A single customer slip-and-fall accident can cost your business $50,000 or more in legal fees and damages. Without proper protection, these incidents threaten your company’s financial stability.

General liability insurance shields businesses from bodily injury claims, property damage lawsuits, and advertising disputes. We at Brooks Cannon Insurance Group help Dallas area businesses understand why this coverage forms the foundation of smart risk management.

What General Liability Insurance Covers

General liability insurance protects your business against three major categories of claims that can devastate your finances. This coverage forms the backbone of business protection, addressing the most common risks that face Dallas area companies every day.

Bodily Injury and Property Damage Protection

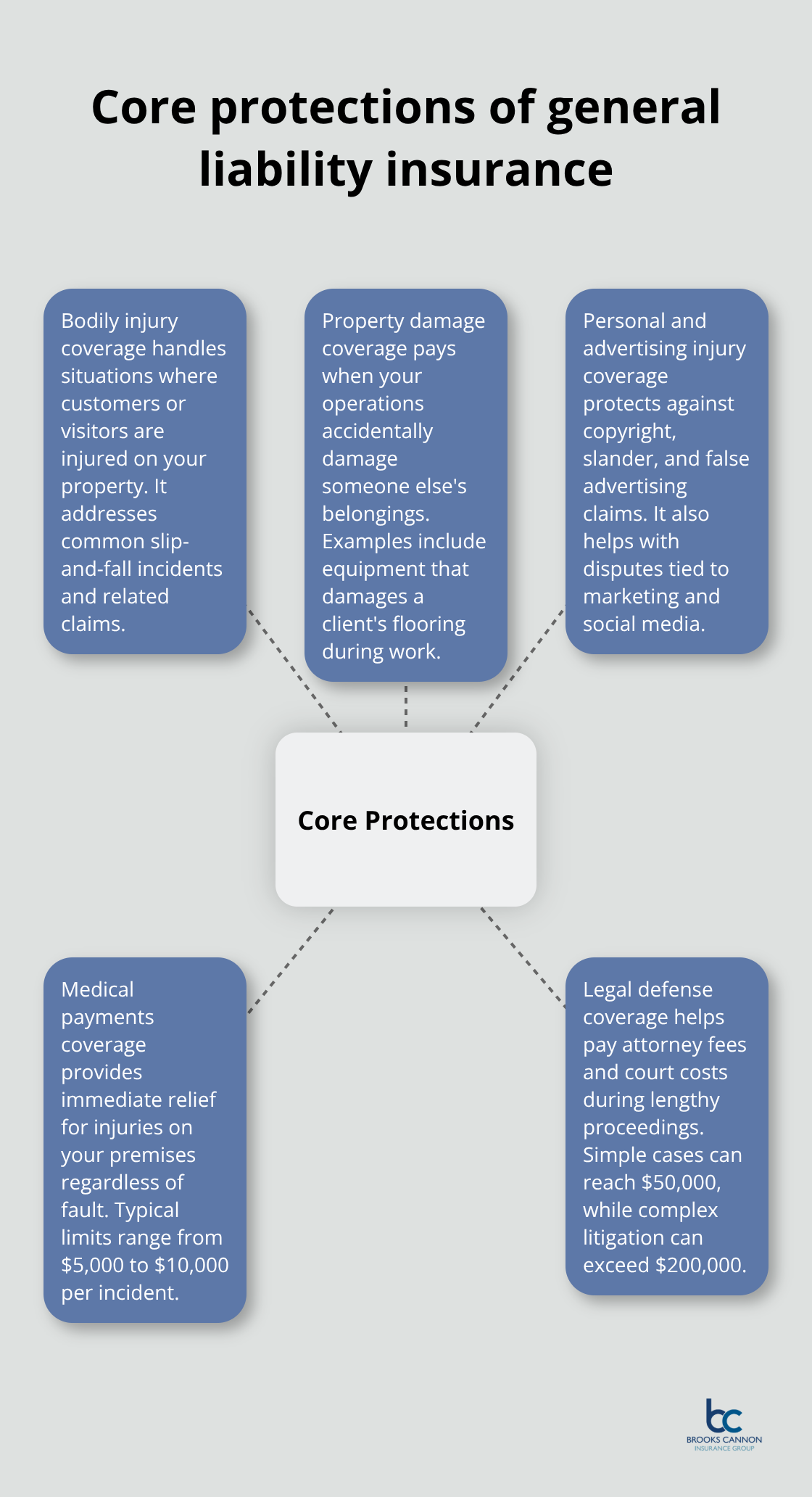

Bodily injury coverage handles situations where customers or visitors get hurt on your property. Slip-and-fall incidents account for a significant portion of all claims according to industry data, with settlements varying widely based on case specifics. Property damage coverage pays when your business operations accidentally damage someone else’s belongings, like a contractor’s equipment that damages a client’s expensive flooring during installation work.

Personal and Advertising Injury Claims

Personal and advertising injury protection covers lawsuits from copyright infringement, slander accusations, or false advertising claims. These disputes can cost businesses thousands in legal defense alone, even when the accusations prove groundless. Social media posts, marketing materials, and customer interactions all create potential exposure that this coverage addresses.

Medical Expenses Coverage

Medical payments coverage provides immediate financial relief when someone gets injured on your premises, regardless of fault. This coverage typically ranges from $5,000 to $10,000 per incident and helps maintain customer relationships by covering emergency room visits or minor treatments. Texas businesses report that quick medical payment responses prevent many incidents from escalating into larger lawsuits.

Legal Defense Costs

Defense costs represent the hidden expense that destroys business budgets. Legal fees alone can reach $50,000 for simple cases, with complex litigation exceeding $200,000 in attorney fees (even when you win the case). Your policy covers these expenses during lengthy legal proceedings that can drag on for months or years. Understanding why every business needs this protection becomes clear when you consider the financial risks that lurk in daily operations.

Why Your Business Cannot Survive Without This Protection

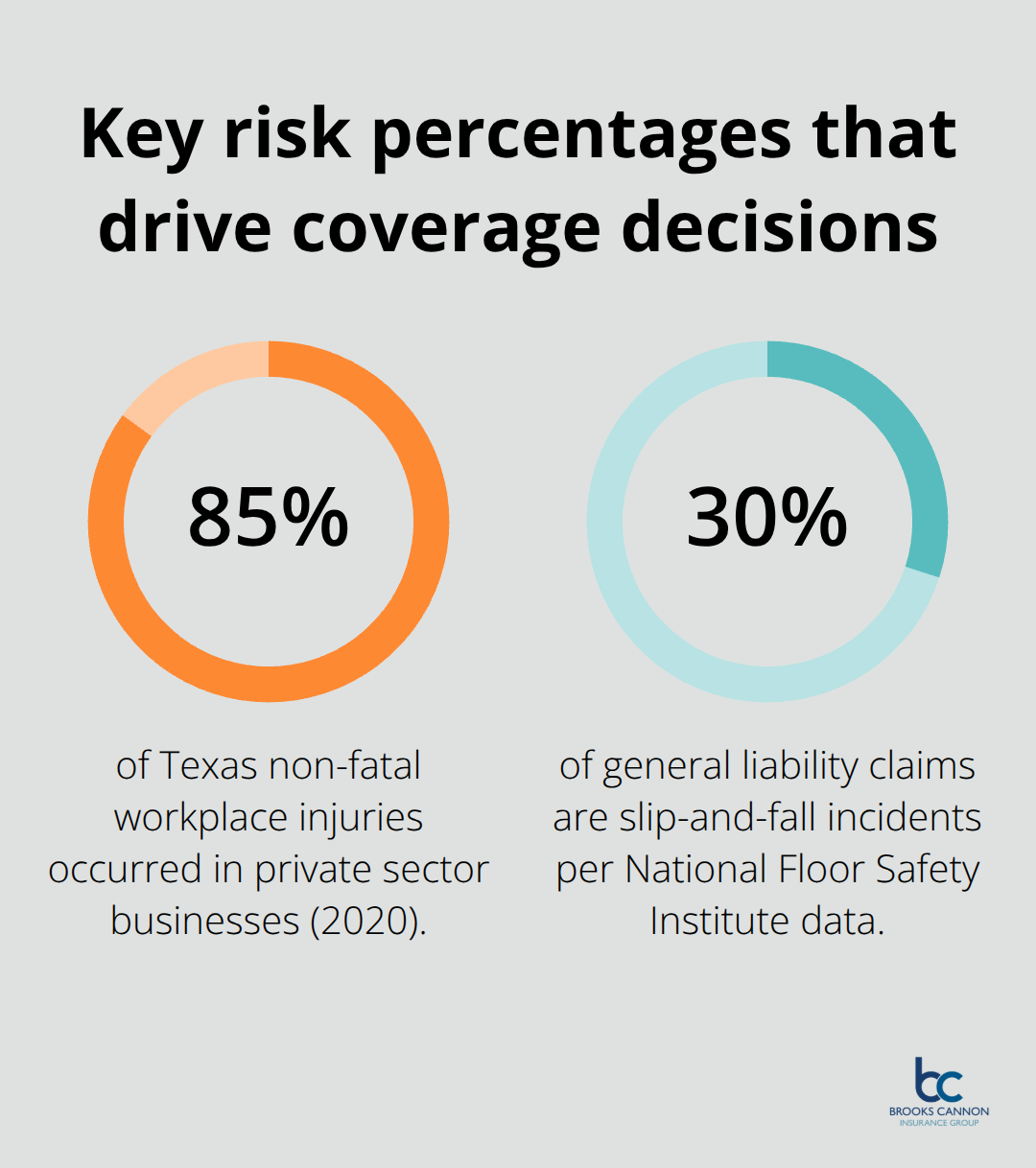

Dallas businesses face mounting financial risks that can destroy decades of hard work in a single incident. The Texas recorded 210,000 non-fatal workplace injuries in 2020, with over 85% occurring in private sector businesses. These numbers translate into real financial consequences for business owners who lack adequate protection.

Customer Accidents Create Immediate Financial Exposure

A restaurant patron who slips on a wet floor can generate legal costs that exceed $75,000, even when the business follows proper safety protocols. Retail stores face similar risks when customers trip over merchandise or sustain injuries from displays that fall. The National Floor Safety Institute data shows that slip-and-fall incidents represent 30% of all general liability claims, which makes this the most common threat that faces Dallas area businesses. Medical bills alone can reach $25,000 for emergency room treatment and follow-up care, while lost wages and pain-and-suffering damages multiply these costs significantly.

Contract Requirements Make Coverage Mandatory

Commercial property leases in Dallas typically require $1 million in general liability coverage before landlords approve rental agreements. Government contractors must provide proof of coverage to bid on public projects, with many that require $2 million aggregate limits. Banks and lenders demand insurance verification before they approve business loans, and they treat coverage as collateral protection for their investments. Professional service providers lose client opportunities when they cannot demonstrate adequate protection, as corporate clients refuse to work with uninsured vendors due to their own risk management policies.

Frivolous Lawsuits Drain Resources Regardless of Merit

Legal defense costs begin to accumulate the moment someone files a lawsuit against your business, regardless of claim validity. Attorney fees range from $300 to $600 per hour in the Dallas market, with simple cases that require 100-200 hours of legal work before resolution. Businesses without coverage often settle meritless claims for $15,000 to $30,000 rather than spend $50,000 to fight in court. Insurance companies have legal teams specifically trained to defend against frivolous claims, and they provide expertise that individual business owners cannot match when they face aggressive plaintiff attorneys. The right coverage selection becomes essential when you consider these financial realities and the specific risks that your industry presents.

At a very high level, General Liability insurance protects your business from customers who are injured or property that is damaged as a result of the services you provide. This protection becomes the foundation that allows your business to operate with confidence while managing the inevitable risks that come with serving customers in today’s litigious environment.

How to Choose the Right General Liability Coverage

Appropriate general liability coverage requires careful analysis of your business revenue, industry risks, and contract obligations. Most Dallas businesses start with $1 million per occurrence and $2 million aggregate limits, which costs approximately $40 to $60 per month. However, restaurants and contractors often need $2 million per occurrence due to higher accident frequency, while professional service firms can sometimes operate safely with $500,000 limits if they maintain separate errors and omissions coverage.

Calculate Coverage Based on Revenue and Assets

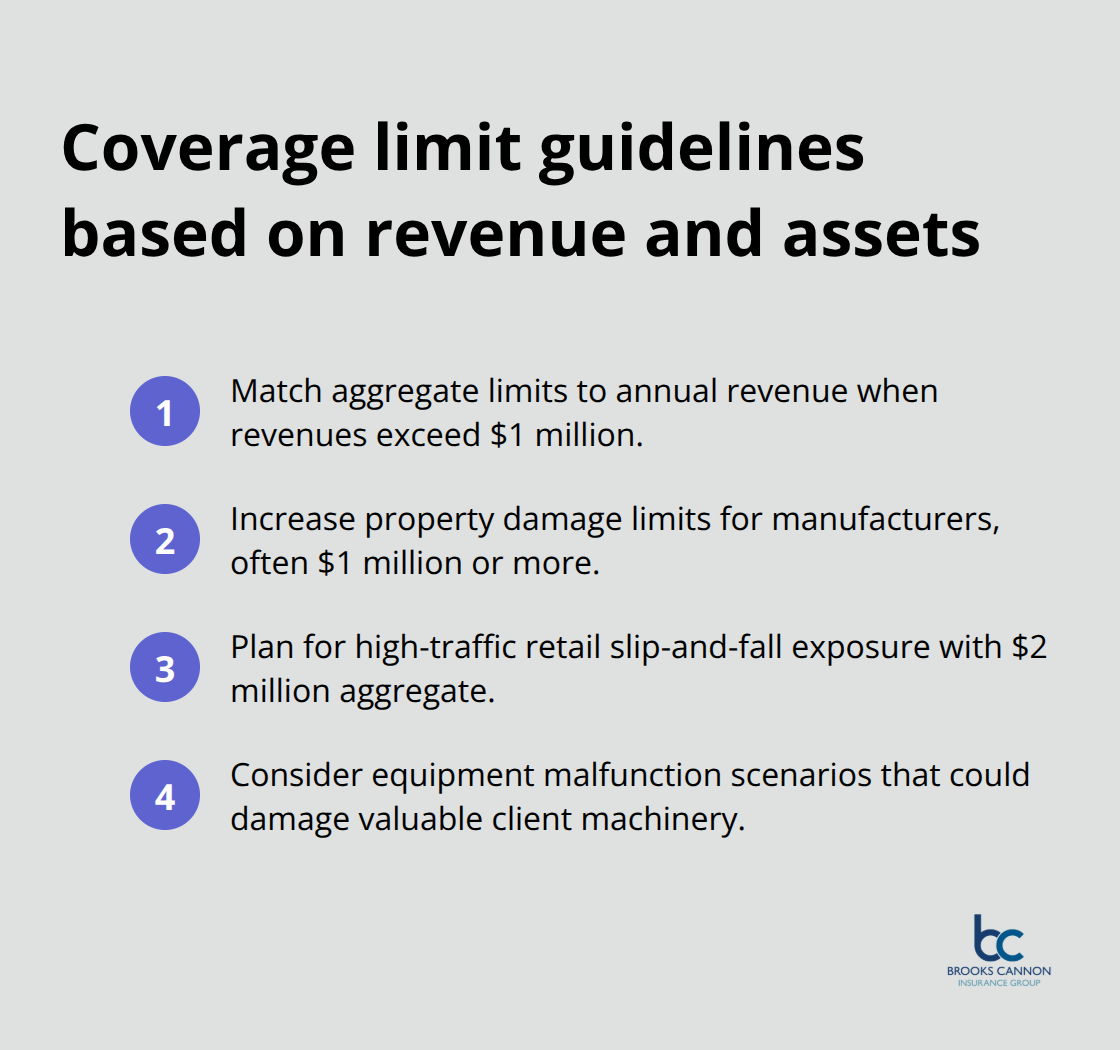

Your coverage limits should reflect your business’s financial exposure rather than minimum legal requirements. Companies with annual revenues that exceed $1 million typically need aggregate limits that match or exceed their yearly income, as successful businesses become attractive lawsuit targets. Manufacturing businesses with expensive equipment require higher property damage limits (often $1 million or more), because a single equipment malfunction can destroy valuable client machinery. Retail businesses in high-traffic Dallas locations face increased slip-and-fall risks and benefit from $2 million aggregate coverage, particularly when customer volume multiplies accident potential.

Industry Risk Factors Determine Premium Costs

Construction companies pay the highest premiums, with costs that average $1,500 to $5,000 annually due to constant physical hazards and equipment operation risks. Restaurants face grease fires, food poisoning claims, and slip hazards that generate frequent claims, which makes comprehensive coverage essential despite higher costs. Technology companies typically pay lower premiums but need cyber liability additions since general liability excludes data breaches and digital asset damage. Healthcare providers require professional liability coverage alongside general liability, as medical malpractice claims fall outside standard business coverage and can exceed $1 million in damages.

Independent Agents Provide Market Access

Independent agents give you access to multiple insurance carriers rather than single-company limitations. These professionals compare rates from top-rated carriers to find optimal coverage combinations that balance protection with affordability. Independent agents understand Dallas market conditions and can identify carriers that specialize in your industry, which often results in better rates and claims handling. Captive agents represent single companies and cannot provide market comparisons, which limits your options and potentially increases costs when your business faces unique risk factors.

Final Thoughts

General liability insurance represents the most fundamental protection that Dallas businesses need to survive in today’s legal environment. A single customer accident or property damage claim can bankrupt years of hard work and investment without this coverage. The monthly cost of $40 to $60 provides exceptional value when compared to potential lawsuit expenses that regularly exceed $100,000.

Smart business owners recognize that general liability insurance functions as cost-effective risk management rather than an unnecessary expense. This protection allows you to focus on growth instead of worrying about financial catastrophe from everyday operational risks. The peace of mind that comes from knowing your business can weather unexpected claims proves invaluable for long-term success.

Professional insurance agents who understand Dallas market conditions help you secure the right coverage quickly. We at Brooks Cannon Insurance Group work with multiple top-rated carriers to find optimal protection that fits your budget and industry requirements (our licensed experts provide personalized service and competitive rates). Contact us today to protect your business with confidence.