Many Dallas property owners assume their standard homeowners policy covers rental properties. This costly mistake leaves landlords exposed to significant financial risks.

Rental property insurance provides specialized protection that homeowners insurance simply cannot match. We at Brooks Cannon Insurance Group see firsthand how the wrong coverage can devastate investment returns when claims arise.

Key Differences Between Rental Property and Homeowners Insurance

Homeowners insurance protects occupied residences where owners live full-time, while rental property insurance addresses the unique risks landlords face. Standard homeowners policies exclude rental activities and leave property owners completely unprotected when they rent out their homes. Rental income on properties requires specialized coverage considerations, which makes dedicated landlord insurance essential for proper protection.

Coverage Scope and Protected Assets

Rental property insurance covers the structure, other buildings on the property, and landlord-owned items like appliances and furnishings provided to tenants. Homeowners insurance protects personal belongings and provides temporary expenses for displaced owners. Landlord policies exclude tenant possessions entirely and require renters to secure separate coverage. Loss of rental income protection stands as the most significant difference-landlord insurance compensates for lost rent when properties become uninhabitable due to covered damages, while homeowners policies offer no income replacement benefits.

Liability Protection Variations

Liability coverage differs dramatically between these insurance types. Rental property insurance typically starts at $300,000 in liability protection and recognizes the higher risk of tenant and visitor injuries. Homeowners policies often provide lower liability limits since fewer people access owner-occupied homes. Landlords face increased liability exposures due to the nature of rental operations and multiple occupants accessing their properties.

Cost Differences and Premium Factors

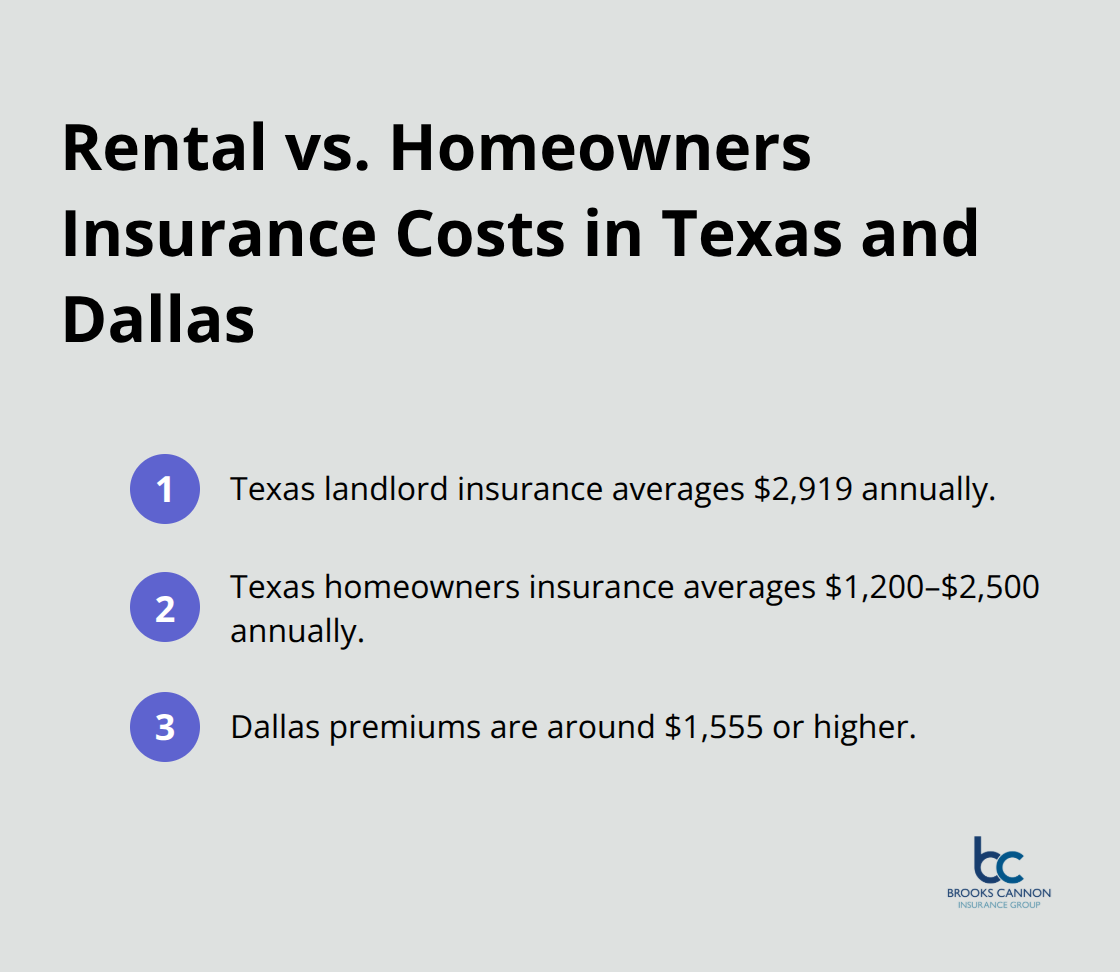

In Texas, landlord insurance averages $2,919 annually compared to homeowners insurance at $1,200-2,500 (reflecting the elevated risk profile). Properties in Dallas command premiums around $1,555 or higher due to urban liability exposures and weather-related risks. These cost differences stem from the specialized protections rental properties require and the increased frequency of claims landlords experience.

Understanding these fundamental differences helps property owners recognize why standard homeowners coverage falls short for rental properties. The specific protections rental property insurance provides become even more apparent when we examine exactly what these policies cover.

What Rental Property Insurance Covers

Rental property insurance delivers three core protection areas that homeowners policies exclude entirely. Dwelling coverage protects the physical structure of your rental property and typically covers repair or replacement costs up to the policy limit when damage occurs from covered perils like fire, wind, or vandalism. This coverage extends to attached structures like garages and includes landlord-owned appliances, flooring, and fixtures that you install permanently in the unit. Most policies in Dallas cover replacement cost rather than actual cash value, which means you receive enough money to rebuild with similar materials at current prices without depreciation deductions.

Dwelling and Structure Protection

Structure coverage protects your rental property’s foundation, walls, roof, and permanently attached fixtures when covered perils cause damage. The policy covers landlord-owned appliances like refrigerators, washers, and HVAC systems that you provide to tenants. Coverage limits typically range from $100,000 to $500,000 depending on property value and location. Wind damage claims in Dallas average $15,000 per incident according to Texas Department of Insurance data, making adequate dwelling coverage essential for property owners.

Loss of Rental Income Coverage

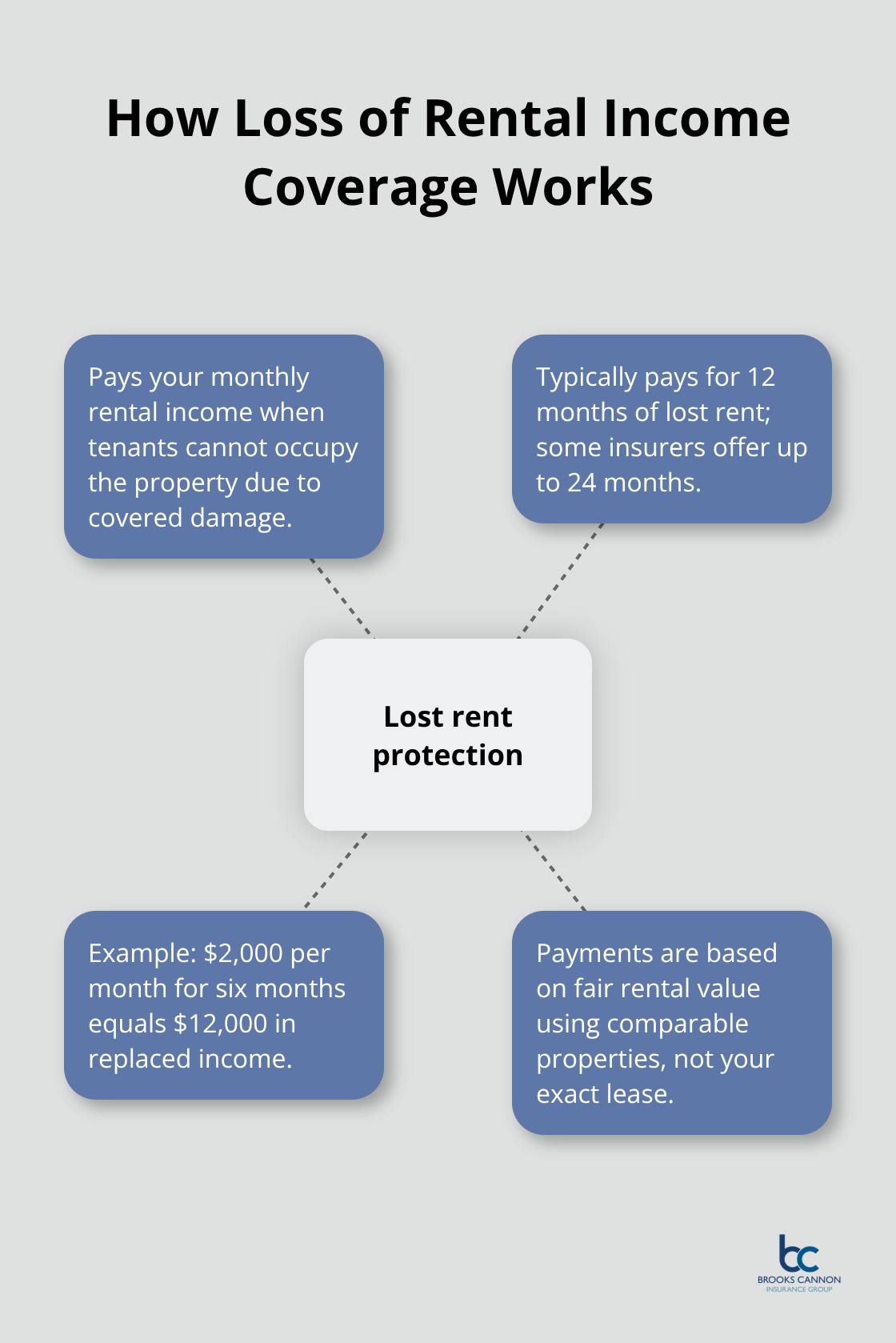

Loss of rental income coverage pays your monthly rental income when tenants cannot occupy the property due to covered damage. This coverage typically pays for 12 months of lost rent, though some insurers offer up to 24 months of protection. If your Dallas rental property generates $2,000 monthly and becomes uninhabitable for six months after storm damage, this coverage pays $12,000 to replace lost income. Fair rental value calculations determine payment amounts based on comparable properties in your area rather than your actual lease agreements.

Landlord Liability and Legal Protection

Landlord liability coverage starts at $300,000 and protects against lawsuits when tenants or visitors suffer injuries on your property. Medical payments coverage (typically $5,000 per incident) pays immediate medical expenses regardless of fault determination. Legal defense coverage pays attorney fees, court costs, and settlement amounts up to policy limits when liability claims arise. Slip-and-fall accidents on rental properties generate average settlement costs exceeding $50,000 according to the Insurance Information Institute.

Even comprehensive rental property insurance contains specific exclusions that can leave landlords exposed to unexpected costs and financial losses.

Common Coverage Gaps and How to Avoid Them

Rental property insurance contains specific exclusions that catch landlords off guard when claims arise. These gaps expose property owners to substantial financial risks that standard policies never address.

Personal Property Exclusions for Tenants

Tenant personal property receives no coverage under landlord policies. Tenants must secure renters insurance to protect their belongings from theft, fire, or water damage. Most renters lack adequate insurance coverage, which leaves landlords potentially liable for disputes over damaged tenant possessions.

Property owners should require renters insurance in lease agreements and collect proof of coverage annually. This requirement protects both parties and eliminates confusion about responsibility when tenant belongings suffer damage. Many landlords add automatic lease termination clauses if tenants fail to maintain continuous renters coverage.

Natural Disaster Limitations

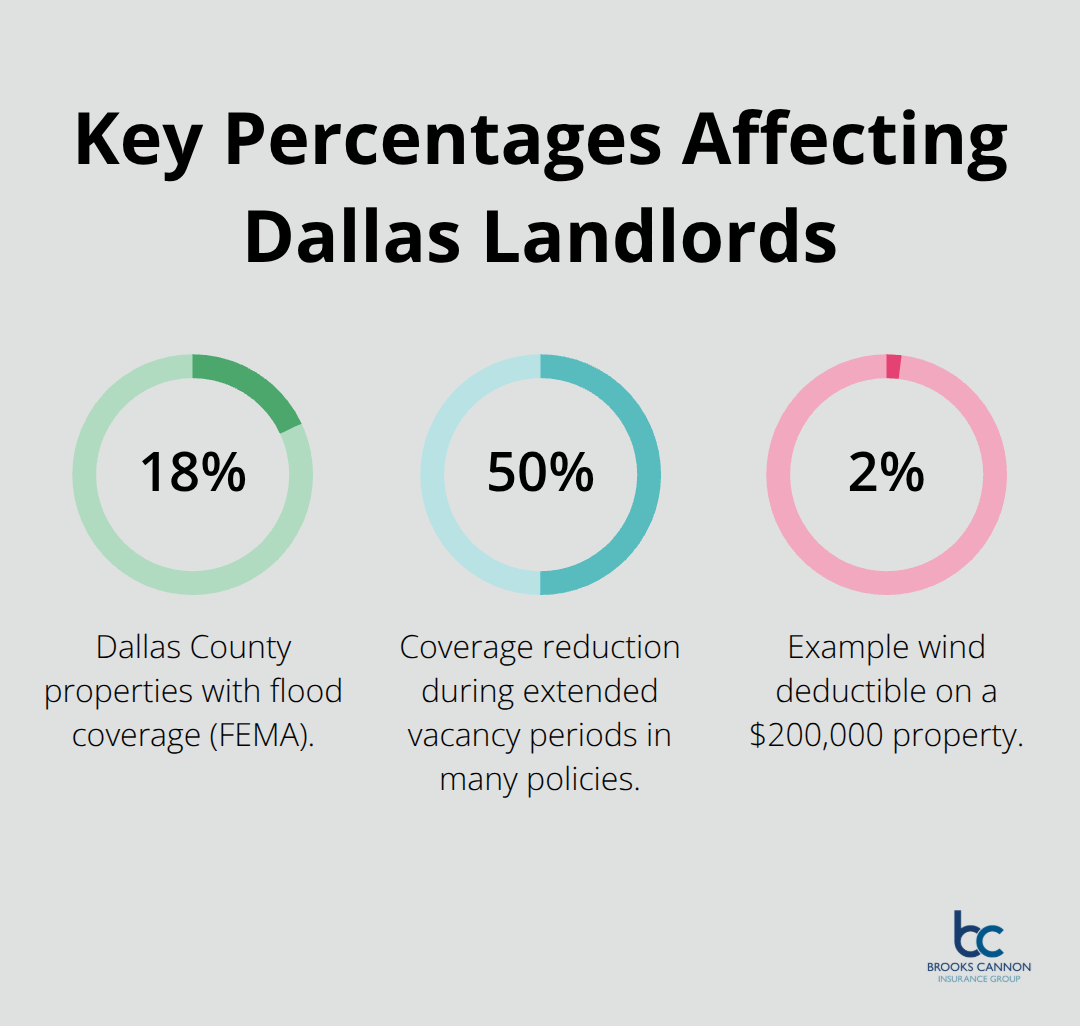

Standard rental property policies exclude flood damage entirely. Property owners must purchase separate flood insurance through the National Flood Insurance Program. Texas experiences floods in 254 counties, yet only 18% of Dallas County properties carry flood coverage according to FEMA data.

Wind damage from hurricanes and tornadoes faces percentage deductibles rather than fixed amounts. A $200,000 property with 2% wind deductible requires $4,000 out-of-pocket before coverage begins. Earthquake coverage requires separate endorsements in Texas, though seismic activity remains minimal compared to California markets.

Vacancy Period Restrictions

Most policies limit coverage when properties remain vacant beyond 30-60 days. Insurers reduce protection by 50% or exclude certain perils entirely during extended vacancy periods. Vandalism and theft coverage often disappears completely when no tenants occupy the property.

Properties between tenants generate more insurance claims than occupied units according to Insurance Information Institute research. Landlords must notify insurers immediately when tenancies end and secure vacant property endorsements to maintain full coverage. Some insurers offer short-term rental endorsements for properties between long-term tenants (though these cost 15-25% more than standard coverage).

Final Thoughts

Dallas landlords need rental property insurance that addresses severe weather risks, urban liability exposures, and tenant-related damages that homeowners policies exclude. Standard homeowners coverage leaves property owners vulnerable to significant financial losses when claims arise. Independent insurance agencies provide access to multiple carriers and competitive rates for comprehensive protection.

Property owners must secure adequate dwelling coverage, liability protection, and loss of rental income benefits to protect their investments. Regular policy reviews maintain appropriate coverage levels as property values and rental markets evolve. Tenant renters insurance requirements and detailed property records reduce liability exposures substantially.

The cost difference between rental property insurance and homeowners coverage reflects the specialized protections landlords require (typically 40-60% higher premiums). Proper coverage protects rental income and prevents financial disasters when unexpected claims occur. Brooks Cannon Insurance Group helps Dallas area property owners secure comprehensive protection at competitive rates.