General liability insurance cost is one of the biggest questions we hear from Dallas business owners. The price you pay depends on several factors-some within your control and others determined by your industry.

At Brooks Cannon Insurance Group, we help businesses understand what drives these costs and how to manage them effectively. This guide walks you through the real numbers and practical strategies to keep your premiums reasonable.

What Drives General Liability Costs

Industry Risk Determines Your Premium

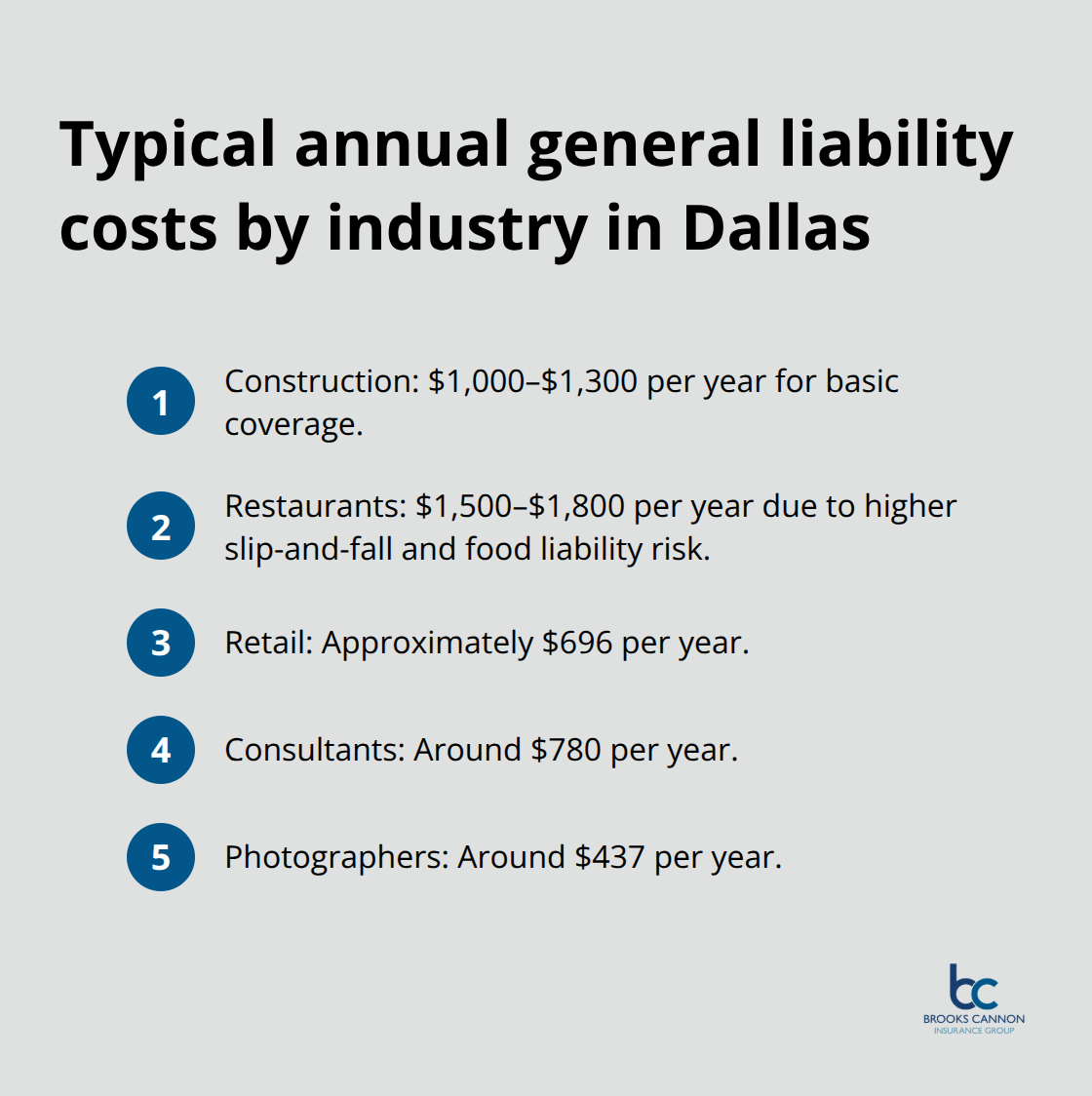

Your industry determines more about your premium than almost anything else. Construction companies in Dallas pay significantly more than consulting firms because the risk profile is fundamentally different. A construction worker on a job site faces hazards that a consultant in an office simply does not. According to industry data, construction businesses typically pay $1,000 to $1,300 annually for basic coverage, while consultants average around $780 per year. Restaurants face even higher costs, ranging from $1,500 to $1,800 annually, because slip-and-fall incidents and food-related liability claims occur more frequently. Retail stores sit in the middle at approximately $696 per year.

Photography businesses, which carry lower inherent risk, average around $437 annually. Underwriters calculate premiums based on actual claim frequency and severity data from each industry sector-this isn’t arbitrary pricing.

Business Size and Employee Count Impact Costs

Your business revenue and number of employees directly influence what you pay because both factors correlate with exposure. A company generating $500,000 in annual revenue with three employees presents different risk than a $2 million operation with fifteen staff members. More employees mean more potential for workplace accidents, property damage claims, and customer interactions that could result in liability. Insurers examine your business claims history closely because past behavior predicts future risk. A business with three claims in the last five years will pay substantially more than an identical business with zero claims.

Location and Claims History Shape Your Rate

Dallas underwriters particularly scrutinize location and premises type when evaluating risk. A busy storefront in a dense downtown area with high foot traffic faces greater slip-and-fall exposure than a small office building. Weather patterns matter too-Texas tornadoes, flooding in certain regions, and heatwaves affecting outdoor work scenarios all influence local underwriting decisions. Your deductible choice directly impacts your monthly cost. Selecting a $1,000 deductible instead of $500 reduces your premium, but you absorb more risk out-of-pocket when a claim occurs.

Coverage Limits and Policy Structure Affect Pricing

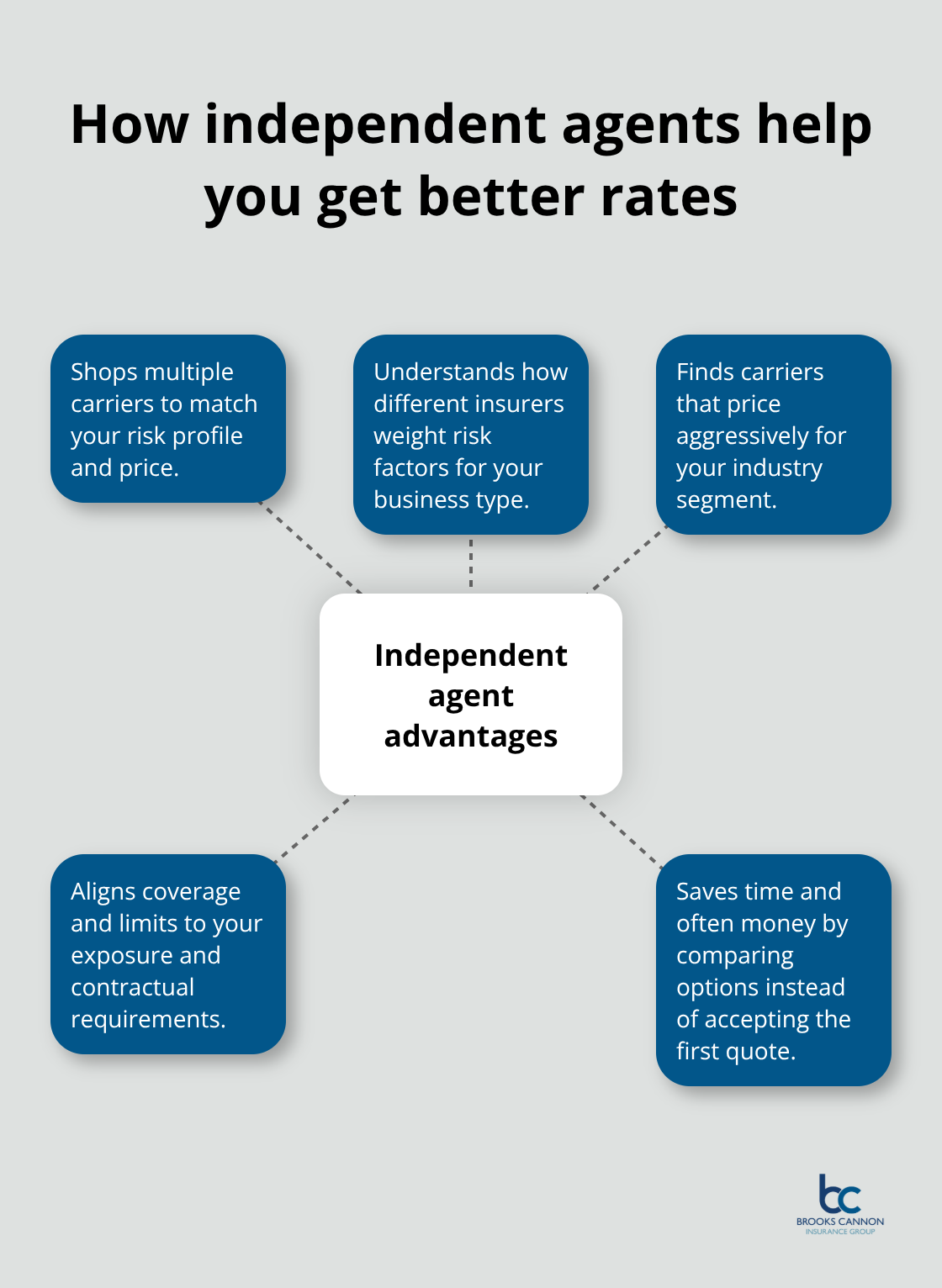

Your coverage limits affect pricing significantly. Jumping from $1 million per occurrence to $2 million increases your annual premium noticeably. The policy structure you choose matters as well. A standalone general liability policy costs more than bundling it with commercial property or other coverages through a Business Owners Policy. Independent agents can compare rates across 80+ carriers to find pricing that matches your specific risk profile and business needs, which brings us to how you can actually lower what you pay.

Ways to Cut Your General Liability Premiums

Safety Programs Lower Claims and Premiums

Safety programs reduce your premiums because they lower claim frequency. Insurers track your risk management efforts closely, and businesses that implement formal safety protocols pay less over time. A painting contractor who maintains clear walkways, uses non-slip mats, and documents daily safety checks demonstrates lower risk than one without these measures. Documented safety procedures signal to underwriters that you take loss prevention seriously. This translates to real premium reductions-safety programs directly impact your insurance costs through measurable reductions in claims frequency and severity. Dallas businesses that track near-misses, train employees on hazard recognition, and update procedures quarterly build the kind of loss history that keeps rates down.

Bundling Coverage Cuts Your Overall Costs

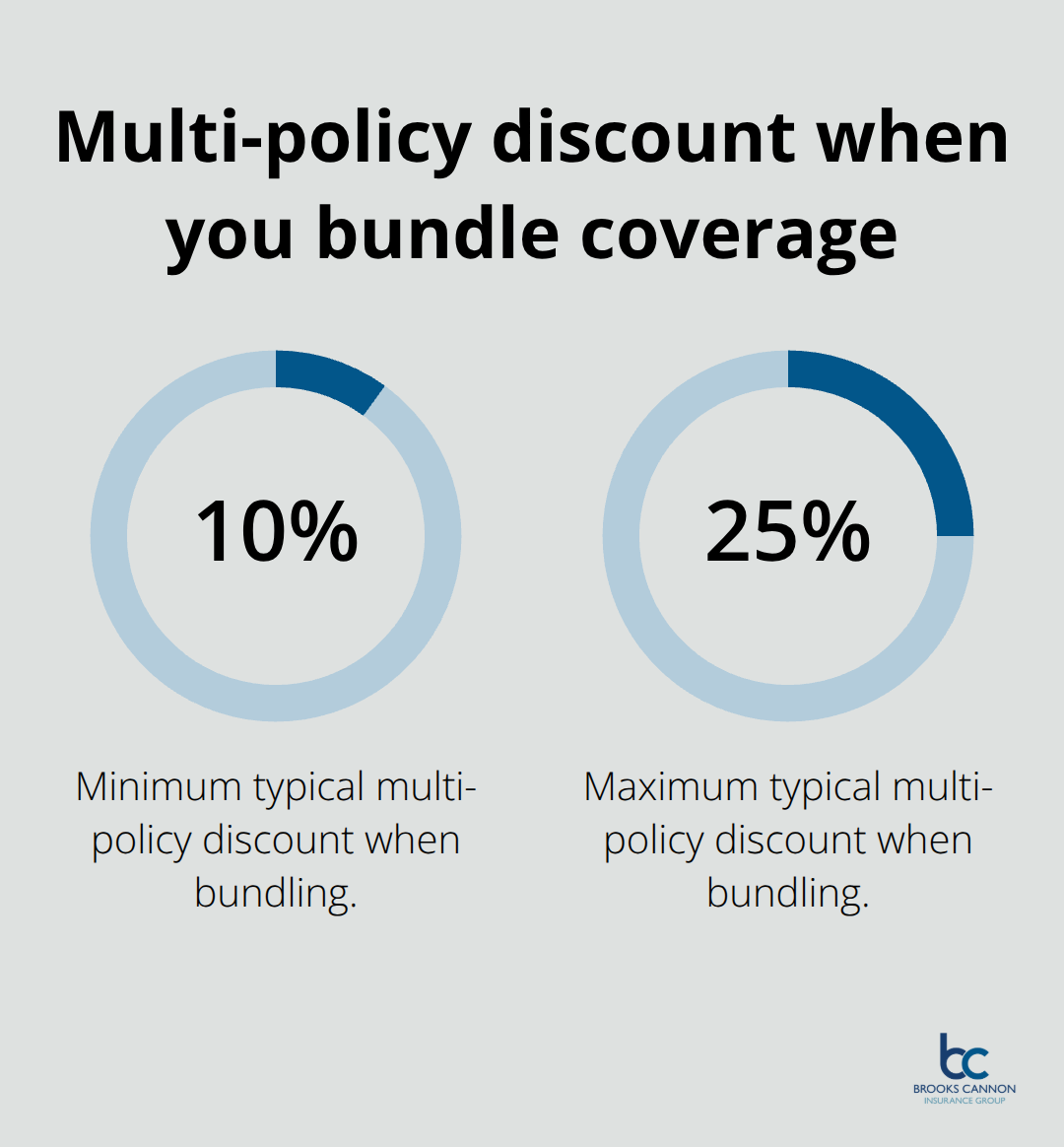

Bundling your general liability with commercial property, workers compensation, or a business owners policy typically costs less than purchasing each separately. When you consolidate coverage with one carrier, insurers offer multi-policy discounts ranging from 10 to 25 percent depending on the combination.

A Dallas restaurant owner paying $1,600 for standalone general liability might drop that to $1,350 when bundling with property coverage. This approach works because carriers reward loyalty and reduced administrative overhead with meaningful savings.

Align Coverage Limits to Your Actual Risk

Your coverage limits should match your actual exposure and contractual requirements rather than defaulting to standard $1 million per occurrence limits. If your lease or contracts require $1 million coverage but your business operations warrant only $500,000, you pay for unnecessary protection. Conversely, underestimating your exposure leaves you vulnerable to catastrophic out-of-pocket costs. Reviewing your limits annually-particularly as your revenue grows or your employee count changes-prevents both over and under-insurance. A business that expanded from five to twelve employees needs to reassess whether current limits still match the increased activity level.

Work with an Independent Agent for Better Rates

An independent agent who evaluates your specific risk profile across multiple carriers ensures you avoid paying for unnecessary coverage while maintaining adequate protection. At Brooks Cannon Insurance Group, we work with multiple top-rated insurance carriers to find the best coverage and pricing for each client’s unique situation. This approach gives you access to competitive options that a single-carrier agent cannot provide. The Texas Department of Licensing and Regulation requires electrical contractors to maintain minimum liability limits of $300,000 per occurrence and $600,000 aggregate to hold their license, which means your industry may have baseline requirements that affect your coverage structure. Understanding these regulatory minimums helps you structure policies that meet legal obligations without overpaying for excess capacity. As your business grows and your risk profile shifts, these baseline requirements and your actual exposure may diverge-making periodic reviews with an agent who shops multiple carriers essential to keeping your premiums aligned with your true risk.

General Liability Insurance Cost Comparison for Dallas Businesses

Industry Type Drives the Biggest Price Differences

Dallas general liability costs vary dramatically based on your industry, and the numbers tell a clear story about risk. Construction companies operating in the Dallas area pay $1,000 to $1,300 annually for standard $1 million per occurrence coverage, while restaurants face $1,500 to $1,800 because slip-and-fall claims and food liability incidents occur regularly in that sector. Retail businesses average around $696 per year, consultants pay approximately $780 annually, and photographers sit at the lower end around $437 per year. These aren’t arbitrary ranges-they reflect actual claims data that underwriters use to price policies. A Dallas coffee shop without general liability faces potential out-of-pocket costs exceeding $20,000 for a single customer injury, which makes the $1,500 to $1,800 annual premium for restaurants genuinely affordable protection. The gap between industries matters significantly because a construction site hazard simply doesn’t exist in a consulting office, and underwriters price accordingly.

Small Business vs. Large Enterprise Pricing

Business size creates the second major pricing divide in Dallas. A one-person consulting firm generating $300,000 in revenue pays substantially less than a twelve-person operation generating $1.5 million because employee count and revenue both correlate directly with exposure. More employees mean more customer interactions, more opportunities for accidents, and more potential liability claims. Revenue matters because higher-volume businesses typically have more transactions, more premises activity, and greater total exposure. A Dallas retail store with three employees pays less than an identical business with eight employees, even with the same square footage and location. Claims history amplifies these differences-a business with zero claims in five years pays roughly 30 to 50 percent less than an identical business with two or three prior claims.

Location and Premises Type Affect Your Rate

Location within Dallas shifts pricing noticeably; a storefront on busy Mockingbird Lane carries higher slip-and-fall risk than an office building in a quieter area, which means your underwriter considers foot traffic patterns and premises type carefully. Small, low-risk Dallas businesses sometimes pay under $200 annually, while high-risk operations with poor claims histories can exceed $3,000. The median monthly cost for new customers across carriers runs around $60, though averages climb to $85 per month when accounting for higher-risk profiles.

How Independent Agents Find Better Rates

Multiple carriers price the same business differently because each insurer weights risk factors in their own way. Some carriers price aggressively on certain business types while others focus on different risk segments.

Shopping rates across multiple insurance companies rather than accepting the first quote often saves 15 to 30 percent on your annual premium, particularly when your business doesn’t fit the standard risk profile that online quote tools assume. An independent agent evaluates how each carrier approaches your specific situation and identifies which one offers the best combination of coverage and price for your needs.

Final Thoughts

General liability insurance cost reflects real risk data that underwriters apply to your specific business. Construction companies pay more than consultants because actual hazards differ, and restaurants face higher premiums than retail because slip-and-fall claims occur more frequently in that sector. These price differences aren’t arbitrary-they protect insurers from predictable losses while keeping your premiums aligned with your actual exposure.

Three actions reduce what you pay for coverage. First, implement safety programs that lower your claims frequency; a painting contractor with documented procedures pays less than one without them because insurers reward loss prevention. Second, bundle general liability with commercial property or workers compensation to capture multi-policy discounts that typically range from 10 to 25 percent. Third, review your coverage limits annually as your business grows, since a company that expanded from five to twelve employees needs different protection than before.

An independent agent makes a measurable difference in your general liability insurance cost by comparing rates across multiple carriers rather than accepting the first quote. We at Brooks Cannon Insurance Group evaluate how each insurer approaches your specific situation and identify which one offers the best combination of coverage and price for your needs. Shopping your business across multiple carriers often saves 15 to 30 percent compared to staying with a single carrier.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation