Your home in the Dallas area likely represents your largest investment. If you own a luxury property or have significant assets inside it, standard homeowners insurance probably leaves you underprotected.

High value home insurance fills those gaps with coverage tailored to what you actually own. We at Brooks Cannon Insurance Group help homeowners understand whether this specialized protection makes sense for their situation.

What High Value Home Insurance Actually Covers

High value home insurance fundamentally differs from standard homeowners policies in both scope and approach. A standard policy tops out at coverage limits that work fine for typical homes-usually $300,000 to $500,000 in dwelling coverage. But if your home’s replacement cost exceeds $750,000, that standard policy creates a dangerous gap.

Luxury home sales in the Dallas-Fort Worth metro area grew 14 percent from 2023 to 2024, and many of those homeowners discover too late that their basic coverage doesn’t match what it would actually cost to rebuild. High value policies start where standard ones fall short, offering dwelling limits that climb to $1.5 million, $2 million, or beyond depending on the carrier and your home’s true reconstruction expenses. The difference isn’t just about bigger numbers-it’s about how the policy treats your property and possessions.

Why Replacement Cost Matters More Than You Think

Standard policies often calculate coverage based on your home’s market value or mortgage amount. That’s the wrong metric entirely. What matters is replacement cost-the actual dollars required to rebuild your home with the same materials, finishes, and quality. A custom home in Dallas with imported marble, high-end smart home systems, and premium architectural details costs far more to replace than its market listing price suggests. High value policies excel here. They require detailed appraisals that account for custom construction, unique architectural features, and those expensive finishes. Bankrate data shows that average annual premiums for high value policies with $750,000 dwelling coverage run around $5,254, compared to roughly $2,424 for standard policies. That premium difference reflects the reality that insurers now price actual reconstruction costs, not guesses.

Personal Property Coverage That Actually Protects Your Valuables

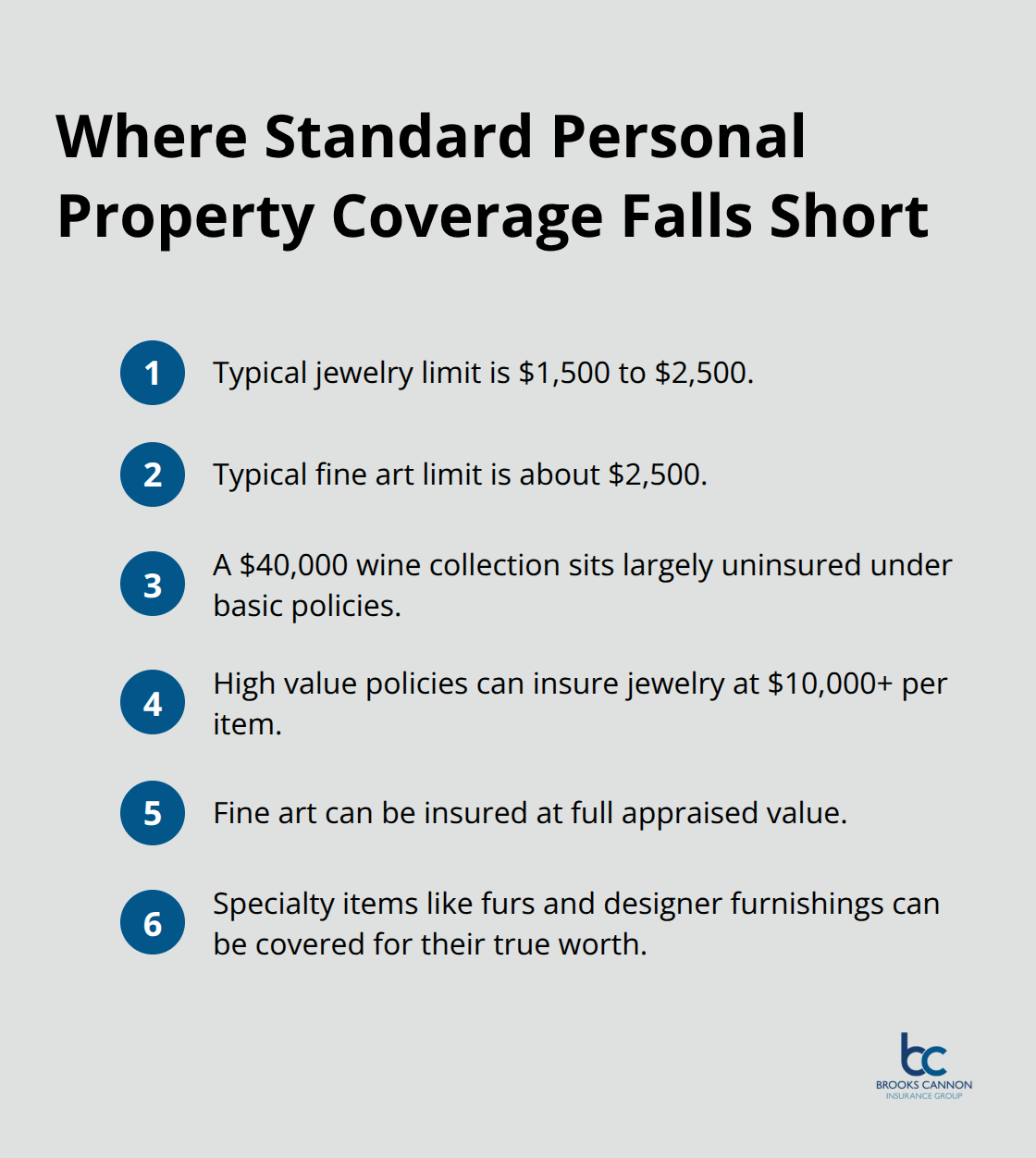

Standard homeowners policies impose strict limits on personal property coverage-typically $1,500 to $2,500 for jewelry, $2,500 for fine arts, and similar restrictions. If you own a wine collection worth $50,000, rare artwork, or high-end furnishings, standard coverage leaves those items severely underprotected. High value policies remove those artificial ceilings. You can insure jewelry up to $10,000 or more per item, fine art at appraised values, and specialty items like rugs and furs at their true worth.

Additional Protections Standard Policies Won’t Provide

High value policies often include protections that standard policies exclude entirely-sewer backup coverage, water damage protection, and loss-of-use limits generous enough to cover temporary housing during reconstruction at luxury standards. As many as 50 percent of high value homes in the United States sit in flood-prone zones, yet standard policies don’t cover flood damage at all. High value policies make flood coverage available as an add-on, acknowledging the real risks that luxury properties face.

Understanding what high value policies cover sets the foundation for determining whether you actually need this protection. The next step involves honestly assessing your home’s true value and the assets inside it-a process that separates homeowners who are adequately protected from those who face significant financial exposure.

Signs You Need High Value Home Insurance

Your Home’s Replacement Cost Reveals the Real Gap

Your home’s replacement cost tells the real story about whether standard insurance protects you adequately. If rebuilding your Dallas-area home would cost more than $750,000, standard policies create immediate exposure. That $750,000 threshold isn’t arbitrary-it marks where standard dwelling limits end and where actual reconstruction expenses for quality custom homes begin. When hail damages your roof or a water event forces major reconstruction, you’ll discover that $500,000 in dwelling coverage won’t pay for impact-resistant shingles, custom woodwork, and premium finishes. High value policies start at $1.5 million in dwelling coverage and climb higher, matching what your home actually costs to rebuild rather than what it sold for.

Personal Property Limits That Leave Valuables Exposed

Your personal property determines whether standard coverage fails you. If you own jewelry worth more than $2,500, fine art beyond $5,000, or collections of any kind, standard homeowners policies won’t protect those items adequately. A wine collection worth $40,000, rare books, high-end furniture, or custom rugs sit almost entirely uninsured under basic policies.

High value coverage removes those artificial limits, letting you insure jewelry at $10,000 per item or more and fine art at full appraised value. Specialty items like furs and designer furnishings receive the same treatment. The Dallas-Fort Worth area’s affluent neighborhoods contain homes with exactly these types of valuables, and their owners face real financial exposure if they haven’t upgraded their coverage.

Unique Risks That Standard Policies Ignore Entirely

Luxury homes present unique risks that standard policies ignore. Water damage from burst pipes in a home with marble floors and hardwood throughout costs far more to repair than standard policies acknowledge. High value policies include protections addressing the real risks that upscale properties face in North Texas weather patterns.

The question shifts now from whether you need high value coverage to which policy and carrier will actually protect your specific situation. Assessing your home’s total value and the assets inside it requires a systematic approach that goes beyond simple guesswork.

How to Choose the Right High Value Home Insurance

Document Your Home’s True Replacement Cost

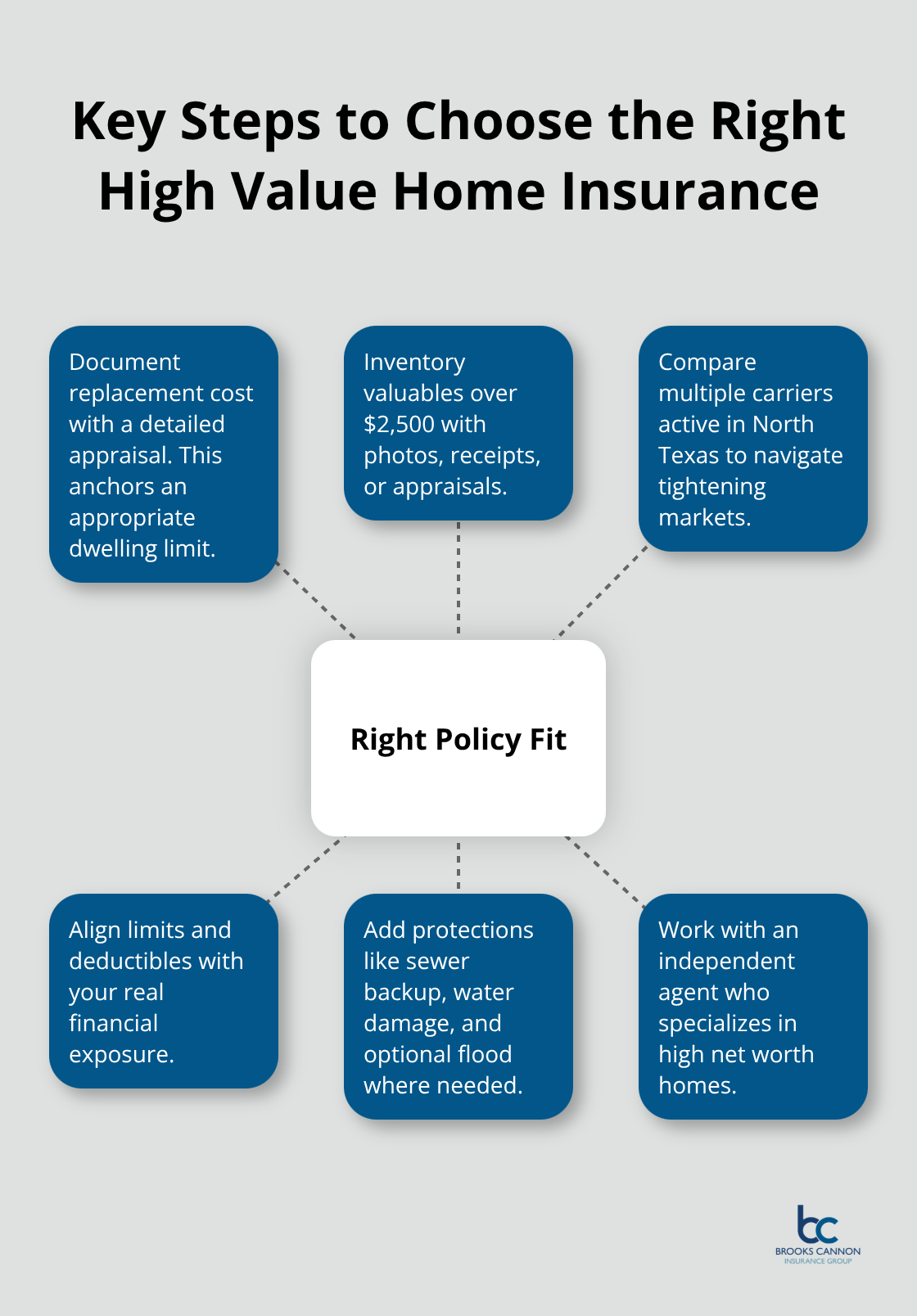

Start with a detailed home appraisal that documents actual replacement cost, not market value. Many homeowners in the Dallas area guess at their home’s reconstruction expenses and end up dramatically underinsured. An appraisal accounts for custom materials, architectural details, and regional labor costs specific to North Texas. This document becomes your foundation for determining the correct dwelling limit.

Inventory Your Personal Property Systematically

Walk through your home and list items worth more than $2,500 individually-jewelry, art, collectibles, designer furniture, wine collections, and specialty items. Photograph or video document these possessions with receipts or appraisals. This inventory reveals whether you need scheduled personal property coverage or higher limits on specific categories. Many homeowners discover they own far more than standard policies protect once they actually account for everything.

Compare Quotes Across Multiple Carriers

Request quotes from multiple carriers, not just one. The North Texas market for high value home insurance has tightened due to severe hailstorms and rising construction costs, meaning carrier availability varies significantly. Some insurers like Chubb specialize in homes exceeding $2 million, while others like Travelers and Hartford offer coverage up to $1.5 million. Safeco and National General extend options to $2 million. Access to carriers still writing policies in North Texas is increasingly valuable, and shopping multiple options prevents you from accepting inadequate coverage simply because one carrier declined your home.

Align Coverage Limits with Your Financial Exposure

Evaluate coverage limits against your actual financial exposure, not the premium cost. A high value policy with $1.5 million in dwelling coverage costs more than standard insurance, but underinsuring your $1.2 million replacement-cost home creates far greater financial risk. Deductibles on high value policies typically range from $2,500 to $10,000, and selecting a higher deductible reduces your premium while maintaining adequate coverage limits.

Also confirm that additional protections like sewer backup, water damage, and loss-of-use coverage match your home’s specific vulnerabilities. Homes in flood-prone areas need flood coverage as an add-on, since standard policies exclude it entirely.

Work with an Independent Agent Specializing in High Net Worth Coverage

An independent agent who specializes in high net worth clients maintains relationships with multiple carriers and can shop your situation across available options rather than pushing a single company’s products. They understand North Texas weather risks, local construction practices, and carrier appetite for luxury homes in specific ZIP codes. An on-site inspection identifies your home’s unique characteristics and build quality, documentation goes to high value carriers to explore options, and the agent negotiates limits and coverages to secure the protection you actually need.

Final Thoughts

High value home insurance addresses a fundamental gap that standard policies leave unprotected. If your Dallas-area home costs more than $750,000 to rebuild, or if you own valuable collections and specialty items, basic homeowners coverage exposes you to significant financial risk. These policies account for your home’s actual replacement cost through detailed appraisals, remove artificial caps on personal property coverage, and include protections like sewer backup and water damage that standard policies exclude entirely.

Determining whether you need this coverage requires honest assessment of your home’s true reconstruction expenses and the value of what you own inside it. Market value and mortgage amount tell you nothing about either-an appraisal that documents replacement cost and a systematic inventory of your possessions reveal your actual exposure. The North Texas market has tightened for high value home insurance due to hail risk and rising construction costs, making access to carriers still writing policies increasingly valuable.

Contact us to discuss your home’s true value and the assets you need to protect. We’ll assess your situation and show you what adequate high value home insurance actually looks like for your Dallas-area property. Call 214-446-9000 or visit us at 5728 Prospect Ave #2003, Dallas, TX 75206 to get started.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation