Many business owners in the Dallas area ask us whether they need a business owners policy or if general liability insurance alone will protect them. The truth is, these two options offer very different levels of protection, and choosing the wrong one could leave your business exposed.

At Brooks Cannon Insurance Group, we help business owners understand exactly what each policy covers so you can make the right decision for your situation. This guide breaks down the real differences between business owners insurance and general liability coverage.

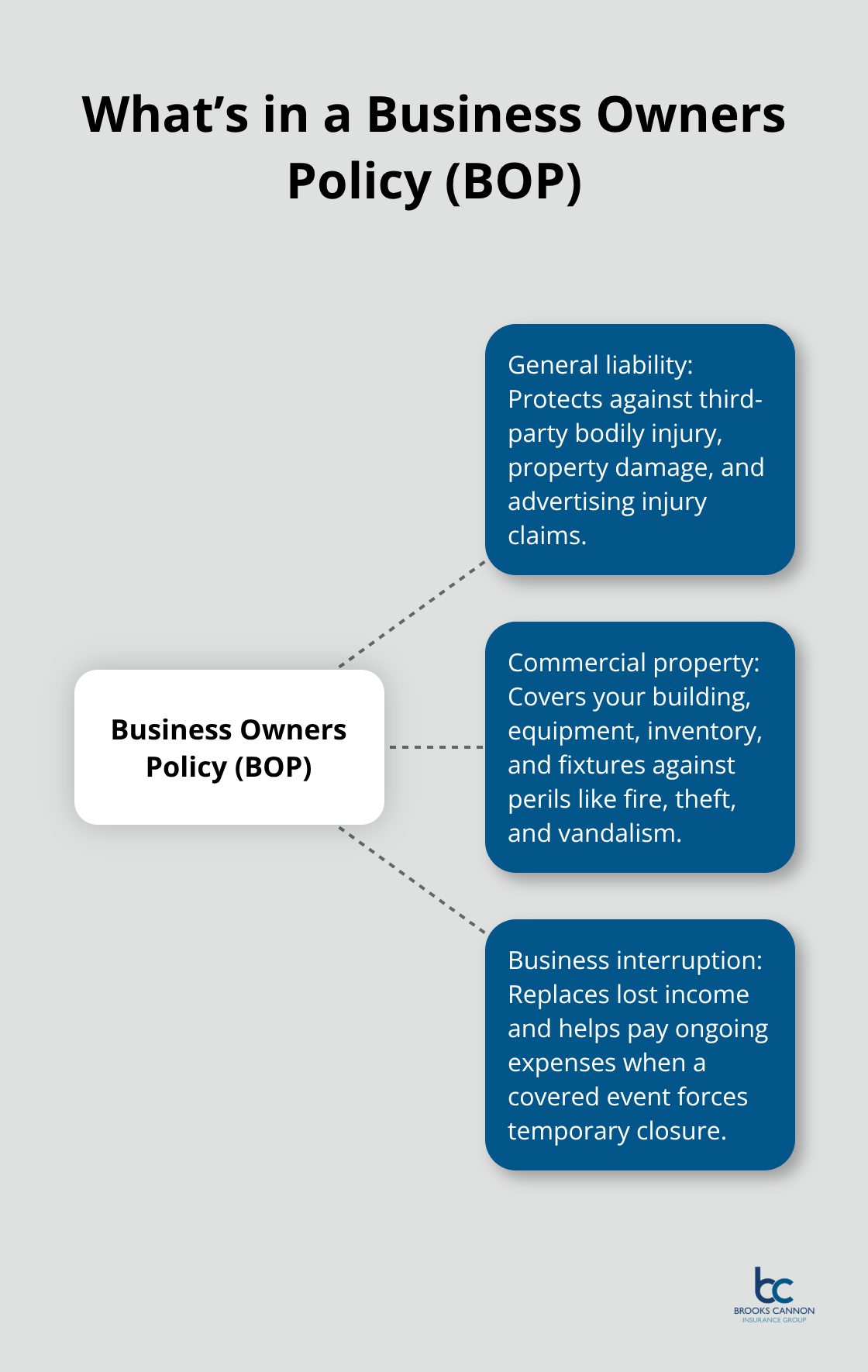

What a Business Owners Policy Actually Covers

The Three Core Components of a BOP

A Business Owners Policy bundles three essential protections into one plan: general liability coverage for third-party claims, commercial property coverage for your physical assets, and business interruption insurance to replace lost income when you cannot operate. General liability within a BOP protects you if a customer gets injured on your premises or if your business operations damage someone else’s property. Commercial property coverage protects your building, equipment, inventory, and fixtures against fire, theft, vandalism, and other covered disasters. Business interruption coverage reimburses your lost income and helps pay ongoing expenses like employee salaries if a covered event forces you to temporarily close.

Why Property Protection Matters in Dallas

For Dallas business owners, this bundled approach matters because weather disasters have caused significant property damage across Texas, making property protection genuinely valuable. A BOP typically costs between 500 and 2,000 dollars annually. When you compare this to buying general liability and commercial property separately, a BOP saves roughly 52 dollars per month or about 624 dollars per year compared to standalone policies, according to data from Insureon customers.

Who Actually Needs a BOP

You genuinely need a BOP if you own or lease a physical location where customers visit, operate from a storefront or office, maintain equipment or inventory that requires protection, or depend on your business location for revenue. Restaurants, retail shops, consulting offices, and construction companies with job sites all benefit from BOP coverage because property damage or business interruption would directly impact their ability to earn. However, if you operate exclusively as a freelancer or independent contractor working from home without significant physical assets, general liability alone may suffice.

Additional Coverage You May Still Need

A BOP is especially attractive for small businesses because it satisfies landlord requirements for commercial property insurance, reduces administrative burden by consolidating policies, and provides cost efficiency through bundling. Dallas businesses should also note that some specialized risks still require separate policies even with a BOP in place-such as workers compensation if you have employees, commercial auto coverage if you use vehicles for business, cyber liability if you handle customer data, or errors and omissions insurance if you provide professional services. Understanding what falls outside your BOP helps you identify the coverage gaps that could expose your business to significant financial risk.

What General Liability Actually Protects

Coverage for Third-Party Claims

General liability insurance covers third-party claims when someone outside your business gets hurt or their property gets damaged because of your operations. This protection includes bodily injury claims like a customer slipping on your floor or getting injured by something your business did, property damage claims such as your work accidentally damaging a client’s asset or your sign falling and hitting a car, and advertising injury claims involving copyright infringement or reputational harm from your marketing materials. According to the Insurance Information Institute, general liability is the most common commercial coverage among Texas small businesses.

Costs and Coverage Limits

For Dallas businesses, general liability typically costs between 500 and 2,000 dollars annually depending on your industry and operation size. The policy also covers your legal defense costs, settlements, and court judgments up to your chosen limit, usually between 1 million and 2 million dollars per occurrence. This means the insurer pays for your attorney fees and any judgment against you, up to that limit.

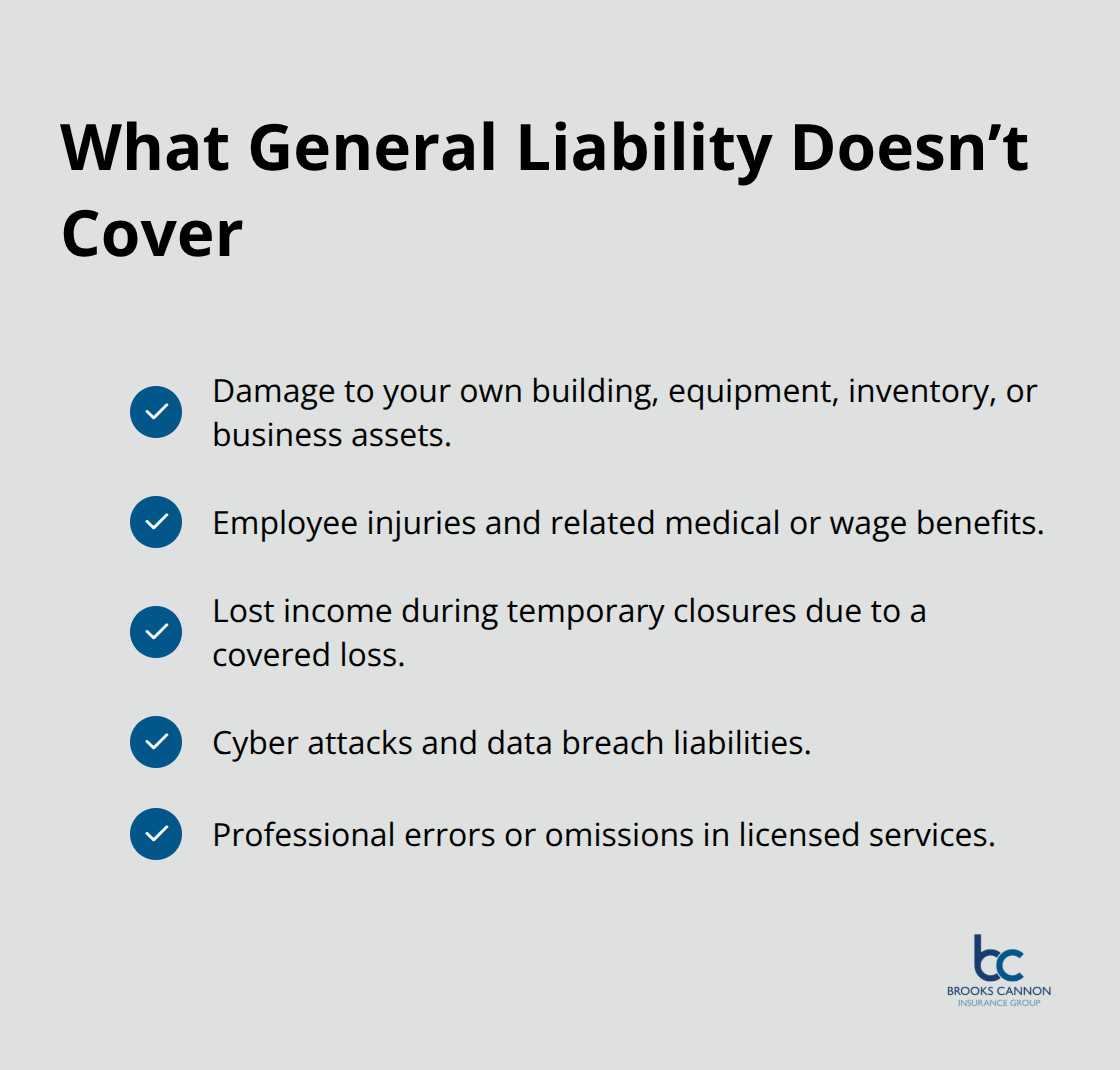

What General Liability Excludes

This policy will not reimburse damage to your own building, equipment, inventory, or business assets-that is exactly why commercial property coverage exists separately or within a business owners policy. General liability does not protect your employees from work-related injuries; that requires workers compensation insurance which Texas businesses can optionally purchase but face serious exposure without it. The policy does not cover your business income if you must temporarily close due to a covered loss, does not protect against cyber attacks or data breaches, and does not cover professional errors if you provide services requiring a license.

Specialized Risks Require Additional Policies

If a customer sues your restaurant for food poisoning or a client claims your accounting advice caused financial harm, general liability will not defend you-those situations require specialized coverage like liquor liability or errors and omissions insurance. Dallas business owners often discover these gaps only after a loss occurs, which is why understanding what falls outside general liability protection matters for your risk management strategy. These limitations highlight why comparing general liability to a bundled business owners policy reveals such significant differences in the protection each option actually provides.

Key Differences Between BOPs and General Liability

The Fundamental Protection Gap

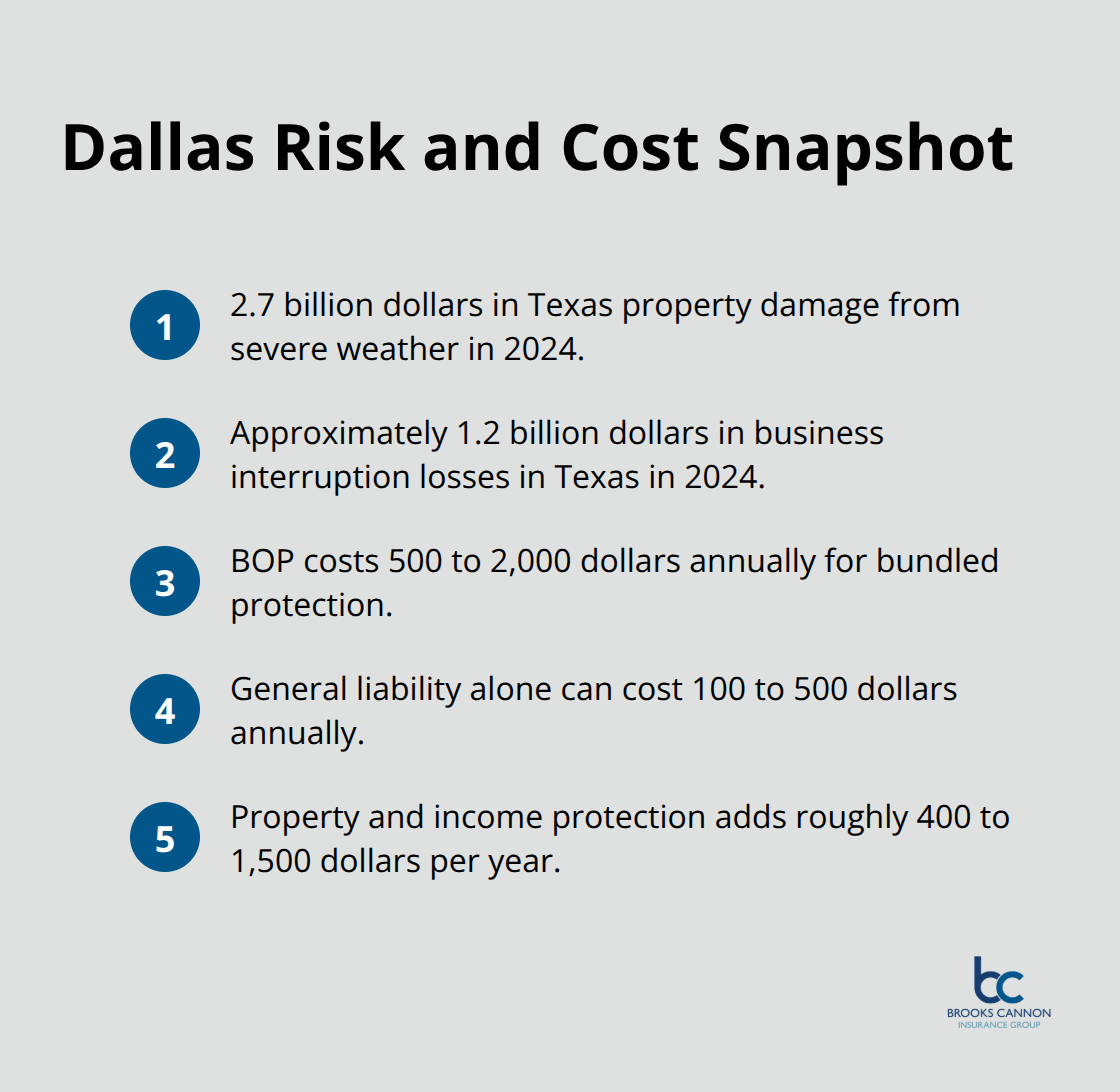

The core difference between a BOP and general liability comes down to what happens when your business faces a loss. General liability only covers third-party claims, meaning it pays when someone outside your business sues you for injuries or property damage they suffered. A BOP extends much further by including that same liability protection plus commercial property coverage and business interruption insurance, creating a safety net for your own assets and income. In Dallas, where severe weather caused about 2.7 billion dollars in property damage across Texas in 2024 according to the Insurance Information Institute, this distinction matters enormously. A general liability policy would leave you personally responsible for repairing your storefront after a hail storm or replacing equipment destroyed by fire, while a BOP would cover those losses.

This represents the difference between recovering from a disaster and facing potential business closure.

Where Your Real Exposure Lies

For most Dallas business owners, the exposure you should worry about most is not just lawsuit risk but asset risk. If you operate from a physical location, own equipment, carry inventory, or depend on continuous operations to generate income, general liability alone creates dangerous gaps. Consider a retail business in Dallas with 50,000 dollars in inventory and a 10,000 dollar monthly payroll. If a fire forces temporary closure for three weeks, general liability pays zero toward lost income or ongoing expenses. A BOP with business interruption coverage would reimburse that lost revenue and help keep your employees paid. According to NOAA, Texas businesses faced approximately 1.2 billion dollars in interruption losses from severe weather in 2024, yet many companies carried only general liability and absorbed those losses themselves. The cost difference between the two options makes this protection affordable-a BOP typically runs 500 to 2,000 dollars annually while general liability alone costs 100 to 500 dollars, meaning property and income protection adds roughly 400 to 1,500 dollars per year depending on your business size and location.

Matching Coverage to Your Business Model

The right choice depends entirely on your business structure and asset exposure. If you work as a freelance consultant, graphic designer, or home-based professional with minimal physical assets and no customer foot traffic, general liability provides the third-party protection you actually need at lower cost. You face lawsuit risk from clients claiming poor work quality or bodily injury claims, but you do not face property loss risk because your business does not depend on a physical location. Conversely, if you operate a salon, dental office, restaurant, construction company, or any business with a physical location and equipment, a BOP becomes the smarter investment. Dallas landlords frequently require commercial property insurance as part of lease agreements, and a BOP satisfies that requirement while providing the protection you genuinely need. The cost difference between purchasing policies separately and buying a BOP reflects real pricing from Dallas-area carriers. Additionally, a BOP streamlines your insurance management by consolidating three separate policies into one renewal date, one set of terms, and one claim process, reducing administrative complexity when you already manage dozens of business decisions daily.

Final Thoughts

Choosing between business owners insurance vs general liability comes down to what your business owns and what it needs to survive. If you operate from a physical location, carry inventory, maintain equipment, or depend on continuous operations to generate revenue, a BOP protects your assets and income simultaneously. General liability alone leaves you exposed to property damage and income loss that could force temporary closure or worse.

A BOP typically costs 500 to 2,000 dollars annually while general liability alone runs 100 to 500 dollars, meaning comprehensive protection adds roughly 400 to 1,500 dollars per year. That investment prevents catastrophic losses that could exceed your annual revenue, and most Dallas landlords require commercial property insurance anyway (which a BOP satisfies while protecting you at the same time). The cost difference between these options is smaller than most business owners expect.

We at Brooks Cannon Insurance Group help Dallas business owners evaluate their specific risks and match them to the right coverage. Our team works with multiple carriers to find policies that fit your business model and budget, so contact us today to discuss whether a BOP or general liability makes sense for your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation