Running a business in Dallas means protecting yourself from unexpected financial losses. General liability insurance and errors and omissions coverage are two distinct protections that work together to shield your company from different types of claims.

At Brooks Cannon Insurance Group, we help business owners understand which coverage types they actually need. This guide walks you through assessing your risks, getting quotes, and selecting the right policies for your situation.

How General Liability and Errors and Omissions Coverage Protect Your Business

General Liability Covers Physical and Reputational Harm

General liability insurance protects against third-party bodily injury, property damage, and advertising injuries. A customer slips on your floor, your equipment damages a client’s building, or someone accuses you of defamation in your marketing-general liability covers these situations. The policy pays for medical expenses, legal defense, court costs, and settlements when someone sues you for these physical or reputational harms.

Errors and Omissions Protects Against Professional Mistakes

Errors and omissions insurance protects against financial losses caused by your professional mistakes or failures to deliver services properly. A tax preparer miscalculates a client’s deductions, or a consultant fails to meet contractual obligations-E&O covers the financial damages that result. This coverage does not apply to bodily injury or property damage. About 60 percent of professional-service firms faced at least one liability claim in the last five years, with average legal costs around $25,000 per case according to the National Association of Insurance Commissioners.

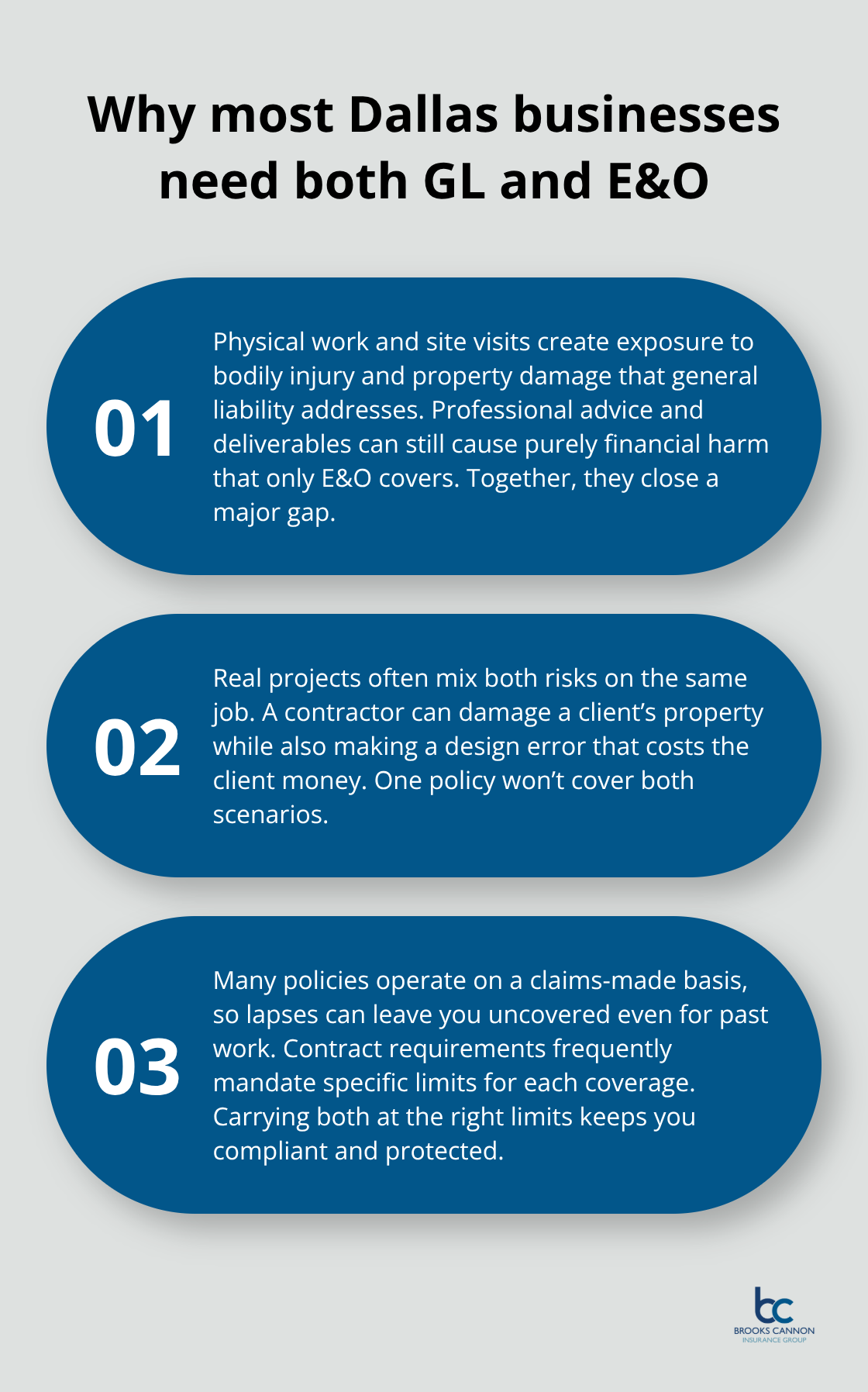

Most Dallas Businesses Need Both Coverages

Most Dallas business owners need both coverages working together. If you visit client property, handle client assets, provide professional services, or sell products, you face both types of risk simultaneously. A contractor might cause property damage (general liability) and also commit a design error that costs the client money (errors and omissions). A tech consultant might damage equipment on-site (GL) and recommend faulty software that disrupts the client’s operations (E&O). Dallas Chamber of Commerce data shows about 65 percent of Dallas commercial contracts require certificates of insurance, often with specific minimums for each coverage type.

Many policies operate on a claims-made basis, meaning the incident and the claim must both occur while coverage is active, so lapses in coverage create dangerous gaps.

Coverage Limits Shape Your Premium and Protection

Coverage limits directly affect both your premium and your protection level. General liability policies typically offer limits like $1 million per occurrence and $2 million aggregate, though smaller businesses sometimes choose $1 million/$1 million to reduce cost. Landscapers and contractors typically pay significantly more than consultants because physical work carries higher accident risk. E&O coverage for professionals starts lower-notary E&O in Texas, for example, begins at $2 per month for basic protection. Location matters substantially in Dallas (hailstorms, flash floods, and tornado risk in North Texas push liability costs higher than safer regions). When evaluating limits, align them with what your clients require and what your revenue justifies; carrying too little leaves you personally liable for the gap, while excessive limits waste premium dollars.

Underinsurance Creates Real Financial Exposure

Annual policy reviews catch underinsurance before a loss occurs. Understanding your actual exposure and matching it to appropriate limits protects both your assets and your ability to operate after a loss. This gap between what you think you’re covered for and what you actually carry can devastate your business when a claim arrives. Once you know what coverage you need, the next step involves requesting quotes from multiple carriers and comparing what each policy actually delivers.

What Coverage Limits Actually Fit Your Business

Your Industry Determines Your Baseline Risk

Your industry determines the baseline risk you face, and that drives everything else. Construction contractors in Dallas face fundamentally different exposures than marketing consultants, which means their coverage needs diverge sharply. Contractors encounter property damage claims regularly because they work on client sites and handle equipment that can cause injury or destruction. According to the Bureau of Labor Statistics, construction and manufacturing account for roughly 42 percent of Texas private-sector nonfatal injuries, with about 156,000 cases reported in 2024. This isn’t theoretical-it’s why a general contractor typically pays $100 to $300 monthly for general liability while a consultant might pay $60 to $85 monthly.

Coverage Needs Shift Across Industries

If you’re in construction, you need inland marine coverage for tools and equipment, builder’s risk for projects under development, and surety bonds for contract work. If you’re a tax preparer or real estate agent, errors and omissions coverage becomes non-negotiable because a single miscalculation or missed deadline creates financial liability that general liability won’t touch. If you run a restaurant, you need liquor liability and spoilage coverage. If you manufacture products, product liability and equipment-breakdown coverage matter more than they do for a service-only business. The hard truth is that generic coverage limits work for almost nobody. A coverage limit might be excessive for a small consulting firm but dangerously low for a contractor managing multiple projects worth millions.

Match Coverage Limits to Your Revenue and Contracts

Once you identify your industry category, match your coverage limits to your actual revenue and contract requirements. Progressive data from 2024 shows that new customers pay a median general liability premium of $60 monthly, with average rates hitting $85 monthly-but these are just benchmarks. Your specific rate depends on claims history, time in business, number of employees, and location within Dallas. Hailstorms, flash floods, and tornado risk in North Texas push costs higher than safer regions, so your zip code matters more than many business owners realize.

If clients demand specific coverage limits in their contracts, that decision is made for you-meet their requirement or lose the contract. If no contract specifies limits, align your coverage with your revenue; a business generating $500,000 annually shouldn’t carry the same limits as one generating $5 million. Dallas Chamber of Commerce research shows about 65 percent of local commercial contracts require certificates of insurance with specific minimums, so you’ll need clarity on what your clients actually demand.

Work with an Independent Agent to Compare Options

The most reliable path forward involves requesting quotes from multiple carriers and comparing what each policy actually covers at your chosen limits. Work with an independent agent who accesses multiple carriers rather than a captive agent tied to one insurance company. An independent broker can show you how adjusting coverage limits and deductibles affects your premium, letting you make informed trade-offs instead of guessing.

Document Your Actual Risk Exposure

Your current risk exposure becomes visible only after you document what you own, who works for you, where you operate, and what your revenue actually is. Skip this step and you’ll either overpay for coverage you don’t need or discover mid-claim that you’re underinsured by hundreds of thousands of dollars. Once you have this information in hand, requesting quotes from multiple carriers reveals exactly what protection costs and what gaps exist in your current approach.

Getting Quotes and Comparing Policies

Gather Your Business Information First

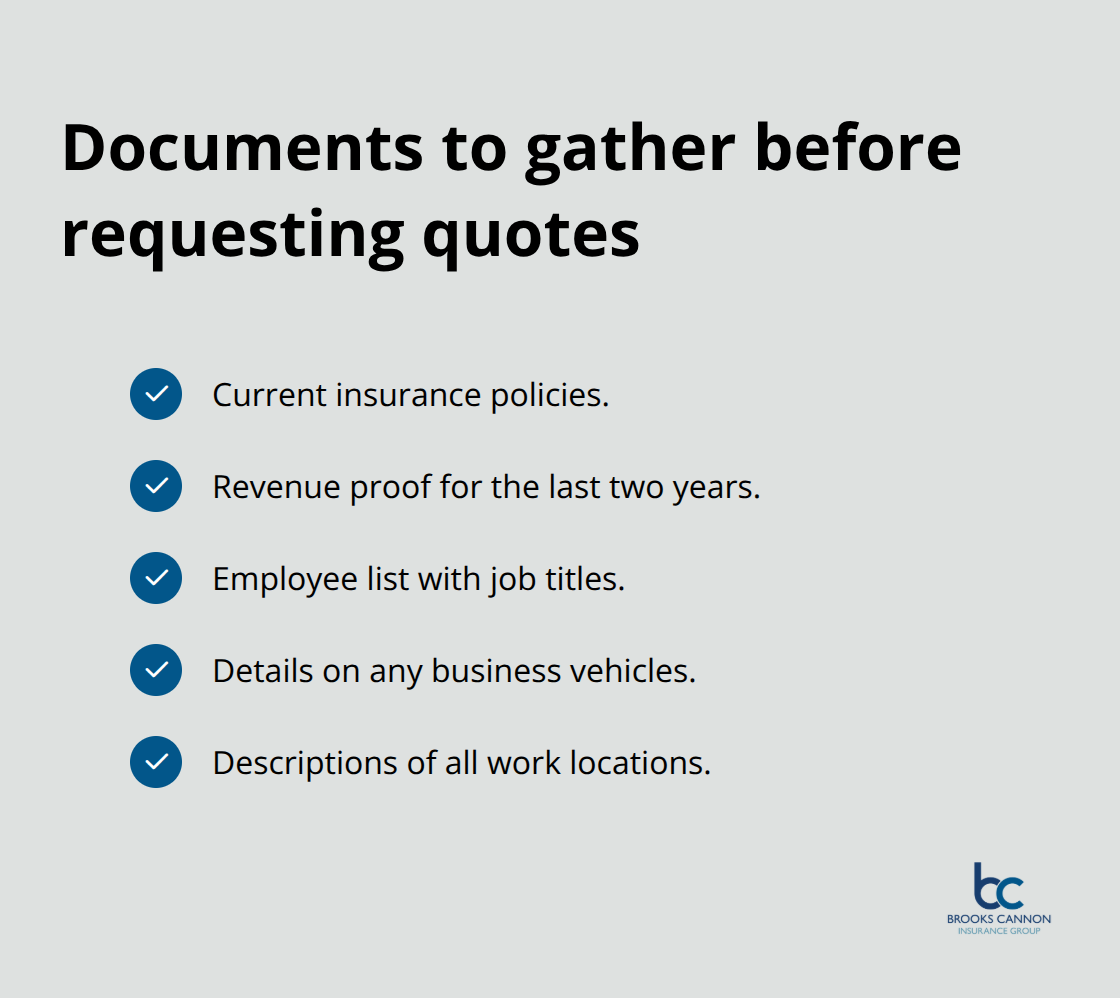

Requesting quotes from multiple carriers reveals what protection actually costs and where gaps exist in your current approach. Start by collecting your business documentation: current insurance policies, proof of revenue from the last two years, a list of employees and their job titles, details about any vehicles used for business, and descriptions of your work locations. Provide this information consistently to all carriers so the quotes remain comparable. Many carriers offer online quote tools that deliver estimates within minutes, though phone quotes often allow agents to explain exclusions and endorsements that affect real-world coverage.

Understand What Drives Your Quote Price

General liability insurance costs depend on your industry classification code, annual revenue, and employee count. A landscaper with three employees and a clean safety record receives a vastly different quote than a construction contractor with ten employees and a prior claim, even if both request identical coverage limits. Location matters substantially-hailstorms, flash floods, and tornado risk in North Texas push liability costs higher than safer regions.

Compare Coverage, Not Just Price

When you receive quotes, compare what each policy actually covers at your chosen limits, what exclusions apply, what deductibles you’d pay out-of-pocket, and whether the policy includes any automatic endorsements or restrictions that surprise you later. Price alone tells you nothing about whether you’re protected. Two policies at the same premium can offer dramatically different coverage when a claim arrives.

Work with an Independent Agent

An independent agent with access to multiple carriers beats a captive agent tied to one company. An independent broker shows you how adjusting your coverage limits between $1 million and $2 million aggregate affects your premium, or how raising your deductible from $500 to $1,000 reduces your annual cost. This transparency lets you make informed trade-offs instead of defaulting to whatever a single carrier offers. Ask each agent whether they’ve placed coverage with other Dallas businesses in your industry and what common claims they’ve observed. A contractor’s agent who handles dozens of construction projects annually spots coverage gaps that a generalist misses.

Verify Contract Requirements and Timeline

After comparing quotes, verify that certificate of insurance requirements in your client contracts align with the limits you’re considering. Dallas Chamber of Commerce data shows roughly 65 percent of Dallas commercial contracts demand certificates of insurance, often with 24-hour turnaround for updates. Requesting quotes takes an afternoon, comparing them takes another hour, and signing up for the right policy takes less than 24 hours once you decide. The cost of requesting multiple quotes is zero. The cost of being underinsured by hundreds of thousands of dollars is catastrophic.

Final Thoughts

General liability insurance and errors and omissions coverage protect your Dallas business from the financial devastation that follows a claim. General liability covers the physical injuries and property damage that occur on your watch, while E&O protects you when your professional work causes financial harm to a client. Skipping either one exposes you to lawsuits that drain your business bank account and threaten your ability to operate.

Document what your business owns, who works for you, where you operate, and what your revenue is. Request quotes from multiple carriers so you can see exactly what protection costs and what gaps exist in your current approach. Compare the actual coverage each policy delivers, not just the price tag, and verify that your chosen limits satisfy what your client contracts demand.

Work with an independent agent who understands your industry and your local Dallas market-they show you options that a captive agent tied to one company cannot. Brooks Cannon Insurance Group works with multiple top-rated carriers to find the coverage and pricing that fit your specific situation. The cost of getting general liability insurance and errors and omissions coverage right is minimal, but the cost of being underinsured when a claim arrives is catastrophic.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation