Running a small business in Dallas means juggling countless responsibilities. One decision that shouldn’t be complicated is protecting your company from financial disaster.

A business owners policy combines essential coverage into one affordable package. We at Brooks Cannon Insurance Group help business owners understand what is a business owners policy and why it matters for their bottom line.

What Makes a BOP Different from Buying Insurance Separately

How BOPs Bundle Coverage Into One Package

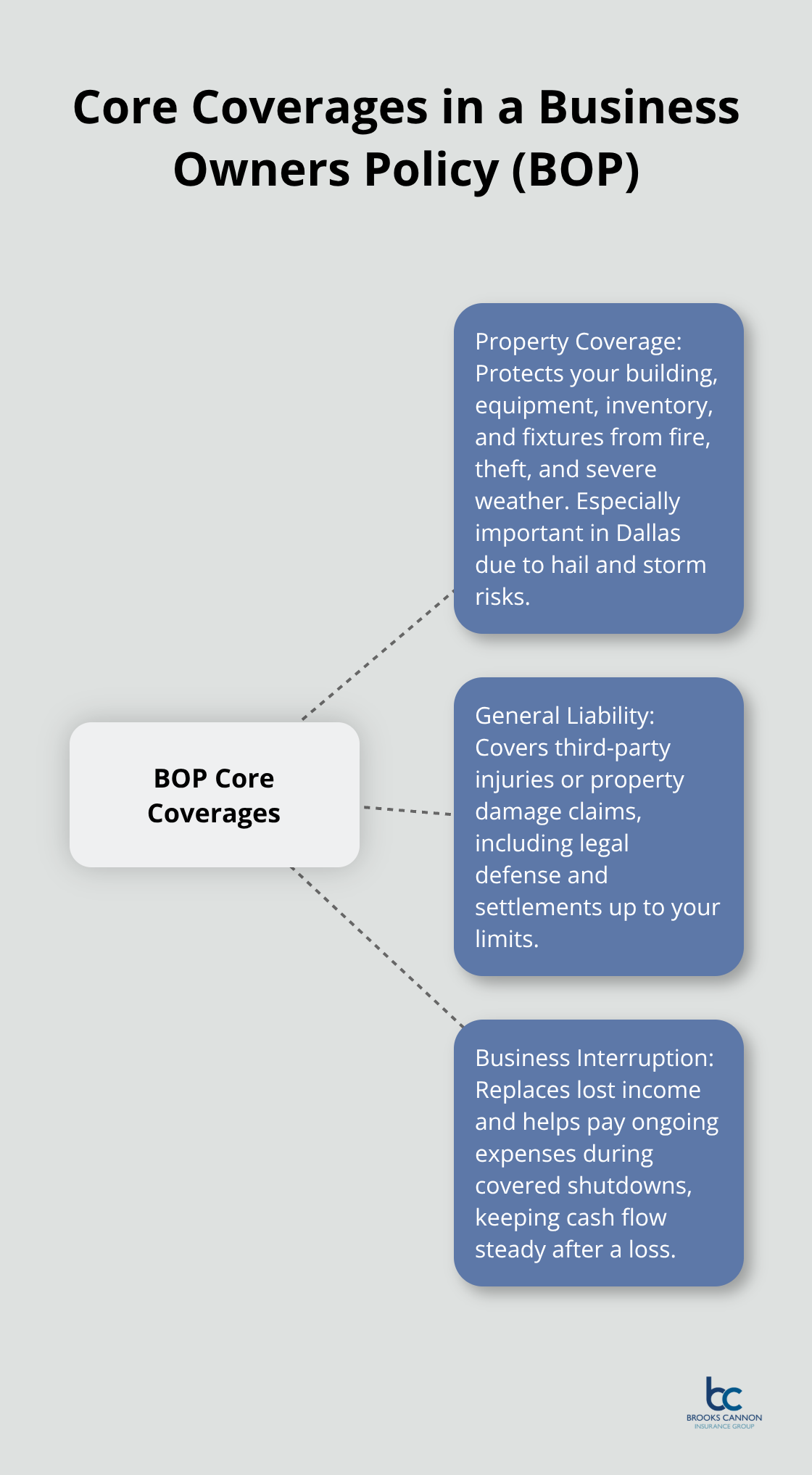

A business owners policy combines property coverage, general liability protection, and business interruption insurance into a single package designed specifically for small and medium-sized businesses. Instead of purchasing three separate policies and managing multiple renewal dates and coverage gaps, a BOP streamlines protection into one coordinated solution. Small businesses make up the vast majority of U.S. businesses, and most operate without adequate coverage because piecing together individual policies feels overwhelming and expensive.

A BOP eliminates that friction by providing standard coverage tiers that address the most common risks business owners face. Property coverage protects your building, equipment, inventory, and fixtures against fire, theft, and weather damage. Liability coverage shields your business when someone gets injured on your property or claims your product or service caused them harm, covering legal fees and settlement costs.

Business interruption coverage replaces lost income if a covered event forces you to temporarily close-which matters tremendously in Dallas where severe weather can disrupt operations for weeks.

Which Businesses Benefit Most from BOPs

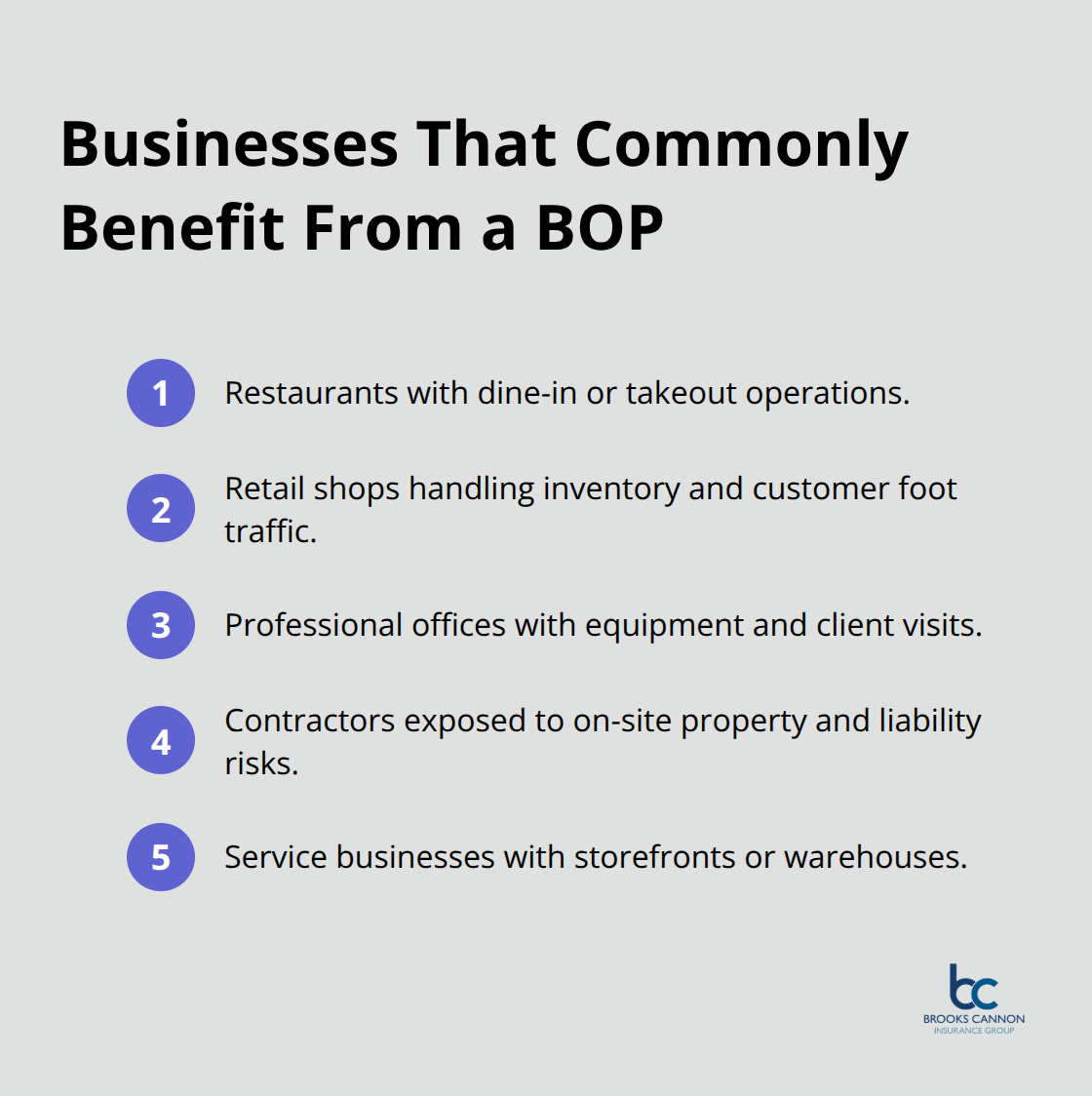

The businesses that benefit most from BOPs are those with physical locations and tangible assets that need protection. Restaurants, retail shops, professional offices, contractors, and service businesses with storefronts or warehouses find BOPs particularly valuable because they face consistent property and liability exposure. These operations typically cannot absorb the financial impact of property damage or liability claims without a coordinated insurance strategy.

The Real Cost Advantage of Bundling

A BOP is fundamentally different from buying general liability and property insurance separately because carriers bundle them with pricing incentives you lose when purchasing individually. When you buy three policies from three different carriers, you pay three separate premiums, three separate deductibles, and coordinate three different claims processes. With a BOP, one deductible applies across most coverage types, one renewal date keeps your protection simple, and one agent manages everything.

Carriers price BOPs aggressively because they retain customers longer and reduce administrative costs. Small businesses in the Dallas area that operate without a BOP typically overpay for coverage or leave themselves dangerously exposed. We at Brooks Cannon Insurance Group work with business owners to structure BOPs that match their actual operations rather than forcing them into generic packages that include coverage they don’t need.

Understanding Your Coverage Options

The specific coverage options available within a BOP vary by carrier and business type, which is why comparing quotes from multiple insurers reveals significant differences in what you actually receive for your premium dollar. Some carriers offer add-ons like cyber liability or employment practices liability that others exclude entirely. Your industry, location, and asset value all influence which coverage options make sense for your situation.

What Your BOP Actually Covers

Property Coverage Protects Your Physical Assets

Property coverage protects the physical assets that keep your business running. This includes your building if you own it, equipment and machinery, inventory, furniture, fixtures, and outdoor property like signs or HVAC units. In Dallas, where hail and severe storms cause significant commercial damage, property coverage matters intensely. Property damage from weather events costs businesses significantly each year.

Your property coverage limit should reflect the actual replacement cost of what you own, not some arbitrary number. If you operate a retail shop worth $300,000 in inventory and equipment, insuring it for $150,000 leaves you exposed. Conducting a physical asset inventory before selecting coverage limits prevents the worst outcome-you pay premiums for years, then face a catastrophic loss you cannot fully recover from. Many business owners mistakenly think their landlord’s insurance covers their belongings, but landlord policies protect only the building structure, not your business property inside it.

Liability Coverage Shields You from Lawsuits

Liability coverage protects you when someone claims your business caused them injury or property damage. A customer slips in your restaurant and breaks their arm, suing for $75,000 in medical costs plus lost wages. A contractor’s work damages a client’s home and they demand $120,000 in repairs. Your product causes an allergic reaction and someone files a lawsuit. General liability coverage pays legal defense costs, court judgments, and settlement amounts up to your policy limit.

Most Dallas businesses operate with inadequate liability limits because they assume major claims won’t happen to them. Your BOP’s liability limit should match your actual exposure level and the severity of potential claims in your industry. A contractor handling home renovations faces far higher liability risk than a consulting firm working remotely.

Business Interruption Coverage Replaces Lost Income

Business interruption coverage replaces your lost income when a covered event forces temporary closure. If a fire damages your restaurant and forces a three-week shutdown, business interruption coverage pays your normal operating expenses and lost profits during that period. This coverage prevents the financial cascade where you lose revenue, cannot pay rent or payroll, and watch your business collapse even though the property damage itself was insurable. Understanding how these three coverage types work together shows why a BOP makes financial sense for most small and medium-sized operations in the Dallas area.

How BOP Premiums Actually Work

What Carriers Measure to Calculate Your Premium

Your BOP premium reflects factors that carriers measure with precision, and understanding what they track helps you control costs. Business location matters enormously-a Dallas contractor operating in a high-crime zip code pays more than one in a safer area, even with identical operations. Building age and construction type heavily influence property coverage costs; a brick structure built in 1995 costs less to insure than a wood-frame building from 1970 because it withstands weather and fire better. Your claims history follows you across carriers through the CLUE database (Comprehensive Loss Underwriting Exchange), meaning a water damage claim from three years ago still increases your premium today.

Revenue and payroll directly affect liability costs because higher revenue typically means more customer exposure and larger potential claims. Square footage of your space, number of employees, and the specific work your team performs all factor into the calculation. A restaurant with deep fryers and alcohol service pays substantially more than a consulting office because the risk profile is dramatically different.

Control the Factors Within Your Reach

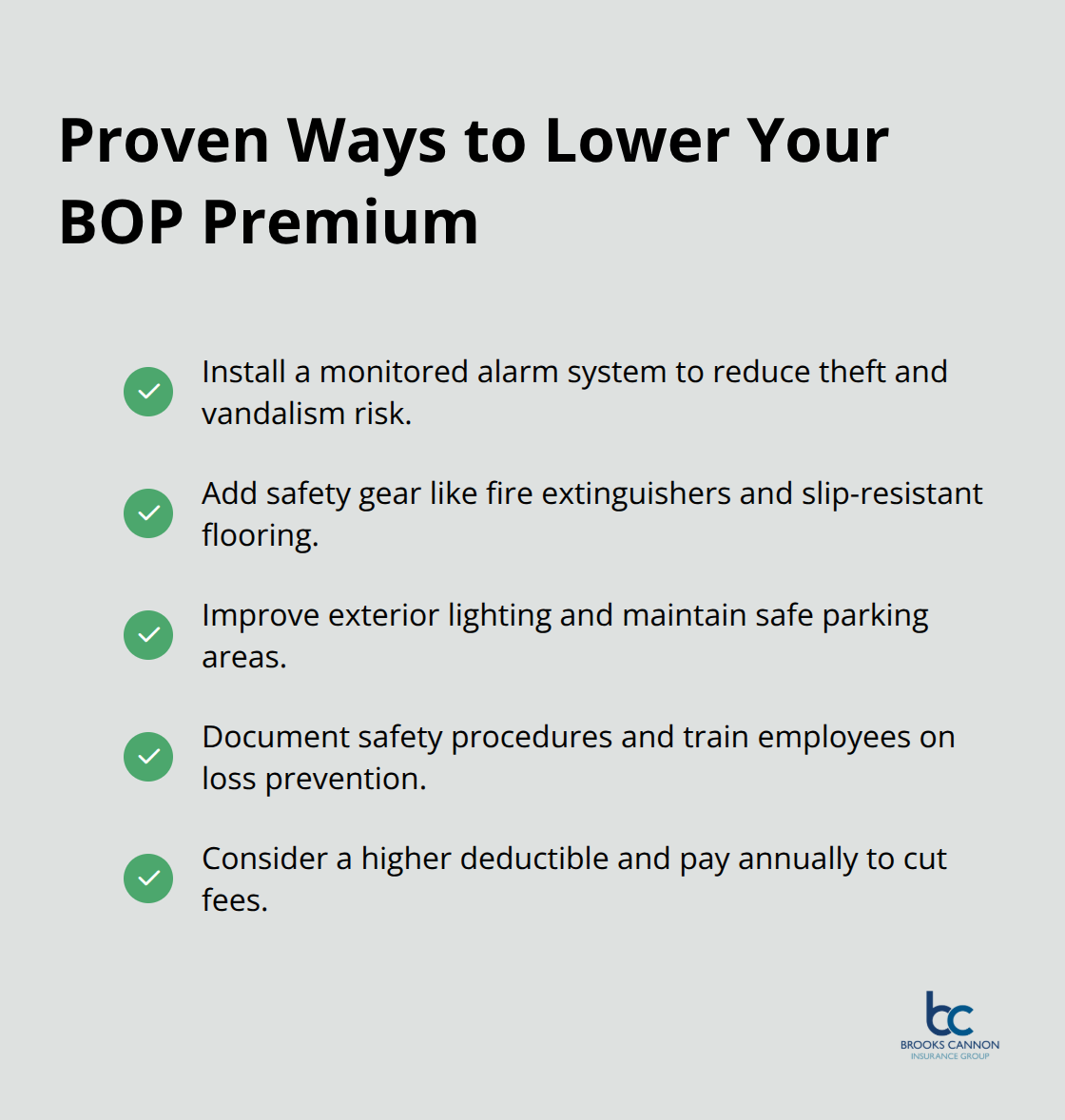

The most effective way to lower your premium is addressing the factors you actually control. A monitored alarm system can reduce your property premium because theft and vandalism risk drops measurably. Safety equipment like fire extinguishers, slip-resistant flooring, or proper lighting in parking areas signals risk management to underwriters and often triggers premium reductions.

Documented safety procedures and employee training on loss prevention demonstrate responsibility that carriers reward with lower rates.

Increasing your deductible from $500 to $2,500 lowers your annual premium significantly, though this strategy only makes sense if you can absorb that deductible amount without financial strain when a claim occurs. Paying your premium annually instead of monthly eliminates financing fees and sometimes triggers additional discounts.

Leverage Multi-Policy Discounts and Competitive Shopping

Bundling your BOP with other business policies like commercial auto or workers compensation often qualifies you for multi-policy discounts depending on the carrier. Comparing quotes from multiple carriers is non-negotiable because premium variations for identical coverage can be substantial between insurers. A contractor in Dallas might pay $1,200 annually with one carrier and $1,900 with another for the same BOP limits and deductible.

Shopping every two to three years matters because your claims history improves, your business profile changes, and new carriers enter the market with aggressive pricing. As an independent agency, we work with multiple top-rated carriers, which means we can access quotes that individual business owners cannot obtain directly.

Final Thoughts

A business owners policy consolidates your essential protections into one coordinated package at a lower cost than buying policies separately. The coverage gaps that plague businesses operating without a BOP create unnecessary risk, and managing multiple policies drains time you should spend running your operation. When you understand what a business owners policy covers-your property, shields you from liability claims, and replaces income during forced closures-the decision becomes straightforward.

The businesses that thrive address their insurance needs before disaster strikes. A fire, lawsuit, or severe weather event can destroy years of hard work in days, and your BOP provides the financial foundation that lets you recover from these events rather than watching your business collapse under uninsured losses. Getting started requires three concrete steps: conduct a thorough inventory of your physical assets so your property coverage limit reflects reality, assess your liability exposure based on your industry and customer interactions, and contact Brooks Cannon Insurance Group to compare quotes from multiple carriers.

We work with multiple top-rated insurance carriers, which means we access pricing and coverage options individual business owners cannot obtain directly. Our team handles the comparison work so you get competitive rates without spending hours on phone calls. Protecting your Dallas business assets through a properly structured BOP represents one of the highest-return decisions you can make as a business owner.