Starting a construction project in the Dallas area means navigating multiple insurance requirements. Lenders, contractors, and local building codes all have specific expectations about builders risk coverage.

At Brooks Cannon Insurance Group, we help property owners and contractors understand exactly when builders risk insurance is required and how to get the right protection in place before breaking ground.

Legal Requirements for Builders Risk

In Texas, builders risk insurance sits at the intersection of state law, lender requirements, and contractual obligations. Dallas-area property owners and contractors often assume that building codes mandate coverage, but the reality is more nuanced. State building codes in Texas do not explicitly require builders risk insurance for residential or commercial construction. However, the Texas Department of Insurance recognizes builders risk as a standard risk-management tool, and the policy becomes effectively mandatory when financing enters the picture.

When Lenders Make Coverage Non-Negotiable

If a lender finances the project-whether through a traditional mortgage, construction loan, or development financing-the lender will require builders risk coverage as a condition of releasing funds. This requirement is non-negotiable. Most lenders in the Dallas area demand proof of active coverage before disbursing the first draw, and they typically require the lender to be named as loss payee on the policy. Without this coverage in place, construction cannot begin, making it a practical requirement even where local code does not explicitly mandate it.

Determining Who Purchases the Policy

The construction contract determines who must obtain builders risk coverage, and this assignment matters significantly. In many Dallas projects, the property owner or developer purchases the policy and lists the general contractor as an additional insured. In other setups, the general contractor buys the policy directly and names the owner as loss payee. Subcontractors often assume they are covered under the main contractor’s policy, but this assumption creates serious exposure. Subcontractors are not automatically named insureds unless explicitly listed in the policy or covered by endorsement. If a loss occurs and the subcontractor is not named, the subcontractor has no direct right to recovery.

This gap has led to disputes and uninsured losses on Dallas-area projects. The construction contract should clearly state who purchases builders risk insurance, whose name appears on the policy, and whether subs receive additional insured status. If you are a subcontractor, request a copy of the builders risk policy and verify your company name is listed. If you are a general contractor managing multiple subs, ensure your builders risk policy explicitly names each sub or includes a blanket additional insured endorsement covering all subs hired for the project.

Municipal Conditions and Contract Requirements

Dallas building permits and municipal approvals sometimes impose insurance requirements at the city level, though these typically defer to the contract between owner and contractor rather than mandate specific coverage. However, some larger Dallas projects, particularly in commercial development zones, may include municipal conditions requiring proof of builders risk before permits are issued.

The construction contract itself often becomes the controlling document, specifying minimum coverage limits, required endorsements, and policy effective dates. If the contract requires $2 million in builders risk coverage and the policy is written for $1.5 million, the project is underinsured and the contractor may face liability if a loss exceeds the policy limit. Additionally, the contract may require coverage for specific perils such as theft, hail, or wind-perils that are standard in Texas but not always automatically included at the highest limits.

Before construction starts, review the contract for insurance requirements, cross-check them against the actual policy, and confirm that all required names, limits, and endorsements are in place. Misalignment between contract requirements and actual coverage is one of the most common reasons claims are denied or underpaid on Dallas construction projects. Once you understand your legal obligations and contractual requirements, the next step is identifying which types of construction projects actually trigger the need for builders risk coverage in the first place.

Types of Construction Projects That Need Builders Risk Coverage

Residential New Construction

Residential new construction in the Dallas area triggers builders risk requirements more consistently than any other project type. When a homeowner or developer finances a new single-family home, townhome, or multi-unit residential project, the lender demands builders risk coverage before releasing construction funds. Dallas-area residential construction has grown significantly, with the Dallas metropolitan area adding over 150,000 housing units between 2015 and 2023 according to the U.S. Census Bureau. Each of these projects required builders risk protection to satisfy financing conditions.

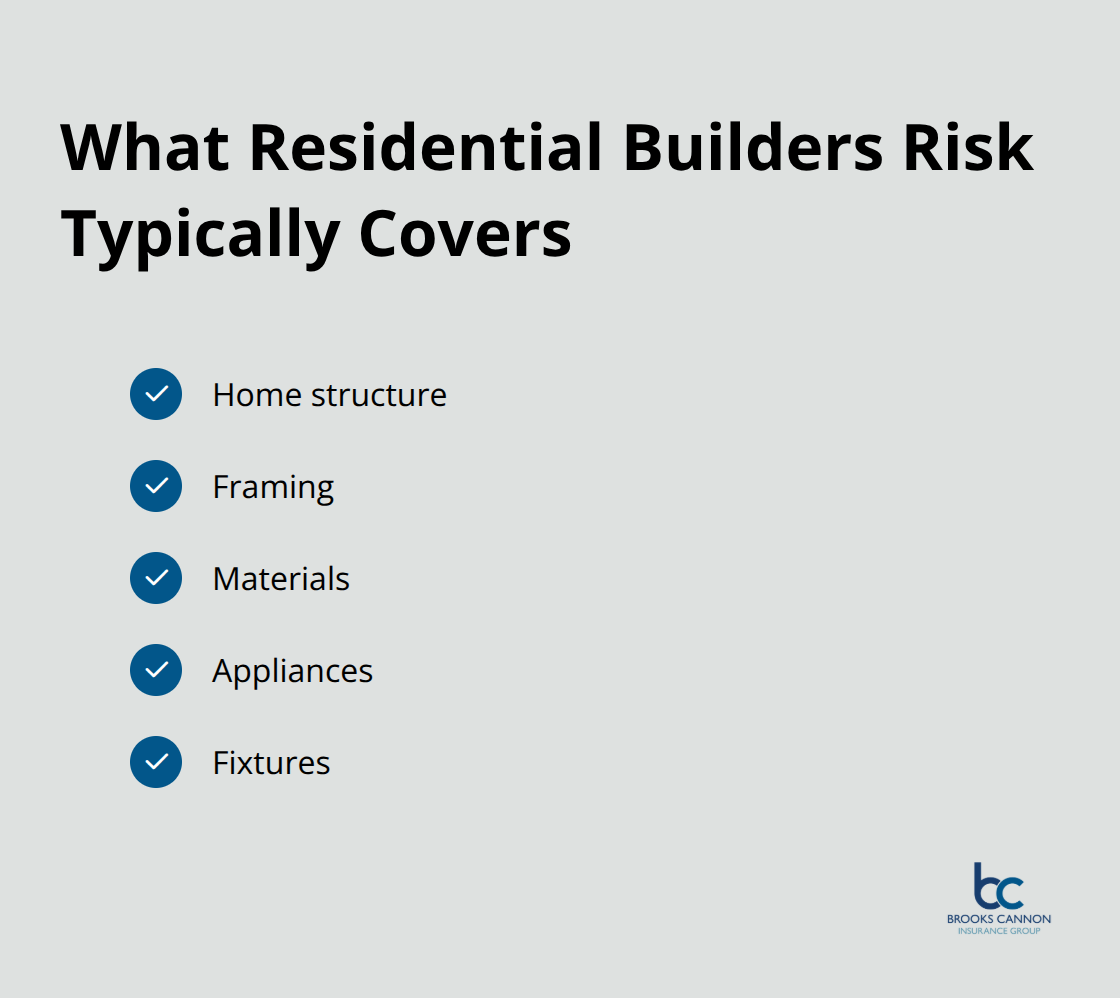

The policy covers the home structure, framing, materials, appliances, and fixtures during construction until the certificate of occupancy is issued. Residential projects typically carry lower coverage limits than commercial work-often between $500,000 and $3 million depending on the home’s final value-but the requirement is absolute whenever a mortgage or construction loan is involved.

If you are building a custom home or developing a residential subdivision in Dallas, your lender will require proof of active builders risk coverage before the first construction draw is released.

Commercial Building Projects

Commercial building projects in Dallas demand builders risk coverage even more rigidly than residential work because project values are substantially higher and lender scrutiny is more intense. A commercial office, retail, or industrial project valued at $10 million or more faces significant financial exposure if a loss occurs during construction. Dallas commercial construction activity reached approximately $45 billion in 2023, representing major economic investment that requires comprehensive risk management.

Commercial lenders and institutional investors virtually always mandate builders risk as a financing condition and often require higher coverage limits, soft costs endorsements covering lost rental income or permit delays, and debris removal coverage. Commercial projects also frequently involve multiple general contractors and dozens of subcontractors, making it critical that the policy clearly names all parties or includes a blanket additional insured endorsement. If you are a commercial general contractor or developer in Dallas, verify that your builders risk policy covers the full project value plus soft costs, and confirm that all subs involved in the work are either named or covered by endorsement. Failure to do so exposes your company to claims from subs who suffer uninsured losses.

Renovation and Remodeling Work

Renovation and remodeling projects present a different risk profile and often create confusion about coverage requirements. A major renovation-such as a complete kitchen remodel, roof replacement, or structural addition to an existing home or commercial building-may or may not require builders risk depending on the scope and financing. If the renovation is financed through a construction loan or home equity line of credit, the lender will likely require builders risk coverage.

However, if the property owner pays cash or uses a personal line of credit, builders risk is technically optional but strongly recommended. In Dallas, renovation projects frequently expose unforeseen damage once walls are opened or existing systems are exposed. The Texas climate also creates specific risks during renovation work: open roof sections during hail season, exposed framing vulnerable to wind damage, and materials stored on-site at risk of theft or weather damage.

A remodeling contractor who assumes the property owner’s homeowners insurance covers construction damage is making a dangerous mistake. Homeowners policies explicitly exclude coverage for property damage caused by construction or renovation work. If a fire occurs in a wall cavity during electrical work, or hail damages newly installed roofing before the project is complete, the homeowners policy will deny the claim. Builders risk fills this gap and protects both the contractor and the property owner.

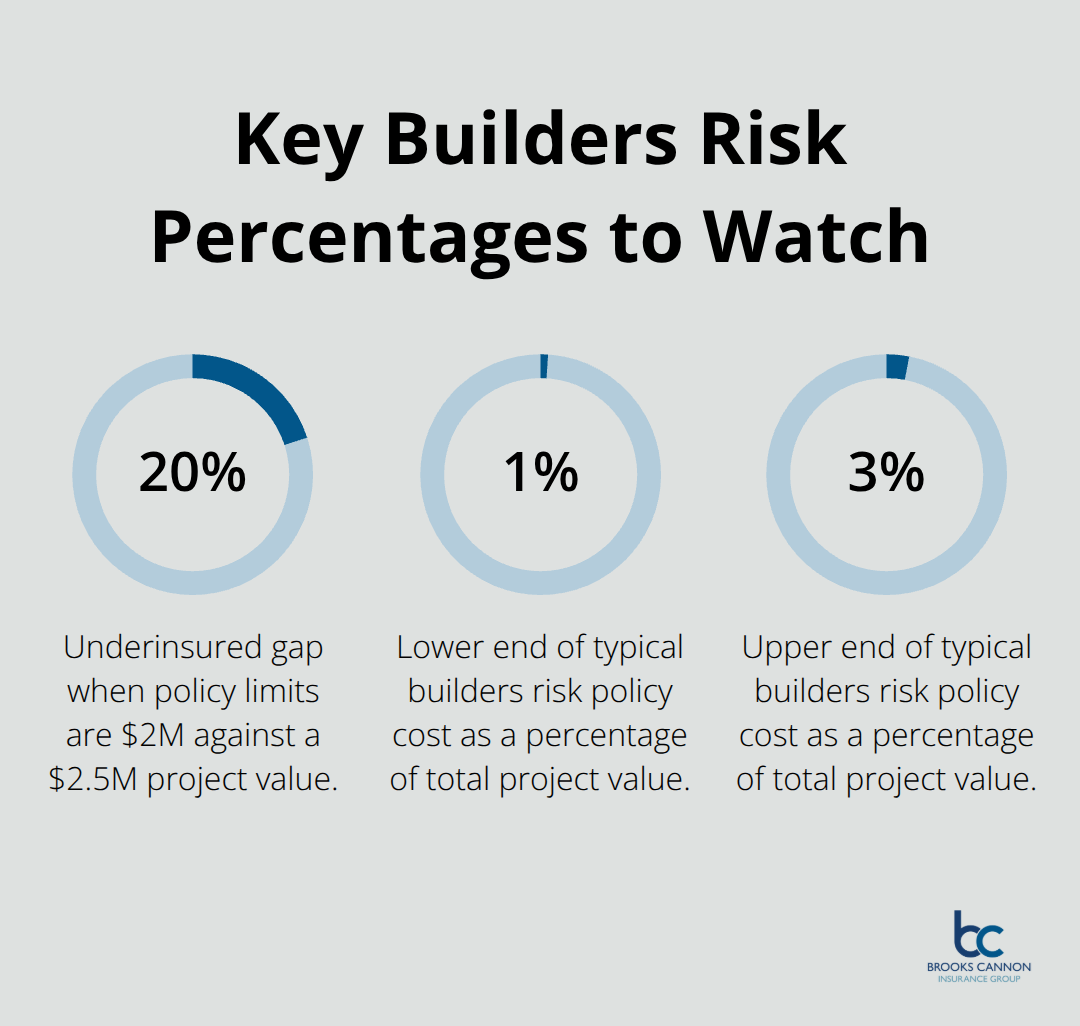

The policy cost is modest relative to the project value-typically 1 to 3 percent of the total construction investment-and the protection is essential. Once you understand which projects require builders risk coverage, the next step is selecting the right policy limits and endorsements to match your specific project risks and contractual obligations.

Selecting Coverage That Matches Your Dallas Project

Calculate Your Total Insurable Value

The gap between underinsurance and overinsurance on a Dallas construction project often comes down to one decision: how thoroughly you assess the actual risks facing your specific job. A commercial office building in downtown Dallas faces different perils than a residential addition in a suburban neighborhood, yet many contractors and owners apply a one-size-fits-all approach to builders risk limits. This mistake costs money either through insufficient coverage that leaves you exposed or excessive limits that inflate premiums unnecessarily.

Start by calculating the total insurable value of your project, which includes the structure cost, materials, equipment, temporary structures, and any soft costs tied to the build. For residential work in the Dallas area, this means the final home value plus construction costs; for commercial projects, it means the complete building value plus site improvements.

Identify Perils Based on Location and Timeline

Next, identify the specific perils that threaten your project based on location and timeline. A roofing project that runs through spring hail season in Dallas County needs robust hail and windstorm coverage, while a winter interior renovation may prioritize theft and vandalism protection instead. Hail claims peak between April and June, so a spring project requires higher deductibles or broader coverage than a fall project.

Match Policy Limits to Project Value

Once you know your project value and primary perils, compare actual policy limits against your calculated exposure. If your policy limit is $2 million but your project value is $2.5 million, you are underinsured by 20 percent and any major loss will leave you short. Conversely, if your policy limit is $5 million for a $1.5 million project, you are paying for coverage you will never use.

The construction contract typically specifies minimum coverage limits, and your policy must meet or exceed those requirements without padding. Many Dallas contractors overlook soft costs coverage, which protects against losses like delayed permits, architect fees, or lost rental income if a covered loss halts the project. A commercial office project with $100,000 in soft costs should add that endorsement rather than assume the base policy covers it; the endorsement cost is minimal compared to the financial impact of a three-month construction delay.

Review Exclusions and Deductibles Carefully

Review the policy exclusions carefully because gaps in coverage are where claims get denied. Standard exclusions like flood, earthquake, and poor workmanship are common, but in Texas you need to align coverage limits to your actual risk if your project sits in a high-risk zone. Hail damage is covered under most builders risk policies, but verify that your deductible is appropriate for your budget. A $10,000 deductible reduces premiums but shifts significant risk to you if a hail event occurs; a $2,500 deductible costs more upfront but protects your cash flow.

Work with an Independent Agent

Once you have identified your coverage needs, work with an independent insurance agent who understands Dallas construction risks and can match your project requirements to the right carrier. An independent agent works with multiple insurers to find policies that fit your specific project value, timeline, location, and contractual obligations rather than selling you a generic package.

Final Thoughts

Builders risk insurance is required whenever a lender finances a construction project, and it becomes a practical necessity for protecting your investment regardless of financing. The Dallas construction market moves fast, and delays caused by uninsured losses can derail timelines and budgets. Understanding when builders risk insurance is required means reviewing your financing terms, construction contract, and project specifics before breaking ground.

If a lender is involved, builders risk coverage is non-negotiable. If you are self-funding, the coverage is optional but strongly recommended given Texas weather risks and the cost of mid-project losses. Either way, the policy must align with your actual project value, include all required parties as named insureds or additional insureds, and cover the specific perils threatening your job.

The difference between adequate protection and costly gaps often comes down to working with an agent who understands your specific project. At Brooks Cannon Insurance Group, we work with multiple top-rated carriers to find builders risk policies that fit your Dallas project’s unique risks, timeline, and budget. Contact us to discuss your project and get coverage in place before construction begins.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation