Owning rental property in Dallas comes with real financial exposure. Property damage, tenant injuries, and lost rental income can quickly drain your investment returns.

At Brooks Cannon Insurance Group, we help landlords protect their assets with the right coverage. This guide walks you through your landlord protection insurance options so you can make informed decisions about what actually protects your bottom line.

What Coverage Types Do Landlord Policies Include?

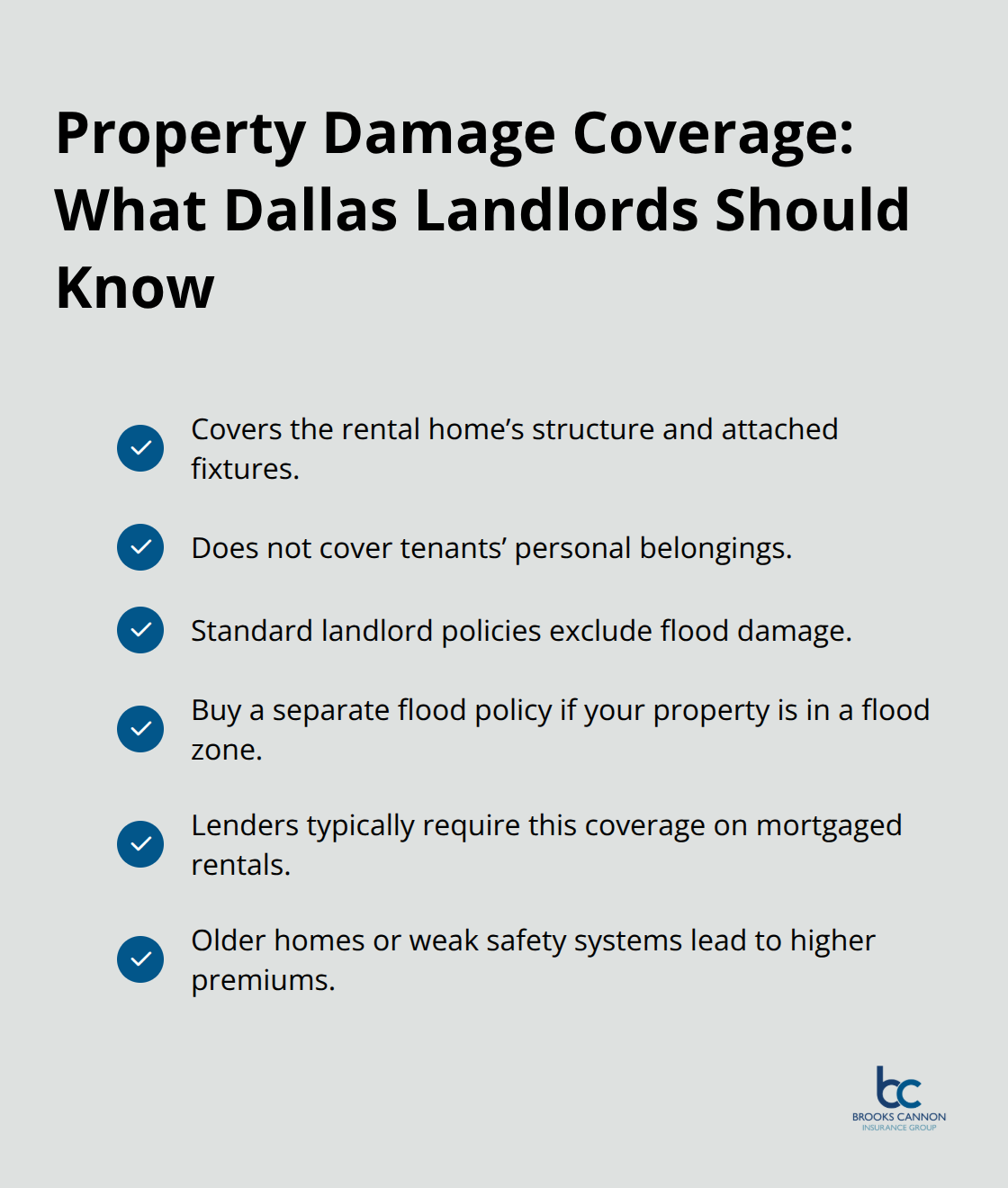

Landlord property damage coverage covers the structure of your rental home and the fixtures attached to it, such as built-in cabinets, flooring, and roof systems. In Dallas, where severe weather causes significant damage, this coverage protects against fire, hail, lightning, and windstorms. It does not cover your tenants’ belongings or normal wear and tear. If you own rental property with a mortgage, your lender almost certainly requires this protection before funding the loan. The Texas Flood Law requires you to disclose flood history to tenants, though standard landlord policies exclude flood damage. You’ll need a separate flood insurance policy for that risk, especially if your property sits in a flood zone. Landlord insurance costs vary based on the home’s age, condition, and security features. Older homes and those without modern safety systems cost more to insure because they present higher risk.

Liability Coverage Protects You From Tenant and Guest Injuries

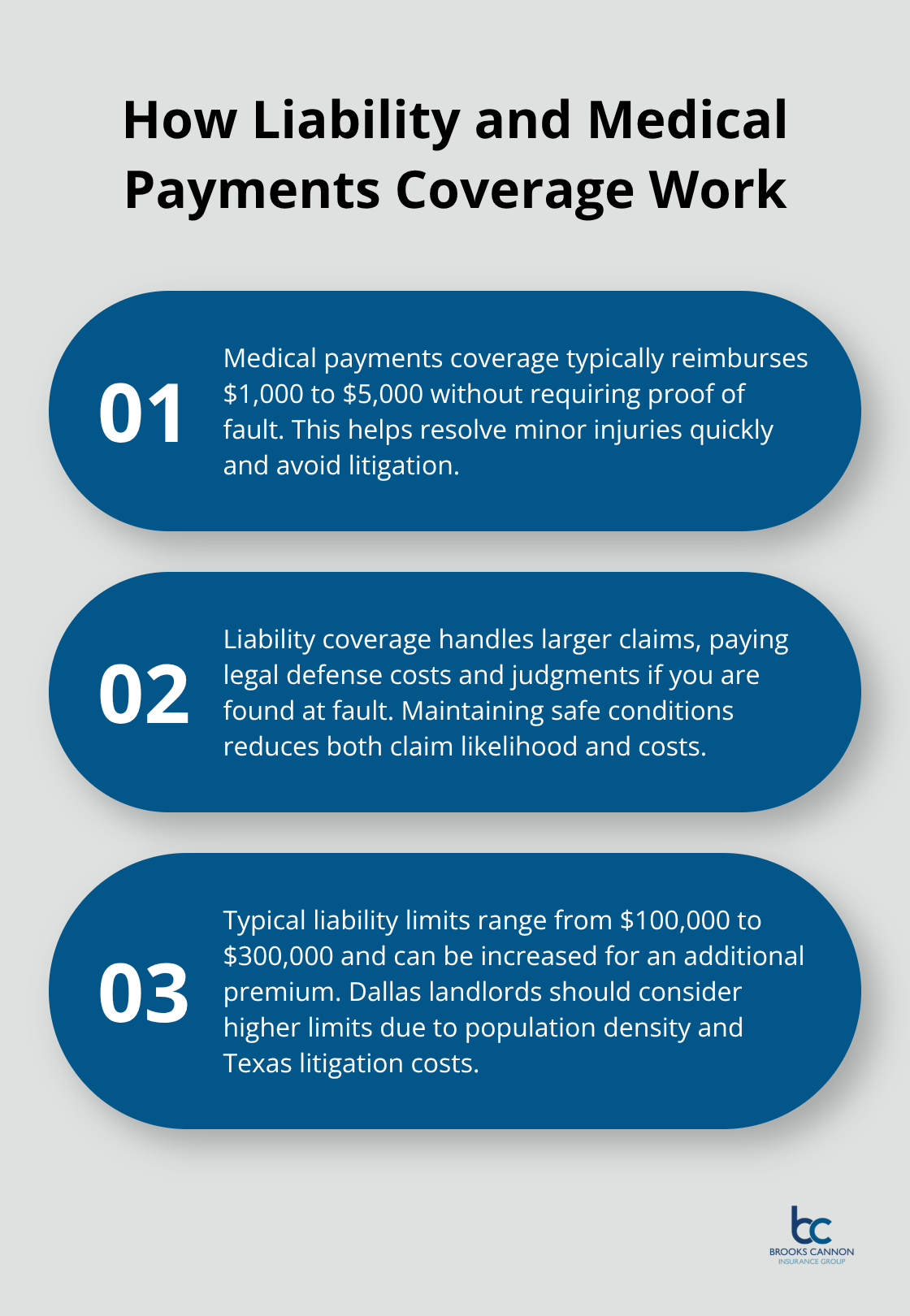

Landlord liability insurance covers medical bills and legal defense costs when someone is injured on your property and you are found at fault. A tenant slips on a broken handrail, or a guest falls down poorly maintained stairs-liability coverage pays their medical expenses and your legal bills. Medical payments coverage typically reimburses up to $1,000 to $5,000 in injury costs without requiring proof of fault, which settles minor incidents quickly. Liability claims in rental properties happen more often than most landlords expect because you’re responsible for maintaining safe conditions. This coverage also protects you if a tenant sues over property damage you caused, such as a water leak from faulty plumbing in a unit above theirs. Most policies include $100,000 to $300,000 in liability limits, though you can increase this for additional premium.

Dallas landlords should strongly consider higher limits given the area’s population density and litigation costs in Texas.

Loss of Rent Coverage Replaces Income When Tenants Cannot Occupy

Loss of rent coverage reimburses you for monthly rental income if a covered event makes the property uninhabitable. A fire damages the kitchen, or a severe storm destroys the roof-your tenants must vacate while repairs happen. Without this coverage, you lose income during weeks or months of repairs while still paying the mortgage and property taxes. Coverage typically reimburses 100% of lost rent for the time needed to repair and restore occupancy, though some policies limit reimbursement to 12 months. This protection is especially valuable in Dallas where storm season can cause extended damage. The coverage does not apply if tenants cannot pay rent due to their own financial hardship or job loss. It also does not cover income loss from tenant turnover, evictions, or normal vacancies between tenants. Understanding these three core protections helps you identify which gaps exist in your current coverage and what additional endorsements might strengthen your policy.

What Does Each Coverage Type Actually Protect

Property Damage Coverage Protects Your Structure, Not Tenant Belongings

Property damage coverage in your landlord policy protects the physical structure and permanent fixtures, but understanding what falls outside this protection matters more than knowing what’s inside. Your policy covers damage from fire, hail, lightning, and windstorms, which account for the majority of claims Dallas landlords file. However, it does not cover theft of items your tenants own, damage from floods, or deterioration from normal wear and tear. If a tenant’s television gets stolen or their personal belongings are damaged, that loss falls entirely on them, which is why requiring renters insurance from your tenants makes financial sense.

Many Dallas landlords overlook this requirement and later discover they have no recourse when tenant belongings are damaged. The Texas Windstorm Insurance Association offers windstorm inspections that identify strengthening measures and can lead to premium reductions, so if your property sits in a windstorm-prone area, request an inspection through TWIA. Property condition directly impacts your premium, with older homes and those lacking modern safety systems costing significantly more to insure because insurers view them as higher risk.

Liability and Medical Payments Coverage Protect You From Injury Claims

Liability and medical payments coverage protect you from financial disaster when someone is injured on your property, and this protection extends far beyond simple slip-and-fall incidents. Medical payments coverage typically reimburses $1,000 to $5,000 in medical bills without requiring you to prove fault, which means a tenant’s minor injury gets resolved quickly without litigation. Liability coverage takes over for larger claims, covering legal defense costs and court judgments if a tenant or guest sues you for injuries or property damage they claim you caused.

A tenant could sue over a water leak from faulty plumbing in the unit above, claiming damage to their belongings, and your liability coverage pays both your attorney fees and any settlement. Dallas property owners should carry at least $300,000 in liability limits given the area’s population density and Texas litigation costs, which tend to run higher than national averages.

Loss of Rent Coverage Protects Your Cash Flow During Repairs

Loss of rent coverage reimburses you for monthly income when a covered loss makes the property uninhabitable, protecting your cash flow during repairs that might otherwise last weeks or months. This coverage pays 100% of lost rent for the repair period, though some policies cap reimbursement at 12 months, and it does not apply when tenants cannot pay due to their own financial hardship or job loss. Understanding these distinctions between what your policy covers and what it excludes helps you identify gaps in your current protection and determine which additional endorsements strengthen your overall position.

How to Pick the Right Coverage for Your Dallas Rental

Assess Your Property’s Risk Profile Honestly

Selecting landlord insurance requires honest assessment of your property’s actual risk profile, not generic coverage limits that sound adequate. Start by documenting your property’s age, construction type, security features, and location within Dallas, since these factors directly determine both what you need to protect and how much insurers will charge. A 40-year-old duplex in East Dallas with outdated electrical systems faces different risks than a newer property in a gated community, and your policy should reflect that difference.

Walk through your rental and identify maintenance issues, safety hazards, and structural vulnerabilities. A broken handrail, missing smoke detectors, or deferred roof repairs increase your liability exposure substantially and will push your premiums higher regardless of which carrier you choose. Insurance companies conduct property inspections before underwriting, so they will discover these issues anyway. Addressing them before you apply for coverage demonstrates risk management and often qualifies you for better rates.

Calculate Loss of Rent Coverage Based on Your Actual Income

Next, calculate your actual monthly rental income and determine how long repairs might take if a covered loss occurred. If you charge $2,000 per month and repairs typically take 60 days, you need loss of rent coverage that reimburses at least $4,000 to protect your cash flow completely. Many Dallas landlords underestimate repair timelines and end up short on coverage when storms or fires strike.

Your loss of rent coverage should account for realistic repair timelines in the Dallas area, particularly when contractor availability tightens after major weather events. This timeline matters because your mortgage and property taxes continue while tenants cannot occupy the unit. Loss of rent coverage that falls short of your actual monthly expenses leaves you paying the difference from your own pocket.

Balance Deductibles Against Your Financial Reserves

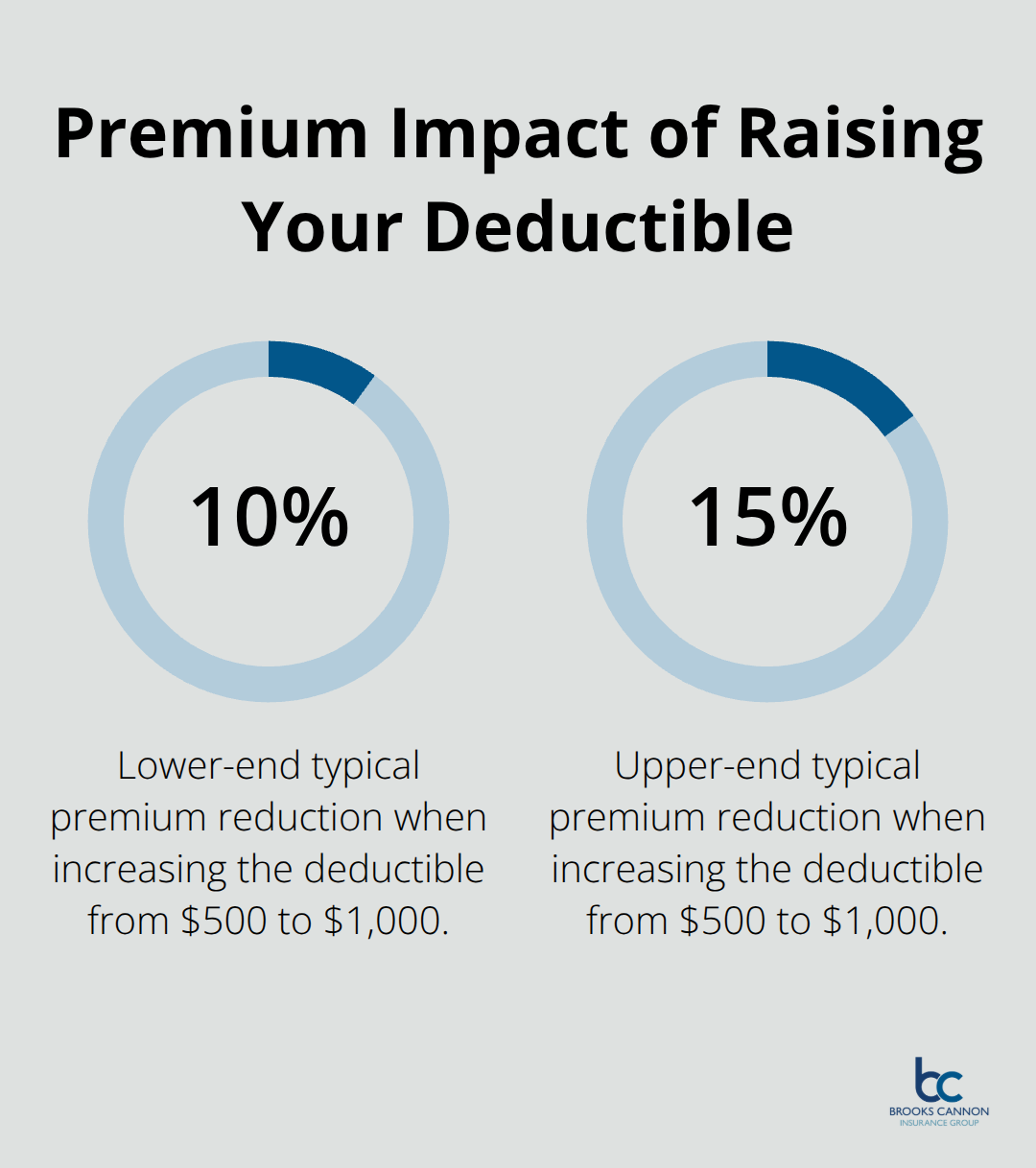

Coverage limits and deductibles directly control what you pay now versus what you’d pay after a claim. Raising your deductible from $500 to $1,000 typically reduces your annual premium by 10 to 15 percent, which sounds attractive until you face a claim and owe that higher amount out of pocket. Dallas landlords with multiple properties or strong cash reserves can absorb higher deductibles and benefit from the premium savings. Those with limited reserves should keep deductibles lower to avoid financial strain after a loss.

Prioritize Adequate Liability Limits for Texas Courts

Liability limits deserve special attention because a single serious injury can generate claims exceeding $100,000 quickly. A tenant’s permanent disability from a fall on your property, or a guest’s severe burn from faulty wiring, can trigger lawsuits seeking substantial damages. Texas courts award damages aggressively, and legal defense costs alone can reach $50,000 to $100,000 before any settlement occurs.

Carrying $300,000 in liability limits is the minimum we recommend for Dallas properties, with $500,000 or higher preferred if you own multiple units or properties in areas with higher injury risk. This protection combined with proper maintenance shields your personal assets from judgment claims that could otherwise devastate your financial position.

Work with an Independent Agent for Multiple Carrier Access

Working with an independent insurance agent who represents multiple carriers gives you access to different underwriting standards and pricing models. Some carriers specialize in older properties and offer better rates than competitors, while others excel at insuring properties with recent claims. An agent familiar with Dallas rental market conditions understands which carriers move fastest on claims, which ones deny medical payments disputes most often, and which offer the best loss of rent coverage terms.

At Brooks Cannon Insurance Group, we work with multiple top-rated carriers to find coverage and pricing tailored to your specific property rather than forcing you into standard packages that don’t fit your situation. Our team of licensed experts can match your property’s unique risk profile with carriers that understand Dallas rental market conditions and price accordingly.

Final Thoughts

Landlord protection insurance protects your Dallas rental investment from the three most costly risks you face as a property owner. Property damage coverage rebuilds your structure after fire, hail, or windstorms, while liability coverage shields you from injury claims that could otherwise drain your personal assets. Loss of rent coverage keeps your cash flow intact during repairs when tenants cannot occupy the unit, and this protection matters most when contractors move slowly after major weather events.

Your specific coverage needs depend entirely on your property’s age, condition, location, and your financial reserves. Calculating your actual monthly rental income and realistic repair timelines ensures your loss of rent coverage matches your real expenses, not generic industry standards. Liability limits deserve the most attention because a single serious injury can generate claims far exceeding $100,000, and Texas courts award damages aggressively enough that legal defense costs alone can reach $50,000 before any settlement occurs.

The right landlord protection insurance policy requires honest assessment of your property’s risk profile and comparison across multiple carriers. We at Brooks Cannon Insurance Group work with top-rated carriers to find coverage and pricing tailored to your specific situation rather than forcing you into standard packages that don’t fit. Contact our licensed experts today to review your current coverage and identify gaps that could leave you exposed.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation