Construction projects in the Dallas area face real financial risks. Materials, equipment, and structures can be damaged or stolen before a project is complete, leaving contractors with significant losses.

We at Brooks Cannon Insurance Group created this builders risk policy guide to help you understand what protection you actually need. This guide covers the specific coverage details, exclusions, and practical steps to get properly protected.

What Builders Risk Actually Covers

A builders risk policy, also called course of construction insurance, protects the physical assets on your construction project from damage or loss before the project reaches completion. This includes the structure itself, building materials and supplies stored on-site or in transit, installed fixtures, temporary structures like scaffolding, and equipment. The policy covers specific perils such as fire, lightning, theft, vandalism, wind, hail, explosions, and water damage. Unlike general liability insurance, which covers bodily injury and property damage claims you cause to third parties, builders risk protects your own property and materials from direct physical loss.

In Texas, lenders typically require builders risk coverage to finance a project. This distinction matters because many contractors mistakenly believe general liability covers construction materials and structures, then face significant gaps when damage occurs.

Who Actually Needs This Coverage

Property owners, general contractors, subcontractors, developers, and even architects with a financial interest in the project should be named as additional insureds. If you manage the build as a contractor, you need this. If you own the property and want to protect your investment during construction, you need this. If you work as a subcontractor on portions of a larger project, confirm that you appear as an additional insured on the primary policy or carry your own coverage.

In the Dallas area, where NOAA reported 118 tornadoes in 2023 along with frequent hail and severe thunderstorms, the risk of material damage before project completion is substantial. The question isn’t whether you need builders risk-it’s whether you can absorb the full cost of replacing damaged materials, delayed schedules, and equipment losses out of pocket.

What Coverage Actually Costs

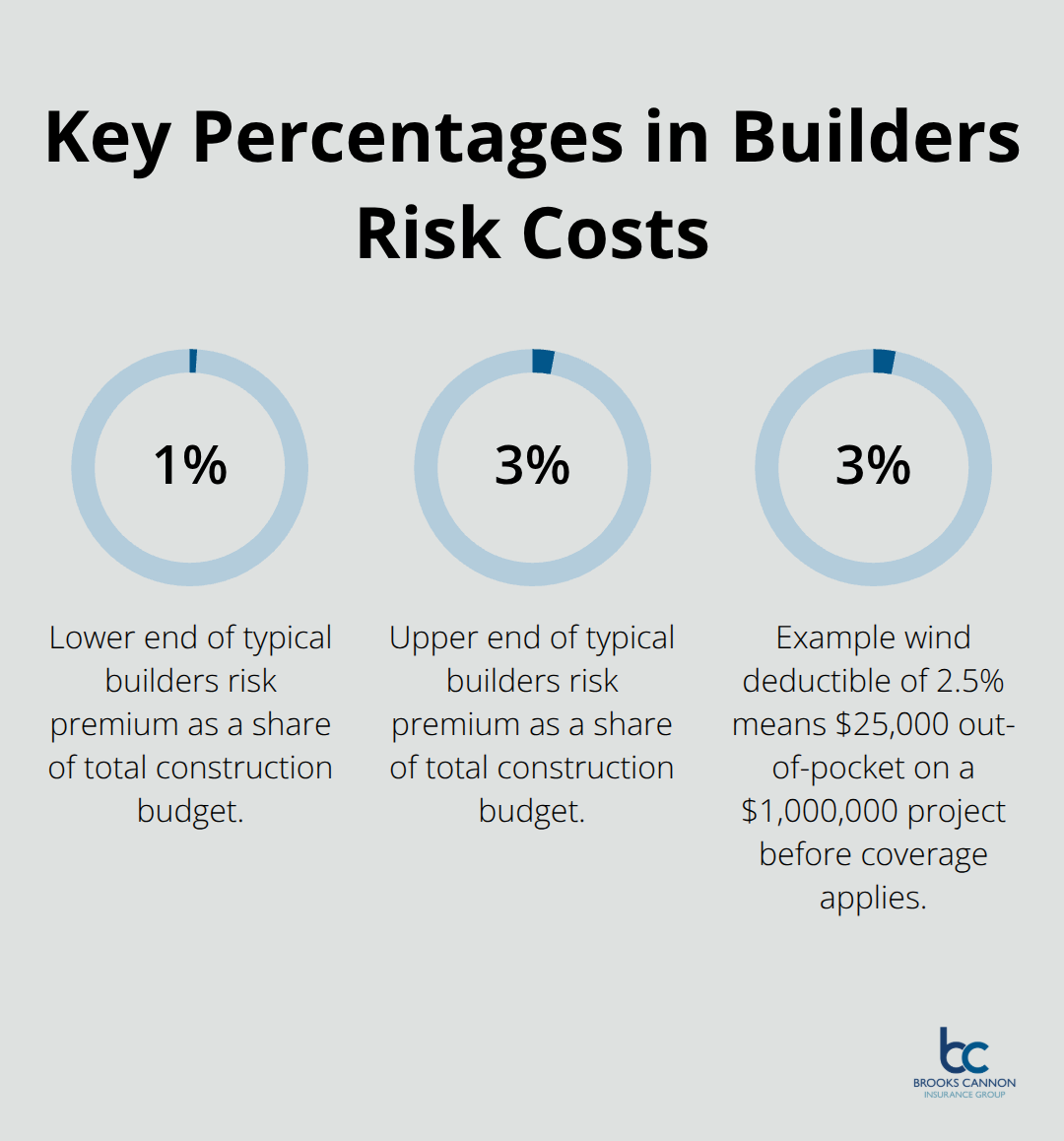

Builders risk premiums typically range from 1 to 3 percent of your total construction budget. For a $300,000 residential project, that translates to roughly $3,000 to $9,000 in annual premium. For a $2.5 million commercial project, you can expect $25,000 to $75,000. Premium costs depend on project value, construction type, location and weather exposure, project duration, security measures you have in place, and your prior claims history.

A frame construction project in North Texas costs more to insure than masonry due to fire risk. Projects lasting 12 months cost more than those lasting 3 months. Better site security with fencing, locked gates, lighting, and cameras can actually lower your premium because carriers view these as loss-prevention measures. The cost is not fixed-it’s negotiable based on the specific details of your project and how you manage risk on-site.

What Happens When Damage Occurs

When a covered peril damages your materials or structures, the policy pays for the direct physical loss. Fire destroys materials stored in a temporary trailer-the policy covers replacement costs. Hail damages roofing materials stacked on-site-you file a claim and receive compensation. Theft removes equipment from your job site-the carrier reimburses you for the loss. However, the policy does not cover every type of damage or loss. Understanding what falls outside your protection matters just as much as knowing what the policy covers, which is why the next section examines the exclusions and limitations that contractors often overlook.

What Your Builders Risk Policy Actually Protects

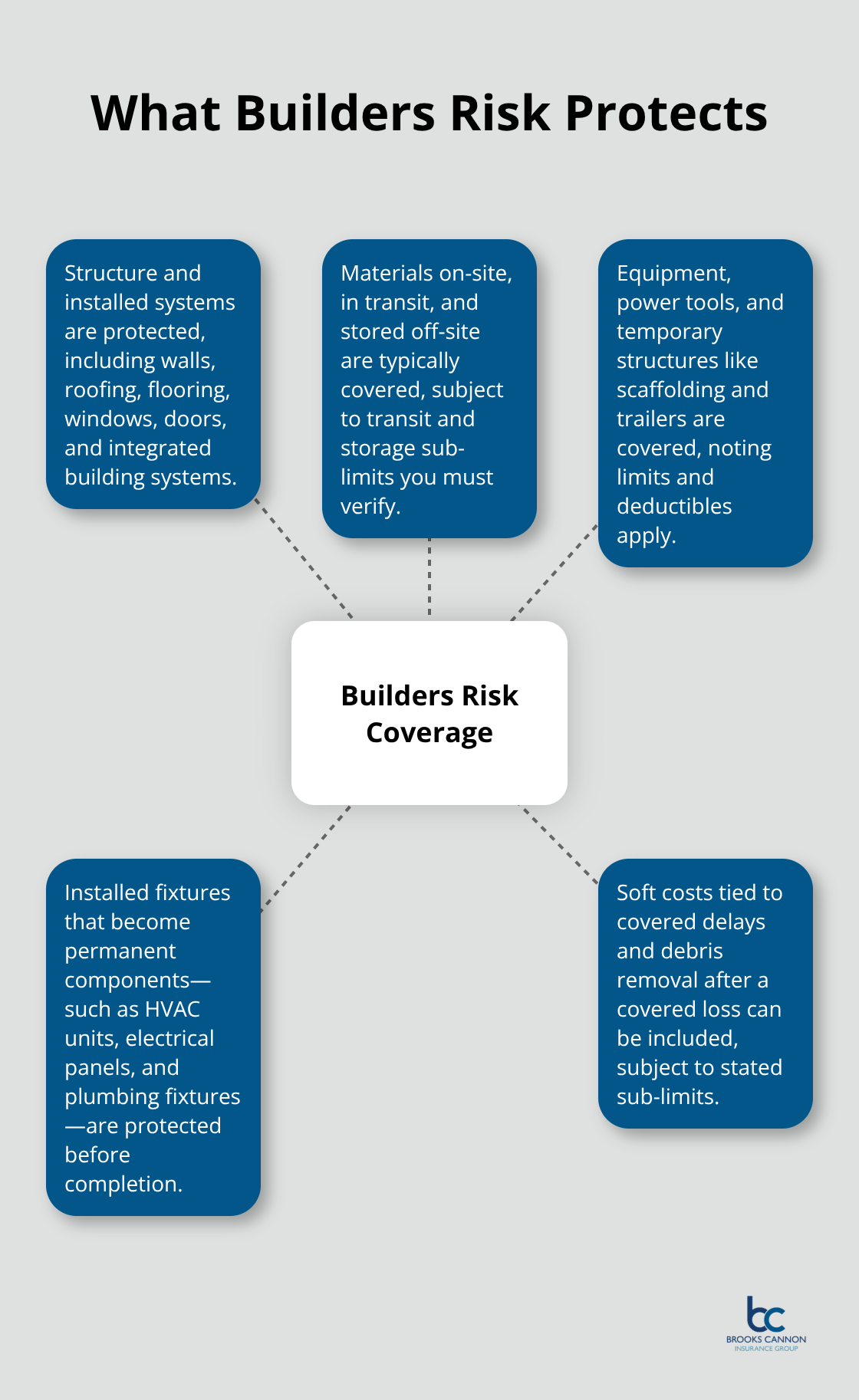

Your builders risk policy covers three distinct categories of property, and understanding exactly what falls into each category prevents expensive gaps when damage strikes.

The Structure and Installed Systems

The structure under construction itself is the primary focus-walls, roofing systems, flooring, installed fixtures like windows and doors, and any permanent systems integrated into the building all receive protection. Building materials and supplies stored on-site or staged for installation are covered, whether they sit in temporary storage containers, lie stacked on the foundation, or remain in vendor packaging. Materials in transit to your job site and materials stored at off-site locations also qualify for coverage under most policies, though you need to verify transit coverage limits and storage location details with your agent before assuming full protection.

Equipment, Tools, and Temporary Structures

Power tools, machinery, and small equipment on your job site are typically covered, but coverage limits and deductibles matter significantly. A $5,000 deductible on a $12,000 air compressor means you absorb $5,000 of the loss yourself. Temporary structures including scaffolding, construction trailers used as offices or material storage, temporary walls, and weather protection systems all receive coverage under your policy.

Installed Fixtures and Permanent Components

The policy covers installed fixtures that will become permanent parts of the building-HVAC equipment, electrical panels, plumbing fixtures, and similar items installed but not yet fully operational all qualify. This matters because a fire destroying an installed HVAC system before final inspection represents a substantial loss that you need protection against.

Soft Costs and Debris Removal

Soft costs associated with project delays triggered by covered damage also receive coverage under most policies. If hail destroys roofing materials and delays your project by two weeks, the policy can cover lost labor, extended equipment rental, and other delay-related expenses. The specific dollar limits for soft costs vary by policy, so confirm these sub-limits with your agent-some policies cap soft cost coverage at $25,000 while others offer $100,000 or higher depending on project value.

Debris removal costs following a covered loss are typically included, which matters because removing damaged materials and cleaning up the site after fire, theft, or weather damage adds substantial expense beyond just replacing the damaged property itself.

Understanding what your policy covers is only half the battle. The exclusions and limitations in your policy can create significant protection gaps, and many contractors discover these gaps only after damage occurs and a claim is denied.

What Your Policy Doesn’t Cover

Builders risk policies exclude specific perils and situations that contractors often assume are protected, and these gaps create serious financial exposure on Dallas-area projects. The most significant exclusion involves weather-related damage classified as acts of God. Flood damage in Texas is excluded from standard builders risk policies. If water from a severe storm floods your job site and destroys materials stored at ground level, your standard policy denies the claim. You need a separate flood insurance endorsement or standalone flood policy to cover this exposure. Similarly, earthquake damage is excluded from standard policies in most states, though you can purchase an earthquake endorsement if your project sits in an area with seismic activity.

Wind Coverage and Deductibles in North Texas

Wind damage presents a more complex situation in North Texas. While standard builders risk policies cover wind and hail damage, carriers often impose higher deductibles or exclude wind coverage in hurricane-prone coastal zones. If you work on a project in Dallas or Fort Worth, wind coverage is typically included, but verify this explicitly with your agent because deductible amounts vary significantly. A policy with a 2.5 percent wind deductible on a $1 million project means you absorb $25,000 of wind damage losses yourself before coverage activates.

Theft and Vandalism Restrictions

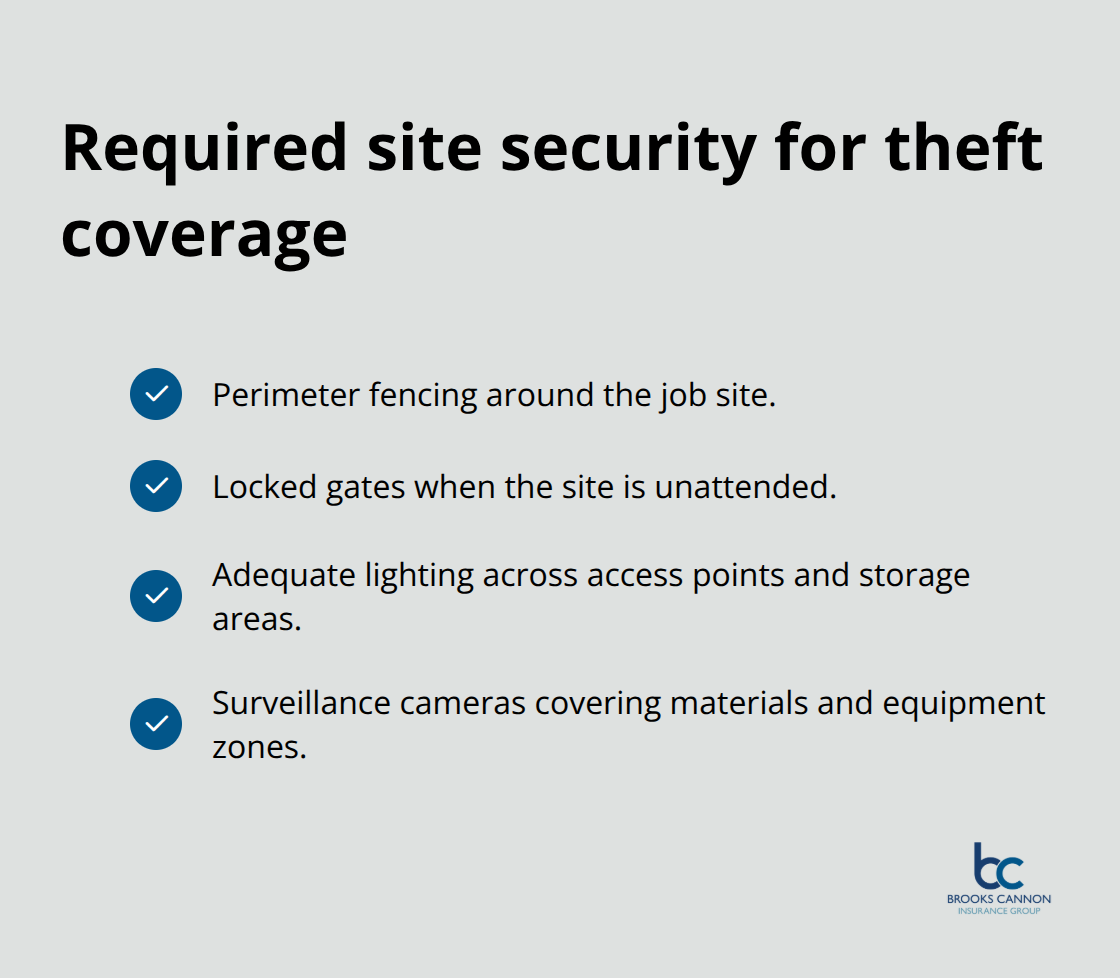

Theft and vandalism coverage contains restrictions that many contractors overlook until materials disappear from their site. Standard policies cover theft of materials and equipment stored on-site, but coverage applies only if you maintain reasonable security measures including perimeter fencing, locked gates, adequate lighting, and surveillance cameras. Carriers view these as loss-prevention requirements, not optional upgrades. If your job site lacks proper fencing and materials are stolen, the carrier may deny your claim based on inadequate security.

General liability coverage is explicitly excluded from builders risk policies and requires separate protection if you need coverage against bodily injury claims. This distinction matters because injuries to workers or visitors on your site create a coverage gap under your builders risk policy. Additionally, coverage for materials stored at off-site locations or in transit carries sub-limits that may not match your actual exposure. A policy might limit off-site storage coverage to $50,000 when you stage $200,000 worth of materials at a warehouse. The gap between your actual property value and the coverage limit becomes your responsibility.

Defective Work and Equipment Failures

Defective workmanship and faulty design work are excluded from standard policies, meaning if a subcontractor installs materials incorrectly and those materials subsequently fail or require replacement, your builders risk policy will not cover the cost of corrective work. Some policies include an ensuing loss provision that covers damage caused by faulty work, but this is not standard. You need to ask your agent specifically whether your policy includes this provision and understand the exact conditions under which it applies.

Normal wear and tear, rust, corrosion, and mechanical breakdowns are also excluded, creating situations where gradual deterioration or equipment malfunction falls outside your coverage even if the equipment sits on your job site. These exclusions mean that equipment that fails due to age or lack of maintenance receives no protection under your builders risk policy, regardless of when the failure occurs during your construction schedule.

Final Thoughts

Builders risk coverage protects your construction investment from real financial damage, and the Dallas area’s weather patterns, material theft risks, and project complexities make this protection non-negotiable for contractors managing any significant build. The most expensive mistake contractors make is assuming their general liability policy covers property damage to their own materials and structures-it does not. A second costly error involves purchasing coverage without understanding sub-limits for soft costs, off-site storage, and debris removal, which creates situations where damage occurs, claims are filed, and coverage is denied because the specific peril or property type fell outside your actual protection.

Working with an insurance agent who understands construction projects in Texas matters significantly because your agent should ask detailed questions about your project timeline, material staging locations, security measures, prior claims history, and whether you need coverage extensions for flood or earthquake exposure. Your agent should explain exactly what your builders risk policy guide covers and what it excludes in plain language, not industry jargon. They should compare quotes from multiple carriers because premium costs vary substantially based on how different insurers assess your specific risk profile.

Contact Brooks Cannon Insurance Group to discuss your project details and receive quotes from multiple carriers-most quotes arrive within 24 hours, and binding coverage can occur within 48 hours. Your builders risk protection is only useful if you act on it before materials arrive on your job site and damage strikes.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation