Construction projects in Dallas face real risks-from severe weather to equipment theft to unexpected delays. A builders risk policy Dallas protects your investment when accidents happen on site.

At Brooks Cannon Insurance Group, we help contractors and builders understand what coverage they actually need. The right policy can mean the difference between a minor setback and a financial disaster.

What Builders Risk Insurance Actually Covers

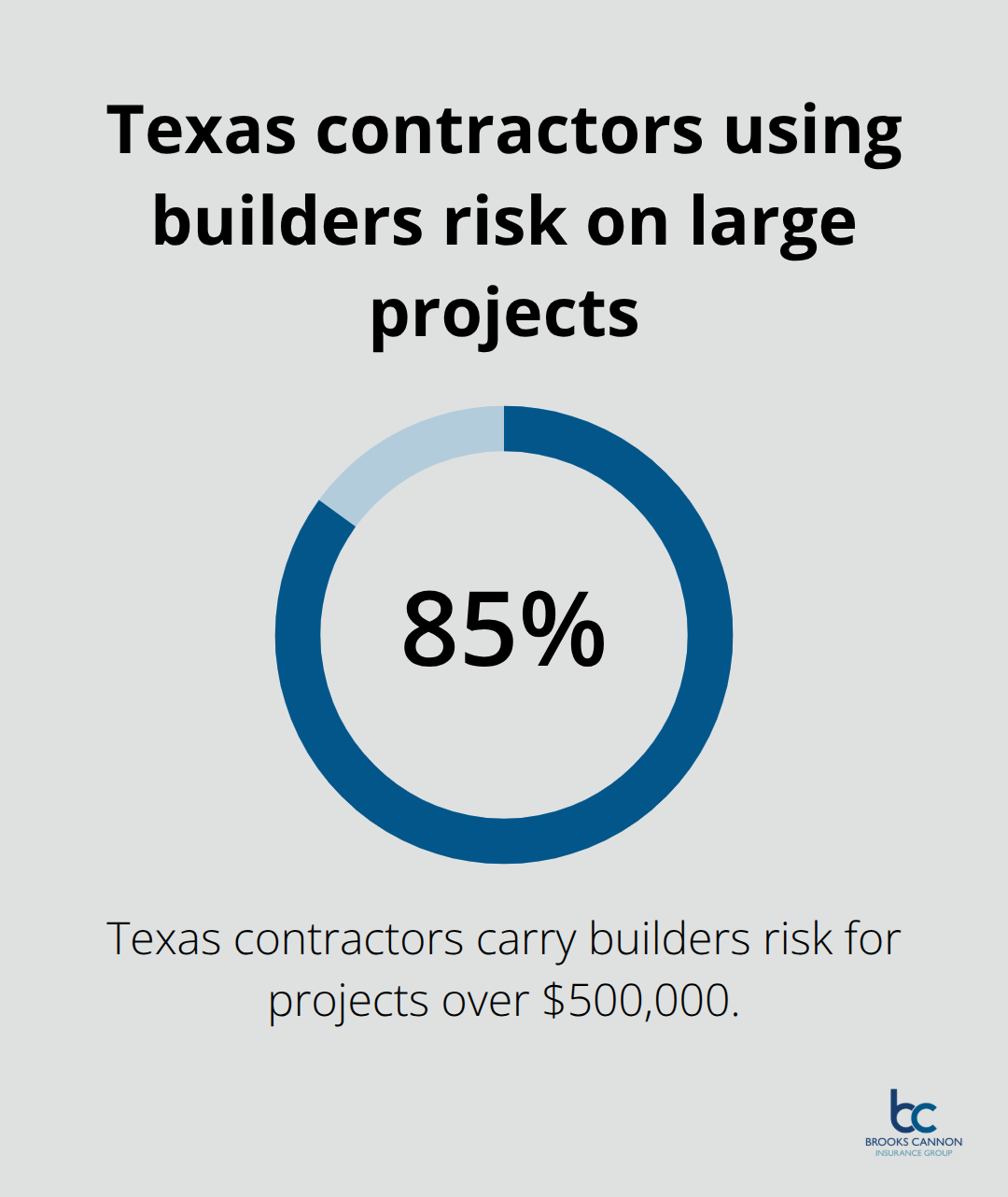

Builders risk insurance protects the physical structure under construction, along with materials, equipment, and fixtures on your Dallas project site. This coverage differs fundamentally from standard property or homeowners policies, which exclude active construction. Coverage starts when materials arrive or construction begins and continues until the building reaches substantial completion and occupancy. According to the Associated General Contractors of America, 85% of contractors in Texas carry builders risk for projects over $500,000-and for good reason. A single weather event or theft incident can wipe out months of progress and thousands of dollars in materials.

Dallas Weather Creates Real Risk

North Texas experiences specific perils that demand robust coverage. In 2023 alone, NOAA recorded 118 tornadoes across Texas, and Dallas sits in a high hail-risk zone where spring storms regularly damage exposed structures and materials. Heavy rainfall poses another serious threat-water damage to framing, drywall, and mechanical systems can occur before the building envelope closes. Wind and lightning strike exposed materials and partially completed structures at higher risk than finished buildings. Your builders risk policy in Dallas must cover these weather-related losses because standard construction insurance gaps leave contractors exposed to massive financial liability when storms hit.

Theft and Vandalism on Construction Sites

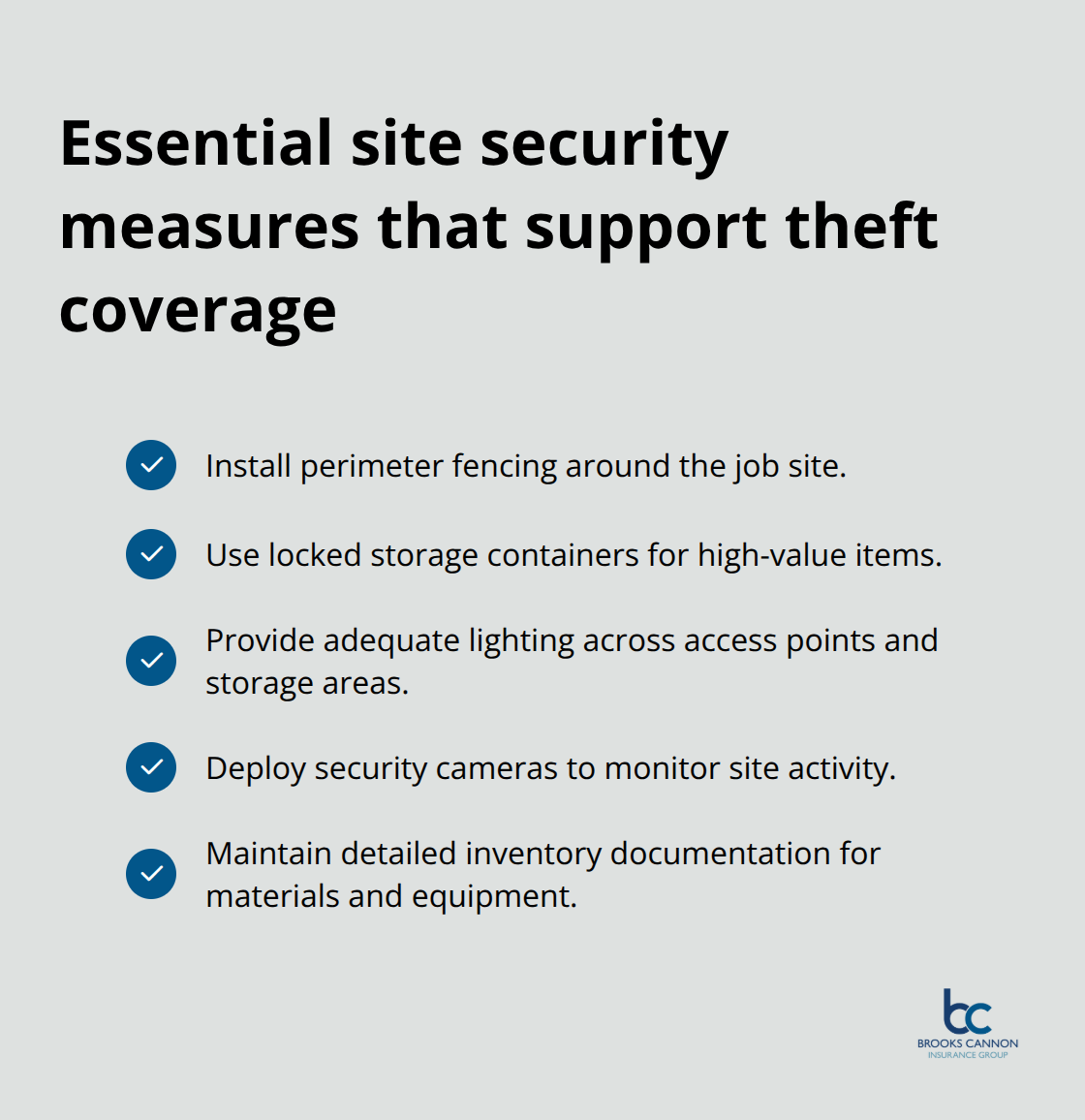

Construction theft in Texas is rampant. Copper wiring, HVAC units, appliances, tools, and lumber disappear from Dallas job sites regularly, and your policy needs to address this reality. Standard builders risk covers theft of materials and installed equipment on site, as well as materials in temporary storage and transit. However, the coverage only works if you implement basic security measures-perimeter fencing, locked storage containers, adequate lighting, security cameras, and inventory documentation all reduce theft claims and may lower your premium. Employee theft is explicitly excluded from standard policies, so if you need protection against internal theft, you’ll require a separate crime or fidelity bond.

Aligning Theft Coverage with Your Project

Verify that your policy’s theft limits align with your project’s material value and that off-site storage coverage matches your logistics plan. The specific items at highest risk on Dallas sites (copper, HVAC equipment, appliances) require attention during the quote process. Work with an agent who understands Texas construction theft patterns and can recommend appropriate sub-limits for your materials and equipment. When you move forward to selecting a policy, you’ll want to know exactly which items your coverage protects and under what conditions.

What Your Dallas Builders Risk Policy Actually Covers

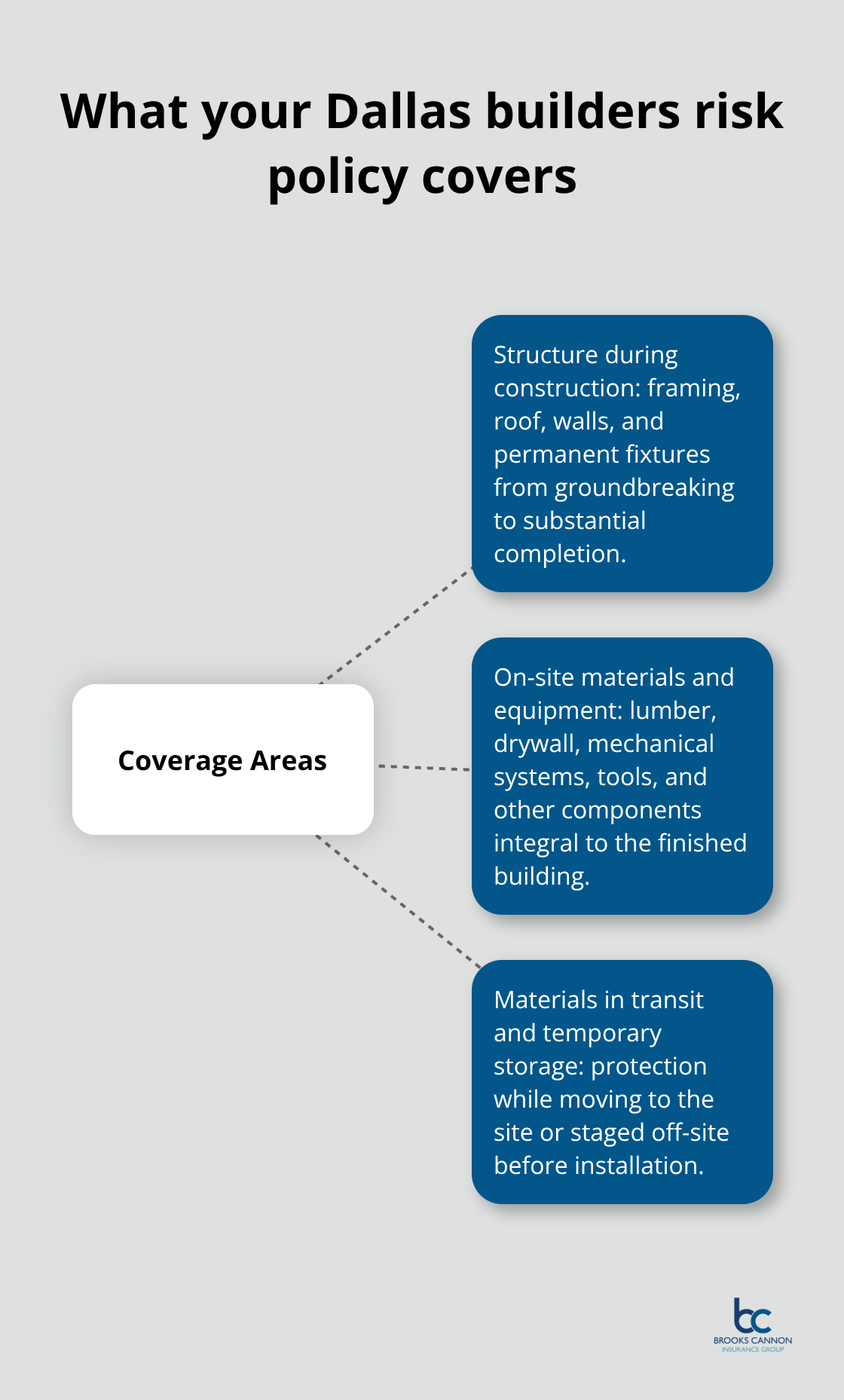

Your builders risk policy protects three critical areas on a Dallas construction site, and understanding exactly what falls under each category prevents costly gaps when claims happen. The structure itself receives coverage from groundbreaking through substantial completion-the framing, roof, walls, and permanent fixtures you install during construction. Materials and equipment on site also receive protection, including lumber, drywall, mechanical systems, tools, and anything else integral to the finished building.

Materials in transit and temporary storage locations are covered as well, which matters enormously because Dallas contractors often stage materials at off-site locations before bringing them to the job. The coverage typically costs between 1% and 3% of your total construction budget, which means a $500,000 project runs roughly $5,000 to $15,000 annually for protection. For a $1 million project, you can expect $10,000 to $30,000 in annual premium.

How Project Size and Location Affect Your Premium

These costs fluctuate based on your project’s specific perils, location within Dallas, material types, and the security measures you implement on site. A project in a high-theft neighborhood costs more than one in a secure area. Projects using wood framing face higher premiums than steel-frame construction due to fire risk. Your agent will assess these factors during the quote process and recommend coverage limits that match your actual exposure. The final premium reflects the real risk your project presents, not a one-size-fits-all calculation.

Soft Costs and Project Delays

Soft costs and project delays represent a separate coverage area that most contractors overlook until a storm or theft actually halts their timeline. Soft costs include additional architectural fees, financing interest, permit extensions, legal costs, and insurance premiums that accumulate when your project stalls. A six-month delay on a substantial project can create significant financial exposure-soft cost coverage is optional but essential for any project where timeline delays create real financial impact. Standard builders risk policies cover the physical property itself but exclude liability for third-party bodily injury or property damage, which is why you need a separate general liability policy running concurrently.

General Liability and Bundled Coverage Options

General liability protects you if a visitor is injured on site or if your construction damages a neighboring property, while builders risk protects the structure and materials you’re building. Many Dallas contractors bundle these coverages into a comprehensive contractors package to streamline administration and often reduce overall costs. When you evaluate quotes, verify that your policy includes price escalation endorsements-these protect you when material and labor costs rise unexpectedly, a real concern in Texas where supply chain disruptions have driven significant cost volatility since 2020. Without escalation coverage, a six-month project delay could leave you underinsured if lumber, steel, or concrete prices spike beyond your original estimate.

Price Escalation and Material Cost Protection

Price escalation endorsements trigger above predefined inflation thresholds (commonly 5–10%) to cover replacement costs at current market rates rather than your original budget. This protection has become increasingly standard on most Texas builders risk policies because material costs have remained volatile. Your agent should confirm whether your quote includes this endorsement and at what threshold it activates. The difference between a policy with and without escalation protection can mean thousands of dollars in coverage when prices move against you mid-project.

Now that you understand what your policy covers and how costs break down, the next step is identifying which specific endorsements and limits your Dallas project actually requires.

Selecting the Right Policy for Your Dallas Project

Start with your project’s actual dollar value and construction timeline, not industry averages. A $250,000 residential renovation costs $2,500 to $7,500 annually for builders risk, while a $1 million commercial project runs $10,000 to $30,000, according to industry cost ranges tied to the 1% to 3% of total construction budget standard. Your timeline matters equally-a three-month project requires different coverage than a two-year build. Projects lasting longer than six months typically need coverage extensions, so contact your carrier at least 30 days before your initial policy expires to avoid gaps. Dallas projects under $5 million often qualify for streamlined online quotes with minimal paperwork, while larger projects require detailed risk assessments. Collect your project scope documentation first: construction type, materials, site location within Dallas, security measures you’ll implement, and planned completion date. This documentation accelerates the quote process and ensures carriers assess your actual risk rather than worst-case scenarios.

Compare Quotes Line by Line

Never compare Dallas builders risk quotes on price alone-three carriers quoting $12,000 annually may offer drastically different coverage. One quote might include price escalation endorsements while another excludes them. One might cover soft costs delays while another treats them as optional add-ons. One might set theft sub-limits at $50,000 while another caps it at $25,000, which matters enormously if your site stores copper or HVAC equipment. Request that each carrier itemize their quote showing base premium, endorsements included, sub-limits for theft and off-site storage, deductibles by peril, and optional coverages available. Ask specifically whether their quote includes replacement cost valuation plus escalation endorsements-this matters because material costs in Texas have remained volatile since 2020. Verify whether the policy covers your specific materials and equipment, especially if your project uses specialized systems or high-value installed components. Request each carrier’s claims process details and their average claim settlement timeline, because when weather or theft hits your Dallas site, speed matters as much as coverage breadth.

Partner with an Agent Who Knows Dallas Construction

An agent familiar with Dallas construction knows that North Texas hail and spring tornado risk demands robust wind and hail coverage with lower deductibles than standard policies offer. They understand that construction theft in Texas exceeds national averages, so they’ll recommend appropriate security measures and theft sub-limits rather than standard coverage. They know which carriers write wrap-up programs (OCIP/CCIP) for large Dallas projects and can coordinate builders risk with your general liability and workers’ compensation to eliminate gaps. They understand the Texas Anti-Indemnity Act and how it affects your additional insured endorsements and contract language. Your agent should ask about your security plan, your material staging locations, your subcontractor structure, and whether you’ve experienced prior theft or weather losses-these details determine whether you receive appropriate coverage at competitive rates or overpay for coverage you don’t need. Work with an agent who offers ongoing support through your project timeline, not just someone who issues a policy and disappears.

Final Thoughts

Builders risk policy Dallas protects your construction investment from the specific perils that threaten projects in North Texas-weather damage, theft, equipment loss, and project delays can derail timelines and drain budgets, but proper coverage transforms these risks into manageable claims. The contractors who succeed in Dallas understand that builders risk insurance is not optional overhead; it’s the foundation of project protection. Your project’s size, location, materials, and timeline determine what protection you actually need, and those details matter far more than comparing quotes on price alone.

A policy that covers price escalation, soft costs, and theft with appropriate sub-limits costs more upfront but prevents catastrophic exposure when storms hit or materials disappear from your site. Lenders and project owners expect proof of coverage before funding or awarding contracts, so securing appropriate protection early eliminates delays and demonstrates contractor credibility. The right builders risk policy gives you confidence that your project can absorb unexpected losses without derailing completion dates or profitability.

We at Brooks Cannon Insurance Group understand the local risks, the carrier options, and the details that separate adequate protection from gaps that cost money when claims happen. Contact us today to discuss your project timeline, materials, and risk profile so we can deliver a quote that protects your investment and keeps your project moving forward. Our team represents carriers who understand Texas construction risk, which means your coverage reflects real Dallas conditions rather than national templates.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation