Running a sole proprietorship means your personal assets are on the line if something goes wrong. One lawsuit or accident could wipe out your savings and business in one blow.

Sole proprietor general liability insurance protects you from exactly that risk. At Brooks Cannon Insurance Group, we help Dallas business owners understand what coverage they actually need and how to get it affordably.

What General Liability Insurance Actually Covers

General liability insurance for sole proprietors covers three main categories of risk that can financially devastate your business and personal life. The first is bodily injury-if a client gets hurt on your job site or at your office, your policy pays their medical bills, lost wages, and legal costs if they sue. The second is property damage, meaning if you accidentally damage a client’s equipment, building, or belongings while performing work, your coverage handles repair or replacement costs. The third is legal defense, which means the insurance company pays your attorney fees even if a claim has no merit, protecting your cash flow from the moment a lawsuit is filed. Without coverage, you pay these expenses directly from your personal bank account.

Medical Expenses and Bodily Injury Claims

A customer slips in your office or gets injured while you perform a service, and medical expenses add up fast. General liability covers emergency room visits, ongoing treatment, rehabilitation, and sometimes even lost income for the injured person. The policy also covers your legal defense if they decide to sue, which Dallas-area sole proprietors should take seriously since studies show that about half of small businesses face litigation each year. Your coverage limit determines how much the insurance company will pay for a single incident; most Dallas businesses should carry at least $500,000 to $1 million per occurrence according to SBA recommendations. If you work under a contract with larger clients, they’ll often require proof of these minimum limits before you start any work.

Property Damage Claims

Property damage claims happen when your work accidentally harms a client’s belongings.

You’re a contractor and accidentally break a window, damage flooring, or harm equipment-your policy covers the cost to repair or replace it. Legal defense costs are included in your coverage, meaning the insurance company assigns an attorney to defend you if someone sues, and they pay those legal bills separate from your coverage limits in most policies. This matters because legal defense alone can cost $5,000 to $50,000 or more before a case even goes to trial.

Advertising Injury Protection

Advertising injury coverage is included in most general liability policies, protecting you if someone claims your marketing materials infringe on their trademark or copyright. In Dallas, where businesses frequently work on multiple projects with different clients, this protection matters. You operate without the constant fear that one mistake will bankrupt you personally. The next step is understanding why this coverage isn’t optional-it’s a business necessity that protects both your operations and your personal wealth.

Why Sole Proprietors Face Real Financial Risk Without Coverage

Lawsuits Cost More Than Most Dallas Owners Expect

Lawsuits against small business owners happen far more often than most Dallas sole proprietors realize. The U.S. Chamber Institute for Legal Reform estimates that small businesses face about $20,000 per year in tort liability costs on average, and the SBA reports that 36 to 53 percent of small businesses face litigation in any given year. Without general liability insurance, you pay every penny of those costs from your personal bank account.

A single client injury claim or property damage lawsuit can drain your personal savings, force you to sell assets, or even push you toward bankruptcy. That’s not theoretical risk-it’s a documented pattern affecting thousands of small business owners. General liability insurance transfers that financial burden to an insurance company instead of leaving it on your shoulders.

Client Contracts Now Require Proof of Coverage

Many Dallas business owners don’t realize that clients and contractors now routinely require proof of general liability coverage before they’ll work with you. Larger companies, property managers, and government agencies won’t hire a sole proprietor without a certificate of insurance showing minimum coverage limits, typically $500,000 to $1 million per occurrence. If you can’t provide that proof, you lose the contract entirely. This requirement has become standard across industries, meaning your ability to compete directly depends on having the right insurance in place.

The Real Cost of Coverage Versus the Cost of a Lawsuit

The cost difference between carrying coverage and going without it is far smaller than most people think. In Texas, general liability insurance cost for small businesses in Texas ranges from $27 to $2,298 monthly depending on your industry, location, and business size. That’s a small price compared to a single lawsuit that could cost $50,000, $100,000, or more in legal fees and damages. Most Dallas business owners spend more on office supplies or vehicle maintenance than they do on liability protection, yet this coverage protects everything they’ve built.

Your Personal Assets Are Directly Exposed

As a sole proprietor, your personal assets-your home, savings, and investments-are directly exposed to business claims because the law doesn’t separate you from your business the way it does for corporations or LLCs. A judgment against your business is a judgment against you personally. General liability insurance creates that legal separation by making the insurance company responsible for claims instead of your personal bank account. This protection becomes even more critical when you understand how quickly legal costs accumulate and how aggressively injured parties pursue compensation.

Understanding these financial risks is the first step toward protecting your business. The next question is how to select the right coverage limits and policy options that actually match your specific exposure.

How to Choose the Right General Liability Coverage

Calculate Your Coverage Limits Based on Business Exposure

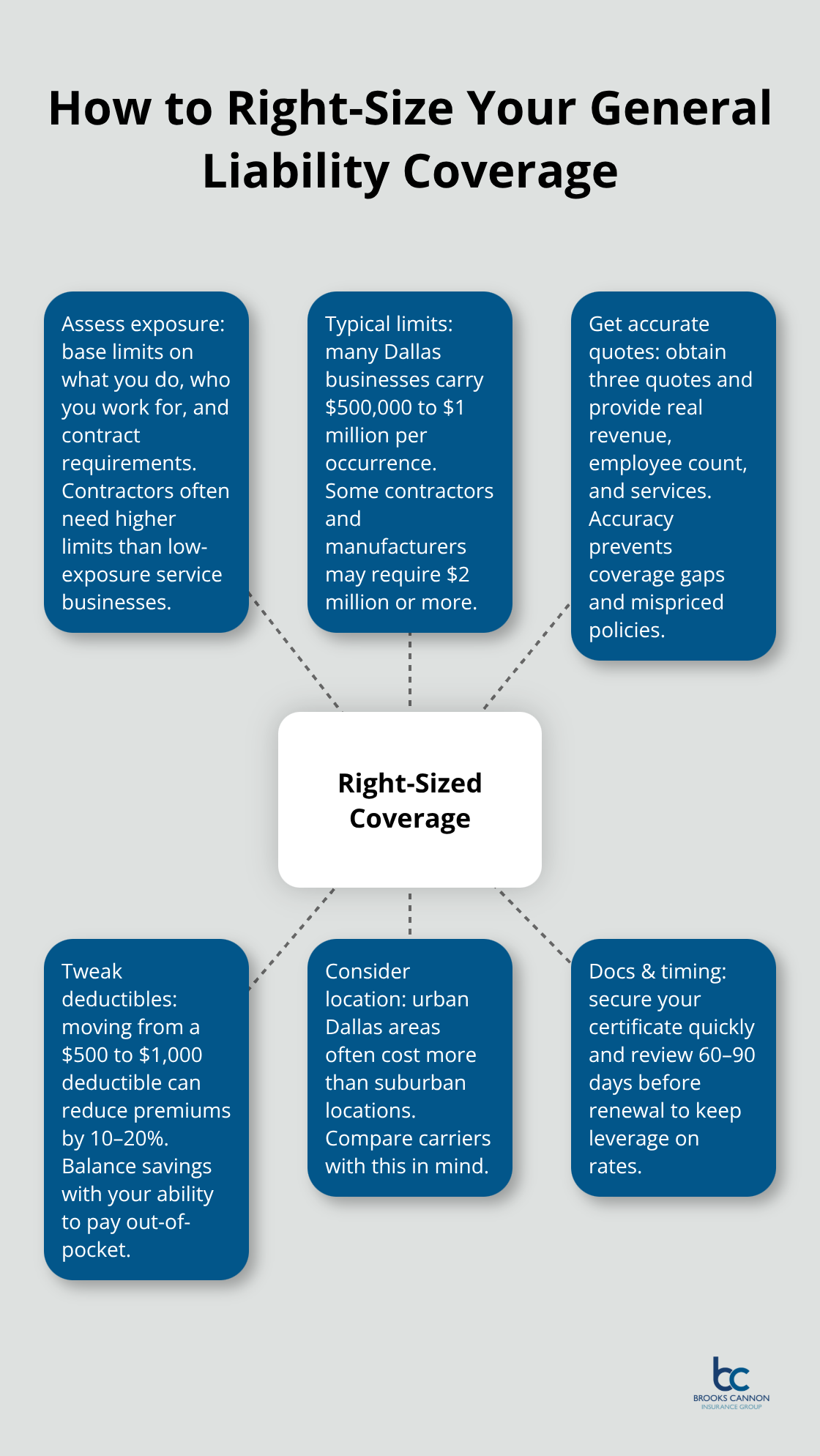

The biggest mistake Dallas sole proprietors make when buying general liability insurance is guessing at coverage limits instead of calculating them based on actual business exposure. The SBA recommends $1 million in general liability coverage for most small businesses, though contractors and manufacturers often need $2 million or more. Your actual coverage needs depend on three concrete factors: what you do, who you work for, and what contracts require. If you work for property managers or larger contractors, many will demand $1 million per occurrence and $2 million aggregate before you step foot on a job site. Construction businesses in the Dallas area typically need higher limits because property damage claims run larger-a contractor accidentally damaging a client’s flooring or structural elements can easily exceed $500,000. Service businesses with minimal property exposure might operate safely at $500,000 per occurrence. The gap between these two scenarios is enormous, and picking the wrong number either leaves you unprotected or wastes money on coverage you don’t need.

Gather Accurate Information for Your Quotes

Obtain three quotes from different insurers before committing to any policy, and provide accurate information about your annual revenue, number of employees, and specific services. Accuracy matters because incomplete details lead to quotes that don’t reflect your real risk, and you’ll discover gaps only after a claim is denied. General liability insurance premiums for sole proprietors in Texas average around $76 monthly according to MoneyGeek data, but this varies dramatically by industry-pressure washing costs about $928 monthly while travel agencies run $21 monthly.

Adjust Your Deductible to Control Monthly Costs

Your deductible choice directly impacts your monthly cost; raising it from $500 to $1,000 typically reduces premiums by 10 to 20 percent. Location within the Dallas area also affects pricing, with urban core locations generally costing more than suburban areas. When comparing quotes, don’t just look at monthly cost-examine what’s excluded, whether defense costs count toward your limit, and if the policy includes advertising injury protection. The Hartford and ERGO NEXT consistently offer competitive rates in Texas markets.

Secure Your Certificate of Insurance Quickly

Once you’ve selected a carrier and limits, request your certificate of insurance immediately; most insurers now issue them through online portals within hours, though some still require 24 to 48 hours for processing. Plan to review and renew your coverage 60 to 90 days before expiration so you can shop for better rates if your business has changed or your claims history improved.

Final Thoughts

General liability insurance for sole proprietors isn’t optional-it’s the foundation that separates your personal wealth from business risk. The three core protections covered in this guide address bodily injury claims, property damage, and legal defense costs, which are the exact scenarios that bankrupt uninsured business owners every year. Without coverage, a single lawsuit drains your savings and forces you to sell personal assets; with it, the insurance company handles those expenses while you keep operating.

Calculate your actual coverage needs based on what you do and who you work for, then request quotes from at least three different carriers. Most Dallas sole proprietors need $500,000 to $1 million per occurrence, though contracts often demand higher limits. Accuracy matters when you apply-provide real information about your revenue, employees, and services so quotes reflect your actual risk.

We at Brooks Cannon Insurance Group work with multiple top-rated carriers to find sole proprietor general liability insurance that matches your specific exposure and budget. Our licensed team understands Dallas business risks and can help you avoid both underinsurance and overpaying for coverage you don’t need. Contact us today to discuss your protection strategy and get competitive quotes.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation