Running a business in Dallas means protecting your assets from multiple risks at once. A Business Owners Policy bundles the coverage you actually need-property protection, liability defense, and business interruption-into one streamlined package.

We at Brooks Cannon Insurance Group help Dallas business owners understand their BOP policy details so they can make confident decisions about their coverage. This guide walks you through what a BOP covers, how to evaluate your specific needs, and why the right policy matters for your bottom line.

What a Business Owners Policy Actually Covers

The Three Essential Components

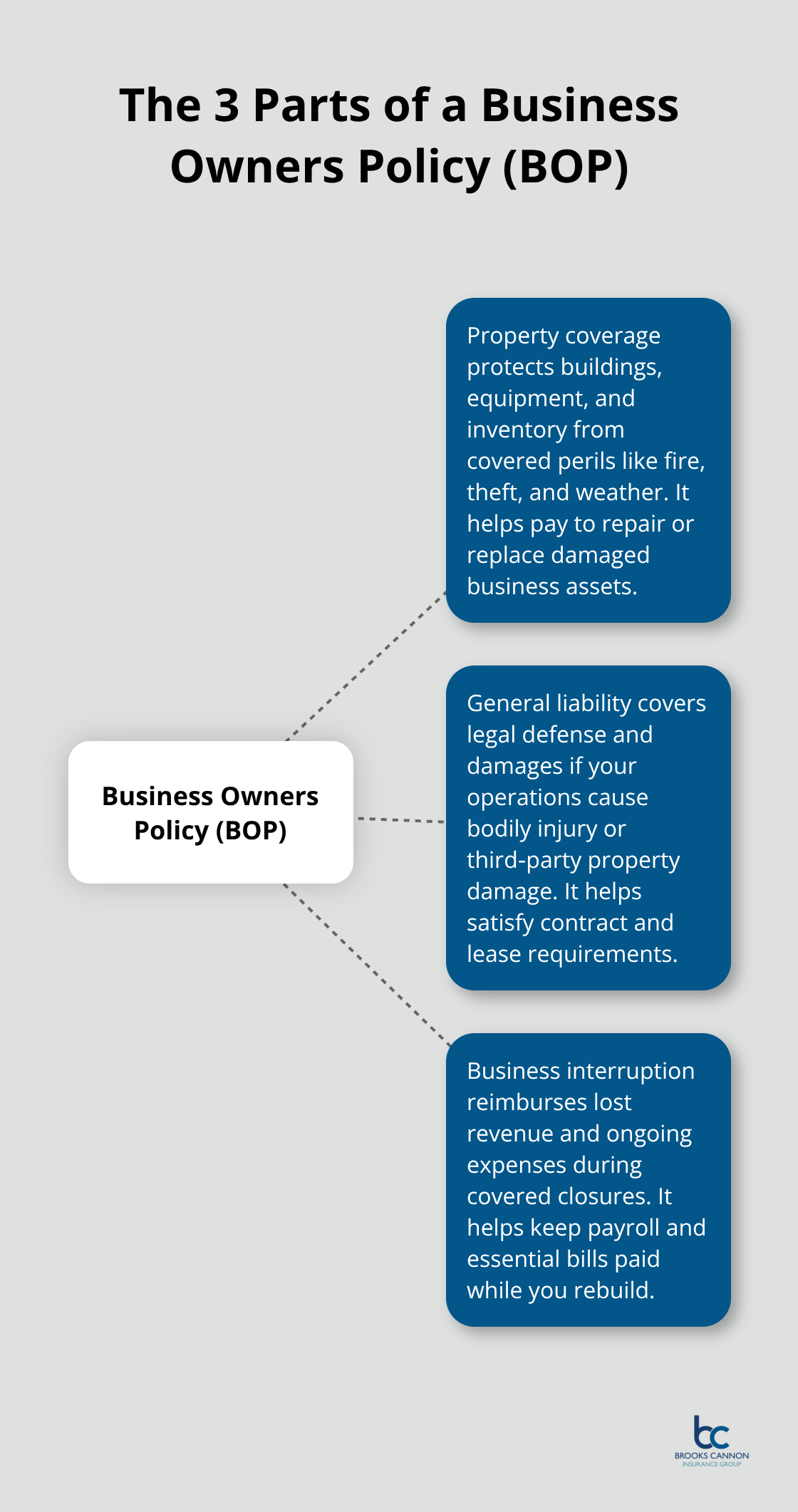

A Business Owners Policy combines three essential coverages that most Dallas businesses need: general liability protection, commercial property coverage, and business interruption insurance. Rather than buying these separately and paying full price for each one, a BOP bundles them together, which typically saves you 15-25% compared to purchasing policies individually according to the Insurance Information Institute. This cost advantage matters significantly for small business owners working with tight budgets.

The property portion protects your building, equipment, inventory, and other business assets against damage from covered events like theft, fire, or weather. General liability covers your legal costs and damages if someone is injured on your premises or if your business operations cause property damage to a third party. Business interruption coverage reimburses lost revenue and ongoing expenses when a covered event forces you to temporarily close your doors-a critical protection in Dallas, where severe weather affected Texas businesses in 2024.

Why Integration Beats Separate Policies

What separates a BOP from buying these coverages separately is the integrated approach and simplified administration. When you purchase general liability, property, and business income as individual policies, you manage three different declarations pages, three separate deductibles, and three renewal dates. A BOP consolidates everything into one policy with one deductible structure and one renewal cycle, which reduces administrative headaches.

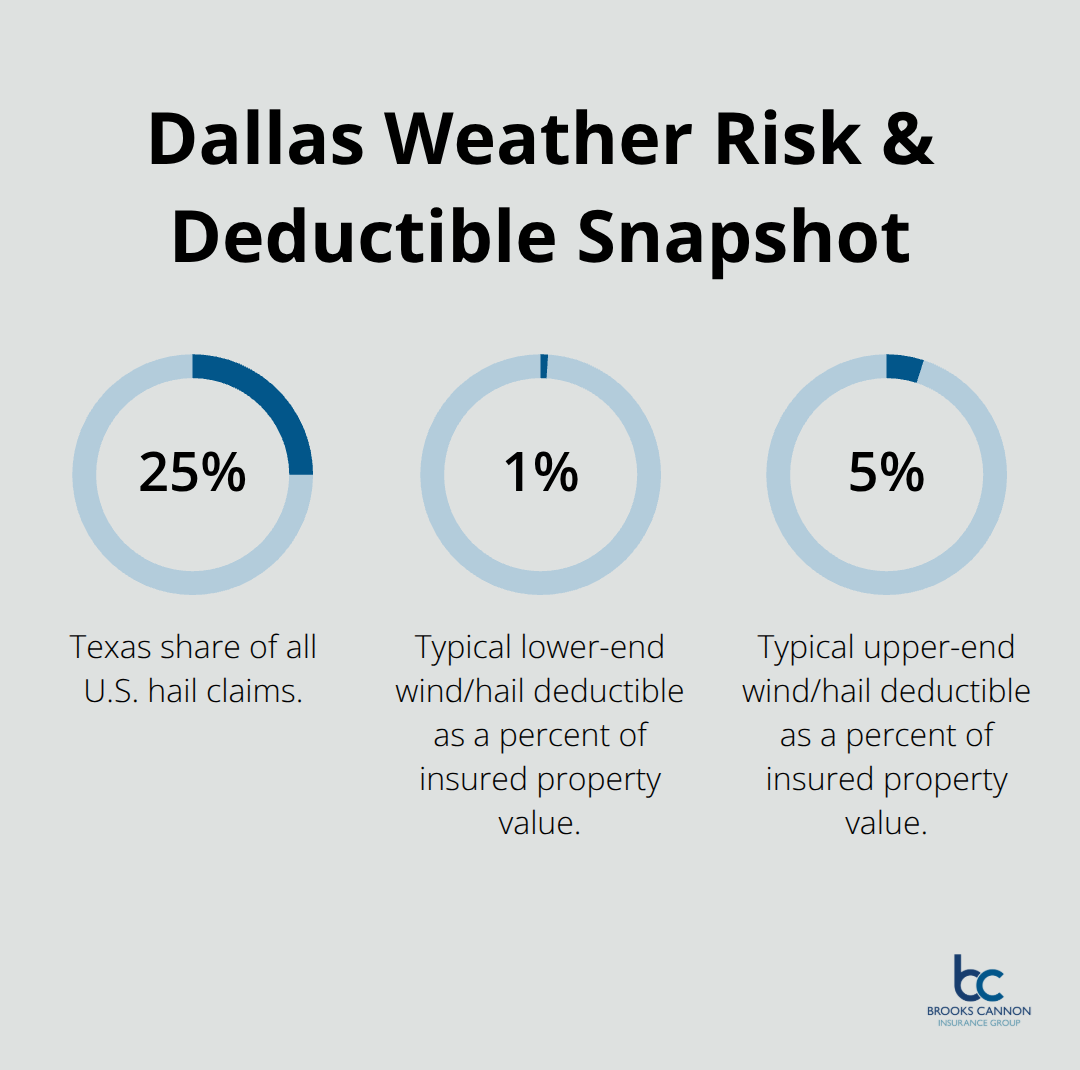

Dallas businesses face specific weather risks that make this consolidation valuable-Texas accounts for 25% of all U.S. hail claims, and in 2023 alone, hail damage exceeded 2 billion dollars statewide. A properly structured BOP addresses these local exposures through coordinated coverage rather than fragmented protection.

Additional Protections Built Into Modern BOPs

Many Dallas business owners discover that standard BOPs now include employee dishonesty coverage and limited cyber liability protection, adding layers of defense without requiring additional policies. The financial strength of your carrier matters too; when evaluating a BOP, confirm your insurer holds an A.M. Best rating of A- or higher to ensure claims get paid when disaster strikes.

As you evaluate your specific business risks and the coverage limits that match your operation, the next step involves assessing what your Dallas business actually needs from a BOP.

What Your BOP Actually Protects

Property Coverage Shields Your Business Assets

Property coverage in a Dallas BOP shields your building, equipment, inventory, and business assets from damage caused by fire, theft, vandalism, and weather events. This protection extends beyond your main location-most BOPs cover business personal property at off-premises storage facilities or temporary job sites, which matters if you operate multiple locations or store seasonal inventory elsewhere. When calculating your property limits, use replacement cost valuation, not depreciated value, because rebuilding after a loss costs significantly more than what an asset is worth on your books.

Verify whether your BOP’s standard property coverage includes flood damage or if you need a separate flood policy through the National Flood Insurance Program. Wind and hail deductibles typically run 1-5% of your insured property value, which means a $100,000 building could have a $2,500 deductible for wind or hail damage-a meaningful out-of-pocket expense that affects your decision-making during claims.

General Liability Protects Against Third-Party Claims

General liability coverage protects your business when someone claims you caused them bodily injury, property damage, or personal injury through your operations. Standard BOP liability limits range around $1 million per occurrence and $2 million aggregate, which adequately covers most small Dallas businesses, though construction firms and high-traffic retail locations often benefit from $2 million per occurrence limits to match urban exposure.

If customers or vendors require you to carry liability insurance as a condition of doing business-which happens frequently in Dallas commercial leases and government contracts-your BOP meets that requirement and generates a Certificate of Insurance within 24 hours when needed. This documentation protects your ability to bid on projects and maintain critical business relationships.

Business Interruption Covers Lost Revenue During Closures

Business interruption coverage reimburses lost revenue and ongoing expenses when a covered event forces temporary closure. Try planning for at least 12 months of business income coverage to handle extended closures from major property damage, and confirm your policy covers both lost profits and necessary operating expenses that continue even when you’re not generating revenue.

Understanding these three core protections helps you evaluate whether standard BOP limits match your operation’s actual exposure. The next step involves assessing your specific Dallas business risks and determining which coverage limits and deductibles align with your financial situation and industry classification.

Tailoring Your BOP to Match Your Dallas Business

Document Your Business Assets and Revenue

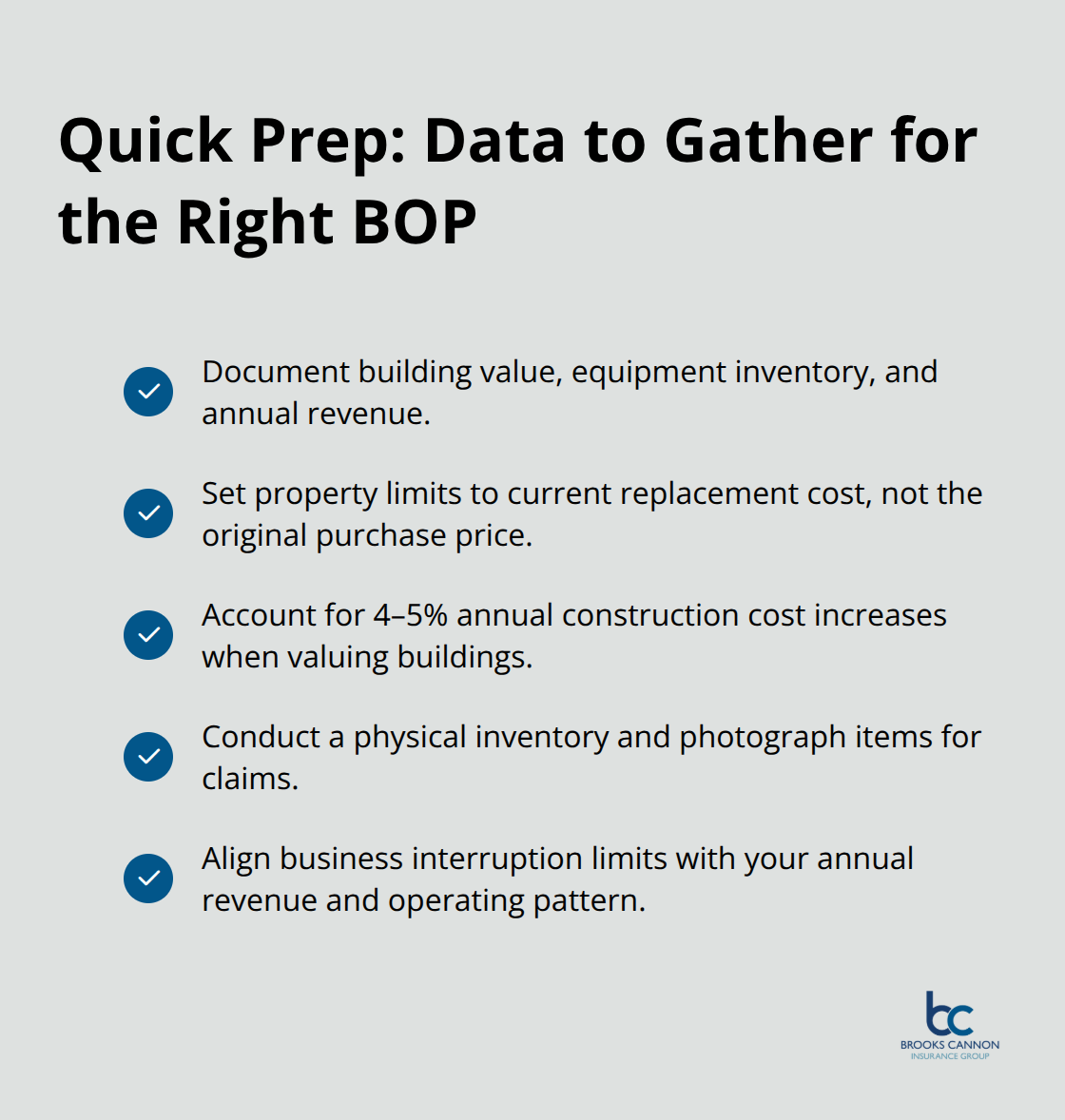

Selecting the right BOP requires honest assessment of what your business actually owns and what could realistically damage it. Start by documenting your building value, equipment inventory, and annual revenue-these three numbers drive your coverage decisions. If you own your Dallas location, your property limit should reflect current replacement cost, not purchase price from years ago. A 4-5% annual increase in construction costs means a building worth $500,000 five years ago costs significantly more to rebuild today.

For equipment and inventory, conduct a physical count and photograph items for your records. Insurance adjusters rely on documentation when settling claims, and vague estimates lead to underpayment. Your annual revenue figure determines business interruption limits-most Dallas businesses should carry coverage to survive extended closures from major property damage, though seasonal businesses might calculate differently based on their actual operating pattern.

Evaluate Deductible Levels Against Your Cash Flow

Comparing BOPs across carriers reveals meaningful differences in how deductibles affect your out-of-pocket costs during claims. A $1,000 property deductible sounds reasonable until you face a wind damage claim and realize you’re paying that amount yourself while waiting for repairs. Wind and hail deductibles often run 1-5% of your insured building value, meaning a $100,000 property could trigger a $2,500 deductible during Dallas hail season-money you need to have available immediately.

General liability deductibles typically range from $500 to $2,500, and choosing the higher deductible saves premium dollars only if your business rarely faces injury or property damage claims. Construction companies and food service operations see more liability claims than retail shops, so your industry matters when deciding deductible strategy.

Shop Multiple Carriers for Real Price Comparison

Request quotes from at least three carriers because Dallas market competition creates meaningful price variation-a $700 annual premium from one carrier versus $900 from another represents real savings over five years. An independent agent can show you premium differences at various deductible levels so you make informed choices rather than guessing.

Verify each quote includes the same limits and deductibles to compare apples-to-apples; carriers sometimes quote different liability limits or exclude certain coverages, making direct comparison impossible without detailed review. This side-by-side analysis reveals which carrier offers the best value for your specific operation and risk profile.

Final Thoughts

A Business Owners Policy delivers real protection for Dallas businesses by combining property, liability, and business interruption coverage into one streamlined package that costs 15-25% less than buying these protections separately. Understanding your Dallas BOP policy details means knowing exactly what your building and equipment are worth, how much revenue you need to survive a closure, and what deductible levels fit your cash flow situation. The specific risks you face in Dallas-hail damage, severe weather, urban liability exposure-demand coverage tailored to your location and industry, not generic protection that leaves gaps when claims happen.

Finding the right BOP requires honest assessment of your assets, realistic evaluation of your business interruption needs, and comparison shopping across multiple carriers to identify genuine value rather than just the lowest premium. Your deductible choices, liability limits, and property coverage amounts should reflect your actual operation, not industry averages or what your competitor carries. An independent agent can show you how different coverage combinations affect both your premium and your out-of-pocket costs during claims, helping you make decisions based on facts rather than assumptions.

Contact Brooks Cannon Insurance Group to discuss your Dallas business risks and receive quotes that show exactly what your coverage costs and what it protects. Our licensed team works with multiple top-rated insurance carriers, giving you access to competitive pricing and coverage options tailored to your business. We help Dallas business owners evaluate their specific risks and find BOP coverage that protects their assets without overpaying for unnecessary protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation