Roofing work exposes your business to serious liability risks. One accident on a job site can result in costly lawsuits and medical bills that threaten your entire operation.

General liability insurance for roofers protects you from these financial disasters. At Brooks Cannon Insurance Group, we help Dallas-area roofing contractors understand their coverage options and build policies that match their actual needs.

What General Liability Insurance Actually Covers

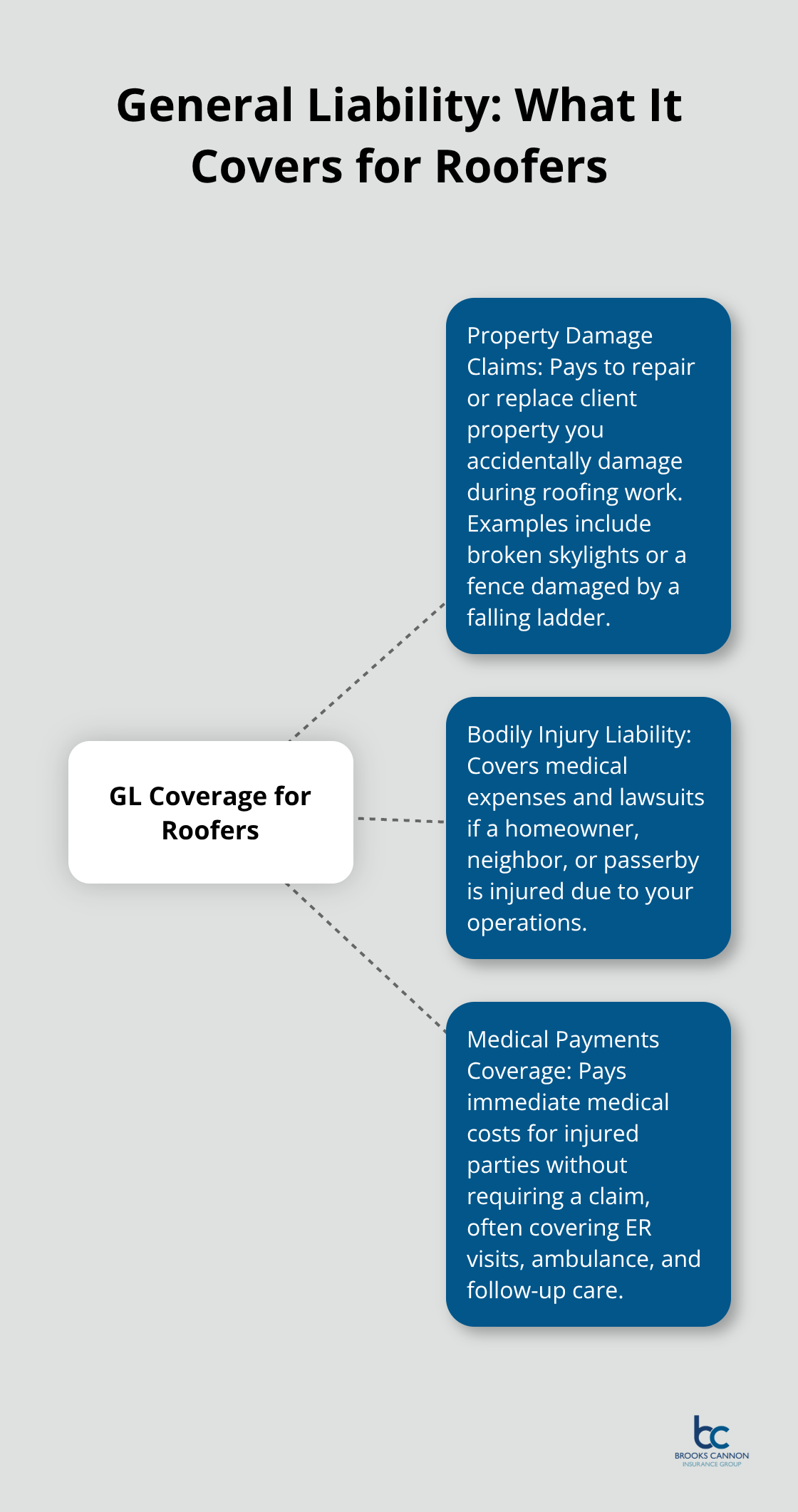

General liability insurance for roofers covers three critical areas when someone is injured or property is damaged during your work.

Property Damage Claims

Property damage claims cover situations where you accidentally damage a client’s home, neighboring structures, or their belongings while performing roofing work. If your crew drops materials through a skylight or a falling ladder damages a client’s fence, general liability pays for repairs or replacement. This coverage is essential rather than optional for protecting your business from costly property damage incidents.

Bodily Injury and Medical Payments

Bodily injury liability protects you when someone is injured on the job site. If a homeowner is struck by roofing debris, a neighbor is harmed by your equipment, or a passerby is injured due to your work, this coverage handles their medical expenses and any resulting lawsuit. Medical payments coverage goes further by paying immediate medical costs for injured parties without requiring them to file a claim against you. This approach often prevents minor incidents from becoming major lawsuits and typically covers emergency room visits, ambulance services, and follow-up treatment.

The Real Cost of Skipping Coverage

A single roofing accident can drain your business quickly. If you face a lawsuit and lack general liability insurance, you become personally responsible for defense costs, settlements, and judgments. Legal fees alone can reach significant amounts before any settlement is paid. Dallas-area roofers face additional pressure because weather-related incidents frequently trigger liability disputes about what caused the damage and who pays for it.

Standard Limits and Critical Exclusions

Standard general liability policies for roofers carry limits of $1,000,000 per occurrence and $2,000,000 aggregate. These limits aren’t arbitrary-most client contracts require at least $1 million per occurrence, and many lending institutions won’t finance projects without proof of this coverage level. If you carry lower limits like $500,000 per occurrence, you’ll struggle to win commercial jobs and may face out-of-pocket liability on larger claims. Standard policies often exclude damage that occurs while a roof is exposed during work, which is why roofing contractors need an open-roof endorsement added to their policy. Without this endorsement, weather damage during an active roofing project may fall outside your coverage.

Understanding what your policy covers and what it excludes determines whether your business survives a major incident or faces financial ruin. The next step is understanding why this coverage matters beyond just protection-it’s also what your clients and lenders demand before you ever step foot on a job site.

Why General Liability Insurance Matters for Your Roofing Business

General liability insurance isn’t a luxury or a checkbox item for roofers in Dallas. It’s the difference between staying in business after a serious incident and filing for bankruptcy. The roofing industry faces genuine, measurable risk. According to the National Roofing Contractors Association, roofing businesses face liability claims related to property damage or worker injuries. That’s not a rare scenario-it’s the norm.

The Financial Reality of Uninsured Claims

When a claim hits your business without insurance backing it, you become personally liable for every dollar of damages, legal fees, and settlements. A single roofing accident involving property damage or bodily injury can easily exceed $50,000 to $100,000 in costs before any judgment is paid. Without general liability coverage, that money comes directly from your business account or personal assets. You lose equipment, vehicles, savings, or worse-your home becomes vulnerable to a judgment lien.

Dallas-area roofers face additional pressure because hail and wind damage claims are common in this region. When disputes arise about whether your work or weather caused damage, liability questions follow quickly. Your client’s insurance company may pursue you for costs, and without general liability coverage, you have no legal defense team or settlement funds available.

Client and Lender Requirements Drive Coverage Decisions

Clients and lenders won’t work with uninsured roofers, which means general liability insurance directly impacts your ability to land jobs and secure financing. Most client contracts explicitly require proof of at least $1 million per occurrence in general liability coverage before they’ll let you on their property. Many commercial clients demand $2 million per occurrence. If you show up without this coverage, the job is gone-even if your crew is the most skilled in Dallas.

Lending institutions that finance roofing projects require documented general liability insurance as a condition of the loan. If you’re bidding on any job worth serious money, the client will ask for a Certificate of Insurance before signing anything. When you have general liability insurance in place, you can issue a same-day Certificate of Insurance to clients, which speeds up the bidding process and shows professionalism.

Protecting Your Business Reputation and Personal Assets

Beyond client requirements, general liability insurance protects your business reputation and personal assets. A lawsuit without insurance coverage becomes public record. Unhappy clients talk, and word spreads in the roofing community. Your business reputation suffers permanently. More critically, a judgment against your uninsured business can extend to your personal assets. Creditors can pursue your bank accounts, equipment, vehicles, and in some cases, your home.

General liability insurance creates a legal shield that separates your personal finances from business liability. This protection is non-negotiable for any serious roofing operation in Dallas. Once you understand why this coverage matters, the next critical step involves selecting the right policy limits and exclusions that actually match your specific roofing projects.

How to Choose the Right General Liability Policy

Match Coverage Limits to Your Project Types

Most Dallas roofers default to the industry standard of $1 million per occurrence and $2 million aggregate general liability coverage because those limits appear everywhere in client contracts and lending requirements. This is the right starting point, but it’s only a starting point. Your actual coverage needs depend on the specific types of projects you pursue. A roofer handling residential re-roofing in residential neighborhoods faces different exposure than a contractor managing commercial roof replacements on multi-story office buildings or shopping centers.

For residential work, $1 million per occurrence typically covers most scenarios, but commercial projects often demand $2 million per occurrence or higher. Before you accept a job, ask the client or general contractor exactly what limits they require in writing. Many roofing contractors miss this step and either over-insure (paying for coverage they don’t need) or under-insure (and face rejection when they submit their certificate).

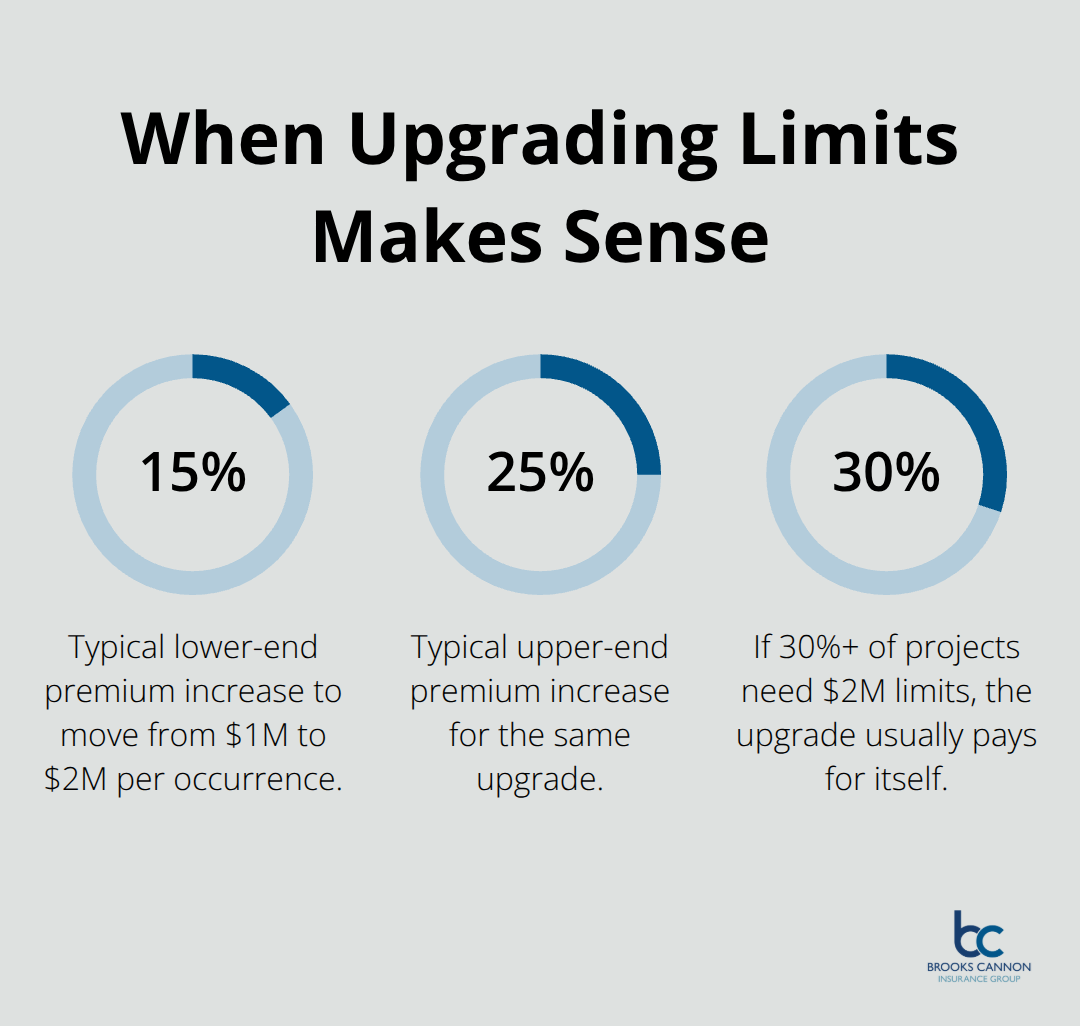

The Texas Department of Insurance reports that general liability and workers compensation coverage are maintained by most RCAT-licensed contractors, with many carrying the $1 million/$2 million standard. That said, upgrading from $1 million to $2 million per occurrence typically costs only 15 to 25 percent more in premiums, making the upgrade worthwhile if you pursue larger commercial contracts regularly. Try this approach: check your actual project pipeline for the next 12 months and ask yourself what percentage of your work requires $2 million coverage. If more than 30 percent of your projects demand higher limits, the upgrade pays for itself through increased job opportunities.

Review Policy Exclusions Before You Bind Coverage

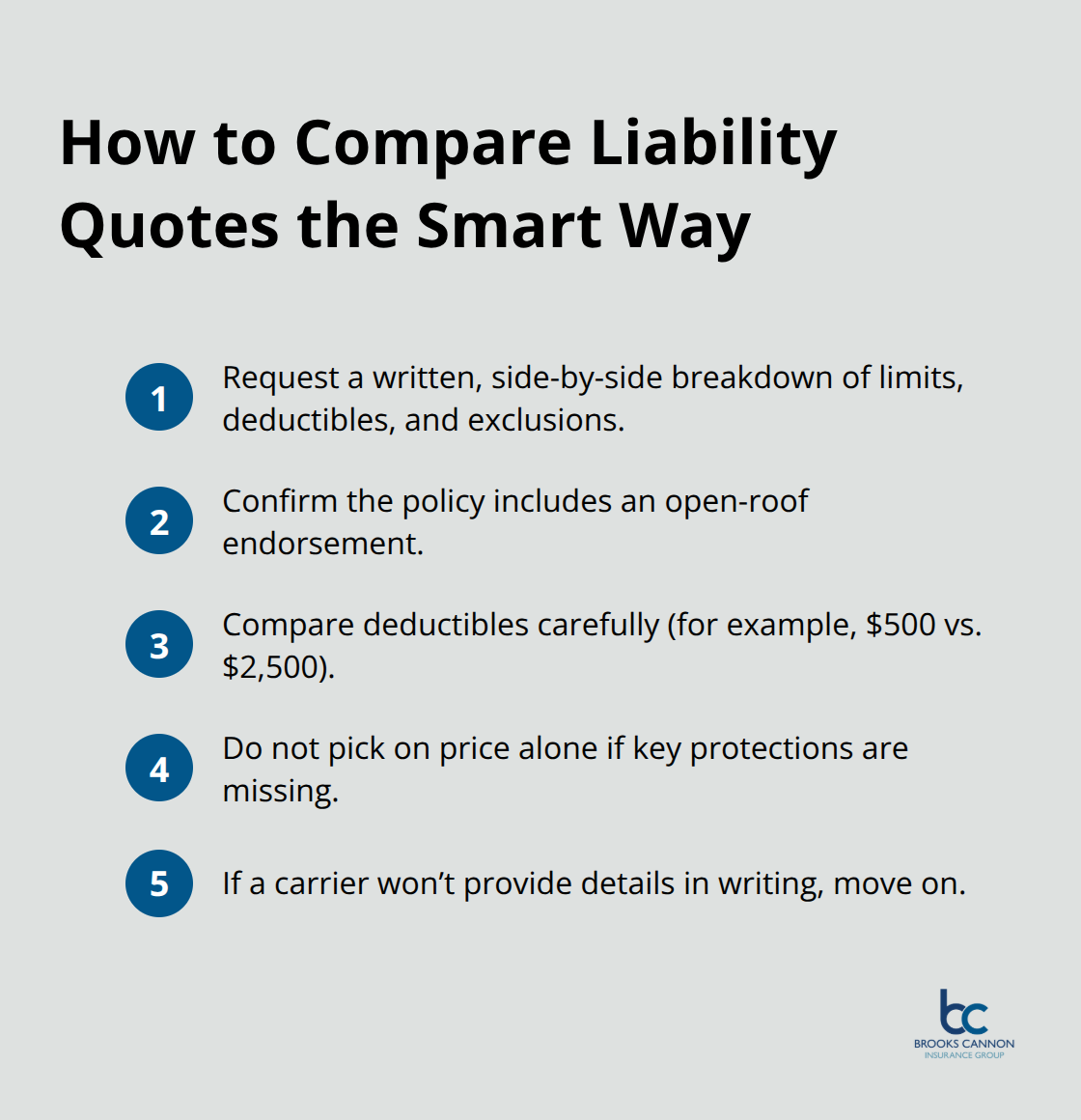

Equally important is reviewing what your policy explicitly excludes before you bind coverage. Standard general liability policies for roofers frequently exclude damage that occurs while a roof is exposed during active work, which is a critical gap for any roofing contractor. You need an open-roof endorsement added to your policy to cover weather damage and other incidents that happen during the roofing process itself. This endorsement is inexpensive but essential.

Additionally, verify whether your policy covers completed operations liability, which protects you against claims that arise after the job is finished. A roof leak discovered three months after completion could trigger a completed operations claim, and without this coverage, you remain unprotected.

Compare Quotes Side by Side

When comparing quotes from multiple carriers, don’t just look at price. A quote that’s $200 per month cheaper means nothing if the policy excludes open-roof damage or has a $2,500 deductible instead of $500. Request a detailed comparison document from each carrier that lists specific coverage limits, deductibles, and exclusions side by side.

If a carrier won’t provide this in writing, move to the next one.

As an independent agency, Brooks Cannon Insurance Group works with multiple top-rated carriers to find coverage that matches your actual roofing operations, not just the cheapest premium available.

Final Thoughts

General liability insurance for roofers protects your finances when accidents happen, satisfies client and lender requirements, and shields your personal assets from judgment liens. Standard limits of $1 million per occurrence and $2 million aggregate form the foundation most roofing contractors need, though your specific projects may demand higher coverage. An open-roof endorsement is non-negotiable because standard policies exclude damage during active roofing work, and completed operations liability protects you against claims that surface months after a job finishes.

Your next step is straightforward: gather your project pipeline for the next 12 months and identify what coverage limits your clients actually require. Request written specifications from general contractors and property owners before you bid work, then compare quotes from multiple carriers using a detailed side-by-side breakdown that shows limits, deductibles, and exclusions clearly. Don’t chase the lowest price alone-a cheap policy with gaps in coverage costs far more when a claim hits.

We at Brooks Cannon Insurance Group understand roofing operations and the specific risks your business faces in the Dallas area. As an independent agency, we work with multiple top-rated carriers to find general liability insurance for roofers that matches your actual roofing work, not generic contractor policies. Contact us to discuss your roofing insurance needs and get a quote that reflects your real exposure.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation