Dallas businesses are under attack. Ransomware, data breaches, and cyber extortion are no longer rare events-they’re happening to local companies every week.

At Brooks Cannon Insurance Group, we’ve seen firsthand how a single cyber incident can devastate a business’s finances and reputation. That’s why Dallas cyber liability insurance isn’t optional anymore-it’s a business necessity.

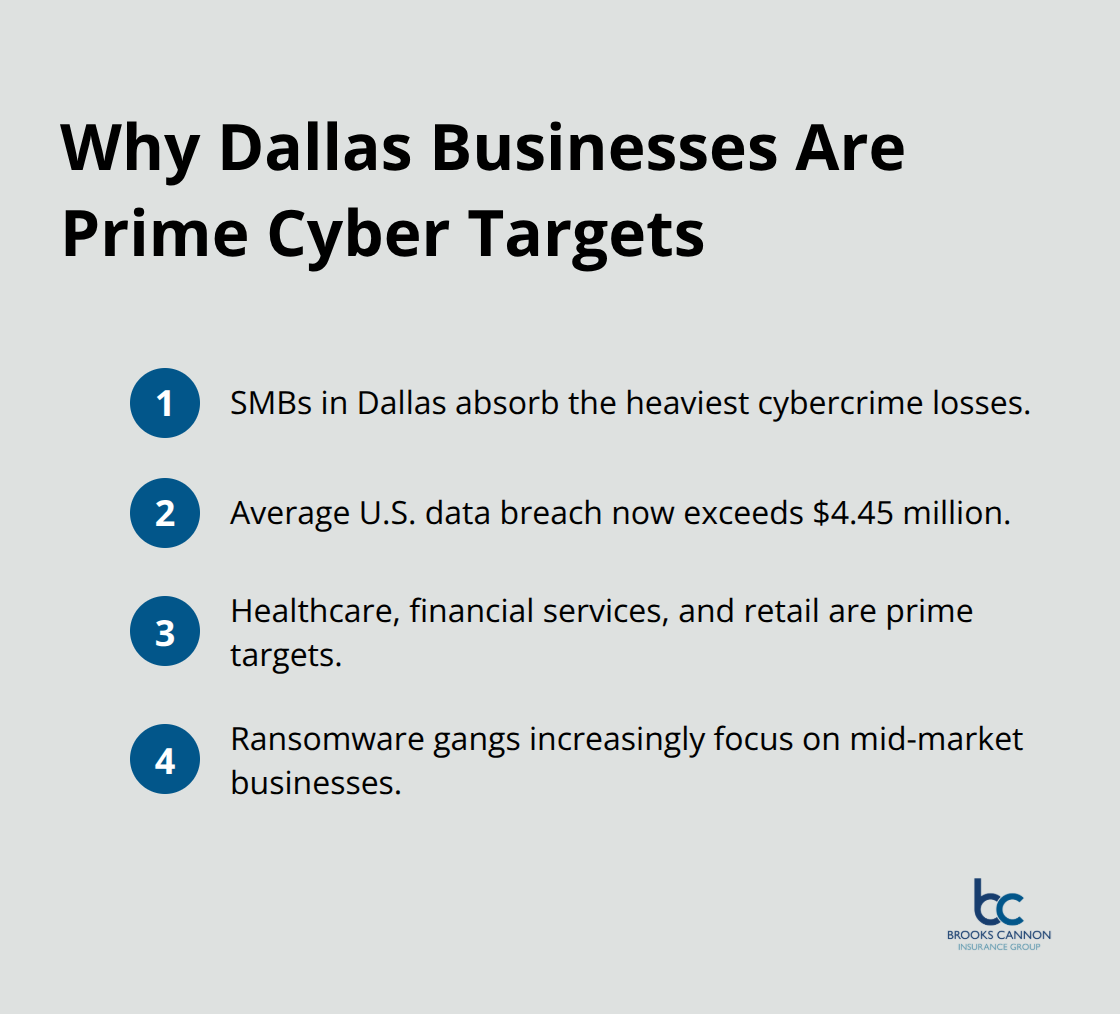

Why Dallas Businesses Are Prime Targets for Cyber Attacks

Dallas has become a hotbed for cyber criminals targeting local businesses, and the numbers prove it. 7,854 extortion attacks reported by Texans in 2024, making it the #1 cybercrime by complaint volume, with small and medium-sized companies absorbing the heaviest losses. The average cost of a data breach for a U.S. business now exceeds $4.45 million, according to IBM’s 2024 Data Breach Report, and recovery takes months of operational disruption. Dallas companies operating in healthcare, financial services, and retail face particular pressure because they store sensitive customer data that criminals actively seek. Ransomware gangs have shifted tactics to target mid-market businesses specifically, knowing they often lack the security infrastructure of larger enterprises but still possess valuable data worth paying for.

Your Business Holds Data Worth Stealing

Small Dallas businesses hold the exact information cyber criminals want: customer records, financial data, payment information, internal documents, and employee data. Most local companies store this data across multiple cloud applications, devices, and networks with limited visibility into whether their systems are properly secured. Weak passwords, outdated software, and poor access controls create easy entry points for attackers. Phishing and email-based attacks remain the top threat vector, exploiting employees who receive convincing messages requesting sensitive information or access credentials. Remote work arrangements expand the attack surface further, as employees connect through home networks and public Wi-Fi without proper encryption or security protocols. A single compromised employee account opens your entire network to attackers within minutes.

What Makes Dallas Organizations Vulnerable

Insufficient data backup and recovery planning prevents many Dallas businesses from restoring operations quickly after an incident strikes. Automated patch management remains rare among local companies, leaving outdated systems running on Windows 10 or older platforms that contain known vulnerabilities criminals actively exploit. Limited cybersecurity awareness training among staff means your employees cannot recognize sophisticated phishing attempts or understand proper data handling procedures. Access controls fail to follow the principle of least privilege, allowing employees to access systems and data far beyond what their job requires. Without continuous monitoring and threat detection capabilities, breaches go undetected for weeks or months, multiplying the damage. The Texas Attorney General requires businesses affected by breaches impacting 250 or more Texans to report within 30 days, and companies without proper incident response plans scramble to meet this deadline while simultaneously managing the crisis.

Why Cyber Liability Insurance Becomes Your Safety Net

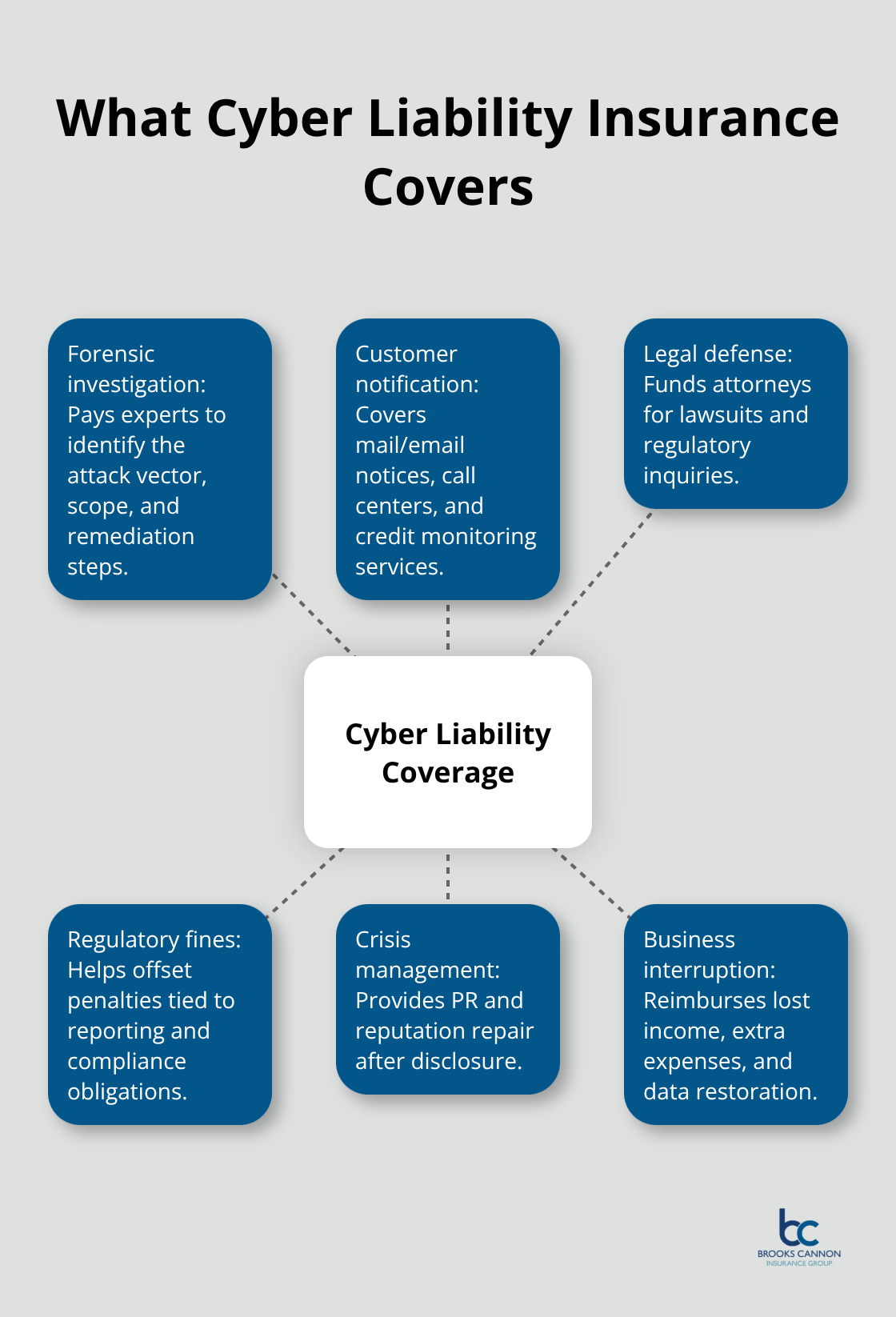

These vulnerabilities create real financial exposure that extends far beyond the initial breach. Your business faces costs for forensic investigations, legal defense, regulatory fines, crisis management, and business interruption-expenses that can total millions of dollars. Cyber liability insurance covers these gaps and protects your bottom line when an attack occurs. Understanding what this coverage includes helps you make informed decisions about protecting your Dallas business and the customers who trust you with their data.

What Cyber Liability Insurance Actually Pays For

Cyber liability insurance covers the financial wreckage that follows a data breach, and understanding exactly what your policy pays for separates smart business owners from those who discover coverage gaps after an attack. When ransomware shuts down your systems or criminals steal customer data, your immediate costs include forensic investigators who determine how the breach happened, what data was accessed, and how to prevent it from happening again. These investigations routinely cost between $50,000 and $150,000 for a mid-sized Dallas business, according to industry incident response data.

Your policy also covers the cost of notifying affected customers through mail or email, a requirement that Texas law mandates for breaches affecting 250 or more state residents. Notification expenses include printing, postage, call center operations to handle inquiries, and credit monitoring services you must offer affected individuals. Cyber liability also covers your legal defense when customers or regulators file lawsuits against your company for failing to protect their data. The Texas Attorney General requires breach reports within 30 days of discovery, and regulatory investigations often lead to fines and penalties that cyber insurance helps offset. Crisis management expenses matter equally-your business needs public relations support, reputation repair, and communications strategy to prevent customer and employee exodus after a breach becomes public.

Forensic Investigation and Breach Response

Forensic investigators determine the attack’s origin, scope, and remediation path when a breach occurs. These specialists analyze your systems, identify compromised data, and document findings for legal proceedings and regulatory compliance. Investigation costs escalate quickly for larger breaches or complex network environments. Your cyber liability policy covers these expenses, allowing you to hire qualified professionals without depleting emergency reserves. The investigation also produces documentation that supports your regulatory filings and demonstrates good-faith response efforts to the Texas Attorney General and affected customers.

Business Interruption Costs More Than Most Realize

When ransomware locks your files or a breach forces you offline for remediation, your revenue stops while expenses continue. Payroll, rent, utilities, and loan payments don’t pause during a cyber incident, yet many Dallas business owners overlook this exposure entirely. Cyber liability insurance compensates for lost income and extra expenses incurred during the downtime, allowing you to survive the recovery period without depleting reserves or taking emergency loans. A manufacturing company hit by ransomware might lose $50,000 daily in production revenue while spending $30,000 daily on incident response and recovery. Without business interruption coverage, that gap becomes catastrophic. The policy also covers costs to restore your data from backups and rebuild systems, expenses that accumulate quickly when you need vendors working around the clock to restore operations.

Regulatory Fines and Legal Defense

Lawsuits and regulatory penalties follow most significant breaches, creating legal expenses that dwarf the initial incident costs. Your cyber liability policy covers legal defense fees when customers file class-action lawsuits or regulators investigate your security practices. The Texas Attorney General imposes fines for breaches affecting 250 or more Texans, and your policy helps offset these penalties. Defense counsel experienced in cyber incidents protects your interests throughout investigations and litigation, reducing settlement amounts and reputational damage.

Security Improvements After an Attack

Some policies include betterment coverage that funds security improvements after a breach, essentially helping you upgrade your defenses so the same attack cannot succeed again. This forward-looking protection transforms a disaster into an opportunity to strengthen your security posture while the insurance carrier shares the cost of improvements. Your business can implement multi-factor authentication, upgrade to modern platforms like Windows 11, deploy continuous monitoring systems, and enhance employee training-all with partial coverage support. These investments reduce your cyber risk profile and lower future insurance premiums. Understanding what your policy covers allows you to focus on the next critical step: strengthening your defenses before an attack occurs.

Protecting Your Dallas Business Before the Attack Happens

Most Dallas business owners focus entirely on what happens after a breach, but the real protection happens before attackers ever target your company. We at Brooks Cannon Insurance Group work with businesses that invested heavily in cyber liability insurance yet still suffered devastating losses because they ignored prevention entirely. The truth is blunt: you cannot buy your way out of a cyber attack with insurance alone. Cyber liability policies cover the financial wreckage, but they do not restore your reputation, recover lost customer trust, or prevent the operational chaos that follows a breach. The businesses that survive cyber incidents with minimal damage share one common trait-they implemented security controls that made their systems difficult targets before insurance ever mattered.

Deploy Multi-Factor Authentication Across All Systems

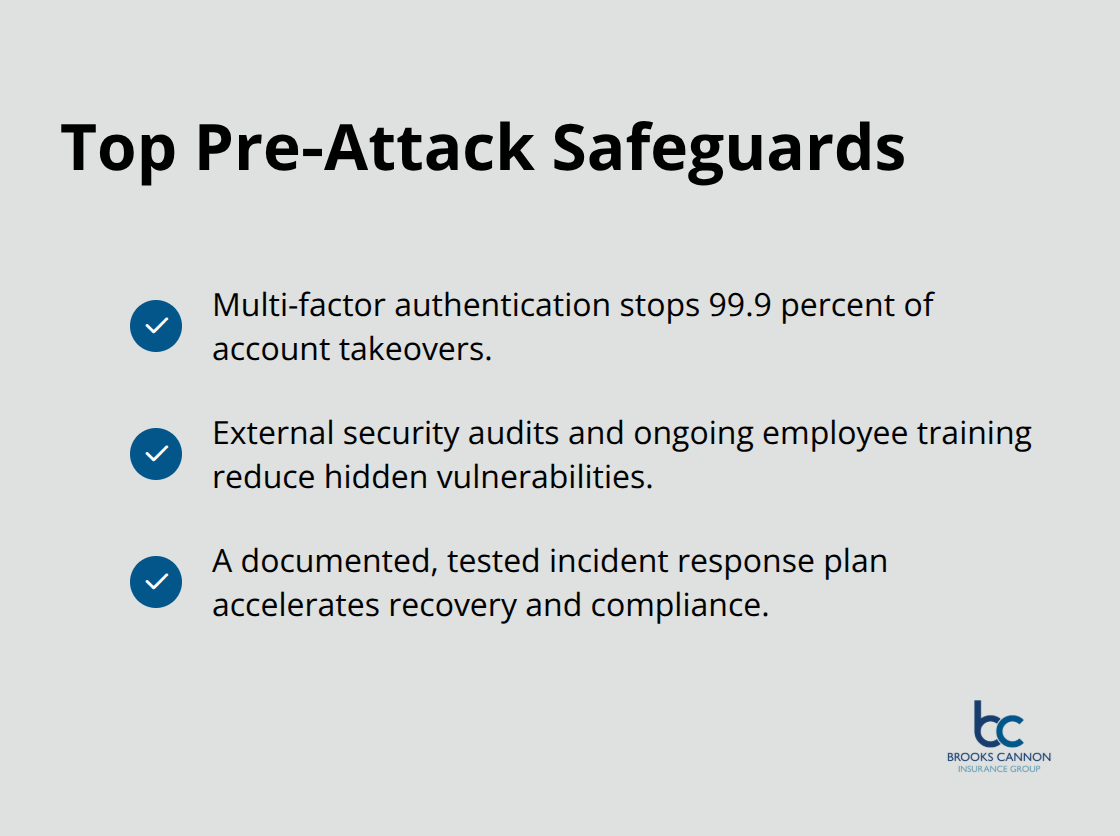

Multi-factor authentication stands as the single most effective defense against the credential theft that enables most successful attacks. When attackers compromise an employee password through phishing or credential stuffing, standard passwords grant them immediate access to your entire network. Adding a second verification factor through authentication apps, hardware keys, or SMS codes stops 99.9 percent of account takeovers cold, according to Microsoft security research. Dallas companies that deployed multi-factor authentication across all systems including email, cloud applications, and remote access tools reduced their breach risk dramatically compared to competitors relying on passwords alone. Implementation takes days, not months-most platforms support multi-factor authentication configuration in hours, and modern solutions like Windows 11 integrate this protection natively. Your employees resist initially, but resistance fades within weeks once they experience the convenience of modern authentication methods.

Conduct External Security Audits and Employee Training

Security audits conducted by external specialists identify vulnerabilities your internal team cannot see, and most Dallas small businesses skip this step entirely because they assume audits cost thousands of dollars. Reality differs sharply-many security firms offer affordable assessments specifically designed for mid-market companies, and CISA provides no-cost cybersecurity assessments and tools to strengthen your defenses. An honest security audit reveals whether your backups actually work, whether your patches deploy automatically across all devices, whether your remote access meets encryption standards, and whether employees can recognize phishing attempts. The audit becomes pointless unless you act on findings, which means allocating budget to patch management automation, upgrading outdated systems to Windows 11, and conducting ongoing employee training on data handling and incident reporting. Training programs that teach staff to recognize phishing attempts and understand proper data handling procedures transform your workforce into a security asset rather than a liability.

Establish an Incident Response Plan Now

Incident response planning separates businesses that recover quickly from those that collapse under crisis pressure. Your response plan should specify who handles different decisions, what communication templates you use for customer notifications, which forensic investigators you contact first, and how you preserve evidence for regulatory reporting. Companies without pre-established incident response plans waste critical hours deciding who approves notifications, whether you contact the Texas Attorney General immediately, and which vendors you hire-delays that compound damage and regulatory violations. Testing your response plan through tabletop exercises before an actual incident occurs identifies gaps in your procedures and builds team confidence. These three investments-multi-factor authentication, external security audits, and documented incident response procedures-cost far less than cyber liability insurance premiums yet prevent the majority of successful attacks from ever occurring.

Final Thoughts

Cyber attacks strike Dallas businesses weekly, costing millions and affecting companies of all sizes. The organizations that survive these incidents with minimal damage combine strong prevention measures with Dallas cyber liability insurance that protects their finances when prevention fails. Your policy covers forensic investigations, customer notifications, legal defense, and regulatory fines-expenses that routinely exceed $4.45 million for a single incident.

Prevention matters more than insurance alone. Implementing multi-factor authentication stops 99.9 percent of account takeovers, conducting external security audits identifies hidden vulnerabilities, and establishing an incident response plan before crisis strikes means you respond decisively rather than scrambling for decisions. These three investments cost far less than cyber liability premiums yet prevent most successful attacks from occurring at all.

Contact Brooks Cannon Insurance Group to discuss Dallas cyber liability coverage tailored to your business size and digital activity. Our team works with top-rated carriers to find protection that fits your risk profile and budget, and we help you understand what your policy covers and which prevention measures matter most for your situation. Cyber risk is not a question of if an attack will happen, but when-the time to act is now.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation