Construction projects in Texas face unique weather challenges, from hail storms to high winds, that can devastate unprotected buildings and materials. Builders risk insurance in Texas is your financial safeguard against these losses during the construction phase.

At Brooks Cannon Insurance Group, we help contractors and builders understand exactly what this coverage protects and why it matters for your bottom line. Getting the right policy in place before breaking ground can save you thousands in unexpected costs.

Understanding Builders Risk Coverage

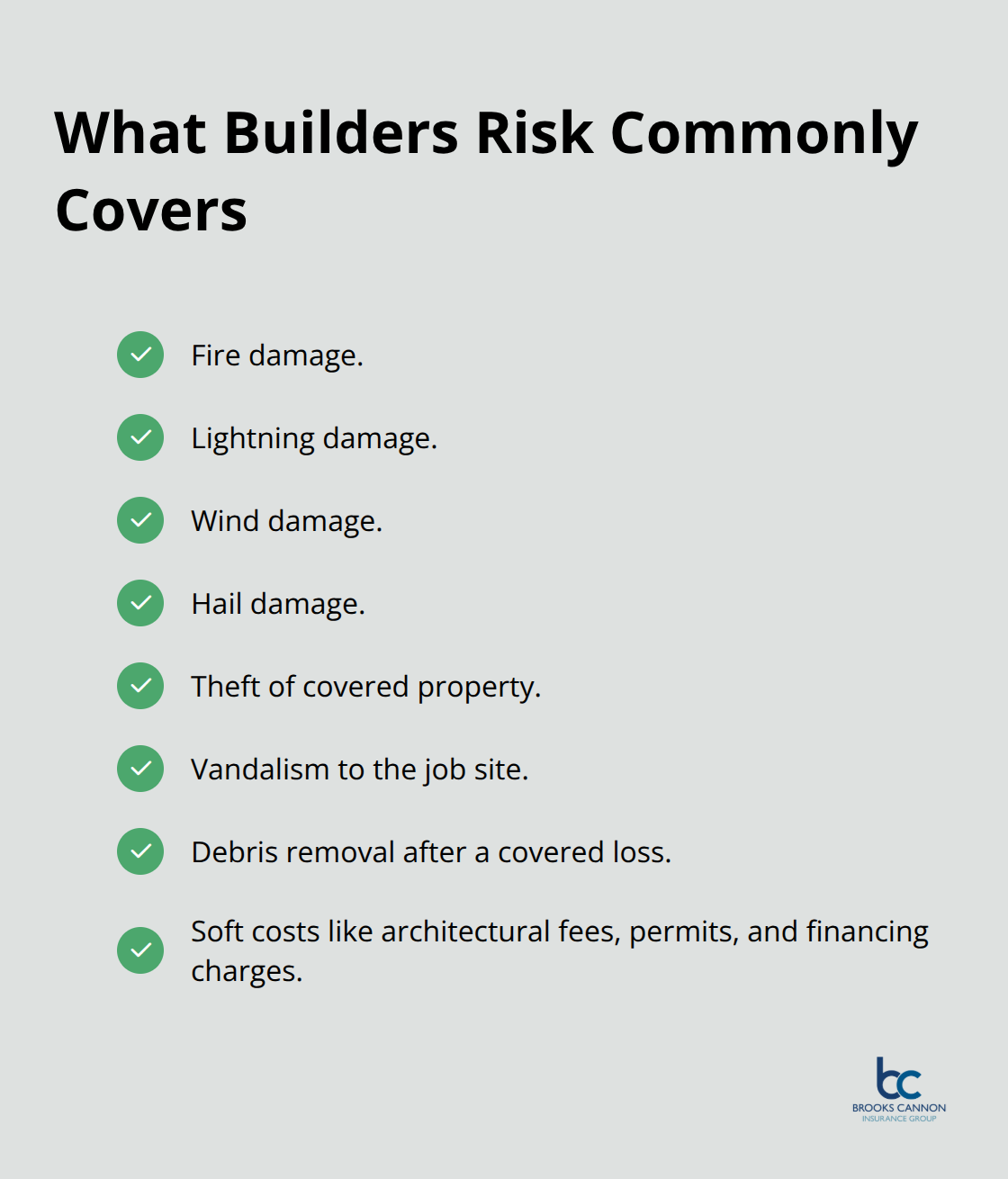

Builders risk insurance protects your construction project from property damage during the building phase. Unlike general liability insurance, which covers injuries or damage you cause to others, builders risk covers damage to the structure itself, materials, equipment, and tools on your job site. The Texas Comptroller’s Office reported that construction contributed about $200 billion to the state economy in 2023, which means thousands of projects face risk every year. This coverage is temporary-it lasts only during construction and ends when the project is complete. You can extend it if delays push your timeline beyond the original schedule. The policy covers fire, lightning, wind, hail, theft, and vandalism. It also includes debris removal costs after a covered loss, which can run into thousands of dollars on larger projects. Many policies add soft costs coverage, which reimburses architectural fees, permits, and additional financing charges if a covered event delays your project.

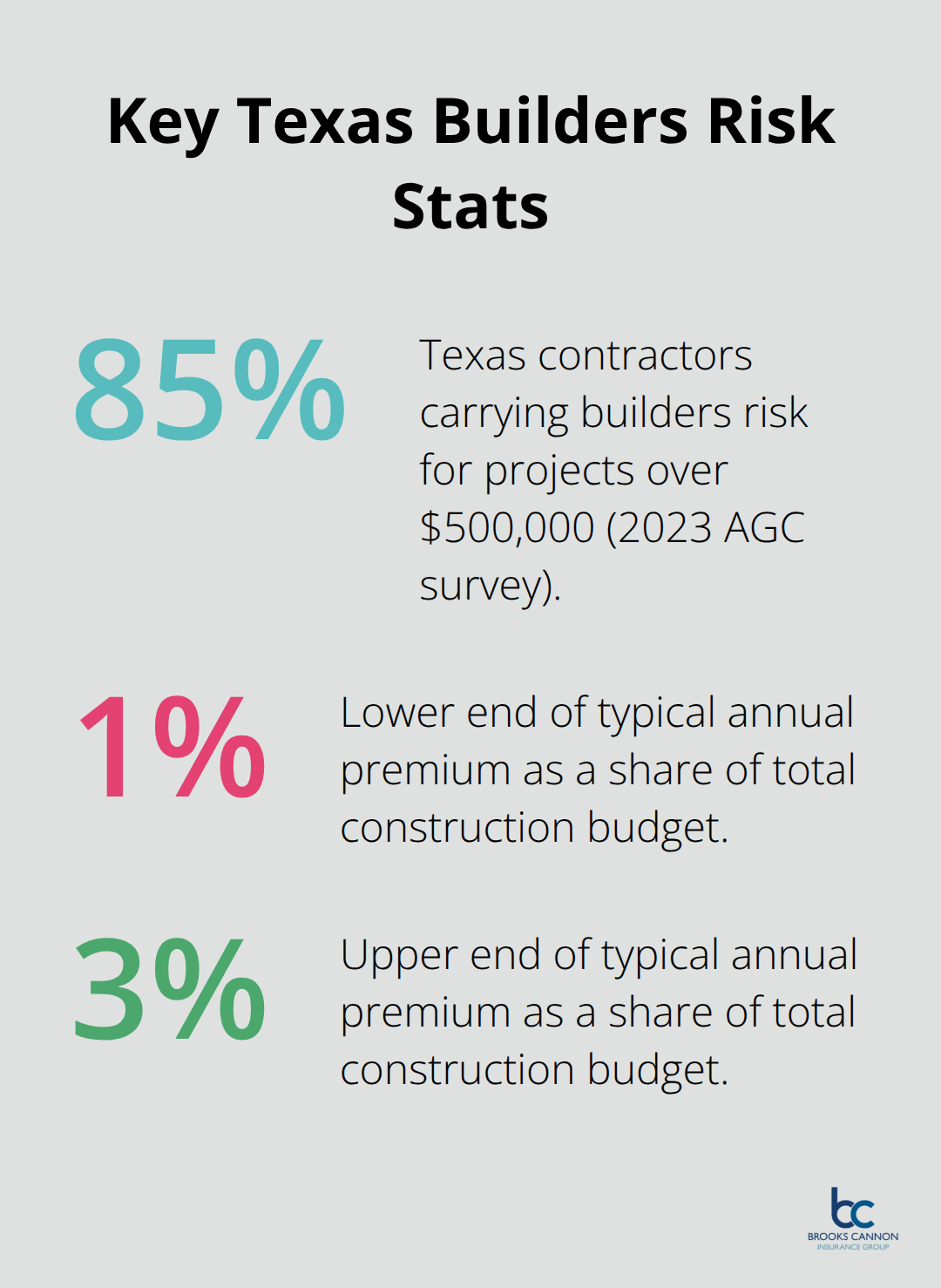

Standard deductibles range from $500 to $5,000, and premiums typically run 1 to 3 percent of your total construction budget-so a $1 million project would cost roughly $10,000 to $30,000 per year for coverage.

Texas Weather Demands Extra Protection

Texas faces serious weather threats that directly impact construction sites. NOAA recorded 118 tornadoes in Texas in 2023 alone, and the state’s coastal regions face hurricane risk annually. Hail storms destroy roofing materials, windows, and HVAC systems before installation. High winds topple cranes, blow away framing, and scatter materials across neighboring properties. Climate change impacts push builders risk premiums higher than many other states. If your project sits near flood zones or the Gulf Coast, standard builders risk excludes flood damage-you’ll need a separate flood endorsement. Windstorm coverage protects against the specific perils that damage Texas construction sites most frequently and costs extra but proves essential for coastal projects. Your lender will likely require coverage that addresses these regional risks before approving your construction loan.

Why Lenders and Contracts Demand This Coverage

A 2023 survey by the Associated General Contractors of America found that 85 percent of Texas contractors carry builders risk for projects over $500,000. That’s not coincidence-lenders require it. Banks won’t fund construction without proof that the building and materials are protected.

Your construction contract probably already mandates this coverage, which means you need it before you can legally break ground. When you apply for a construction loan, the lender becomes a named insured on your policy, protecting their financial interest in the project. This requirement exists because uninsured losses can sink projects financially and leave lenders holding the bag. Standard exclusions in builders risk policies include employee theft, normal wear and tear, poor workmanship, and damage from faulty design. Earthquakes and floods are excluded unless you add them as endorsements. Reviewing these exclusions carefully prevents gaps in coverage after a loss occurs.

What Happens When You Skip This Coverage

Construction projects without builders risk insurance face serious financial exposure. A single weather event can halt work for weeks, pushing your timeline back and triggering additional labor costs, equipment rentals, and financing charges. Materials stolen from an unprotected site represent a total loss with no recovery. Debris removal after fire or wind damage costs thousands and falls on you without coverage. Lenders will simply refuse to advance funds if you lack proof of protection, which means your project stalls before it starts. The cost of builders risk insurance (typically 1 to 3 percent of your construction budget) is far less than the cost of a single major loss or project delay.

What Builders Risk Actually Covers on Your Job Site

The Three Core Protection Categories

Builders risk insurance protects three distinct categories of property during construction, and understanding exactly what falls into each one prevents costly gaps when a loss occurs. The policy covers the building structure itself, which includes framing, roofing, windows, doors, mechanical systems being installed, and any permanent fixtures attached to the building. It also covers materials and equipment staged on-site, whether stacked in piles, stored in temporary structures, or positioned for immediate use. Transit coverage extends protection to materials moving from suppliers to your job site, which matters significantly in Texas where theft from delivery trucks and job sites runs high.

Materials in Motion and Soft Costs Protection

Texas consistently ranks among the top five for construction equipment theft incidents. Transit coverage activates the moment materials leave the supplier’s facility and continues until workers unload them at your site. Soft costs coverage reimburses indirect expenses when a covered event delays your project-architectural fees, permit costs, additional financing charges from your construction lender, and bond interest all qualify. A contractor working on a $2 million commercial project in Dallas faces $15,000 to $25,000 in monthly financing charges alone if weather delays the timeline by 30 days. That’s where soft costs coverage becomes essential rather than optional.

Deductibles and Debris Removal

Standard deductibles of $500 to $5,000 mean you absorb small losses yourself, but the policy activates for anything exceeding your chosen deductible amount. Debris removal coverage handles cleanup expenses after fire, wind, or other covered damage-costs that frequently reach $50,000 or more on mid-sized projects. This coverage prevents unexpected cleanup bills from derailing your budget after a loss.

What Standard Policies Exclude

Standard builders risk policies explicitly exclude several important exposures that catch contractors off guard. Employee theft is never covered, which means tools and equipment disappearing inside your secure fence remain your responsibility entirely. Normal wear and tear, rust, corrosion, and mechanical breakdowns fall outside coverage because they result from age and use rather than sudden, unexpected damage. Damage caused by faulty design or poor workmanship is excluded because design flaws and construction mistakes belong to the contractor’s liability rather than property coverage.

Regional Exclusions and Subcontractor Equipment

Flood damage is completely excluded from standard policies in Texas, which creates serious exposure for projects near rivers, low-lying areas, or FEMA flood zones-you must purchase a separate flood endorsement to cover these properties. Earthquakes are also excluded unless specifically added. Employee injuries or worker compensation claims are not covered by builders risk; those belong under workers compensation insurance. The policy does not cover tools and equipment that belong to subcontractors-their own policies should protect their property. Understanding these exclusions before a loss occurs allows you to purchase additional endorsements that address your specific project risks. For a Dallas area project near flood-prone zones or one involving high-value equipment, adding flood coverage and equipment breakdown protection costs extra but eliminates potentially devastating exposure gaps. Once you understand what your policy covers and what it excludes, the next step involves selecting the right coverage limits and deductibles for your specific project.

How to Choose the Right Builders Risk Policy for Your Project

Calculate Your Coverage Limit Based on Actual Project Costs

The biggest mistake contractors make when selecting builders risk coverage is guessing at coverage limits instead of calculating them precisely. Your coverage limit must equal your total hard costs-the sum of all materials, labor, equipment rentals, and subcontractor fees for the project. A $2 million construction budget demands a $2 million coverage limit, not $1.5 million. Insurance companies will not pay more than your stated limit, so underestimating creates a gap that comes directly from your pocket when a loss occurs. The Insurance Information Institute notes that Texas weather hazards push builders risk premiums higher than most states, which tempts contractors to cut corners on limits to save on premiums. That’s backwards thinking. A $50,000 premium difference between a $1.5 million and $2 million limit is trivial compared to absorbing a $500,000 loss yourself because you were underinsured.

Coverage limits commonly run at 1 to 3 percent of total construction cost, but that percentage means nothing if your actual limit falls short of your actual exposure. You must match your limit to your real financial exposure, not to an industry average. Projects with tight budgets and high material costs need higher limits than projects with lower material intensity. Calculate your exact exposure, then select a limit that covers it completely.

Choose Your Deductible Based on Cash Flow Position

Deductible selection directly affects your monthly premium, so many contractors automatically select the highest deductible ($5,000) to minimize cost. That works only if your project has strong cash flow and you can absorb that amount after a loss. A $2,500 deductible costs roughly 10 to 15 percent more than a $5,000 deductible, but that extra cost protects you from unexpected out-of-pocket hits during construction. For projects running tight on working capital, the lower deductible makes financial sense. For larger commercial projects with deep reserves, a $5,000 deductible reduces annual premiums by $1,000 to $2,000. The math depends entirely on your project’s financial position and risk tolerance.

Soft costs coverage deserves separate attention because it’s optional but essential for any project where delays cost money. A 30-day weather delay on a $3 million commercial project triggers $30,000 to $50,000 in additional financing costs alone. Soft costs coverage reimburses those indirect expenses, and the endorsement typically costs $500 to $1,500 per year. That’s insurance you cannot afford to skip.

Request Quotes from Multiple Carriers

Pull quotes from three different insurance agents or carriers before committing to a policy. Premiums for identical coverage vary significantly across insurers because each carrier prices Texas construction risk differently based on their claims history and underwriting appetite. One carrier might quote $18,000 annually for your project while another quotes $22,000 for the same limits and deductibles. That $4,000 difference justifies the time spent gathering competitive bids. Independent agents work with multiple top-rated carriers and can pull quotes from five or six companies simultaneously, saving you hours of phone calls.

When requesting quotes, provide identical project details to each agent: exact construction budget, project location, start and completion dates, whether flood zones or coastal areas apply, and any specialized equipment or exposures. Apples-to-apples comparison reveals which carriers price your specific risk most competitively. Many insurers offer same-day quotes through online tools, but agent-assisted quotes often yield better pricing because experienced agents negotiate discounts that online systems don’t automatically apply.

Add Endorsements That Match Your Project Location

Standard builders risk excludes flood and earthquake damage, but Texas projects near FEMA flood zones absolutely require flood coverage endorsement. The cost ranges from $1,500 to $5,000 annually depending on flood risk designation, but a single flood event can destroy $500,000 in materials and equipment. Skipping flood coverage on a flood-prone project is financial recklessness. Windstorm coverage matters for any project within 50 miles of the Gulf Coast, where hurricanes and tropical storms create specific wind damage exposure that standard policies exclude.

Equipment breakdown coverage protects HVAC systems, generators, and mechanical equipment against internal damage during installation. For projects using expensive temporary structures like scaffolding or crane systems, verify your policy covers these items with adequate sublimits. Each endorsement costs extra, but each one closes a coverage gap that could otherwise devastate your project. The decision comes down to identifying which endorsements match your specific project location and exposures, then comparing their cost against the financial impact of remaining uninsured for those perils.

Final Thoughts

Builders risk insurance in Texas protects your construction investment from weather damage, theft, and unexpected delays that derail timelines and budgets. Lenders require it, contracts demand it, and the financial exposure without it exceeds what any contractor should accept. A single hail storm, tornado, or theft incident costs tens of thousands of dollars, and that’s before accounting for project delays that trigger additional financing charges and labor costs.

Match your coverage limit to your actual construction budget, select a deductible that fits your cash flow position, and add endorsements for flood and windstorm protection if your project location demands them. Request quotes from multiple carriers to compare pricing on identical coverage-independent agents pull quotes from several top-rated insurers simultaneously, saving you time and revealing significant premium differences for the same protection. Same-day quotes are available through most carriers, so you have no reason to delay this step until the last minute.

At Brooks Cannon Insurance Group, our team works with multiple top-rated carriers to find the best coverage and pricing for your specific project. We understand Texas construction risks, regional weather threats, and the endorsements that close coverage gaps. Contact us before your next project to discuss your builders risk insurance in Texas and secure the protection your investment requires.