One liability claim can drain your business’s savings and damage your reputation for years. We at Brooks Cannon Insurance Group see Dallas business owners face unexpected lawsuits every month-and most aren’t prepared.

Commercial liability planning isn’t optional anymore. It’s the foundation that keeps your business standing when things go wrong.

What Liability Claims Actually Cost Dallas Businesses

The Real Numbers Behind Dallas Liability Exposure

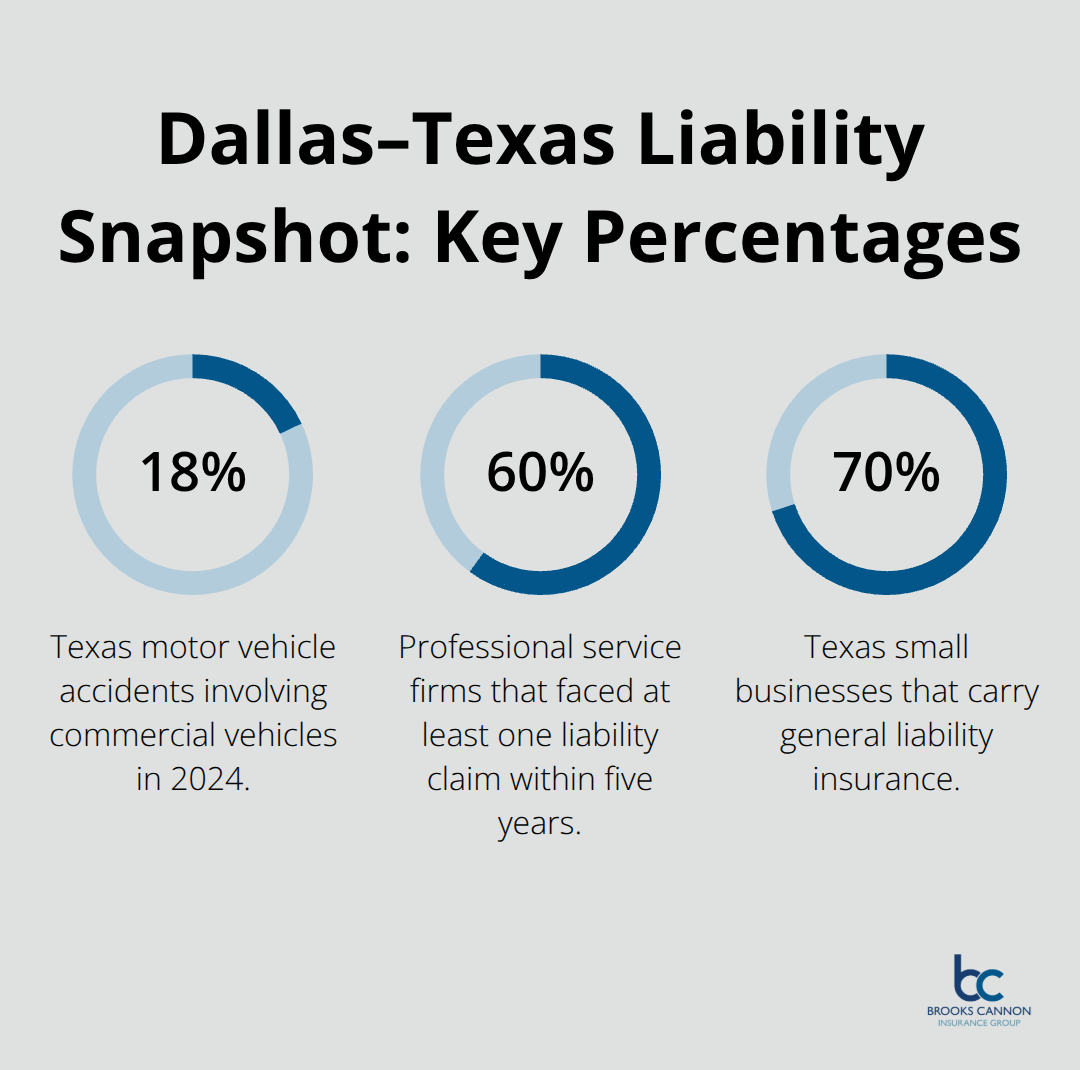

Dallas businesses face genuine liability exposure, and the data tells the story. Texas logged 563,000 motor vehicle accidents in 2024, with 18% involving commercial vehicles, according to the Texas Department of Transportation. That’s just one category of risk. Dallas County recorded around 10,500 personal injury lawsuits in 2024 alone. A single lawsuit carries serious consequences-the average legal cost per claim runs about $15,000, which can cripple a cash-strapped operation before insurance even enters the picture. About 60% of professional service firms faced at least one liability claim within a five-year span, with average legal costs around $25,000 per case according to the National Association of Insurance Commissioners.

How Industry Type Shapes Your Liability Profile

Restaurants, contractors, healthcare providers, and retail shops operate in different risk worlds, yet all face exposure that most owners underestimate. Construction businesses confront bodily injury claims from job-site accidents. Restaurants battle slip-and-fall incidents and foodborne illness allegations. Professionals like accountants and consultants face negligence claims that can destroy client relationships. Retailers fight product liability and customer injury claims. Manufacturing operations manage equipment-related injuries and product recalls. The pattern is clear: liability hits differently depending on what you do.

Why Uninsured Exposure Destroys More Than Finances

An uninsured liability claim doesn’t just cost money; it threatens your business’s survival. Texas saw approximately 12,000 business-related lawsuits in 2024. Without general liability coverage, a single bodily injury claim can reach your personal assets, even if you operate as an LLC. About 70% of Texas small businesses carry general liability insurance, which means 30% operate exposed. A Dallas restaurant case illustrates the danger: a customer slip-and-fall resulted in a judgment that the owner couldn’t absorb. The reputational damage lasted longer than the financial wound. Judgments don’t disappear-creditors can pursue wage garnishment and asset liens for years.

Operating without coverage also creates contract problems. About 65% of Dallas commercial contracts require a Certificate of Insurance before work begins, and many projects demand delivery within 24 hours. Without coverage, you simply can’t bid on those contracts. General liability insurance in Texas typically costs $40–$80 per month for small businesses, making the protection far cheaper than the risk. High-risk industries like construction pay $100–$200 monthly, still a bargain compared to legal exposure.

Matching Coverage to Your Industry’s Actual Risks

A construction company’s liability profile bears no resemblance to a marketing consultant’s. Construction operations face bodily injury claims from job-site accidents, equipment damage, and third-party injuries. These businesses need general liability plus inland marine, builders risk, and surety bonds. Restaurants require general liability plus liquor liability and spoilage coverage-the cost of liability jumps significantly due to alcohol service and food safety risks. Retail shops should prioritize product liability and cyber protection, particularly if they handle customer payment data. Professional services-accountants, lawyers, engineers-must carry errors and omissions coverage because a missed deadline or calculation error can cost clients six figures. Manufacturing operations need product liability, recall coverage, and equipment breakdown protection. Healthcare providers face the highest liability exposure of any sector and typically pay the steepest premiums.

Texas’s fastest-growing industries include energy, logistics, technology, and healthcare, each carrying distinct liability profiles. Energy companies face environmental liability. Logistics operations manage transportation and cargo risks. Technology firms confront data breach and cyber liability. Healthcare providers battle medical malpractice claims. A one-size-fits-all approach fails because risks compound differently across sectors. An independent broker with access to multiple carriers can match your industry’s actual exposure to appropriate coverage, not generic solutions. This precision matters when you’re ready to build your comprehensive liability strategy.

How to Build Your Liability Strategy Without Guessing

Most Dallas business owners approach liability coverage backward. They buy a general liability policy because it’s cheap, then hope nothing catastrophic happens. That’s not a strategy-it’s wishful thinking. A real liability strategy starts with understanding your specific exposure, then layering coverage to address gaps that generic policies miss. This requires honest assessment of your operation, not industry averages or competitor practices. Your restaurant faces different risks than your neighbor’s consulting firm, and your coverage should reflect that difference precisely.

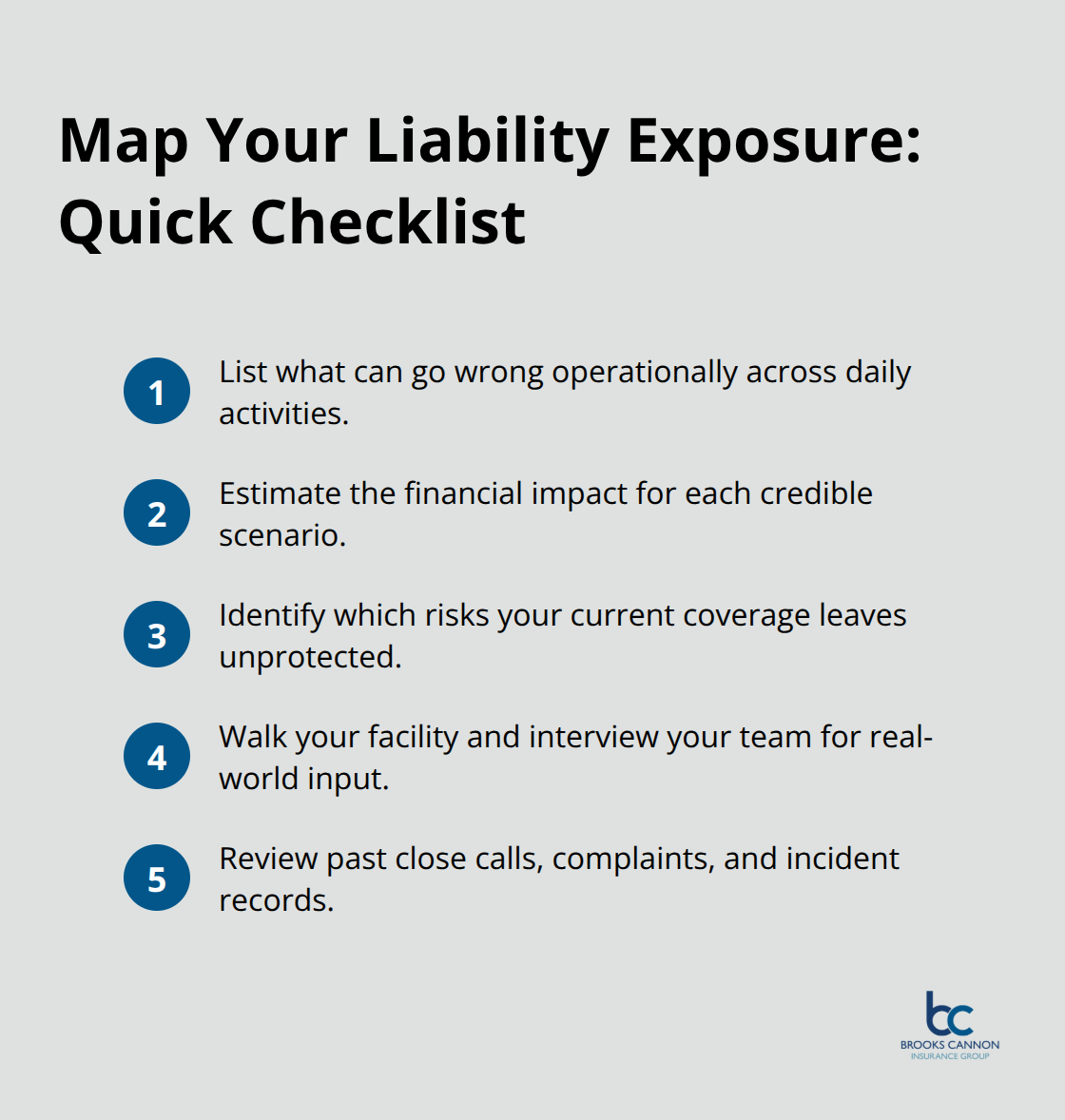

Map Your Actual Liability Exposure

Start by mapping your liability exposure across three dimensions: what can go wrong operationally, what financial impact each scenario carries, and which risks your current coverage leaves unprotected. A construction contractor should document job-site hazards, equipment used, subcontractor relationships, and past injury claims. A professional service firm needs to identify the highest-value client relationships, the types of errors most likely to trigger claims, and which mistakes cost the most to fix. A retail operation should assess foot traffic patterns, product types, and customer demographics. This assessment isn’t theoretical-walk your facility, interview your team, review past close calls and complaints.

Identify Coverage Gaps That Matter

Professional liability coverage for service businesses typically costs $40–$80 monthly in Texas, but that expense only makes sense if you’ve identified the specific negligence risks you’re protecting against. If you haven’t, you’re overpaying for coverage you don’t need or underpaying for exposure you can’t afford. An independent broker with access to 80+ carriers can help translate your specific risk map into actual policy recommendations, rather than pushing standard packages. They’ll spot gaps that matter. For example, if you operate vehicles for business but employees sometimes use personal cars for client visits, you need hired and non-owned auto coverage-a detail most business owners miss until a claim happens.

Address Hidden Exposures in Your Operations

Similarly, if you hold client data or process online payments, cyber liability becomes essential regardless of industry. Texas saw a 15% rise in cyber incidents in 2024 according to the Texas Department of Information Resources, and the average cost of a data breach reaches about $4.5 million according to IBM’s Cost of a Data Breach Report. A $150 monthly cyber policy prevents that exposure far better than hoping your password policy stays strong. These hidden exposures often hide in plain sight-they don’t appear in your daily operations until a claim forces them into focus. The difference between adequate coverage and inadequate coverage frequently comes down to whether someone asked the right questions during the assessment phase. An independent agent who understands your industry can ask those questions and uncover exposures that generic online quotes miss entirely. Once you’ve mapped your exposure and identified your coverage gaps, the next step involves selecting the right policy types and limits to create a layered protection strategy that actually matches your business.

What Each Coverage Type Protects and Why It Matters

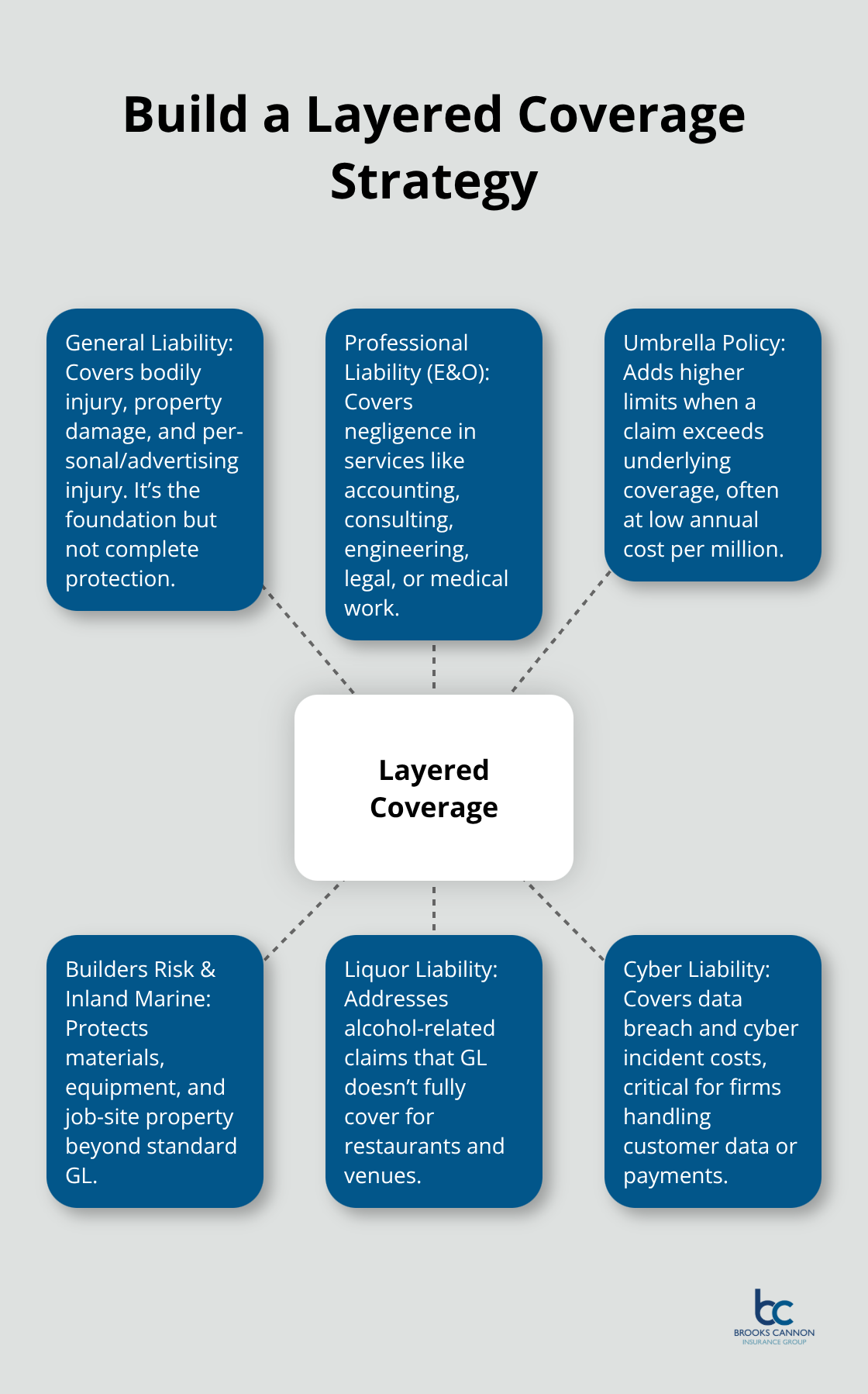

General Liability: The Foundation That Isn’t Enough

General liability insurance forms the foundation of commercial protection in Dallas, but it only covers bodily injury, property damage, and personal advertising injury claims. This policy won’t protect you if a client sues for negligence in your professional work, if your product causes harm beyond property damage, or if your business operations halt unexpectedly. Texas small businesses typically pay $40–$80 monthly for general liability, yet this baseline coverage leaves significant exposure uncovered depending on your industry.

A construction firm needs general liability, but without builders risk and inland marine policies, equipment and materials on job sites remain unprotected. A restaurant carries general liability for slip-and-fall incidents, but liquor liability coverage specifically addresses alcohol-related claims-a separate policy many owners overlook until a lawsuit forces the issue.

The mistake most Dallas business owners make is treating general liability as complete protection when it actually covers only one category of risk.

Professional Liability: Protecting Against Service-Based Negligence

Professional liability insurance serves an entirely different purpose and applies to completely different claims. If you provide services-accounting, consulting, engineering, legal advice, medical care-your mistakes or negligence can cost clients far more than property damage ever could. A missed tax deadline costs your client money. A miscalculation in structural design creates safety hazards. A misdiagnosis causes harm.

The National Association of Insurance Commissioners reports that professional service firms faced at least one liability claim within five years, with average legal costs around $25,000 per case. Professional liability typically costs $50–$150 monthly in Texas, depending on your profession and the specific services you offer. Higher-risk sectors like healthcare and legal services often exceed $200 monthly. This coverage exists because general liability explicitly excludes professional negligence. You cannot purchase your way out of this gap with a cheaper general liability policy. Service-based businesses must carry professional liability or operate with uninsurable exposure.

Umbrella Policies: Coverage When Claims Exceed Your Limits

Umbrella policies handle claims that exceed your underlying coverage limits. If your general liability policy carries a $1 million limit per occurrence and a lawsuit demands $2 million, your umbrella policy covers the additional $1 million. Texas saw approximately 12,000 business-related lawsuits in 2024, and large claims happen more frequently than most owners expect.

A contractor recently faced a $1.5 million claim from a serious job-site injury, and umbrella coverage paid the $500,000 excess beyond the underlying policy limit. Without that umbrella, the contractor would have personally absorbed the difference. Umbrella policies cost far less than you might think-typically $100–$300 annually per million dollars of additional coverage, making them one of the most cost-effective protections available.

Layering Coverage to Match Your Actual Exposure

The real value of umbrella protection emerges when you understand that one serious claim can exceed your underlying limits, particularly in high-risk industries or high-value projects. A restaurant with a $1 million general liability limit faces genuine risk if a food poisoning outbreak affects dozens of customers. A consulting firm with a $2 million professional liability limit operates exposed if a single client relationship involves multi-million-dollar decisions.

Layering coverage means starting with industry-appropriate underlying policies, then adding umbrella protection to cover gaps that exceed those limits. An independent agent can model scenarios specific to your business-worst-case claims in your industry, your typical contract values, your employee count-and recommend umbrella limits that actually match your exposure rather than generic industry standards.

Final Thoughts

Commercial liability planning protects your Dallas business from the financial devastation that one lawsuit can trigger. Lawsuits happen regularly, legal costs mount quickly, and uninsured exposure threatens your personal assets regardless of your business structure. The strategy you build today determines whether a claim becomes a manageable insurance matter or a business-ending catastrophe.

Your liability strategy must start with honest assessment of your actual risks, not industry averages or competitor practices. Map what can go wrong in your specific operation, identify which gaps your current coverage leaves exposed, and address hidden exposures before claims force them into focus. General liability forms the foundation, but professional liability protects service-based negligence, and umbrella policies cover claims exceeding your underlying limits-the right combination depends entirely on your industry, your operations, and your financial exposure.

Most Dallas business owners approach this backward and buy cheap coverage while hoping nothing happens. That approach relies on luck, not resilience. Real resilience comes from understanding your exposure, selecting appropriate coverage types and limits, and working with someone who asks the right questions rather than pushing standard packages. Contact Brooks Cannon Insurance Group to discuss your commercial liability planning needs with licensed experts who understand your operation and your market.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation