![What Does General Liability Insurance Cover? [2025 Guide]](https://brookscannon.com/wp-content/uploads/emplibot/What-Does-General-Liability-Insurance-Cover_-_2025-Guide__1768626731-1080x675.jpeg)

General liability insurance is one of the most important protections a business can have, yet many owners don’t fully understand what does general liability insurance cover-or what it doesn’t.

At Brooks Cannon Insurance Group, we work with Dallas businesses every day who discover gaps in their coverage after a claim happens. That’s why we created this guide to walk you through exactly what’s protected and where you might have exposure.

The Three Core Protections in General Liability

General liability insurance protects your Dallas business in three main ways, and understanding each one helps you see why this coverage matters.

Bodily Injury Claims

Bodily injury claims cover medical expenses, lost wages, and legal judgments when someone is hurt on your property or because of your work. If a customer slips in your retail location and breaks their arm, or a contractor you hired damages a client’s home and injures them in the process, your policy steps in to cover their medical bills and any settlement or court judgment. The Insurance Information Institute reports that many Texas small businesses carry general liability coverage, yet some owners still operate without it-exposing themselves to attorney fees that run between $100 and $500 per hour according to Lawyers.com.

Property Damage Coverage

Property damage coverage pays for repairs or replacement when your work or operations damage someone else’s property. This applies whether you accidentally damage a client’s building during a renovation, or your delivery vehicle hits a parked car in a parking lot. Your policy covers the replacement cost without requiring the property owner to absorb the financial burden themselves.

Medical Payments to Others

Medical payments to others covers immediate medical expenses for injuries that happen at your business location, regardless of fault. A visitor who gets injured at your Dallas office doesn’t have to prove you were negligent to receive medical care coverage-your policy pays their treatment costs directly, which often prevents minor incidents from becoming expensive lawsuits.

Real-World Scenarios Where Coverage Applies

The real value of general liability insurance shows up in everyday business situations. A contractor damages a client’s custom cabinetry while installing new fixtures-your property damage coverage handles the replacement cost. A customer’s child is injured at your business event-medical payments coverage pays their emergency room visit without requiring a liability determination. An employee of your business is accused of making a defamatory comment about a competitor-your personal and advertising injury coverage addresses the claim.

Understanding Your Policy Limits

Texas businesses face commercial lawsuits regularly, and many of those claims involve property damage, bodily injury, or reputational harm that general liability policies cover. The per-occurrence and aggregate limits matter here-a typical policy might offer $1 million per occurrence and $2 million aggregate, meaning your coverage pays up to $1 million for each separate incident and up to $2 million total across all claims in a policy year. Once you understand what these limits cover, you can determine whether they match your actual risk exposure and whether you need additional protection through an umbrella policy or higher underlying limits.

What General Liability Insurance Doesn’t Protect

General liability insurance has clear boundaries, and knowing what falls outside your coverage is just as important as understanding what’s protected. Many Dallas business owners assume their general liability policy covers more than it actually does, which leads to costly gaps when claims arise. The reality is that your policy excludes entire categories of risk, and operating without the right supplemental coverage in those areas can expose you to six-figure losses.

Professional Errors and Mistakes

Professional errors and mistakes made by licensed professionals fall outside general liability coverage because they require errors and omissions insurance instead. If you work as a consultant, accountant, architect, or engineer and you provide faulty advice that costs a client money, your general liability policy won’t defend you or pay the claim. This gap affects thousands of Dallas professionals who operate without proper E&O protection.

Employee Injuries and Workers’ Compensation

Employee injuries fall outside general liability coverage entirely-those belong under workers’ compensation insurance. Texas makes workers’ compensation optional for most private employers, but that doesn’t mean the risk disappears. In 2024, Texas private sector employers reported about 156,000 non-fatal workplace injuries according to the Bureau of Labor Statistics, and if you don’t carry workers’ comp, an injured employee can sue you directly for unlimited damages. The financial exposure here far exceeds what most business owners anticipate.

Vehicle-Related Incidents

Vehicle-related incidents sit outside general liability because they require commercial auto insurance instead. A delivery driver hitting a pedestrian or damaging property while on company business isn’t covered by your general liability policy, even if the incident happens while performing job duties. Texas commercial auto liability minimums are 30/60/25 for business-owned vehicles (bodily injury per person $30,000, per accident $60,000, property damage $25,000), and many businesses also need hired and non-owned auto coverage for vehicles they don’t own but use for business purposes.

Intentional Acts and Criminal Behavior

Intentional acts and criminal behavior are never covered under general liability. If you or an employee deliberately damages someone’s property or intentionally causes harm, your insurance won’t step in, and you’ll face personal liability exposure. Dallas businesses need to recognize these gaps aren’t minor details-they’re substantial exposures that require separate policies or additional endorsements to address properly.

Understanding which coverage types protect each risk category helps you build a complete insurance strategy that actually matches your business operations.

Why General Liability Insurance Matters for Dallas Businesses

Contracts and Client Requirements Drive Coverage Demand

General liability insurance isn’t optional for most Dallas businesses-it’s the foundation of responsible risk management. Contracts, leases, and client agreements regularly demand proof of coverage before work starts. Without it, you’ll lose deals to competitors who have their coverage in place. Your clients and landlords aren’t asking for general liability insurance to be named as an additional insured on your certificate of insurance to be difficult-they’re protecting themselves and ensuring they have recourse if something goes wrong. Refusing to carry coverage doesn’t make you look tough; it makes you look unprepared and forces potential clients to work with someone else.

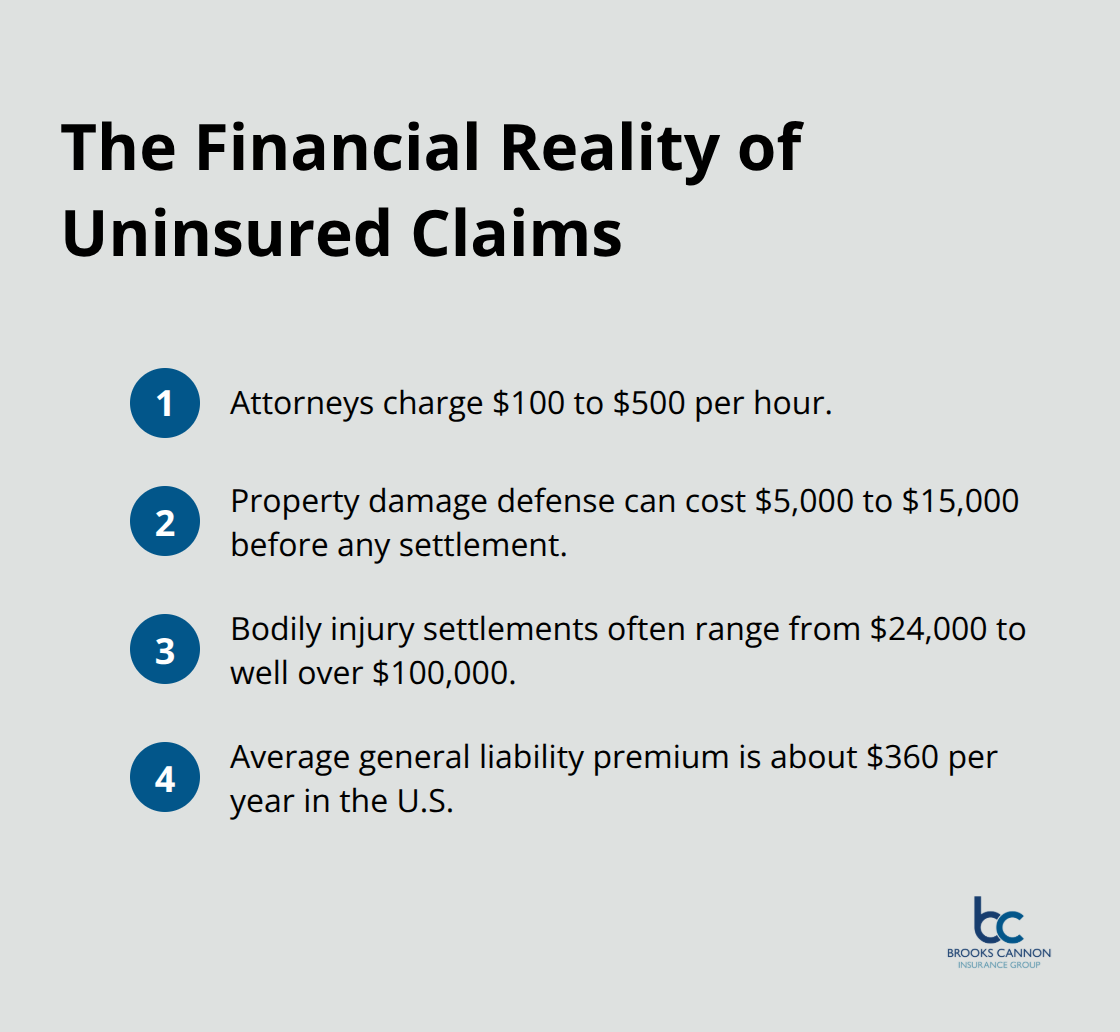

The Financial Reality of Uninsured Claims

A single lawsuit can devastate a business that operates uninsured. Attorneys charge $100 to $500 per hour to defend liability claims, and even a straightforward property damage case can run $5,000 to $15,000 in legal fees before any settlement or judgment. A serious bodily injury claim can result in settlements ranging from $24,000 to well over $100,000, depending on injury severity and jurisdiction. The average general liability premium runs about $360 per year in the US, yet most Dallas business owners spend far more defending themselves against uninsured claims than they would ever pay in annual premiums.

Industry-Specific Risk Exposure

Texas businesses operating in high-risk industries face even steeper exposure. Construction firms, restaurants, retail locations, and professional service providers all encounter scenarios where third-party bodily injury or property damage claims arise regularly. You can’t get a certificate of insurance issued within 24 hours if you don’t have a policy in place, and missing that deadline costs you the contract.

Asset Protection and Peace of Mind

General liability insurance transfers financial exposure to your carrier, protecting your business assets and allowing you to operate without constant fear of catastrophic loss. This protection matters whether you run a small service business or manage a larger operation with multiple employees and clients. The coverage sits between you and the financial devastation that liability claims can inflict on unprepared businesses.

Final Thoughts

General liability insurance protects your Dallas business from third-party bodily injury claims, property damage, and medical expenses-but only if you understand what general liability insurance covers and where gaps exist. The coverage you carry today determines whether a single incident drains your business bank account or your insurance carrier handles it. Most Dallas business owners underestimate how quickly legal fees and settlements accumulate when claims arise, and waiting until after a loss to understand your coverage leaves you exposed to financial devastation.

Your next step is straightforward: obtain a quote that reflects your actual business operations and risk exposure. A $1 million per-occurrence limit works for some businesses and leaves others dangerously underprotected, so the cost difference between adequate coverage and insufficient coverage often amounts to just a few dollars per month, yet the protection gap can cost you hundreds of thousands of dollars when claims happen. Don’t guess at coverage limits or assume a standard policy matches your needs.

We at Brooks Cannon Insurance Group work with Dallas businesses to build insurance strategies that match their operations. As an independent agency, we work with multiple top-rated insurance carriers to find coverage and pricing that fits your situation, and our licensed experts identify gaps before they become expensive problems. Contact Brooks Cannon Insurance Group to discuss your coverage needs and get a quote that protects what you’ve built.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation