Running a small business in Dallas means protecting what you’ve built. A BOP insurance policy bundles the coverage you actually need-liability, property, and business income protection-into one affordable package.

We at Brooks Cannon Insurance Group see too many business owners overpaying for separate policies when a BOP could save them thousands annually. This guide walks you through what BOP insurance covers and why it makes financial sense for your operation.

What a BOP Actually Covers

The Three Essential Protections in One Package

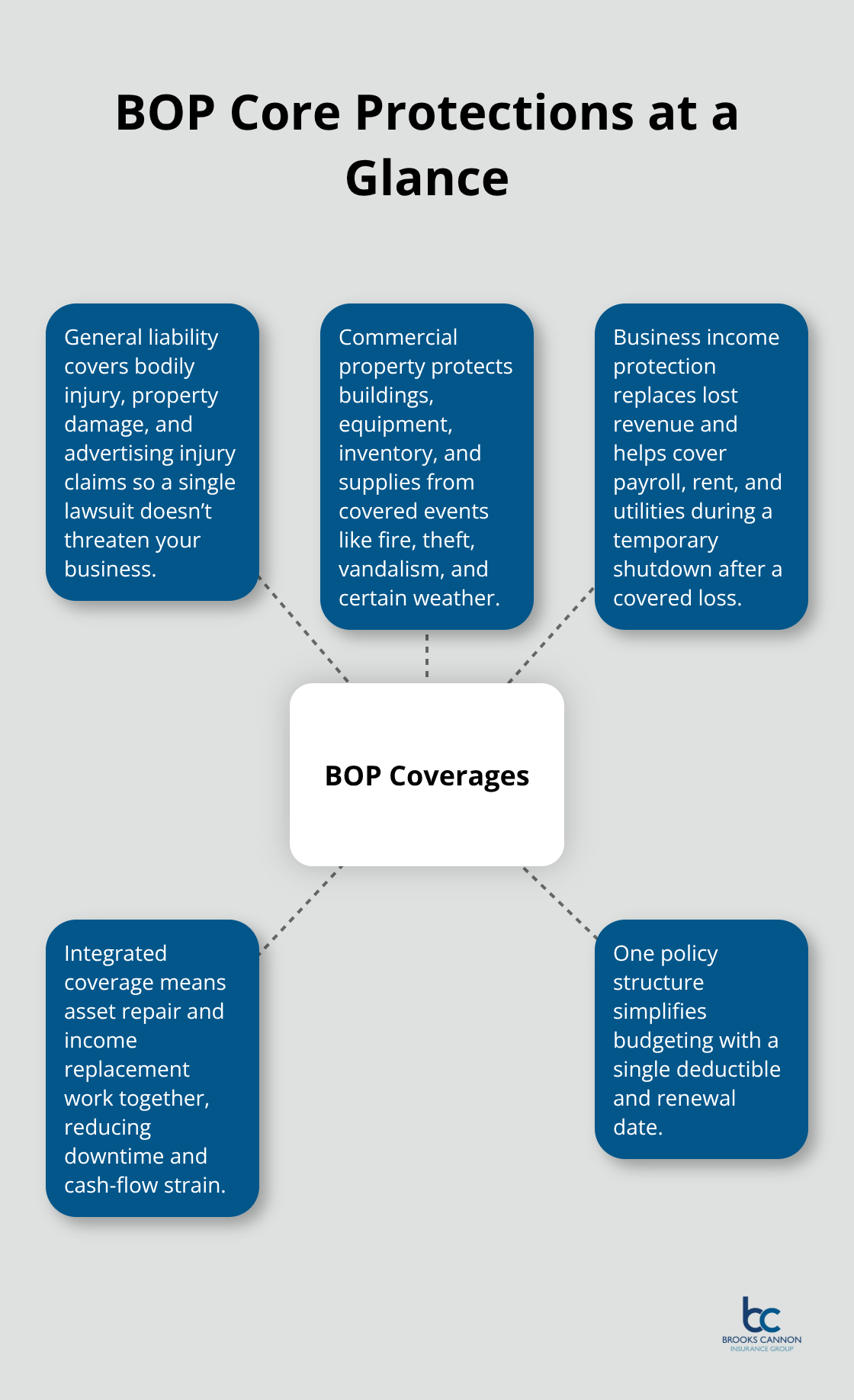

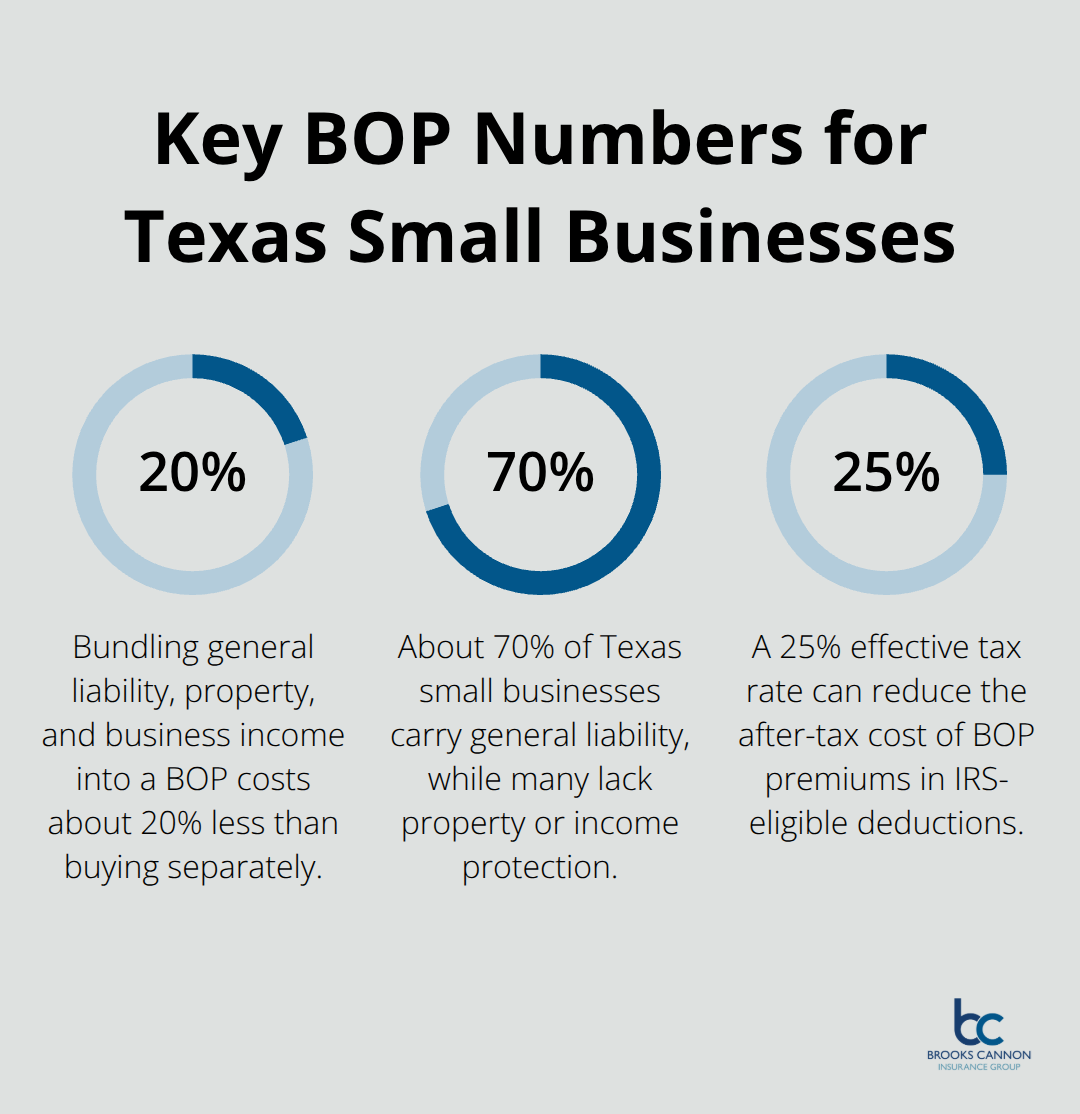

A Business Owners Policy packages three essential coverages into one policy: general liability, commercial property, and business income protection. General liability covers bodily injury and property damage claims when someone is hurt or their property is damaged because of your business operations. Commercial property protects your building, equipment, inventory, and supplies from fire, theft, weather, and other covered events. Business income coverage replaces lost revenue if a covered event forces you to temporarily close or reduces your ability to operate. According to the National Association of Insurance Commissioners, bundling these three coverages into a BOP costs about 20% less than purchasing them separately-a significant advantage for Dallas small businesses operating on tight margins.

Why Separate Policies Create Problems

Buying general liability, property, and business interruption as individual policies creates gaps and wastes money. Many business owners don’t realize that a standard property policy alone leaves them exposed to liability claims, while a liability-only policy offers zero protection if a fire destroys your equipment or inventory. A BOP solves this problem by combining protections in one package with one deductible and one renewal date, making your coverage simpler to manage and your budget easier to track.

The Coverage Gap Most Dallas Businesses Face

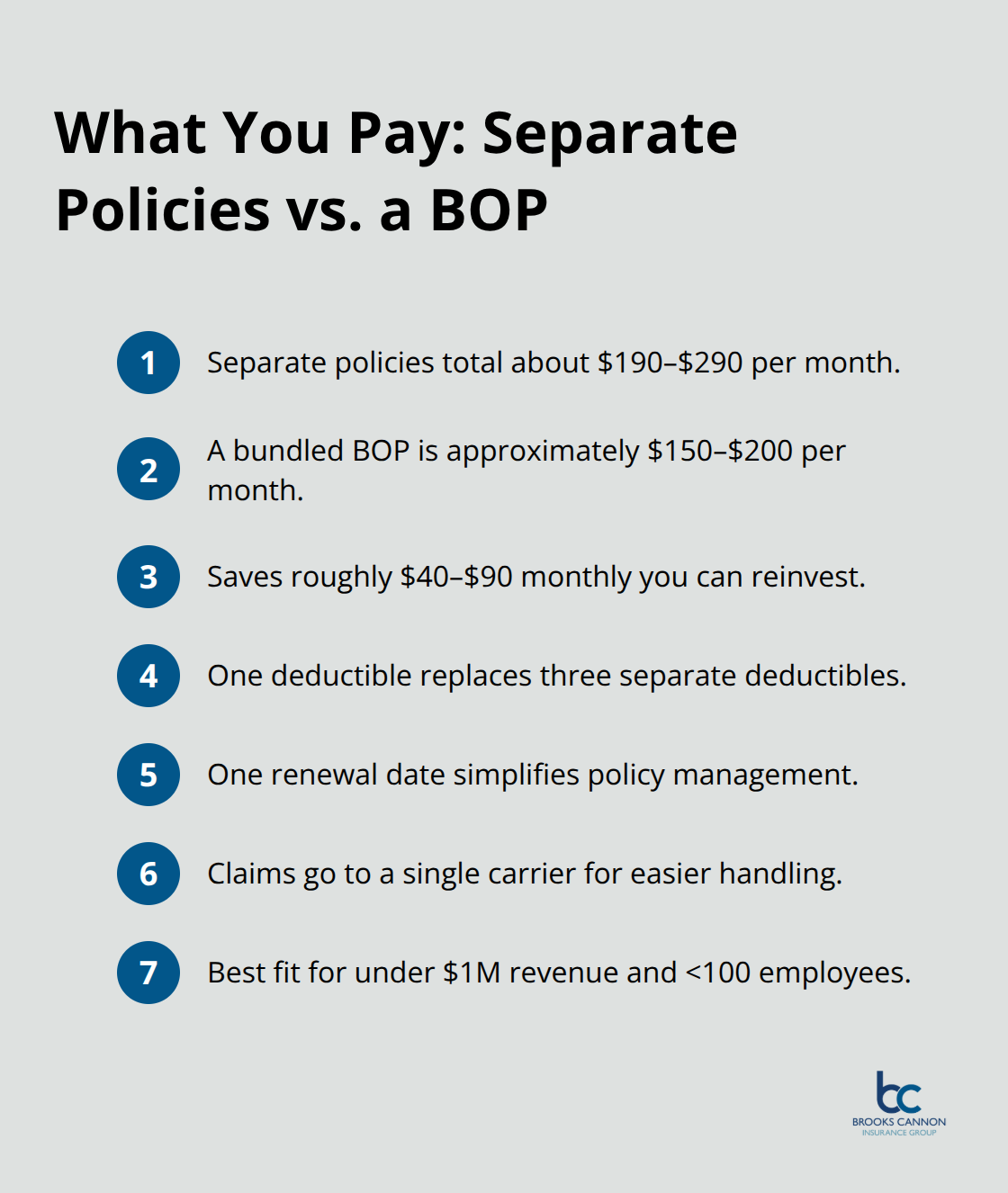

In Texas, approximately 70% of small businesses carry general liability coverage, but far fewer have adequate property or business income protection, leaving them vulnerable to catastrophic losses. For Dallas retailers, restaurants, and service businesses with less than $1 million in annual revenue and fewer than 100 employees, a BOP is the most practical first step because it addresses the two biggest risks small business owners face: someone suing you and losing revenue when disaster strikes.

Understanding what specific coverages your industry needs (and what optional add-ons might protect you further) requires a closer look at how BOPs adapt to different business types and risk profiles.

What Each Part of Your BOP Actually Protects

General Liability: Your Defense Against Lawsuits

General liability coverage within your BOP handles the claims that keep business owners awake at night. If a customer slips in your retail space and sues for medical bills and lost wages, or if your service accidentally damages a client’s property, general liability covers their legal defense costs and damages up to your policy limit. For a small Dallas retail business, general liability typically costs between $65 and $90 monthly according to industry pricing data, but bundling it into a BOP reduces that cost significantly. The coverage applies to bodily injury, property damage, and advertising liability claims-meaning if someone claims your marketing materials harmed their reputation, that defense falls under this protection. An estimated 12 million lawsuits are filed against small businesses every year, and without this coverage, a single claim could bankrupt a small operation.

Property Coverage: Protecting Your Physical Assets

Property coverage protects the physical assets that generate your revenue. Your building, leased equipment, owned machinery, inventory, and supplies all fall under this protection when fire, theft, vandalism, or weather damage strikes. Dallas businesses face real weather threats; Texas suffered about $2.7 billion in severe-weather property damage in 2024 according to the Insurance Information Institute, making this coverage essential rather than optional. This protection covers losses that would otherwise force you to replace equipment and inventory out of pocket while your business sits idle.

Business Income Protection: Replacing Lost Revenue

Business income protection is where many Dallas owners discover the true value of a BOP. If a covered event forces temporary closure, this coverage replaces your lost revenue and covers ongoing expenses like payroll, rent, and utilities while you rebuild. Texas businesses faced approximately $1.2 billion in business interruption losses due to severe weather in 2024 according to NOAA data, demonstrating that income loss often exceeds property damage in real disasters. The combination of these three protections in one package means you maintain continuous operation during recovery rather than watching cash flow disappear while waiting for repairs.

How These Protections Work Together

The real strength of a BOP lies in how these three coverages interact. A property loss triggers both immediate asset replacement and business income protection, so you recover your physical assets and your revenue stream simultaneously. This integrated approach (unlike separate policies that operate independently) addresses the full scope of what a disaster actually costs your business. Understanding how your specific industry uses these protections helps you identify which optional add-ons strengthen your coverage further.

Cost Savings and Flexibility of BOP Insurance

The 20% Savings That Adds Up Fast

A BOP costs roughly 20% less than purchasing general liability, commercial property, and business income coverage separately. For a Dallas small business, that difference translates into real money. If general liability runs $65 to $90 monthly, property coverage costs $75 to $120 monthly, and business income protection adds another $50 to $80 monthly when bought individually, you’re spending $190 to $290 per month across three separate policies. A bundled BOP collapses that into a single package at approximately $150 to $200 monthly for the same protections, freeing up $40 to $90 monthly for payroll, inventory, or growth.

The savings multiply when you factor in a single deductible instead of three separate ones, one renewal date instead of staggered renewal cycles, and simplified claims reporting to a single carrier. The bundling discount exists because insurers reduce administrative overhead when policies combine, and they pass those savings to customers. For businesses with under $1 million in annual revenue and fewer than 100 employees, a BOP represents the most cost-efficient starting point for comprehensive protection.

Customization Matches Your Actual Risks

The real advantage emerges when you customize a BOP to match your specific industry risks rather than paying for generic coverage you don’t need. A restaurant owner doesn’t benefit from inland marine coverage designed for contractors, so stripping unnecessary add-ons keeps premiums lean while adding liquor liability protection that actually matters for their operation. Construction firms can layer in contractors’ equipment and hired-vehicle coverage without purchasing a bloated policy full of irrelevant protections. Retail businesses might add crime coverage for cash handling without paying for professional liability designed for consultants.

This flexibility means your premium reflects your actual risk profile, not a one-size-fits-all template. Commercial property insurance alone typically costs $75 to $120 monthly, but when bundled into a BOP and tailored to exclude irrelevant coverages, that same protection shrinks substantially.

Tax Deductions Lower Your True Cost

Business insurance premiums qualify as tax-deductible business expenses under IRS guidelines, reducing your effective out-of-pocket cost by your marginal tax rate. A business paying a 25% effective tax rate on a $1,800 annual BOP premium effectively pays $1,350 after tax deduction benefits. This tax advantage applies whether you purchase a BOP or separate policies, but the BOP’s lower base cost amplifies the benefit.

Annual Reviews Prevent Underinsurance

Revisiting your BOP annually with an agent ensures your coverage grows with your business rather than remaining frozen at last year’s revenue and asset levels.

Final Thoughts

A BOP insurance policy protects your Dallas business investment by combining the three coverages you actually need into one affordable, manageable package. General liability, property protection, and business income coverage work together to address both immediate threats and revenue loss when disaster strikes. The 20% cost savings compared to separate policies, combined with customization options that eliminate unnecessary coverage, makes BOP insurance the practical foundation for small business protection in Texas.

Choosing the right BOP means matching coverage to your specific industry and risk profile rather than accepting generic templates. A retail business needs different protections than a contractor or professional service firm, and your annual revenue, number of employees, physical assets, and operational risks all shape which add-ons strengthen your policy. Working with an agent who understands Dallas business conditions and Texas insurance requirements ensures your coverage reflects reality rather than assumptions.

Contact Brooks Cannon Insurance Group to discuss your business, review your current coverage gaps, and get quotes for a customized BOP that fits your actual needs and budget. Most carriers provide same-day quotes and can issue coverage quickly when you need it for contracts or lease requirements. Our team works with multiple carriers to compare options and deliver competitive pricing tailored to your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation