Your art collection represents years of passion and investment. Yet most homeowners policies leave these treasures dangerously underprotected, capping coverage at just a fraction of their true value.

Precious art protection requires specialized insurance designed specifically for fine art, collectibles, and high-value items. We at Brooks Cannon Insurance Group help Dallas collectors safeguard their most prized possessions with coverage that actually matches what they own.

Why Standard Home Insurance Falls Short for Art

Standard homeowners policies treat your art collection like any other household item, which is why they fail to protect what matters most. Most homeowners policies cap coverage for fine art at limited coverage, according to industry data from insurance brokers specializing in art protection. This means a single painting worth $10,000 or a collection of vintage jewelry totaling $50,000 receives almost no meaningful protection. The policy language typically excludes coverage for damage caused by fading, deterioration, inherent vice, or gradual wear-exactly the risks that threaten valuable art over time. Water damage and transit losses, which rank among the most frequent museum claims according to Huntington T. Block insurance experts, often fall outside standard homeowners coverage limits or come with restrictions that make claims difficult to settle.

How Agreed Value Changes Everything

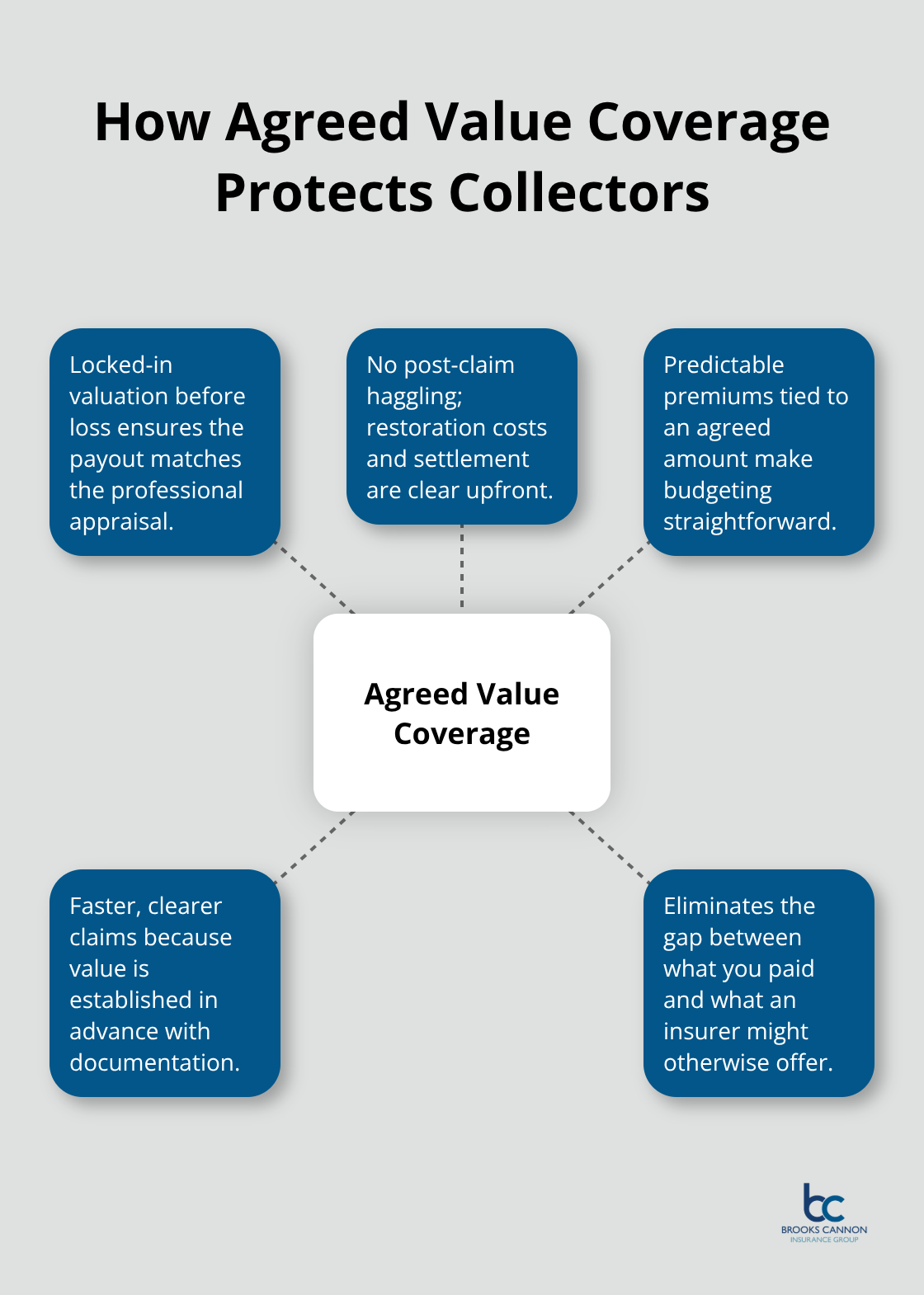

Art collection insurance works fundamentally differently. Instead of paying whatever the insurer decides your piece is worth at claim time, agreed value coverage locks in the value upfront based on a professional appraisal. You and the insurer agree on what your painting, sculpture, or collectible is worth before any loss occurs. There’s no negotiation after damage happens, no haggling over whether restoration costs are covered, and no surprise denials because the insurer questions the valuation. You pay the premium based on that agreed value, and that’s exactly what you receive if a covered loss occurs.

This approach eliminates the most common frustration Dallas collectors experience with standard policies: the gap between what they paid for their art and what an insurer will pay when something goes wrong.

Specialized Coverage for Real Threats

Fine art faces risks that standard homeowners policies simply don’t address. Professional art insurance covers packing materials, installation equipment, and transit damage-costs that add up quickly when you move valuable pieces. Many policies now include coverage for wind and storm damage, which matters increasingly as weather patterns shift. Some specialized policies address terrorism and cyberattack risks, though these typically require separate endorsements. The critical difference is that art collection insurance acknowledges what your treasures actually face: not just theft or fire, but the specific vulnerabilities of valuable objects in transit, storage, and display. Dallas collectors who’ve experienced water damage from burst pipes, fading from sunlight exposure, or damage during moves understand why generic homeowners coverage leaves them exposed. Art collection insurance closes those gaps with language written specifically for what fine art owners need.

Understanding these differences sets the stage for the next critical step: identifying which pieces in your collection actually require this specialized protection and which items demand the most attention.

What Actually Needs Specialized Art Coverage

Paintings and Sculptures: Where Most Collectors Fall Short

Not every item in your home demands art collection insurance, but identifying which pieces do is where most Dallas collectors make costly mistakes. Paintings and sculptures represent the obvious candidates, yet many collectors underestimate the value threshold that triggers real risk. A single oil painting worth $8,000 or more, or a sculpture by a recognized artist valued above $5,000, sits dangerously exposed under standard homeowners coverage. Water damage from a burst pipe, fading from sunlight exposure, or damage during transit can destroy decades of investment, yet your homeowners policy treats it the same as damaged furniture.

The problem intensifies when you own multiple pieces. A collection of five paintings averaging $6,000 each totals $30,000 in exposure, but most homeowners policies cap fine art coverage limits at $2,500 total. That gap between what you own and what your policy covers is exactly where financial disaster happens. Dallas collectors who believed they were protected until a loss revealed the truth learned this lesson the hard way.

Collectibles, Antiques, and Vintage Items: Values That Shift

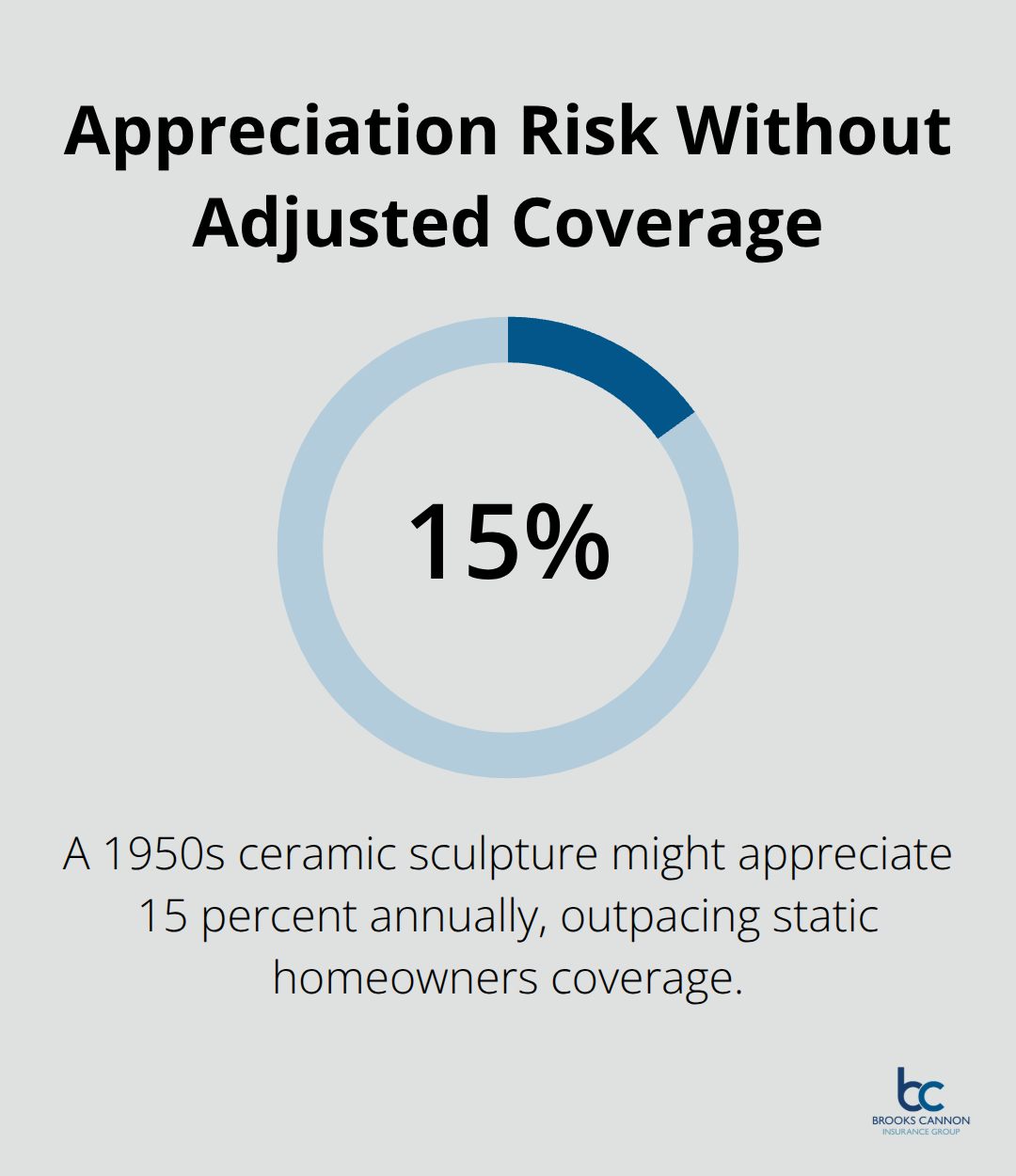

Collectibles, antiques, and vintage items demand equally serious attention because their values fluctuate in ways insurers struggle to understand. A 1950s ceramic sculpture might appreciate 15 percent annually, but your standard homeowners policy won’t adjust coverage to match that growth. Vintage jewelry compounds this problem further.

A watch collection or inherited jewelry pieces often lack recent appraisals, meaning your insurer has no basis for valuation at claim time.

High-value accessories like designer handbags, fine watches, and gemstone jewelry face specific transit risks that standard policies explicitly exclude. Specialized jewelry coverage fills gaps that homeowners policies leave wide open. Antique furniture, rare books, and collectible items face fading, deterioration, and handling damage that homeowners policies classify as wear and tear rather than covered losses.

Setting Your Protection Threshold

The critical insight is this: if you’d struggle to replace an item from your own pocket, it needs specialized coverage. That threshold differs for every collector, but try professional appraisals for any single item exceeding $5,000 or any collection category exceeding $10,000 combined value. Huntington T. Block insurance experts note that collections grow organically, and most owners fail to update their coverage as values increase.

A collection worth $25,000 five years ago might easily exceed $40,000 today through both appreciation and new acquisitions, yet your insurance remains frozen at outdated limits. High-value policies remove artificial ceilings on coverage limits, allowing you to insure jewelry and fine art at their true appraised values. This gap between your collection’s actual value and your policy’s protection creates the exact vulnerability that specialized art coverage eliminates. Understanding what you own and what it’s worth sets the foundation for the next step: assessing your collection and implementing the protections that match its true value.

How to Assess and Protect Your Art Collection

Professional Appraisals: The Foundation of Coverage

Professional appraisals form the bedrock of art collection insurance, yet most Dallas collectors postpone this step until after a loss occurs. An appraisal conducted by an International Society of Appraisers member who follows the Uniform Standards of Professional Appraisal Practice provides documentation that insurers actually trust at claim time. Without this documentation, your insurer has no basis for valuation when you file a claim, leaving you vulnerable to lowball settlement offers.

Appraisals require updates every three to five years for active collections, or whenever a piece appreciates significantly. Market conditions shift constantly, and your coverage should reflect current values. The cost of professional appraisal runs roughly $300 to $500 per piece for detailed documentation, a fraction of what you’ll lose if undervalued coverage fails you at claim time.

Documentation That Protects Your Claim

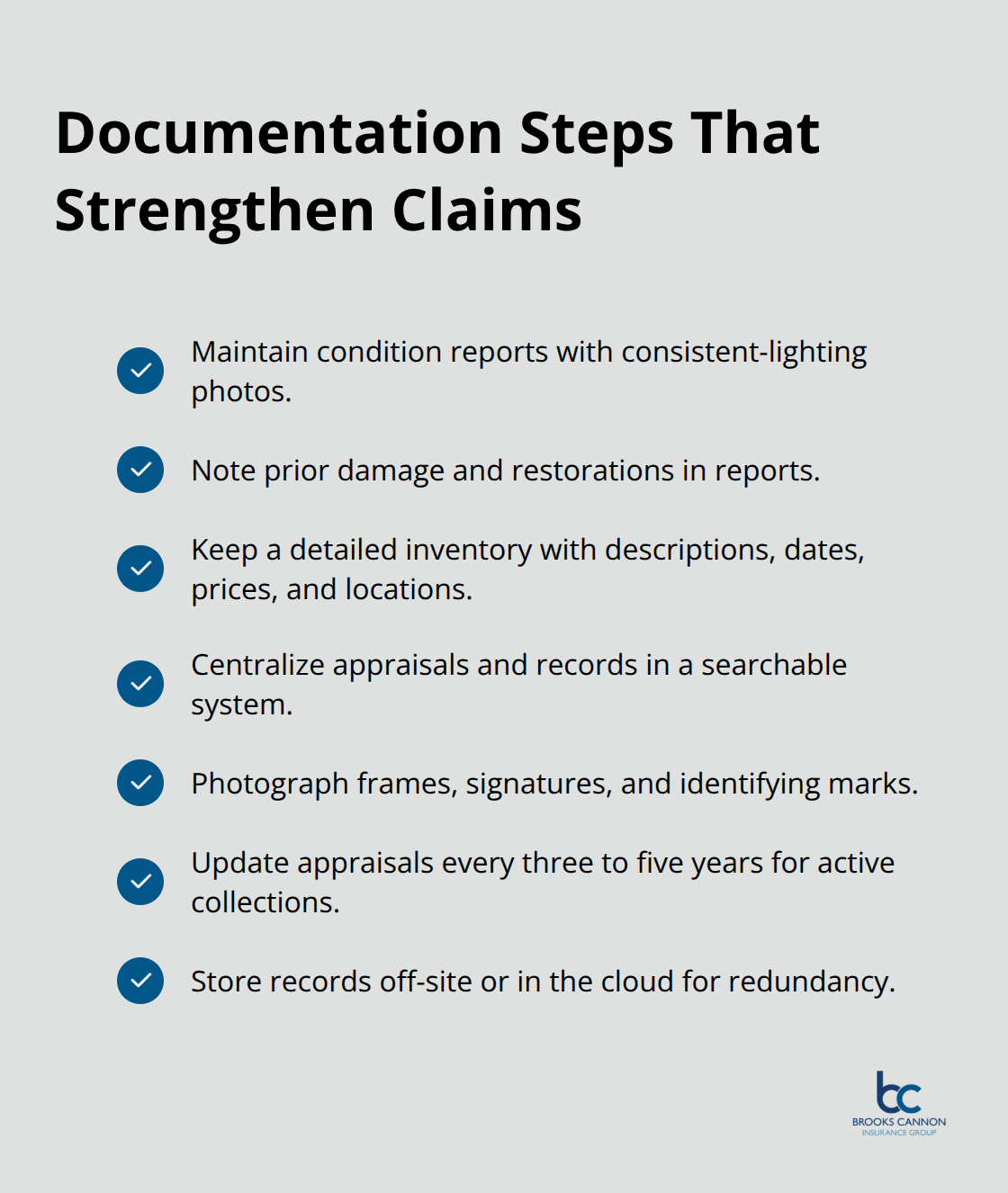

Condition reports with photographs taken in consistent lighting form your second line of defense. Note any existing damage or restoration work in these reports, as they become invaluable when documenting losses to insurers. These images eliminate disputes about what the piece looked like before damage occurred, strengthening your position during claims settlement.

Create a detailed inventory spreadsheet listing each item’s description, acquisition date, purchase price, current appraised value, location, and any special storage requirements. Many collectors use Artwork Archive or similar platforms to centralize appraisals, condition reports, and loan agreements in one searchable database. This organization matters tremendously when filing claims, as insurers demand comprehensive documentation before processing payments. Photograph every piece from multiple angles, capturing frames, signatures, and any identifying marks.

Storage and Security: Reducing Risk and Premiums

Climate-controlled storage maintains stable temperature and humidity, preventing the gradual deterioration that homeowners policies classify as wear and tear rather than covered loss. Theft-resistant display cases, alarm systems, and security cameras reduce your premiums while protecting against opportunistic theft. Document your security measures when requesting quotes, as insurers offer meaningful discounts for verified protections.

Store your images and documents separately from your home, ideally in cloud storage or a safety deposit box, so a fire or theft doesn’t destroy both your collection and your proof of ownership simultaneously. This separation strategy protects your documentation when it matters most-after a loss occurs.

Final Thoughts

Your art collection deserves protection that matches its true value, not the generic coverage that standard homeowners policies provide. Precious art protection requires three concrete steps: securing professional appraisals from qualified appraisers, documenting your collection with photographs and condition reports, and implementing security measures that reduce both risk and insurance premiums. These actions form the foundation for coverage that actually protects what you own.

Start by identifying which pieces in your collection exceed the $5,000 threshold for individual items or $10,000 for collection categories, then schedule appraisals with International Society of Appraisers members who follow professional standards. Photograph each piece and store documentation separately from your home, updating your appraisals every three to five years as values shift. Climate-controlled storage and security systems reduce your premiums while protecting against the specific risks that threaten fine art.

We at Brooks Cannon Insurance Group work with multiple top-rated insurance carriers to find coverage that protects your treasures at competitive rates. Our team understands the gaps that standard homeowners policies leave in art protection, and we specialize in matching collectors with policies that provide agreed value coverage for paintings, sculptures, collectibles, jewelry, and antiques. Contact us today to discuss your collection’s specific needs and discover how specialized art insurance closes the gaps that put your treasures at risk.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation