromised. The policy covers legal defense costs and settlement payments that can reach millions (depending on the breach scope).

Crisis Management Prevents Reputation Damage

Professional crisis management services activate immediately after a breach, with specialized teams that coordinate media responses and customer communications to minimize reputation damage. These services include public relations experts who craft message strategies, legal advisors who handle regulatory communications, and technical consultants who work with law enforcement agencies.

The coverage pays for emergency response teams available 24/7, social media monitoring to track reputation impacts, and executive coaching to prepare leadership for media interviews. Without this coordinated response, businesses face significant customer loss after a data breach according to recent industry studies. Crisis management coverage typically costs just 5-10% of total policy premiums but prevents reputation losses that can exceed the original breach costs significantly.

Policy Limits Determine Real Protection

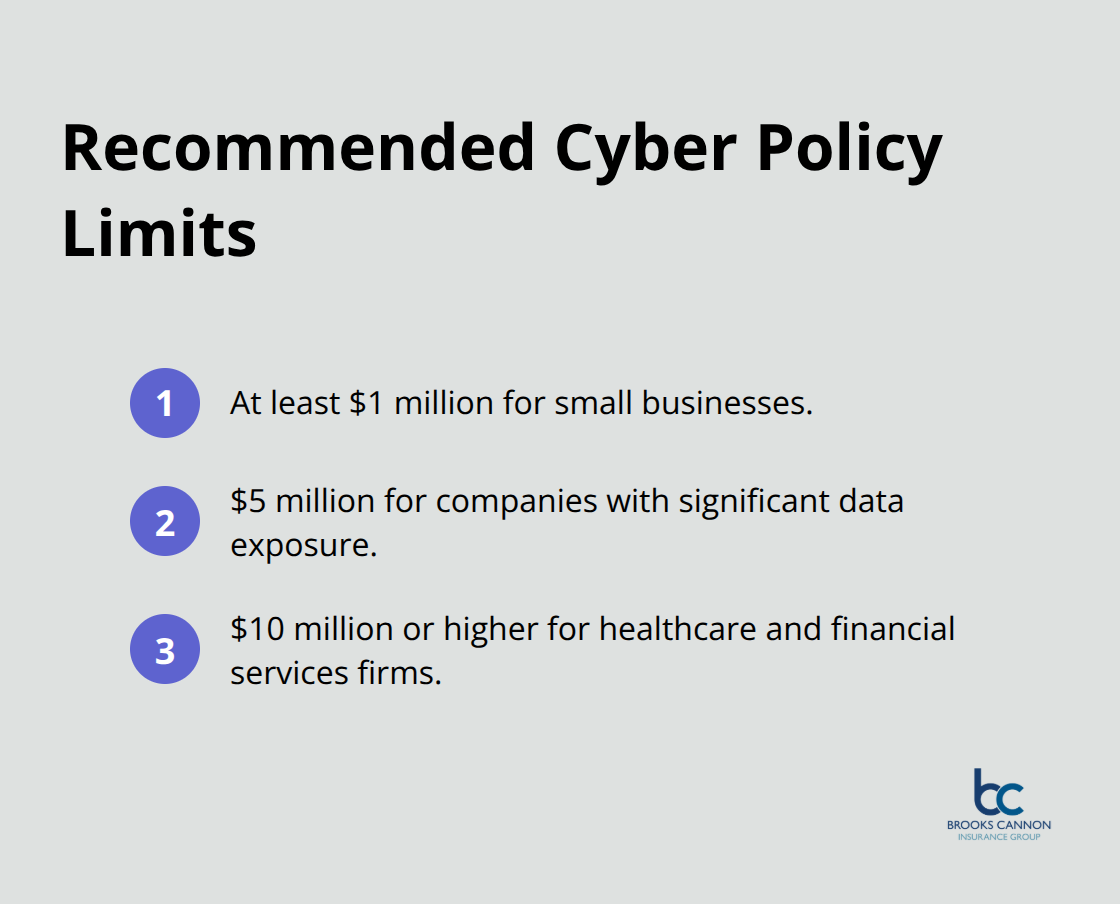

Most Dallas businesses underestimate their cyber exposure and purchase inadequate coverage limits that leave them vulnerable to catastrophic losses. Effective cyber policies require minimum limits of $1 million for small businesses and $5 million for companies with significant data exposure (though healthcare and financial services firms need $10 million or higher).

The policy structure should include separate limits for different coverage types rather than shared limits across all protections, which can exhaust coverage quickly during major incidents. Businesses that choose shared limits often discover their coverage disappears after the first major expense category gets paid.

Final Thoughts

The cyber insurance market will reach $29 billion by 2027, which reflects how digital threats now pose existential risks to businesses of all sizes. What is cyber liability insurance transforms from a question into a necessity when data breaches affect nearly 350 million victims annually. Costs average $9.44 million per incident in the United States, making protection essential for business survival.

Smart business owners recognize cyber insurance as their most cost-effective risk management strategy. The average policy costs significantly less than a single day of business interruption from a ransomware attack. Dallas businesses that invest in comprehensive cyber protection position themselves to survive attacks that destroy unprepared competitors.

The right coverage starts with honest assessment of your digital exposure and data practices (work with experienced agents who understand both cyber risks and policy differences between carriers). We at Brooks Cannon Insurance Group help Dallas businesses navigate complex cyber insurance markets to find coverage that matches their specific risk profiles. The question isn’t whether cyber attacks will target your business, but whether you’ll have adequate protection when they strike through comprehensive cyber liability coverage.